Capital Gains Tax in Japan (2026): Rates, Rules & Foreigner Guide

Does Japan have capital gains tax? Yes — Japan taxes capital gains on stocks at a flat 20.315%, real estate at 20.315–39.63% depending on holding period, and crypto at up to 55% (with a 2026 reform expected to cut it to ~20%). Here’s exactly how it works for foreign residents.

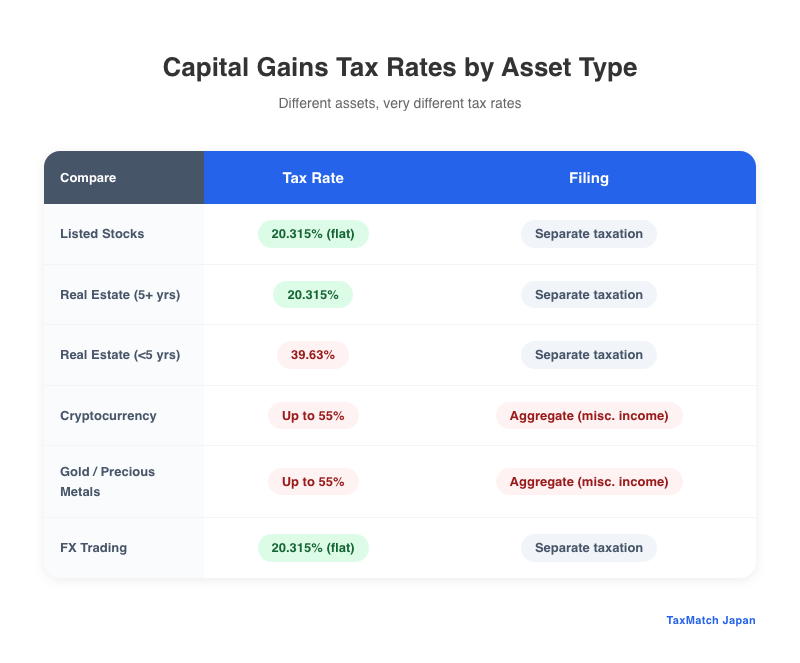

Capital Gains Tax Rates: Different assets, very different rates

Quick Summary: Capital Gains Tax in Japan

- Listed stocks & ETFs: Flat 20.315% (separate from salary — not progressive)

- Real estate: 39.63% if held ≤5 years, 20.315% if held >5 years

- Crypto (until 2025): Up to 55% as miscellaneous income — 2026 reform may cut to ~20%

- Residency matters: Non-Permanent Residents (≤5 years) are only taxed on gains remitted to Japan

- Exit tax: If you have ¥100M+ in financial assets and leave Japan, unrealized gains may be taxed

Need help with investment taxes in Japan? We’ll match you with a bilingual tax accountant — free.

Table of Contents

- How Residency Status Affects Your Tax

- Listed Stocks, ETFs & Mutual Funds

- Real Estate Capital Gains

- Cryptocurrency (2025 Rules & 2026 Reform)

- Tax-Free Accounts: NISA

- iDeCo: Tax Benefits & Gains Treatment

- The Exit Tax: Leaving Japan with Assets

- Avoiding Double Taxation

- Reporting Requirements & Common Mistakes

- FAQ

How Residency Status Affects Your Tax

The scope of what Japan can tax depends entirely on how long you’ve lived here:

| Tax Residency | Definition | What Capital Gains Are Taxed |

|---|---|---|

| Non-Resident | Lived in Japan <1 year | Japan-sourced gains only (e.g., Japanese real estate) |

| Non-Permanent Resident (NPR) | Foreign national, ≤5 years in Japan (within past 10 years) | Japan-sourced gains + overseas gains remitted to Japan |

| Permanent Resident (tax) | >5 years in Japan (within past 10 years) | Worldwide capital gains — everything, everywhere |

The NPR Remittance Trap

If you’re an NPR with overseas gains, using a foreign credit card in Japan counts as “remitting” funds — potentially triggering tax on your offshore income. The NTA doesn’t let you choose which funds you’re bringing in. They apply a strict mathematical order: current-year foreign income is deemed remitted first.

Post-Arrival Stock Purchases Are NOT Protected

The NPR remittance exemption only applies to assets acquired before you moved to Japan. If you buy foreign stocks in an overseas brokerage after becoming a Japanese resident, gains on those purchases are taxable in Japan immediately — even if the money stays offshore.

Our bilingual tax accountants handle capital gains, RSU, and crypto tax for foreign residents.

Get Matched with an Investment Tax Specialist →

Free matching · No obligation · English support

Listed Stocks, ETFs & Mutual Funds

Capital gains on listed securities are taxed at a flat 20.315% — separate from your salary income:

| Tax Component | Rate |

|---|---|

| National income tax | 15% |

| Reconstruction surtax | 0.315% (15% × 2.1%, through 2037) |

| Local resident tax | 5% |

| Total | 20.315% |

Key benefits of this system:

- Loss offset: Stock losses can offset dividend income from listed shares and interest from specified bonds

- Loss carryforward: Unused losses can be carried forward for 3 years

- Specified accounts (Tokutei Koza): Japanese brokerages can auto-calculate and withhold the 20.315%, so you may not need to file

Unlisted/private shares: Also taxed at 20.315%, but losses from unlisted shares cannot offset gains from listed shares. They’re ring-fenced.

Real Estate Capital Gains

Japan taxes real estate gains separately, with a massive difference based on how long you’ve owned the property:

| Holding Period | Tax Rate | Breakdown |

|---|---|---|

| Short-term (≤5 years as of Jan 1 of sale year) | 39.63% | 30% national + 0.63% surtax + 9% local |

| Long-term (>5 years as of Jan 1 of sale year) | 20.315% | 15% national + 0.315% surtax + 5% local |

The January 1st Rule

The 5-year clock is measured as of January 1 of the year you sell — not from your actual purchase date. If you bought on December 1, 2020, and sell on February 1, 2026, it’s only 5 years as of Jan 1, 2026 — still short-term (39.63%). You’d need to sell in 2027 (Jan 1, 2027 = 6+ years) for the long-term rate.

Primary residence exemption: If you sell your main home, you can exclude up to ¥30 million of the gain from tax, regardless of holding period. For homes held 10+ years, gains above ¥30M (up to ¥60M) are taxed at a reduced rate of ~14.21%.

Non-residents selling Japanese property: The buyer must withhold 10.21% of the gross sale price and remit it to the NTA. You’ll need to file a return to claim any overpayment back.

Cryptocurrency (2025 Rules & 2026 Reform)

Through 2025: Crypto gains are taxed as miscellaneous income at progressive rates up to 55%. Losses cannot offset other income or be carried forward. (See our detailed Crypto Tax guide.)

2026 reform (proposed): Crypto may be reclassified as a “financial product,” bringing it under the flat ~20% separate taxation rate — with 3-year loss carryforward. Not yet law; expected to apply from the 2027 tax year if passed.

Important Caveat

The proposed 20% rate will likely only apply to tokens that meet a “wealth-building” standard (think Bitcoin, Ethereum). Speculative meme coins and obscure DeFi tokens may remain under the 55% miscellaneous income regime.

Tax-Free Accounts: NISA

Japan’s NISA (Nippon Individual Savings Account) lets foreign residents invest tax-free on both capital gains and dividends:

- Capital gains and dividends within NISA are permanently tax-free

- Lifetime contribution limit: ¥18 million

- Available to any resident with a My Number Card

- Two tiers: Tsumitate (regular savings, ¥1.2M/year) and Growth (lump sum, ¥2.4M/year)

US Citizens: NISA Is a Tax Trap

The IRS does not recognize NISA as tax-advantaged. Japanese mutual funds inside NISA are classified as PFICs (Passive Foreign Investment Companies), which face punitive US tax treatment. US citizens should generally avoid Japanese mutual funds and only hold individual stocks or US-domiciled ETFs in NISA.

iDeCo: Tax Benefits & Investment Gains Treatment

iDeCo (individual Defined Contribution pension) is one of the most powerful tax tools available to foreign residents in Japan. Here’s how investment gains inside iDeCo are treated:

| Tax Benefit | Detail |

|---|---|

| Contributions | Fully tax-deductible from your income (reduces income tax + resident tax) |

| Investment gains | 100% tax-free while inside iDeCo — no capital gains tax on growth |

| Withdrawal (lump sum) | Taxed as retirement income (退職所得) with generous deductions: ¥400K/year for first 20 years, ¥700K/year after |

| Withdrawal (annuity) | Taxed as public pension income with separate deduction |

Contribution limits (2026):

- Company employees without corporate pension: ¥23,000/month (¥276,000/year)

- Self-employed / freelancers: ¥68,000/month (¥816,000/year)

- Company employees with corporate pension: ¥20,000/month (2024 reform expanded this)

For foreign residents planning to leave Japan:

- If you contributed for ≤5 years: eligible for lump-sum withdrawal (脱退一時金)

- If you contributed for >5 years: funds are locked until age 60, even after leaving Japan

- Investment gains earned during your Japan residency remain tax-free inside iDeCo

iDeCo vs. NISA for Foreign Residents

NISA offers more flexibility (withdraw anytime), but iDeCo gives a larger tax benefit through the income deduction. If you plan to stay in Japan long-term, maxing out iDeCo first is generally more tax-efficient. If you might leave within 5 years, NISA is safer since there’s no lock-up period.

The Exit Tax: Leaving Japan with Assets

If you’re a long-term foreign resident planning to leave Japan, the Exit Tax (国外転出時課税) may apply.

It applies if both conditions are met:

- You’ve lived in Japan >5 years (within past 10 years) on a Table 2 visa (Permanent Resident, Spouse of Japanese National, etc.)

- Your financial assets (stocks, funds, derivatives — not real estate or cash) total ¥100 million+

If triggered, Japan taxes the unrealized gains on your portfolio at 15.315% — even though you haven’t sold anything.

Deferral is possible: You can defer payment for up to 5 years (extendable to 10) by posting collateral and appointing a Tax Agent in Japan. If the assets decline in value after you leave, you can petition for a recalculation.

Table 1 visa holders (standard work visas like Engineer/Specialist) are generally exempt from the exit tax, even if they exceed the ¥100M threshold. The exit tax primarily targets holders of long-term relationship-based visas.

Avoiding Double Taxation

If you’re taxed on the same capital gain by both Japan and another country, you can claim a Foreign Tax Credit on your Japanese return.

Japan has tax treaties with 80+ countries. The credit is calculated as:

Credit limit = Japanese tax × (Foreign-source income / Total worldwide income)

Excess credits can be carried forward for 3 years.

US citizens: You’ll need to coordinate with both a Japanese zeirishi and a US CPA. Japan generally gets primary taxing rights as the country of residence, and you claim a Foreign Tax Credit on your US return (Form 1116).

Reporting Requirements & Common Mistakes

Filing deadline: February 16 – March 16, 2026 (for 2025 gains)

Overseas Asset Report: If you’re a Permanent Resident with overseas assets exceeding ¥50 million (gross, not net of debt), you must file a declaration by June 30. Failing to file can extend the audit statute of limitations from 5 to 8 years.

Top mistakes foreign investors make:

| Mistake | Reality |

|---|---|

| “My overseas brokerage is invisible to the NTA” | Japan uses CRS — your account data is automatically shared by 100+ countries |

| “I bought stocks after moving here, but the money’s still offshore” | Post-arrival purchases = taxable regardless of where the funds are |

| “I only used my US credit card, not a bank transfer” | Credit card use in Japan = remittance under NTA rules |

| “Crypto isn’t taxable until I cash out to yen” | Every swap, spend, and reward receipt is a taxable event |

| “I subtracted my mortgage from my overseas asset valuation” | The ¥50M threshold uses GROSS value — debts are irrelevant |

Frequently Asked Questions

Does Japan have capital gains tax?

Yes. Japan taxes capital gains on listed stocks and ETFs at a flat 20.315%, real estate at 20.315–39.63% depending on holding period, and cryptocurrency at progressive rates up to 55% (with reform expected in 2026–2027 to reduce this to ~20%).

What is the capital gains tax rate in Japan?

The standard rate for listed securities is 20.315% (15% income tax + 0.315% surtax + 5% resident tax). Real estate held over 5 years is also 20.315%, but property sold within 5 years is taxed at 39.63%. Crypto is currently taxed as miscellaneous income at rates from 5% to 55%.

Are foreigners exempt from capital gains tax in Japan?

No, but the scope depends on residency status. Non-Permanent Residents (in Japan ≤5 years) are only taxed on Japan-sourced gains and overseas gains remitted to Japan. After 5 years, you’re taxed on worldwide capital gains.

Are investment gains inside iDeCo taxed in Japan?

No — investment gains (capital gains and dividends) inside iDeCo grow completely tax-free. You only pay tax when you withdraw, and retirement income deductions significantly reduce the tax burden. Contributions are also fully tax-deductible.

Do I need to report overseas investments to the Japanese tax office?

Yes. If you’re a tax-permanent resident (>5 years) with overseas assets exceeding ¥50 million, you must file an Overseas Asset Report by June 30 each year. Japan also receives automatic account information from 100+ countries through CRS (Common Reporting Standard).

Get Expert Help with Investment Taxes

Need a Tax Accountant Who Understands Investments?

TaxMatch Japan connects you with bilingual tax professionals experienced in stocks, real estate, crypto, and cross-border capital gains — completely free matching.

We typically respond within 24 hours.

Disclaimer

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax rates, thresholds, and rules are subject to change. The 2026 crypto reform and minimum tax provisions described here reflect our understanding as of early 2026. Always consult a qualified tax professional (税理士) for your specific situation. TaxMatch Japan is a matching service and does not provide tax advice directly.