Japan Exit Tax for Foreigners — What You Must Know Before Leaving | TaxMatch Japan

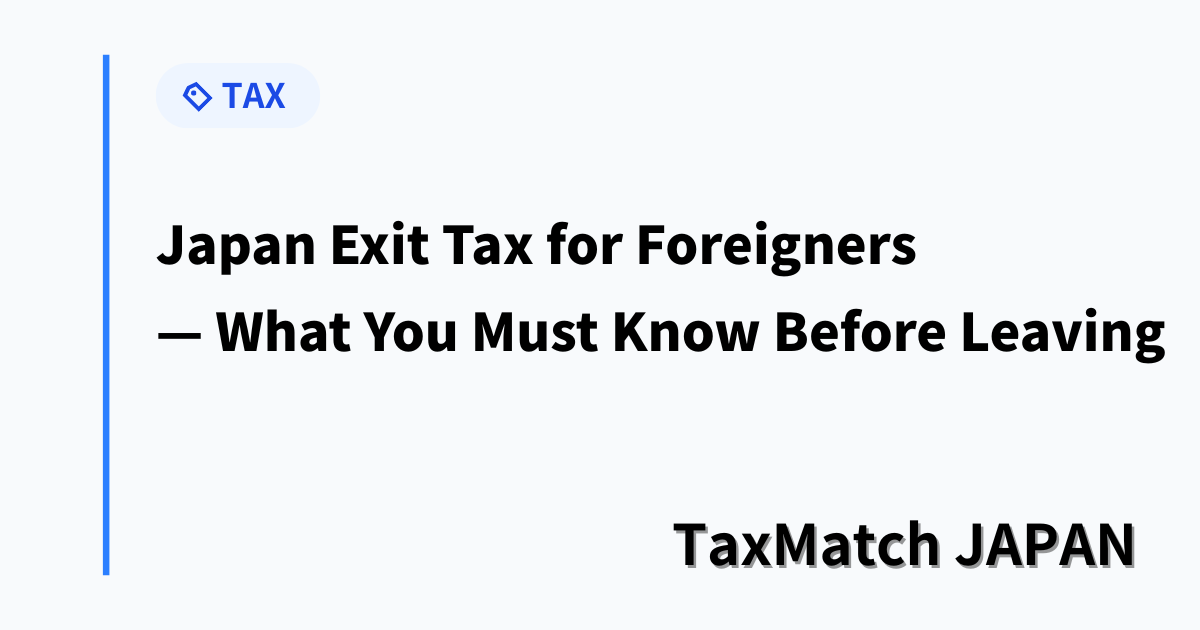

Exit Tax: Does it apply to you? Two conditions must both be met

Japan’s exit tax can reach tens of millions of yen on assets you haven’t even sold yet. Here’s everything foreign residents need to know before leaving Japan.

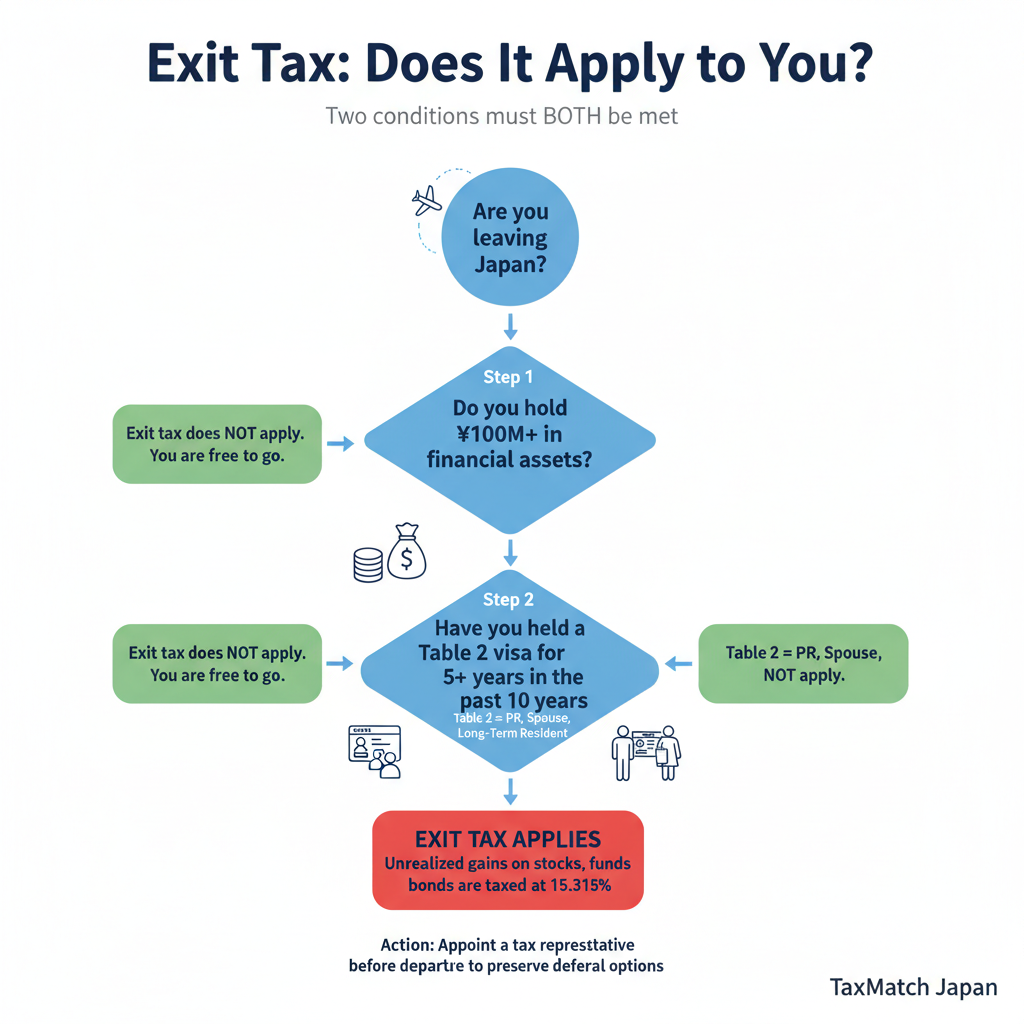

Exit Tax: The currency trap — taxed on gains you never realized

Planning to leave Japan with significant assets? Speak with a specialist before you book your flight.

Get Matched Free →Japan’s exit tax — formally known as the Departure Tax (国外転出時課税制度, Kokugai Tenzoku Ji Kazei) — was introduced in 2015 to prevent wealthy residents from moving to low-tax jurisdictions and selling their assets tax-free. It works by treating all your financial assets as if you sold them on your departure date, triggering a capital gains tax on all unrealized gains.

The law is widely misunderstood. Many foreigners assume they are automatically exempt. They are not — and the consequences of being caught unprepared can be catastrophic.

Exit Tax: Does it apply to you?

Do You Qualify? The Two Conditions

Japan’s exit tax applies only if you meet both of the following conditions simultaneously:

Condition 1: Asset Threshold — ¥100 Million or More

At the time of departure, the total fair market value of your specified financial assets must be ¥100 million (approximately $670,000) or more. This threshold is based on the gross value, not your unrealized gain. If your stock portfolio is worth ¥105 million and you paid ¥104 million for it, the exit tax still applies — even though your actual gain is minimal.

Assets that count toward the ¥100M threshold:

- Domestic and foreign listed stocks, mutual funds, ETFs

- Unlisted stocks (including your own company’s shares)

- Investment trusts and bond holdings

- NISA account holdings

- Unsettled derivatives and margin trading positions

Assets that do NOT count:

- Cash and bank deposits (including foreign currency deposits)

- Real estate (domestic or foreign)

- Physical assets: art, precious metals, vehicles

Exit tax, final returns, and pension refunds — get everything right before you leave Japan.

Plan Your Departure with a Tax Expert →Free matching · No obligation · English support

Condition 2: Residency Duration — 5+ Years in the Last 10

You must have lived in Japan for more than 5 cumulative years within the preceding 10 years. However, not all years count equally — and this is where most foreigners get confused.

| Visa Type | Examples | Counts Toward Exit Tax’s 5-Year Rule? |

|---|---|---|

| Table 1 visas (activity-based) | Highly Skilled Professional, Business Manager, Engineer/Humanities, Intra-company Transferee, Student | ❌ Does NOT count |

| Table 2 visas (status-based) | Permanent Resident, Spouse of Japanese National, Long-Term Resident | ✅ COUNTS toward 5 years |

📌 The Permanent Resident Trap

An executive on a highly skilled professional visa could live in Japan for 20 years with ¥500 million in assets and owe zero exit tax. But the day they switch to Permanent Resident status, a 5-year countdown begins. Switching to PR triggers exit tax exposure for anyone who crosses ¥100M in financial assets. This is one of the most consequential decisions foreign residents in Japan make — and few realize it.

How the Tax Is Calculated

The Tax Rate: 15.315% (Not 20.315%)

Unlike the standard capital gains rate of 20.315% (which includes 5% local inhabitant tax), the exit tax is assessed at 15.315%. The reason: local inhabitant tax requires residency as of January 1 — but if you’re leaving Japan, you won’t be a resident on the next January 1, so the 5% local tax doesn’t apply.

The Currency Risk: Phantom Gains from Yen Weakness

This is one of the cruellest aspects of the exit tax. All assets are valued in Japanese yen using the TTM exchange rate on your departure date. If you bought US stocks when the yen was strong and the yen has since weakened dramatically, you may owe enormous tax on “gains” that are purely a currency effect — even if the dollar value of your portfolio is flat.

📌 Calculation Example

You bought US index funds in 2012 for $500,000 (¥40M at 80 JPY/USD). In 2026, the same funds are worth $650,000 (¥97.5M at 150 JPY/USD).

- Dollar gain: $150,000 (30%)

- Yen gain: ¥57.5M (143%)

- Exit tax owed: ¥57.5M × 15.315% = approximately ¥8.8 million

You owe ¥8.8M in cash — on an investment that hasn’t been sold.

Valuing Unlisted Stocks

If you own shares in a private company (including your own startup), their value must be determined using the NTA’s asset valuation guidelines (財産評価基本通達). This typically requires a formal valuation report from a CPA or tax accountant before you leave Japan.

Practical Procedures Before Departing

The Two Scenarios: With vs. Without a Tax Representative

| Situation | Asset Valuation Date | Tax Filing Deadline | Can Apply for Deferral? |

|---|---|---|---|

| Appoint a tax representative (strongly recommended) | Actual departure date | March 15 of the following year | ✅ Yes |

| Leave without a representative | 3 months before departure date | Before you leave Japan (you must file and pay in full) | ❌ No |

⚠️ Don’t Leave Without a Tax Representative

If you leave without appointing a tax representative (納税管理人), you are legally required to file and pay all exit tax before boarding your plane — using an asset value calculated from 3 months before your departure. If markets fall in those 3 months, you pay tax on a higher phantom value. You also lose the right to request any deferral.

The Deferral Option: Up to 10 Years

If you qualify for exit tax, you don’t necessarily need to pay it immediately. You can apply for a tax deferral (納税猶予) of up to 5 years (extendable to 10 years with proper application), provided you:

- Appoint a Japanese tax representative before departure

- File the exit tax return and check the deferral box by March 15

- Provide collateral equal to the deferred tax amount plus accrued interest tax

- File annual continuation reports by March 15 each year

During the deferral period, if you sell any of the covered assets, you must immediately pay the corresponding deferred tax plus interest. However, if the assets drop in value after your departure, you can request a corrected assessment (更正の請求) to reduce the tax based on the lower actual sale price — this is an important protection against market risk during deferral.

International Double Taxation: US, Germany, France

Germany: Step-Up in Basis (Best Case)

Under German domestic law, Japan’s exit tax valuation date is recognized as the new German acquisition cost (step-up in basis). When you later sell in Germany, only the gains from the Japan departure date forward are taxed in Germany. Result: no double taxation.

US Citizens: The 10-Year Carryforward Trap

The US does not automatically recognize Japan’s exit tax valuation as a step-up in basis. You must rely on the Foreign Tax Credit (Form 1116). But here’s the problem: at the time you pay Japan’s exit tax, you haven’t sold anything — so there’s no US capital gain to offset. The unused credit is carried forward, but US law limits carryforward to 10 years. If you don’t sell those assets within 10 years of leaving Japan, the credit expires — and you’ll face full double taxation when you eventually sell.

📌 Strategic Solution for US Citizens: Basis Reset Before Leaving

The most powerful strategy for US citizens is to sell your portfolio while still in Japan and immediately repurchase the same assets. This triggers an actual capital gains event (Japan taxes at 20.315% or 15.315%), which you can then claim as an FTC on your US return in the same tax year. Your US cost basis resets to current market value, eliminating future double taxation entirely. This is completely legal in both countries.

France: Negotiated Relief

France has its own exit tax system. The Japan-France treaty provides mechanisms for resolving double taxation through mutual agreement procedures, though the process is complex and requires expert French-Japanese dual-qualified advisors.

Pre-Departure Tax Planning Strategies

Strategy 1: Keep Assets Below ¥100 Million

The simplest approach. If your portfolio is near the threshold, consider whether selling some assets before departure to bring total value below ¥100 million would be more efficient than paying exit tax. The “cliff effect” means ¥99.9M triggers zero exit tax while ¥100.1M triggers tax on all unrealized gains.

Strategy 2: Basis Reset (for US Citizens)

As described above: sell and repurchase before leaving. Pay standard Japan capital gains tax (20.315%), claim FTC on US return, and eliminate the exit tax overhang entirely.

Strategy 3: Manage Your Visa Status Carefully

If you are still on a Table 1 visa (Engineer, Business Manager, Highly Skilled Professional, etc.) and have accumulated significant financial assets, you are completely exempt from exit tax regardless of how long you’ve lived in Japan. Obtaining Permanent Resident status intentionally accelerates your exposure — weigh this carefully if your assets are significant.

Strategy 4: Time Your December 31 Departure

If you sell assets to reset your basis or realize gains, departing Japan before December 31 of that year eliminates the 5% local inhabitant tax on those gains (since inhabitant tax is based on January 1 residency). On large transactions, this alone can save millions of yen.

Cryptocurrency and the Exit Tax

As of 2025, cryptocurrency is not yet explicitly included in Japan’s exit tax framework. However, the government’s 2026 tax reform plans are expected to treat crypto the same as stocks — meaning it will likely be included in exit tax calculations for departures in 2026 and beyond. Anyone holding significant crypto portfolios should monitor this closely and consult a specialist.

Exit Tax and Inheritance: The Compound Risk

The exit tax extends beyond your own departure. If you are a Japanese resident with ¥100M+ in financial assets and you gift or bequeath those assets to a non-resident relative, the same exit tax logic applies. Your estate may owe 15.315% on unrealized gains — layered on top of Japan’s inheritance/gift tax, which reaches 55% at the top bracket. Proper estate planning well in advance of death or gifting is essential for high-net-worth foreign residents.

📝 Exit Tax Summary Checklist

- Do I have over ¥100M in financial assets (stocks, funds, derivatives)?

- Have I held a Table 2 visa (Permanent Resident, Spouse, Long-Term Resident) for 5+ cumulative years?

- If both: exit tax applies — begin planning at least 2 years before departure

- Appoint a tax representative before leaving

- Consider basis reset strategy (especially for US citizens)

- Consider timing departure before December 31 to avoid local inhabitant tax

- For unlisted stock: get a valuation report prepared before departure

Leaving Japan with significant assets?

TaxMatch Japan connects you with tax specialists experienced in exit tax planning — completely free matching service.

Or reach us directly on LINE

This article is for informational purposes only and does not constitute tax or legal advice. Japan’s exit tax rules are complex and change regularly. Please consult a qualified licensed tax accountant (zeirishi) for personalized guidance specific to your situation.

Frequently Asked Questions

What is Japan’s exit tax?

Japan’s exit tax (kokugai tensei kazei) is a tax on unrealized capital gains applied when a qualifying individual leaves Japan. It treats certain financial assets as if they were sold at fair market value on the date of departure, triggering a tax on paper gains.

Who has to pay exit tax in Japan?

The exit tax applies to individuals who have lived in Japan for 5 or more of the past 10 years AND hold financial assets (stocks, bonds, derivatives) with a total market value exceeding ¥100 million at the time of departure.

How can I avoid exit tax in Japan?

If your financial assets are below ¥100 million, the exit tax does not apply. You can also apply for a tax payment deferral (nozei yuyo) by appointing a tax agent and providing collateral. If you return to Japan within 5 years (extendable to 10), the deferred tax may be cancelled.