Double Taxation in Japan: How to Avoid It (US, UK & India Guide 2026)

Are you being taxed twice on the same income? Japan has tax treaties with 80+ countries to prevent double taxation. Here’s how the Foreign Tax Credit works, country-specific rules for US, UK, and Indian residents, and the exact steps to claim relief.

Living in Japan with income from abroad? Get matched with a bilingual international tax specialist — free.

Japan has concluded tax treaties with over 80 countries, covering more than 95% of its international trade and investment. These treaties establish clear rules about which country has the right to tax which types of income — and what relief is available when both countries claim jurisdiction. However, the rules differ significantly depending on the type of income, your nationality, and which specific treaty applies.

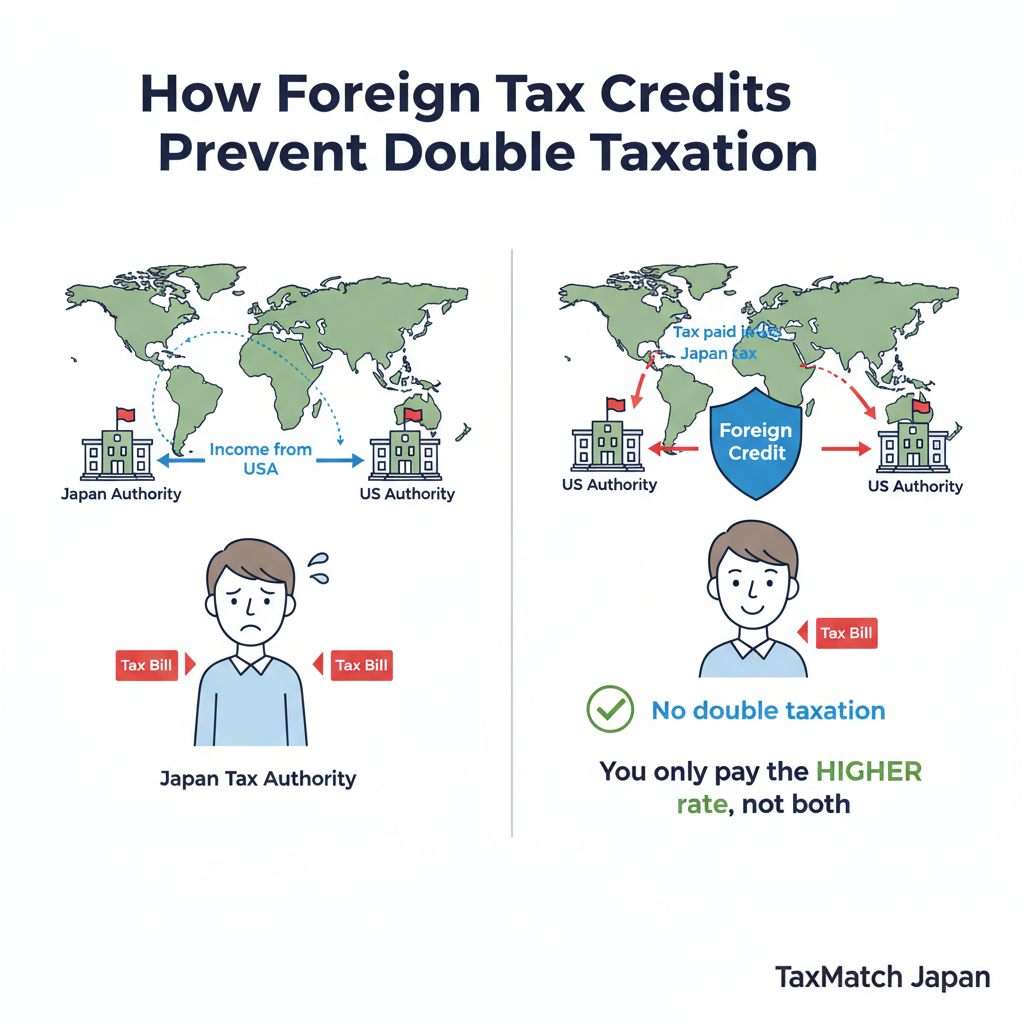

How Foreign Tax Credits prevent double taxation

How Double Taxation Relief Works: Two Methods

Japan’s domestic law and its tax treaties use two distinct methods to prevent double taxation:

| Method | How It Works | Where It Applies |

|---|---|---|

| Tax Credit Method | You pay tax in both countries, then claim a credit for foreign tax paid against your Japanese tax liability | Most income types under most treaties (Japan’s default domestic method) |

| Exemption Method | One country waives its tax entirely — the source country taxes, residence country exempts | Some treaty provisions (e.g., business profits taxable only in source country under PE rules) |

In practice, Japan almost always uses the foreign tax credit method (外国税額控除) — you declare all worldwide income in Japan, then deduct foreign taxes paid from your Japan tax bill, subject to a credit limit formula. The exemption method applies mainly to specific treaty provisions like Permanent Establishment rules and some employment income clauses.

Japan’s Credit Limit Formula

Japan does not allow unlimited credit for all foreign taxes paid. The credit is capped at:

📌 Credit Limit Formula

Credit Limit = Japan Tax Liability × (Foreign-Source Income ÷ Total Worldwide Income)

If foreign taxes paid exceed this limit, the excess is carried forward for up to 3 years. This carryforward is particularly important for US citizens who accumulate large FTC pools but have limited Japan-source income in some years.

Key points about the credit limit:

- The limit applies separately to each “basket” of income (though Japan uses a single-basket system)

- Only taxes imposed on income are creditable — withholding taxes on dividends and interest generally qualify

- Excess foreign taxes can be refunded in some cases if a treaty provides a more favorable result

- The credit applies against national income tax (所得税) only — local inhabitant tax (住民税) is calculated separately

Navigate tax treaties, claim foreign tax credits, and optimize your cross-border tax position.

Stop Paying Tax Twice — Get Expert Help →

Free matching · No obligation · English support

US Citizens in Japan: The Most Complex Case

The United States is unique in taxing its citizens on worldwide income regardless of where they live — a system called Citizenship-Based Taxation (CBT). This creates the most complex double taxation situation of any nationality in Japan, because both countries claim unlimited jurisdiction over your income.

The FBAR and FATCA Reporting Obligations

| Obligation | Threshold | Deadline | Penalty for Non-Compliance |

|---|---|---|---|

| FBAR (FinCEN 114) | $10,000 aggregate in foreign accounts at any point in the year | April 15 (auto-extended to October 15) | Up to $10,000/year negligent; up to $100,000+ or 50% of account balance for willful violations |

| FATCA (Form 8938) | $200,000 single / $400,000 married at year-end, OR $300K/$600K at any point | With your US tax return | $10,000 initial penalty + $10,000/30-day continuation; possible criminal charges |

| Form 3520 | Foreign gifts >$100,000 or trust transactions | April 15 | 35% of gift amount or greater |

⚠️ Japan Accounts That Trigger FBAR

Every bank account, brokerage account, NISA account, and iDeCo account you hold in Japan is a “foreign financial account” for US purposes. Most US expats in Japan have significant FBAR exposure — and many are unaware. The FBAR is filed separately from your tax return and is commonly missed.

FEIE vs. FTC: The Core US Expat Tax Decision

US citizens abroad have two main strategies to avoid double taxation:

| Foreign Earned Income Exclusion (FEIE) | Foreign Tax Credit (FTC) | |

|---|---|---|

| What it does | Excludes up to $126,500 (2024) of earned income from US taxable income | Reduces US tax dollar-for-dollar by foreign taxes paid |

| Best for | Lower-income expats; those in low-tax countries | Higher earners in high-tax countries like Japan |

| Japan context | Usually worse — Japan’s top rates (45% + 10% local) far exceed US rates, leaving excess credits unused under FEIE | Usually better — Japan taxes generally exceed US taxes, so FTC offsets US tax to near-zero |

| Self-employment tax | FEIE does NOT reduce self-employment tax (15.3%) | FTC does NOT reduce SE tax either |

| Interaction | Cannot claim FTC on excluded income | Claim on all income; excess carries forward 3 years (back 1 year) |

📌 Why Most US Residents in Japan Should Use FTC, Not FEIE

Japan’s marginal tax rate (45% national + 10% local = 55%) is significantly higher than the US top rate (37%). For most US expats in Japan earning above $50,000, the FTC method results in zero or near-zero US tax liability — because Japanese taxes already exceed what the US would charge. Using FEIE instead wastes potential credits and can create tax disasters when you eventually return to the US.

US-Japan Social Security Totalization Agreement

The US-Japan Totalization Agreement prevents dual social security taxation:

- Employees seconded from US companies: Generally exempt from Japanese social insurance for up to 5 years; continue paying US Social Security

- Locally hired employees: Pay Japanese social insurance (厚生年金) and are exempt from US Social Security on those wages

- Totalization benefit: Periods in both countries can be combined to meet minimum contribution requirements for pension eligibility

- Self-employed: Pay self-employment tax in the country where you live and work

RSU and Stock Option Proration for US Citizens

When RSUs vest after a period spanning both US and Japan residence, the income must be prorated between the two countries. The Japan-US treaty generally follows the OECD approach:

📌 RSU Proration Formula

Japan-Taxable Portion = Total RSU Income × (Days Worked in Japan ÷ Total Vesting Period Days)

Example: 1,000 RSUs granted during a 3-year vesting period. You spent 18 months in Japan out of 36 months total. At vesting, the shares are worth ¥10M. Japan taxes: ¥10M × (18/36) = ¥5M at salary income rates. The remaining ¥5M is taxable in the US (or wherever you previously resided).

UK Nationals in Japan: The Post-Non-Dom Era

The UK underwent a fundamental shift in 2025: the non-domicile tax regime was abolished for UK income tax purposes. This has significant implications for UK nationals living in Japan.

Before 2025: The Non-Dom Advantage

Under the old system, UK nationals with non-UK domicile could elect the “remittance basis” — paying UK tax only on UK-source income and foreign income remitted to the UK. A UK national living in Japan with Japan-source income and non-UK domicile could structure affairs to minimize UK tax exposure.

After April 2025: The New Residence-Based System

The UK has moved to a residence-based system:

- New arrivals: Foreign-source income is exempt from UK tax for the first 4 years of UK tax residence — but if you are already living in Japan (i.e., not a new UK arrival), this transitional relief may not help you

- UK residents: UK residents (those who were UK-resident) now pay UK tax on worldwide income regardless of domicile

- Japan residents: UK nationals living in Japan and not UK tax residents generally remain unaffected — they are Japan tax residents and benefit from the Japan-UK treaty

📌 Japan-UK Treaty: Key Points

- UK-source dividends: 10% withholding if you hold less than 10% of voting shares; 0% for substantial holdings

- UK pension income: Generally taxable in Japan if you are Japan-resident (not exempt from Japanese tax)

- UK rental income: Taxable in the UK under source rules; also declared in Japan with FTC relief available

- Business profits: Taxable only in Japan unless you have a UK Permanent Establishment

UK Nationals: Japan NTA Reporting

UK nationals who are Japan tax residents must report all worldwide income in Japan, including:

- UK rental income and mortgage interest (net basis)

- UK ISA gains (Japan does not recognize the UK ISA tax exemption)

- UK pension contributions and eventual pension income

- UK company dividends and share sale proceeds

Indian Nationals in Japan: The FEMA and Income Tax Complexity

Indian nationals living in Japan face a unique dual-layer challenge: India’s tax rules and its foreign exchange regulations (FEMA) operate independently, and compliance with both is mandatory.

Residency Status Under Indian Law

| Status | India Income Tax Scope | FEMA Status |

|---|---|---|

| Resident and Ordinarily Resident (ROR) | Worldwide income taxable in India | Resident — restrictions on foreign assets/transfers |

| Resident but Not Ordinarily Resident (RNOR) | India-source income + foreign business income + foreign salary received in India | Resident — some FEMA flexibility |

| Non-Resident Indian (NRI) | India-source income only | Non-Resident — more freedom to hold/transfer foreign assets |

Most Indian nationals living in Japan for more than 182 days in a tax year will be NRIs under Indian tax law — meaning India taxes only their India-source income (dividends from Indian companies, Indian rental income, Indian bank interest, capital gains on Indian assets). Japan taxes their worldwide income.

Form 67: India’s Mandatory FTC Claim Form

⚠️ Critical: Form 67 Must Be Filed Before the ITR Deadline

To claim a Foreign Tax Credit in India for taxes paid in Japan, Indian nationals must file Form 67 with the Income Tax Department before or simultaneously with the India Income Tax Return (ITR). If you miss this deadline, the FTC claim is rejected — even if you later file a revised return. This is a strict procedural requirement that catches many Indian expats off guard.

India-Japan Treaty Highlights

- Dividends: 10% withholding in source country

- Interest: 10% withholding in source country

- Capital gains on shares: Taxable in country of residence; gains on immovable property taxable in source country

- Employment income: Taxable in country where work is performed (Japan) if Japan-resident

- Business profits: Taxable only in Japan unless permanent establishment exists in India

FEMA Compliance for Japanese Salary Earnings

Even as an NRI, FEMA rules affect how you handle your Japan-earned salary:

- NRE accounts: Freely repatriable; interest is tax-free in India. Japan-earned income can be deposited here.

- NRO accounts: India-source income; repatriation capped at $1M per year with CA certification

- Returning to India: NRI status ends once you return permanently; must convert NRE accounts to resident accounts within specified timeframe

Practical Steps: Filing Both Countries’ Tax Returns

The Annual Filing Sequence

| Step | Action | Deadline |

|---|---|---|

| 1 | Gather all income documents (Japan + home country) | January-February |

| 2 | File Japan income tax return, including worldwide income declaration and FTC claim | March 15 |

| 3 (US) | File FBAR (FinCEN 114) for Japanese bank/brokerage accounts | April 15 (auto-extended October 15) |

| 3 (India) | File Form 67 (FTC claim) simultaneously with Japanese tax payment proof | Before ITR deadline (typically July 31) |

| 4 | File home country tax return with FTC claim for Japan taxes paid | US: April 15 (June 15 automatic extension for expats) / India: July 31 / UK: January 31 |

📌 Documentation You Must Keep

- Japanese tax payment certificates (納税証明書) — proof of taxes actually paid in Japan for FTC claims abroad

- Withholding tax statements (源泉徴収票) from employer

- Brokerage account statements showing cost basis and proceeds

- Exchange rates used for currency conversion (TTM rate on transaction date)

- Records of days spent in each country during the tax year

Common Double Taxation Mistakes

- Assuming the treaty automatically solves everything — Treaties set rules; you must actively claim relief on both countries’ returns. Nothing is automatic.

- Missing the 3-year carryforward window — Unused Japanese FTC credits can be carried forward for 3 years in Japan. Once that window closes, the credit expires permanently.

- Wrong exchange rate for FTC calculation — Japan allows you to choose TTM (mid-rate), TTB (buying rate), or TTS (selling rate) for different types of income. The choice affects your credit calculation and should be consistent year-to-year.

- Forgetting local inhabitant tax — Japan’s 10% local inhabitant tax cannot be used as a FTC against US federal tax. It does qualify as a foreign tax credit for some other purposes.

- Not adjusting RSU cost basis — If income tax was withheld at RSU vesting in Japan, that amount becomes part of your cost basis for capital gains purposes when you later sell the shares.

- FAQ

📝 Double Taxation Checklist

- Identify all income sources and which country has primary taxing rights under your treaty

- Calculate Japan FTC limit and compare with actual foreign taxes paid

- File Japan return by March 15 and obtain tax payment certificates

- US: File FBAR by April 15; consider FTC vs. FEIE strategy; file Form 8938 if needed

- India: File Form 67 with Japan tax payment proof before ITR deadline

- Keep records of days in each country and all income documentation for 7+ years

Managing income across Japan and your home country?

TaxMatch Japan connects you with bilingual international tax specialists experienced in US, UK, and Indian cross-border taxation — completely free matching service.

Or reach us directly on LINE

This article is for informational purposes only and does not constitute tax or legal advice. Tax treaty provisions are complex and fact-specific. Please consult a qualified licensed tax accountant (zeirishi) and, where relevant, a tax advisor licensed in your home country for personalized guidance specific to your situation.

Frequently Asked Questions

Does Japan have double taxation agreements?

Yes. Japan has signed tax treaties with over 80 countries, including the US, UK, India, Australia, Canada, Germany, France, and most major economies. These treaties allocate taxing rights and provide mechanisms to eliminate double taxation.

How do I avoid double taxation in Japan?

The primary method is the Foreign Tax Credit (gaikoku zeiaku kōjo). When you file your Japanese tax return, you can claim a credit for taxes paid to another country on the same income. You’ll need proof of foreign taxes paid and must file Form 1 or Form 2 with Schedule 7.

Can I get a refund for taxes paid in two countries?

Yes, in most cases. If you’ve been taxed on the same income by both Japan and another treaty country, you can claim the Foreign Tax Credit on your Japanese return (or the foreign country’s return) to recover the excess tax. The refund process typically takes 1–3 months after filing.

Which countries have tax treaties with Japan?

Japan has tax treaties with 80+ countries including the United States, United Kingdom, India, China, South Korea, Australia, Canada, Germany, France, Singapore, and most EU nations. Each treaty has specific provisions, so the details vary by country.