Japan’s dependent deduction (扶養控除 / fuyo kojo) can reduce your taxable income by up to ¥630,000 per qualifying family member — but for foreign residents, the rules around claiming overseas dependents changed dramatically in 2023. If your parents, siblings, or adult children live outside Japan, you now need specific proof that you sent them at least ¥380,000 per year, or the deduction is denied entirely. This guide explains exactly who qualifies, how much you save, and what documents you need for each category of dependent.

Income Walls: How your earnings affect deductions and insurance

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Dependent deduction rules are subject to legislative amendments and individual circumstances vary. Always consult a qualified tax professional (税理士 / zeirishi) for advice specific to your situation.

Quick Summary

- Dependent deduction reduces taxable income by ¥380,000–¥630,000 per qualifying family member

- Dependents must earn less than ¥480,000 in total income (roughly ¥1,030,000 in salary)

- Overseas dependents aged 30–69 require remittance proof of ¥380,000+ per person per year (since 2023)

- Children under 16 provide no income tax deduction but reduce resident tax

- Spouse deduction is a separate system — do not confuse with dependent deduction

Confused about which family members you can claim?

Table of Contents

- What Is the Dependent Deduction?

- Who Qualifies as a Dependent?

- Deduction Amounts by Age Bracket

- Spouse Deduction vs. Spouse Special Deduction

- Overseas Dependents: The 2023 Rule Change

- Required Documents

- Impact on Resident Tax and NHI Premiums

- Common Mistakes Foreigners Make

- How to Claim: Year-End Adjustment vs. Tax Return

- Frequently Asked Questions

1. What Is the Dependent Deduction?

The dependent deduction (扶養控除) is an income deduction that reduces your taxable income — not your tax bill directly — for each qualifying family member you financially support. It is available to all taxpayers in Japan, including foreign residents on any visa type.

Unlike the US system of “claiming dependents” on your tax return, Japan’s system uses a fixed deduction amount per dependent rather than a per-child tax credit. The deduction lowers your taxable income, which in turn reduces both your income tax (国税) and resident tax (住民税).

How Much Does It Save You?

The actual tax savings depend on your marginal tax rate:

| Your Taxable Income | Income Tax Rate | Tax Saved per ¥380,000 Deduction | Tax Saved per ¥630,000 Deduction |

|---|---|---|---|

| ¥1,950,000–¥3,300,000 | 10% | ¥38,000 | ¥63,000 |

| ¥3,300,000–¥6,950,000 | 20% | ¥76,000 | ¥126,000 |

| ¥6,950,000–¥9,000,000 | 23% | ¥87,400 | ¥144,900 |

| ¥9,000,000–¥18,000,000 | 33% | ¥125,400 | ¥207,900 |

Additionally, each dependent provides a resident tax deduction (separate amounts, covered in Section 7), saving an additional ~¥33,000–¥45,000 per dependent per year.

2. Who Qualifies as a Dependent?

To qualify as your dependent (扶養親族) for tax purposes, a family member must meet all four of the following conditions:

| Condition | Details |

|---|---|

| 1. Relationship | Must be a relative within the 6th degree of kinship (血族) or 3rd degree by marriage (姻族), OR a person who shares a household with you (事実上婚姻関係と同様の事情にある人を除く) |

| 2. Living together or supported | Must share a household with you (同居) OR receive regular financial support from you (仕送り). Overseas family qualifies if you send money regularly. |

| 3. Income threshold | Total income (合計所得金額) must be ¥480,000 or less for the year. For salary earners, this means gross salary of approximately ¥1,030,000 or less (after the employment income deduction). |

| 4. Not a business partner | Must not be a blue-return designated employee (青色事業専従者) or a white-return family business employee (白色事業専従者) who received compensation. |

Key Point: Income vs. Revenue

The ¥480,000 threshold is based on total income (所得), not gross revenue (収入). For salary earners, the employment income deduction (給与所得控除) of at least ¥550,000 means a person earning ¥1,030,000 in salary has total income of exactly ¥480,000. For self-employed family members, it is business revenue minus expenses.

Who Counts as “Family”?

Japan’s definition is broader than many Western countries:

- Parents and grandparents (lineal ascendants)

- Children and grandchildren (lineal descendants)

- Siblings

- Uncles, aunts, nephews, nieces (within 6th degree)

- In-laws (within 3rd degree — parents-in-law, siblings-in-law)

Note: Your spouse is never classified as a dependent (扶養親族). Spouses have their own separate deduction system (配偶者控除), covered in Section 4.

3. Deduction Amounts by Age Bracket

The deduction amount varies based on the dependent’s age as of December 31 of the tax year:

| Age Category | Age Range | Income Tax Deduction | Resident Tax Deduction |

|---|---|---|---|

| Young dependent (年少扶養親族) | Under 16 | ¥0 (no deduction) | ¥330,000 (for non-taxable threshold calculation only) |

| General dependent (一般扶養親族) | 16–18 | ¥380,000 | ¥330,000 |

| Specific dependent (特定扶養親族) | 19–22 | ¥630,000 | ¥450,000 |

| General dependent (一般扶養親族) | 23–69 | ¥380,000 | ¥330,000 |

| Elderly dependent — co-residing (老人扶養親族・同居) | 70+, living together | ¥580,000 | ¥450,000 |

| Elderly dependent — separate (老人扶養親族・別居) | 70+, living apart | ¥480,000 | ¥380,000 |

Why No Deduction for Children Under 16?

Japan eliminated the income tax deduction for children under 16 in 2011 when it introduced the Child Allowance (児童手当) — a direct monthly cash payment of ¥10,000–¥15,000 per child. The government decided direct payments were more equitable than tax deductions, which benefit higher earners more. However, children under 16 still count for resident tax non-taxable threshold calculations, which can eliminate your resident tax entirely if your income is low enough.

The “Specific Dependent” Bonus (Ages 19–22)

The ¥630,000 deduction for dependents aged 19–22 is significantly higher than the standard ¥380,000 because this age range typically corresponds to university attendance, when families face heavy educational costs. This is Japan’s way of providing tax relief for parents paying university tuition — a cost that averages ¥500,000–¥1,350,000 per year at national universities and up to ¥4,000,000+ at private universities.

4. Spouse Deduction vs. Spouse Special Deduction

Your spouse cannot be claimed as a “dependent” (扶養親族). Instead, Japan has two separate deduction systems for spouses:

Spouse Deduction (配偶者控除)

Available when your spouse’s total income is ¥480,000 or less (salary of ~¥1,030,000 or less):

| Your Total Income (taxpayer) | Income Tax Deduction (spouse under 70) | Income Tax Deduction (spouse 70+) |

|---|---|---|

| ¥9,000,000 or less | ¥380,000 | ¥480,000 |

| ¥9,000,001–¥9,500,000 | ¥260,000 | ¥320,000 |

| ¥9,500,001–¥10,000,000 | ¥130,000 | ¥160,000 |

| Over ¥10,000,000 | ¥0 (no deduction) | ¥0 (no deduction) |

Spouse Special Deduction (配偶者特別控除)

When your spouse earns more than ¥480,000 but less than ¥1,330,000 in total income (salary of ~¥1,030,001 to ~¥2,016,000), you can claim a gradually decreasing deduction:

| Spouse’s Total Income | Approx. Salary Equivalent | Your Deduction (if your income ≤ ¥9M) |

|---|---|---|

| ¥480,001–¥500,000 | ~¥1,030,001–¥1,050,000 | ¥380,000 |

| ¥500,001–¥550,000 | ~¥1,050,001–¥1,100,000 | ¥360,000 |

| ¥550,001–¥600,000 | ~¥1,100,001–¥1,150,000 | ¥310,000 |

| ¥600,001–¥667,000 | ~¥1,150,001–¥1,217,000 | ¥210,000 |

| ¥667,001–¥833,000 | ~¥1,217,001–¥1,383,000 | ¥160,000 |

| ¥833,001–¥900,000 | ~¥1,383,001–¥1,450,000 | ¥110,000 |

| ¥900,001–¥950,000 | ~¥1,450,001–¥1,500,000 | ¥60,000 |

| ¥950,001–¥1,000,000 | ~¥1,500,001–¥1,550,000 | ¥30,000 |

| ¥1,000,001–¥1,330,000 | ~¥1,550,001–¥2,016,000 | ¥0 (phases out entirely) |

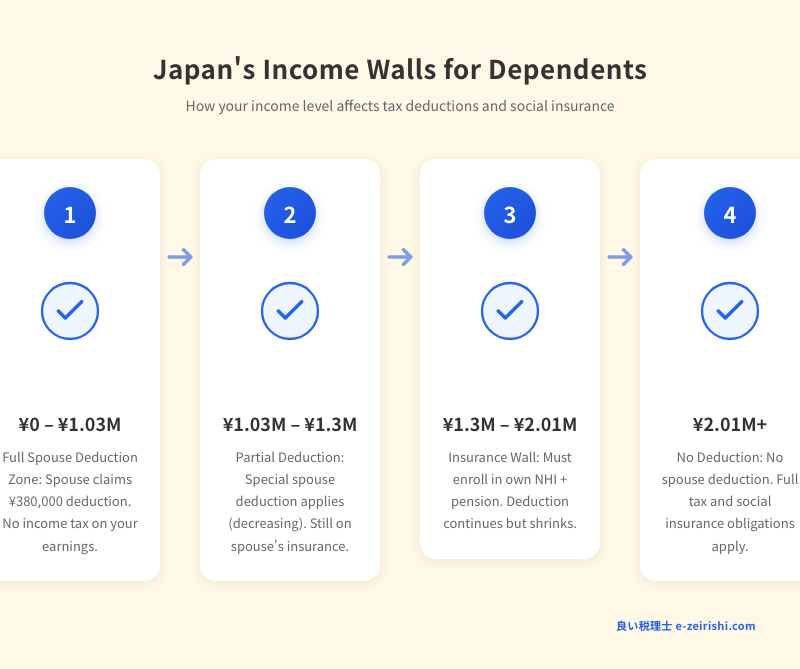

The “Income Walls” Explained

Japan’s tax system creates several thresholds — colloquially called “walls” (壁) — where a small increase in your spouse’s income can cause a disproportionately large loss in benefits:

- ¥1,030,000 wall: Above this salary, your spouse loses the full spouse deduction (配偶者控除)

- ¥1,060,000 wall: The spouse special deduction starts decreasing noticeably

- ¥1,300,000 wall: Your spouse must enroll in their own social insurance (health insurance + pension) — the biggest cost jump

- ¥2,016,000 wall: The spouse special deduction phases out entirely

5. Overseas Dependents: The 2023 Rule Change

This is the section most relevant to foreign residents in Japan. Before 2023, claiming overseas family members as dependents was relatively straightforward — and widely abused. The NTA found that some foreign residents were claiming 10+ overseas dependents with minimal documentation, significantly reducing their tax burden.

What Changed in 2023

Starting from the 2023 tax year, overseas dependents aged 30–69 face strict new requirements. They can only be claimed if they fall into one of these categories:

| Category | Who Qualifies | Documentation Required |

|---|---|---|

| A. Studying abroad | Family member studying at an overseas educational institution on a student visa | Proof of enrollment + visa documentation |

| B. Disabled | Family member with a recognized disability (障害者) | Disability certificate or equivalent documentation |

| C. Receiving ¥380,000+ in remittances | Family member to whom you sent at least ¥380,000 in the tax year for living expenses or education | Remittance receipts showing ¥380,000+ per dependent |

Warning: The ¥380,000 Must Be Per Person

If you claim three overseas siblings (all aged 30–69) as dependents, you need remittance proof of ¥380,000 each — totaling ¥1,140,000 in documented transfers. A single lump-sum transfer to one family member who then distributes the money does not satisfy this requirement. Each dependent must receive individually documented transfers.

Who Is NOT Affected by the 2023 Rule

The stricter rules apply only to overseas dependents aged 30–69. The following overseas dependents can still be claimed under the old (simpler) rules:

- Under 16: No income tax deduction anyway, but still counts for resident tax threshold

- 16–29: Standard documentation (relationship proof + remittance proof of any amount)

- 70+: Standard documentation (relationship proof + remittance proof of any amount)

6. Required Documents

Whether claiming domestic or overseas dependents, you need documentation. For overseas dependents, the requirements are significantly more stringent.

For Overseas Dependents

| Document | Purpose | Accepted Forms |

|---|---|---|

| 1. Proof of Relationship (親族関係書類) | Proves the family relationship | Birth certificate, marriage certificate, family register from home country, or notarized family tree. Must include Japanese translation. |

| 2. Proof of Remittance (送金関係書類) | Proves you financially support them | Bank transfer receipts, remittance service records (e.g., Wise, Western Union), credit card statements showing overseas payments. Must show sender, recipient, amount, and date. |

| 3. For ages 30–69: Additional proof | Proves category A, B, or C eligibility | Student visa/enrollment certificate, disability certificate, or remittance receipts totaling ¥380,000+ per dependent |

Tip: Keep Remittance Records All Year

Do not wait until tax filing season to gather remittance proof. Use a consistent method (bank wire or Wise) throughout the year so you have a clean paper trail. Cash sent informally through friends or family does not qualify as documentation. Set up recurring monthly transfers if possible — 12 monthly transfers of ¥32,000 each clearly meets the ¥380,000 threshold and is much easier to document than sporadic large transfers.

Translation Requirements

All foreign-language documents must include a Japanese translation. The translation does not need to be professionally certified — you can translate it yourself — but it must be accurate and include the translator’s name and date.

7. Impact on Resident Tax and NHI Premiums

The dependent deduction affects more than just your income tax:

Resident Tax (住民税)

Resident tax applies its own set of dependent deduction amounts (generally ¥330,000–¥450,000 per dependent, as shown in the table in Section 3). Since resident tax is a flat 10%, each dependent saves you approximately:

- General dependent (16–18, 23–69): ¥330,000 × 10% = ¥33,000 savings

- Specific dependent (19–22): ¥450,000 × 10% = ¥45,000 savings

- Elderly dependent (70+, co-residing): ¥450,000 × 10% = ¥45,000 savings

Non-Taxable Threshold for Resident Tax

Resident tax has a non-taxable threshold (非課税限度額) that increases with each dependent. In most municipalities, the formula is:

Non-taxable threshold = ¥350,000 × (number of dependents + 1) + ¥100,000 + ¥210,000

Example: A taxpayer with 3 dependents is exempt from resident tax if their total income is below ¥350,000 × 4 + ¥310,000 = ¥1,710,000. Without dependents, the threshold would be only ¥450,000–¥500,000.

Children Under 16 Matter Here

Even though children under 16 provide no income tax deduction, they do count as dependents for the resident tax non-taxable threshold calculation. This means registering your young children as dependents can eliminate your resident tax entirely if your income is modest.

National Health Insurance (NHI) Premiums

NHI premiums are calculated based on your prior-year income and the number of enrolled household members. The dependent deduction indirectly reduces your NHI premiums because:

- Lower taxable income → lower income-based NHI portion

- If your income falls below certain thresholds (which the dependent deduction helps achieve), you qualify for NHI premium reductions of 20%, 50%, or 70%

For detailed NHI information, see our Japan Health Insurance Guide for Foreigners.

8. Common Mistakes Foreigners Make

Mistake 1: Claiming Overseas Family Without Proper Documentation

The problem: Listing parents and siblings on your year-end adjustment form without providing relationship certificates or remittance receipts. Your employer may process the deduction initially, but the NTA can — and increasingly does — audit and reverse these deductions years later, resulting in back taxes plus penalties.

Mistake 2: Claiming a Spouse as a Dependent

The problem: Writing your spouse’s name in the “dependent” (扶養親族) section instead of the “spouse” (配偶者) section of the tax form. These are completely separate deduction systems. Claiming your spouse as a regular dependent will be rejected.

Mistake 3: Not Claiming Dependents at All

The problem: Many foreign workers, especially those unfamiliar with the Japanese tax system, simply skip the dependent section entirely. If you have qualifying family members (including overseas), you are leaving significant money on the table. A worker in the 20% bracket with 2 general dependents and 1 specific dependent saves approximately ¥228,000 in income tax alone every year.

Mistake 4: Ignoring the Income Threshold for Dependents

The problem: Claiming a family member as a dependent when their income exceeds ¥480,000 (合計所得金額). A common scenario: your spouse starts a part-time job earning ¥1,200,000/year (income of ¥650,000 after employment deduction), but you continue claiming the spouse deduction. This will be caught during reconciliation and result in additional tax assessment.

Mistake 5: Sending Lump-Sum Remittances to One Family Member

The problem: Sending ¥1,000,000 to your mother and expecting that to cover remittance proof for your mother, father, and a sibling. Under the 2023 rules, each dependent aged 30–69 must receive individually documented remittances of ¥380,000+.

9. How to Claim: Year-End Adjustment vs. Tax Return

Option 1: Year-End Adjustment (年末調整)

If you are employed by a Japanese company, the easiest way to claim dependents is through the year-end tax adjustment process in November/December:

- Fill out the Declaration of Deduction for Dependents (扶養控除等(異動)申告書) — your employer provides this form

- List each dependent with their name, date of birth, relationship, estimated income, and address

- Attach documentation for overseas dependents (relationship proof + remittance proof)

- Submit to your employer by the deadline (usually late November)

For more details on this process, see our Year-End Tax Adjustment Guide.

Option 2: Tax Return (確定申告)

File a tax return if:

- You missed the year-end adjustment deadline

- You need to correct your dependent claims

- You are self-employed or have multiple income sources

- You want to retroactively claim dependents for up to 5 years back

Tip: Retroactive Claims

If you have been in Japan for several years and never claimed your qualifying overseas dependents, you can file amended returns (更正の請求) for up to 5 prior years. For a worker in the 20% tax bracket with 2 overseas parents (aged 60, general dependents), this could mean a refund of approximately ¥76,000 × 2 × 5 years = ¥760,000.

For the full tax return filing process, see our Step-by-Step Tax Filing Guide.

Need help claiming dependents or filing a correction?

Get Matched with an English-Speaking Tax Accountant — Free →

Frequently Asked Questions

Can I claim my parents overseas as dependents in Japan?

Yes, if they meet the income requirement (total income under ¥480,000) and you provide proof of your family relationship and financial support (remittance receipts). If your parents are aged 30–69, the 2023 rule change requires documented remittances of at least ¥380,000 per parent per year. Parents aged 70+ can be claimed as elderly dependents with a higher deduction of ¥480,000 (or ¥580,000 if co-residing).

My child is 5 years old. Can I get a tax deduction?

Children under 16 do not qualify for the income tax dependent deduction. However, they do count toward the resident tax non-taxable threshold, which can reduce or eliminate your resident tax. You should still list them on your tax forms. Additionally, you may be eligible for the Child Allowance (児童手当), which provides ¥10,000–¥15,000 per month per child.

What happens if my dependent’s income exceeds the threshold mid-year?

The income threshold is measured for the full calendar year (January 1 – December 31). If your dependent’s total income exceeds ¥480,000 by year-end, you cannot claim the deduction for that year. If you already claimed it through year-end adjustment, you must file a tax return to correct it or face penalties when the discrepancy is discovered.

Can both spouses claim the same child as a dependent?

No. A dependent can only be claimed by one taxpayer. If both spouses work, you should decide which spouse claims each dependent — typically the higher earner benefits more from the deduction due to higher marginal tax rates. You cannot split or share dependent claims.

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax rules change frequently and individual circumstances vary. Always consult a qualified tax professional (税理士) for advice specific to your situation. Information is current as of March 2026.