Consumption Tax & Invoice System in Japan for Foreign Business Owners (2026) | TaxMatch Japan

If you run a business or freelance in Japan, consumption tax (消費税 / shouhizei) is one of those things you can’t afford to get wrong. Since the Qualified Invoice System (インボイス制度) launched in October 2023, the rules have gotten more complex — and more consequential. Miss a registration deadline, format an invoice incorrectly, or miscalculate your cross-border obligations, and you could lose clients, face penalties, or overpay by hundreds of thousands of yen. This guide explains everything foreign business owners and freelancers need to know in 2026.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Consumption tax rules are subject to frequent legislative amendments. Always consult a qualified tax professional (税理士 / zeirishi) for advice specific to your situation.

Need a bilingual tax accountant? Get matched with a consumption tax specialist — free.

Do you need to register for consumption tax?

Table of Contents

- What Is Consumption Tax?

- Are You Required to Register?

- The Qualified Invoice System (インボイス制度)

- Transitional Relief Schedule

- Simplified Taxation Options

- Cross-Border Transactions

- Consumption Tax + Withholding Tax Interaction

- Practical Scenarios

- Common Mistakes (And How to Avoid Them)

- When to Hire a Tax Accountant

- Frequently Asked Questions

1. What Is Consumption Tax?

Japan’s consumption tax (消費税 / shouhizei) is a value-added tax (VAT) applied at every stage of the supply chain. If you’re from the US, think of it as fundamentally different from sales tax — it’s not just charged once at the point of sale. If you’re from the EU or UK, it works much like VAT, but with its own quirks.

The Two Rates

| Rate | Breakdown | Applies To |

|---|---|---|

| 10% (standard) | National 7.8% + Local 2.2% | Most goods and services |

| 8% (reduced) | National 6.24% + Local 1.76% | Food & beverages (excl. dining out & alcohol), newspaper subscriptions (2+ per week) |

How It Differs from US Sales Tax

In the US, sales tax is a single-stage tax collected only when the final consumer buys something. Japan’s consumption tax is a multi-stage tax. Every business in the supply chain charges it on sales and claims credits for the tax paid on purchases. Only the final consumer truly bears the cost.

Example: A manufacturer sells materials to a retailer for 1,100 yen (1,000 + 100 JCT). The retailer sells the finished product to a customer for 2,200 yen (2,000 + 200 JCT). The retailer owes 200 yen in output tax but claims 100 yen as input tax credit, so they remit only 100 yen to the government. The customer paid 200 yen total. The government collected 200 yen total (100 from the manufacturer + 100 from the retailer).

How It Differs from EU VAT

The mechanism is similar to EU VAT, but with key differences:

- Japan has only two rates (10% and 8%), compared to the EU’s multiple reduced rates

- Japan’s registration threshold is based on taxable sales, not total revenue

- The Qualified Invoice System is relatively new (October 2023) — before that, Japan used a simpler bookkeeping-based system

- Unlike many EU countries, Japan does not offer a quick VAT refund mechanism for newly registered businesses

Tip

Japan’s consumption tax is sometimes abbreviated as JCT (Japanese Consumption Tax) in English-language business contexts. You may also see it referred to as shouhizei (消費税) in Japanese documents.

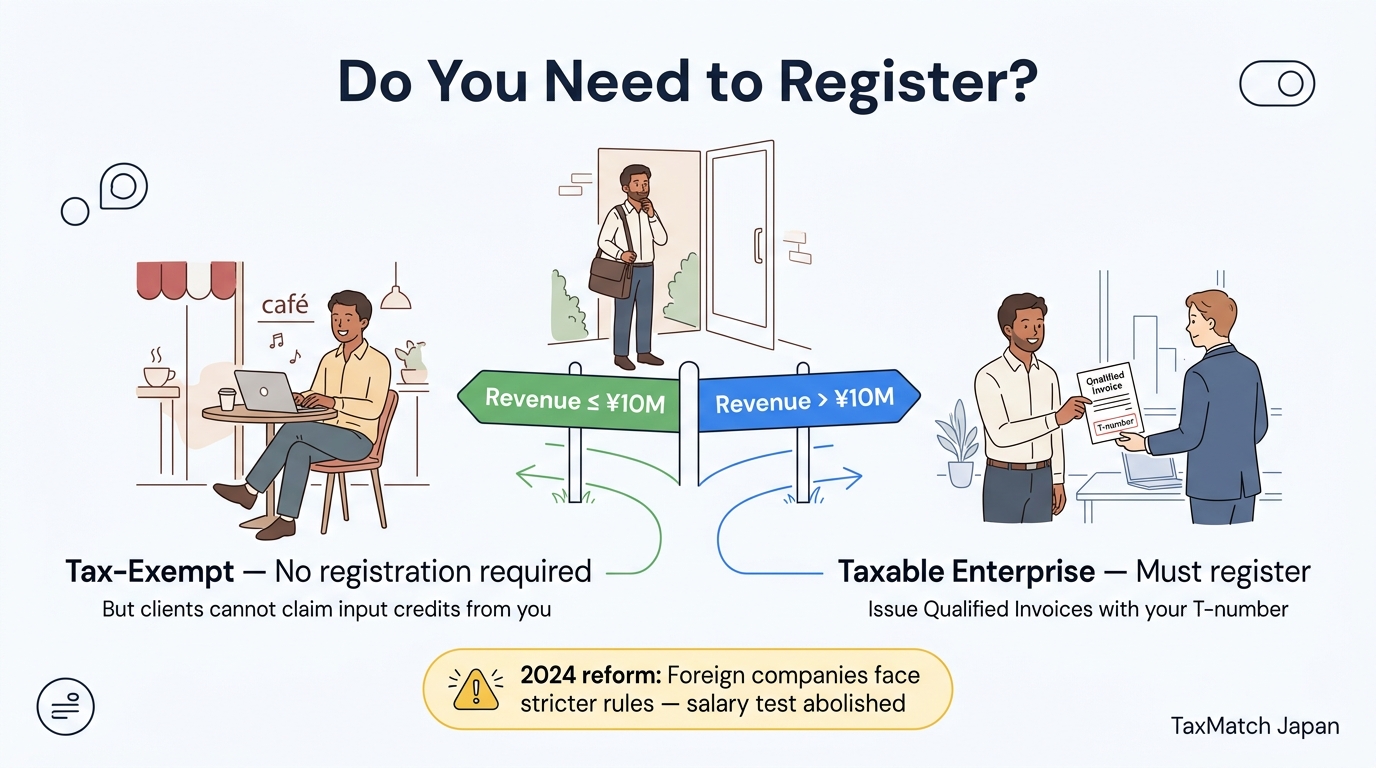

2. Are You Required to Register?

Not every business in Japan needs to charge and remit consumption tax. The key factor is your taxable sales volume.

The 10 Million Yen Threshold

You become a taxable enterprise (課税事業者 / kazei jigyousha) — meaning you must charge, collect, and remit consumption tax — if your taxable sales exceed 10,000,000 yen in the base period (基準期間 / kijun kikan).

What is the base period?

- Sole proprietors: The calendar year two years prior (e.g., for 2026, the base period is January-December 2024)

- Corporations: The fiscal year two years prior (e.g., for a corporation with a March fiscal year, the base period for FY ending March 2027 is FY ending March 2025)

If your taxable sales in the base period were 10 million yen or less, you are an exempt enterprise (免税事業者 / menzei jigyousha) and are not required to charge consumption tax.

The Specified Period Test

Even if your base period sales were under 10 million yen, you may still be required to register based on the specified period (特定期間 / tokutei kikan):

- Sole proprietors: January 1 – June 30 of the previous year

- Corporations: The first 6 months of the previous fiscal year

If both taxable sales AND salary payments exceed 10 million yen during the specified period, you become a taxable enterprise. You can use either taxable sales or salary payments for this test — if one is under 10 million, you remain exempt.

2024 Reform: Foreign Enterprise Rule Change

Warning

Starting from fiscal years beginning on or after October 1, 2024, foreign enterprises (those with no domestic office in Japan) can no longer use the salary payment alternative for the specified period test. Only the taxable sales criterion applies. This means more foreign businesses may be caught by the specified period test than before.

Newly Established Corporations

A newly established corporation has no base period for its first two fiscal years, so it would normally be exempt. However, if the corporation’s paid-in capital is 10 million yen or more at the time of establishment, it is treated as a taxable enterprise from day one.

Voluntary Registration

Even if you’re under the threshold, you may choose to voluntarily register as a taxable enterprise. Why would you? Two main reasons:

- Your clients require qualified invoices — under the new invoice system, your business clients can only claim input tax credits if you issue qualified invoices, which requires registration

- You want to claim refunds on purchases — if you buy expensive equipment or have large input costs, registration lets you claim input tax credits, potentially resulting in a refund

Section Summary

- Taxable sales over 10 million yen in the base period (2 years prior) = mandatory registration

- Specified period test (first 6 months of prior year) can also trigger registration

- Foreign enterprises lost the salary alternative for specified period testing from October 2024

- Voluntary registration is possible and sometimes advantageous

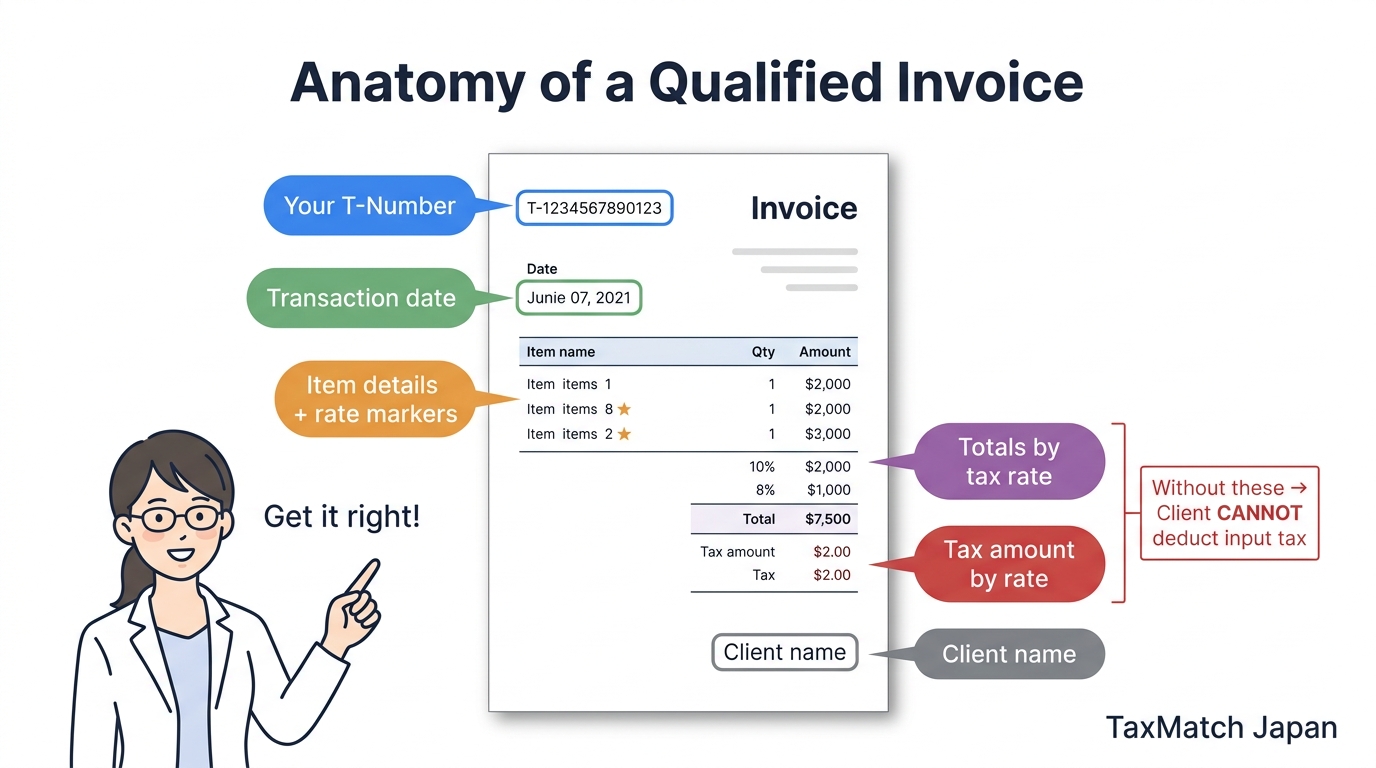

3. The Qualified Invoice System (インボイス制度)

Anatomy of a Qualified Invoice — Get it right!

Since October 1, 2023, Japan has required qualified invoices (適格請求書 / tekikaku seikyuusho) for businesses to claim input tax credits. This was a major change from the old “account-based” system where any invoice would do.

What Does This Mean for You?

If you’re a taxable enterprise and want your business clients to be able to deduct the consumption tax on your invoices, you must:

- Register as a Qualified Invoice Issuer (適格請求書発行事業者) with the tax office

- Receive a T-number (registration number starting with “T” followed by 13 digits)

- Include all required elements on every invoice you issue

How to Register

Submit the Application for Registration as Qualified Invoice Issuer (適格請求書発行事業者の登録申請書) to your jurisdictional tax office. You can file via e-Tax or on paper. Processing typically takes 2-4 weeks.

Your T-number is publicly searchable on the National Tax Agency’s website, so your clients can verify your registration.

What a Qualified Invoice Must Contain

A qualified invoice must include all six of the following elements:

| # | Required Element | Notes |

|---|---|---|

| 1 | Name and T-number of the invoice issuer | T + 13-digit number (e.g., T1234567890123) |

| 2 | Date of the transaction | Date goods were delivered or services rendered |

| 3 | Description of goods or services | Must clearly identify what was sold, with applicable tax rate indicated per item |

| 4 | Tax-rate-separated totals | Separate subtotals for 10% and 8% items |

| 5 | Consumption tax amount per rate | The exact yen amount of tax at each rate (fractions rounded per invoice) |

| 6 | Name of the recipient | The business receiving the invoice |

Tip

For retail and similar businesses, a Simplified Invoice (適格簡易請求書) is permitted. It omits the recipient’s name and allows showing either the tax amount or the tax rate (instead of both). This applies to retail, food service, taxi, parking, and similar businesses that issue receipts to unspecified customers.

If You’re an Exempt Enterprise

If you’re under the 10 million yen threshold and remain an exempt enterprise, you cannot issue qualified invoices. This means your B2B clients cannot claim input tax credits on your invoices. For some freelancers and small businesses, this creates pressure to register voluntarily — even though you’d then have to charge and remit consumption tax.

The transitional relief schedule (covered in the next section) softens this impact through 2031.

4. Transitional Relief Schedule

To ease the transition to the Qualified Invoice System, the government introduced a phase-out schedule. Even when buying from non-registered (exempt) enterprises, purchasers can still claim a partial input tax credit during the transitional period:

| Period | Claimable % | Effective Cost Increase for Buyer |

|---|---|---|

| Oct 2023 – Sep 2026 | 80% | ~2% (only 20% of the 10% tax is non-creditable) |

| Oct 2026 – Sep 2028 | 50% | ~5% |

| Oct 2028 – Sep 2029 | 50% | ~5% |

| Oct 2029 – Sep 2030 | 50% | ~5% |

| Oct 2030 – Sep 2031 | 30% | ~7% |

| Oct 2031 onwards | 0% | Full 10% — no credit at all |

What this means in practice: If you’re a freelance designer who hasn’t registered for the invoice system, your corporate clients are currently losing only about 2% by working with you (they can claim 80% of the input tax). But from October 2026, that cost jumps to 5%. By October 2031, they lose the entire 10% — which creates real pressure for them to switch to registered suppliers.

Warning

October 2026 is a critical deadline. The jump from 80% to 50% creditability is the largest single step in the transition schedule. If you’re an exempt enterprise selling primarily to businesses, expect increased pressure to register around this date. Start planning now.

The 20% Rule (2-Wari Tokureii) — Sunsetting

For businesses that voluntarily registered as invoice issuers despite being under the 10 million yen threshold, there’s a special relief measure: the “2-wari” special rule (2割特例). Under this rule, your consumption tax liability is simply 20% of your output tax (i.e., you’re deemed to have input tax credits of 80%).

This rule is available for taxable periods starting through December 31, 2026. After that, it sunsets, and you’ll need to use either the standard method or the simplified taxation system.

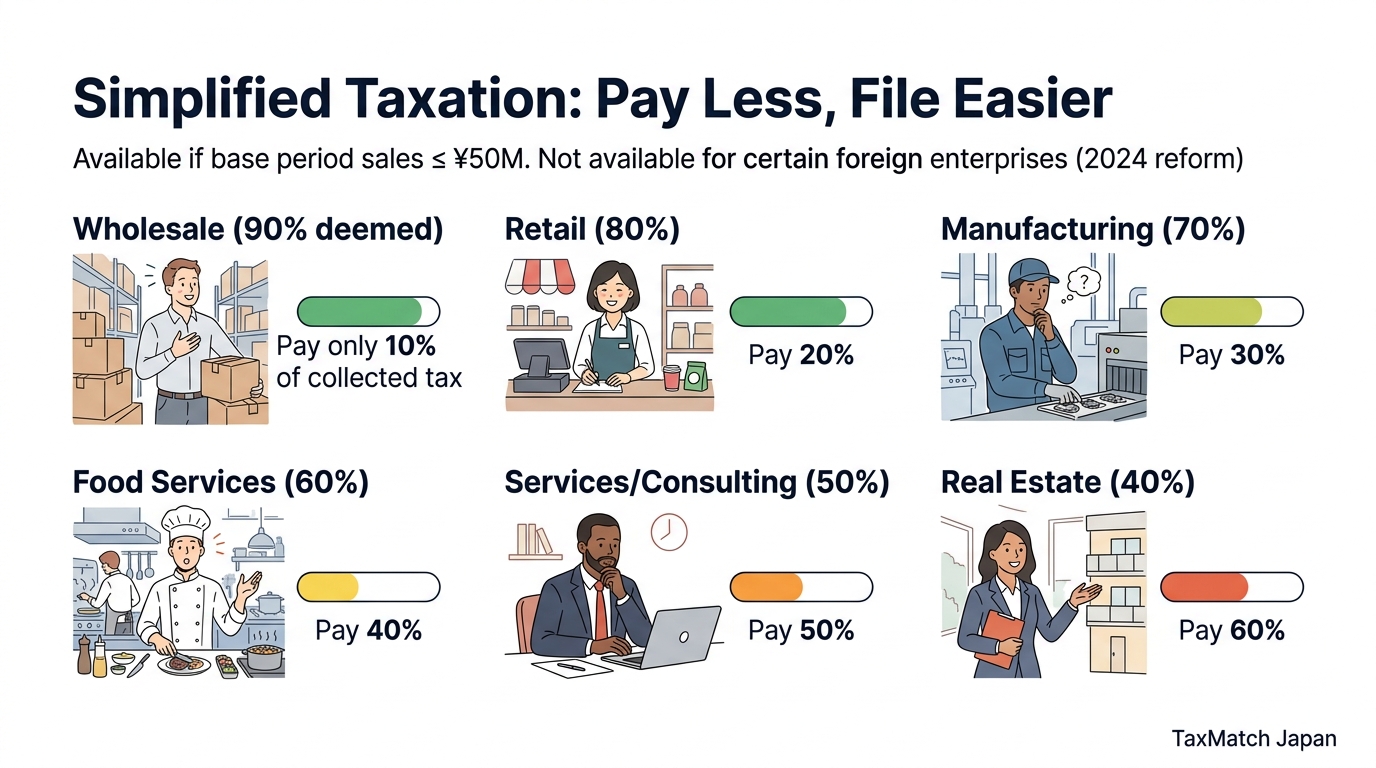

5. Simplified Taxation Options

Simplified Taxation: Pay less, file easier

Calculating actual input tax credits requires tracking every purchase with proper invoices. For smaller businesses, Japan offers a Simplified Taxation System (簡易課税制度 / kani kazei seido) that replaces actual input credits with a deemed purchase rate based on your industry.

Eligibility

You can use simplified taxation if your taxable sales in the base period were 50 million yen or less. You must submit an election form (消費税簡易課税制度選届出書) by the last day of the fiscal year before the year you want to apply it.

Deemed Purchase Rates by Industry

| Type | Industry | Deemed Rate | Effective Tax |

|---|---|---|---|

| Type 1 | Wholesale | 90% | 1% of sales |

| Type 2 | Retail | 80% | 2% of sales |

| Type 3 | Manufacturing, Construction | 70% | 3% of sales |

| Type 4 | Food Service, Other | 60% | 4% of sales |

| Type 5 | Services, Consulting, IT | 50% | 5% of sales |

| Type 6 | Real Estate Rental | 40% | 6% of sales |

Example: You’re a freelance IT consultant (Type 5) with 12 million yen in annual taxable sales. Under simplified taxation:

- Output tax: 12,000,000 × 10% = 1,200,000 yen

- Deemed input credit: 1,200,000 × 50% = 600,000 yen

- Tax payable: 600,000 yen (5% of sales)

If your actual expenses are low (as is common for service businesses), the standard method might result in a higher tax bill because your real input tax credits are less than 50% of output tax. Simplified taxation can be a significant advantage.

Special 30% Calculation for Sole Proprietors (2027-2028)

Tip

For taxable periods from January 2027 through December 2028, sole proprietors who newly become taxable enterprises (due to invoice registration) can use a special calculation: if 30% or more of their total sales come from a single industry type, they can apply that industry’s deemed rate to all sales — even if they have revenue from multiple industry types. This simplifies the calculation significantly for newly registered freelancers with mixed income streams.

6. Cross-Border Transactions

This is where things get especially relevant for foreign business owners. Japan’s consumption tax treatment of cross-border transactions depends on the direction, type, and parties involved.

Export Exemption (輸出免税)

Goods and services exported from Japan are generally zero-rated (taxed at 0%). This means:

- You don’t charge consumption tax to overseas customers

- You can still claim input tax credits on your domestic purchases

- This can result in a net refund — the government refunds the input tax you paid because your output tax is zero

Export evidence required: Customs declaration forms (for goods), contracts proving the service is provided to a non-resident for consumption outside Japan (for services).

B2B Reverse Charge (リバースチャージ)

When a Japanese business purchases certain services from a foreign enterprise with no office in Japan, the reverse charge mechanism applies. Instead of the foreign seller charging JCT, the Japanese buyer self-assesses and remits the consumption tax.

This applies to “specified services provided by enterprises” (事業者向け電気通信利用役務の提供) — essentially B2B digital services like cloud computing, SaaS, online advertising, and similar services.

B2C Digital Services

For digital services sold to Japanese consumers (B2C), the foreign service provider must register and remit Japanese consumption tax if they have significant Japanese sales. This includes streaming services, digital downloads, online courses, and similar offerings.

Foreign providers can register under the simplified registration system for foreign digital service providers, which has fewer administrative requirements than standard registration.

2026 Platform Taxation Reform

Warning: New Rule from April 2025

Japan is introducing platform taxation (プラットフォーム課税) for digital services. Under this reform, digital platforms with annual Japanese B2C digital service sales exceeding 5 billion yen become the deemed seller for consumption tax purposes. The platform — not the individual seller — is responsible for charging and remitting the consumption tax.

This affects foreign sellers on major platforms like app stores, digital marketplaces, and streaming platforms. If your platform handles JCT on your behalf, you do NOT separately charge consumption tax on those sales.

Low-Value Goods Import Reform

Previously, imported goods valued at 10,000 yen or less were exempt from consumption tax. This exemption is being abolished as part of ongoing reforms. All imported goods will be subject to consumption tax regardless of value, aligning Japan’s rules with similar reforms in the EU and other jurisdictions.

Tax Agent Requirement

If you are a foreign enterprise with no domicile, residence, or office in Japan, you must appoint a tax agent (納税管理人 / nouzei kanrinin) who resides in Japan. This agent handles your tax filings and receives correspondence from the tax office on your behalf.

Cross-border tax is complex. A bilingual tax accountant who handles international clients can help you avoid costly errors. Get matched free →

7. Consumption Tax + Withholding Tax Interaction

This is one of the most confusing areas for foreign freelancers and consultants in Japan. When you provide certain services to Japanese businesses, your client may be required to withhold income tax from your payment — and this interacts with consumption tax in ways that trip up many people.

The 20.42% Withholding Rate

For non-employee service fees (freelance, consulting, etc.) paid to individuals, the payer must withhold:

- 10.21% on payments up to 1,000,000 yen per transaction

- 20.42% on the portion exceeding 1,000,000 yen

For non-residents, the withholding rate is generally a flat 20.42% on the entire amount.

JCT-Inclusive vs. JCT-Exclusive Invoicing

Here’s the critical question: is withholding tax calculated on the amount before or after consumption tax?

The answer depends on how your invoice is formatted:

| Invoice Format | Withholding Base | Example (100,000 yen fee) |

|---|---|---|

| JCT shown separately on invoice | Withholding on pre-tax amount only | Withholding: 100,000 × 10.21% = 10,210 yen |

| JCT included (total shown as one amount) | Withholding on full amount including JCT | Withholding: 110,000 × 10.21% = 11,231 yen |

Tip

Always show consumption tax separately on your invoices. This reduces the withholding base and puts more cash in your pocket upfront. The withheld amount is an advance payment of your income tax (credited at filing), so minimizing it improves your cash flow throughout the year.

Full Invoice Example

A freelance consultant bills 500,000 yen for services plus 50,000 yen JCT (10%), with JCT shown separately:

| Item | Amount |

|---|---|

| Consulting fee | 500,000 yen |

| Consumption tax (10%) | 50,000 yen |

| Subtotal | 550,000 yen |

| Withholding tax (10.21% of 500,000) | -51,050 yen |

| Amount due | 498,950 yen |

8. Practical Scenarios

Let’s walk through four common situations that foreign business owners and freelancers face.

Scenario A: Freelance Web Developer Earning 8 Million Yen

Profile: American on a Business Manager visa, sole proprietor, annual revenue of 8,000,000 yen from Japanese clients, base period revenue was 6,000,000 yen (under 10M threshold).

Question: Does she need to register for consumption tax?

Answer: Her base period revenue (6M yen) is under the 10M threshold, so she is not required to register. However, she should consider:

- Her B2B clients may prefer working with registered invoice issuers

- If she voluntarily registers, she can use the simplified taxation (Type 5, 50% deemed rate), meaning her tax would be 8,000,000 × 10% × 50% = 400,000 yen

- If she uses the 2-wari special rule (available through 2026), her tax would be 8,000,000 × 10% × 20% = 160,000 yen

- She could potentially raise prices by 10% to offset the tax burden

Scenario B: Foreign Consultant with Mixed Clients

Profile: British consultant, registered taxable enterprise, 15,000,000 yen from Japanese B2B clients, 5,000,000 yen from UK clients (remote services).

Analysis:

- Japanese B2B revenue: Subject to 10% consumption tax → output tax of 1,500,000 yen

- UK client revenue: Export exempt (zero-rated) → output tax of 0 yen

- Total output tax: 1,500,000 yen

- Input tax credits on domestic expenses (office, equipment, software): estimated 300,000 yen

- Tax payable: 1,200,000 yen

The export portion is zero-rated, so input credits related to export sales contribute to reducing his overall tax liability. This makes registration advantageous when you have significant export revenue.

Scenario C: E-Commerce Seller

Profile: Korean entrepreneur selling handmade goods from Japan to customers worldwide via Shopify, annual revenue 12,000,000 yen (7M domestic, 5M international).

Analysis:

- Base period revenue exceeded 10M yen → mandatory registration

- Domestic sales: 10% JCT applies

- International sales: Export exempt (zero-rated), but must maintain customs documentation

- Can claim input credits on materials, shipping supplies, etc.

- The export portion may generate a refund after offsetting input credits

Scenario D: Digital Service Provider

Profile: Indian SaaS company (no Japan office) selling subscription software to Japanese businesses and consumers, annual Japan revenue 30,000,000 yen.

Analysis:

- B2B sales: Reverse charge applies — the Japanese business clients self-assess JCT. The Indian company does not charge JCT on B2B invoices.

- B2C sales: The Indian company must register and remit JCT on sales to Japanese consumers (or the platform handles it under the 2026 platform taxation rules)

- Must appoint a tax agent (納税管理人) in Japan

- Can use the simplified registration system for foreign digital providers

9. Common Mistakes (And How to Avoid Them)

Mistake 1: Miscalculating the Base Period

The problem: A sole proprietor checks their 2025 revenue to determine 2026 obligations, when they should be checking 2024 (the year two years prior).

Why it happens: The “two years prior” rule is counterintuitive. Many foreigners assume the previous year’s revenue determines their current obligations.

The fix: For sole proprietors, always look at the calendar year ending December of two years ago. For 2026 obligations, check your 2024 taxable sales. Mark this in your calendar every November so you can plan ahead.

Mistake 2: Invoice Formatting Errors

The problem: You issue invoices that look professional but miss one of the six required elements for a qualified invoice — commonly the T-number or the tax-rate-separated totals.

Why it happens: Many foreign freelancers use invoice templates designed for other countries that don’t include Japan-specific requirements.

The fix: Use accounting software that supports Japan’s qualified invoice format (freee, MoneyForward, Yayoi), or create a template that includes all six elements. Double-check every invoice before sending.

Mistake 3: Withholding Gross-Up Failure

The problem: You quote a client “100,000 yen” for a project. The client withholds 10.21%, so you receive 89,790 yen. You expected 100,000.

Why it happens: You didn’t account for withholding when setting your price. The client is legally required to withhold, and they did it correctly — from their perspective.

The fix: When quoting prices, decide whether your fee is before or after withholding and communicate this clearly. If you want to receive 100,000 yen after withholding, you need to invoice approximately 111,374 yen (so that 111,374 × 10.21% = 11,374 withholding, and you receive 100,000).

Mistake 4: Ignoring the Specified Period Test

The problem: Your base period revenue was under 10M yen, so you assume you’re exempt. But your revenue in the first half of the prior year exceeded 10M yen.

Why it happens: Many resources only mention the base period test and skip the specified period test entirely.

The fix: Check both tests every year. If your January-June revenue of the prior year exceeds 10M yen (and for individuals, salary payments also exceed 10M), you’re a taxable enterprise regardless of the base period.

Mistake 5: Not Keeping 10% and 8% Items Separate

The problem: You sell mixed items (some at 10%, some at the reduced 8% rate) but lump them together on invoices.

Why it happens: The dual-rate system is relatively new and easy to overlook, especially for businesses that occasionally sell food or beverages alongside other goods.

The fix: Always separate 10% and 8% items on your invoices with distinct subtotals and tax amounts for each rate. Your accounting software should handle this automatically if configured correctly.

Section Summary

- Check both the base period and specified period to determine your registration status

- Ensure invoices include all six required elements for qualified invoices

- Always show JCT separately to minimize withholding impact

- Keep 10% and 8% items separate on every invoice

- Account for withholding when setting your prices

10. When to Hire a Tax Accountant

Consumption tax is one of the most technical areas of Japanese tax law, and the Qualified Invoice System has added another layer of complexity. You can handle basic compliance on your own if you have a simple domestic business with straightforward transactions. But seriously consider hiring a tax accountant (税理士) if:

- You’re approaching the 10M yen threshold and need to plan for registration timing

- You have cross-border transactions — export exemptions, reverse charge, and platform taxation rules are complex and the penalties for errors are significant

- You need to choose between standard and simplified taxation — the wrong choice can cost you hundreds of thousands of yen

- You’re a foreign enterprise with no Japan office and need a tax agent (this is legally required)

- You’re dealing with the withholding + consumption tax interaction and want to optimize your invoicing

- You’ve received a notice from the tax office about your consumption tax filing or invoice compliance

- The 2-wari special rule is sunsetting and you need to transition to simplified taxation or the standard method

Filing Deadlines

| Business Type | Consumption Tax Filing Deadline |

|---|---|

| Sole proprietor (個人事業主) | By March 31 of the following year |

| Corporation (法人) | Within 2 months of fiscal year end |

Note that the consumption tax filing deadline for sole proprietors (March 31) is different from the income tax deadline (March 15). Don’t confuse the two.

A bilingual tax accountant who specializes in consumption tax and understands the challenges foreign business owners face can save you far more than their fee — in avoided penalties, optimized tax method selection, and correct invoice compliance. See our pricing guide for typical fee ranges.

Need help with consumption tax or the invoice system? Get matched with an English-speaking tax accountant who specializes in JCT compliance — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

Do foreigners need to pay consumption tax in Japan?

As a consumer, everyone pays Japan’s 10% consumption tax (8% on food and beverages). As a business owner, you must collect and remit consumption tax if your taxable sales exceeded ¥10 million in the base period (generally 2 years prior).

What is the invoice system in Japan?

Japan’s Qualified Invoice System (tekikaku seikyusho hozonsho hoshiki), introduced in October 2023, requires businesses to issue invoices with a registered invoice number (T + 13 digits) for buyers to claim consumption tax input credits. Unregistered businesses cannot issue qualified invoices.

When do businesses need to register for consumption tax?

Registration is mandatory when taxable sales exceed ¥10 million in the base period. Voluntary registration is available for businesses below this threshold that want to issue qualified invoices, which can be important for B2B relationships where clients need input tax credits.