Foreign Tax Credit in Japan: How to Claim It and Avoid Paying Tax Twice | TaxMatch Japan

If you earn income abroad while living in Japan, you may be paying tax twice — once in the foreign country and once in Japan. Japan’s Foreign Tax Credit system is your primary tool to prevent this. Here’s exactly how it works and how to use it correctly.

Foreign income and unsure how to handle Japan taxes? Get matched with a bilingual specialist — free.

Get Matched Free →Japan’s tax law requires residents to declare all worldwide income — salaries earned abroad, dividends from foreign companies, foreign rental income, capital gains on overseas assets, and more. Without the Foreign Tax Credit (外国税額控除), you would pay the full tax rate of both countries. The credit mechanism ensures that you pay at most the higher of the two countries’ tax rates, not the combined total.

Foreign Tax Credit: Calculate your limit

Legal Basis: Articles 95 to 95-4 of the Income Tax Act

Japan’s Foreign Tax Credit is governed by Articles 95 to 95-4 of the Income Tax Act (所得税法) and corresponding provisions of the Corporation Tax Act. These articles establish:

- Article 95: The basic Foreign Tax Credit for individuals — direct credit for foreign taxes paid on foreign-source income

- Article 95-2: The indirect foreign tax credit for domestic corporations with foreign subsidiaries

- Article 95-3: Provisions for controlled foreign corporation (CFC/タックスヘイブン) inclusions

- Article 95-4: The 3-year carryforward mechanism for excess foreign tax credits

For most foreign residents working in Japan, Article 95 — the basic individual credit — is the relevant provision.

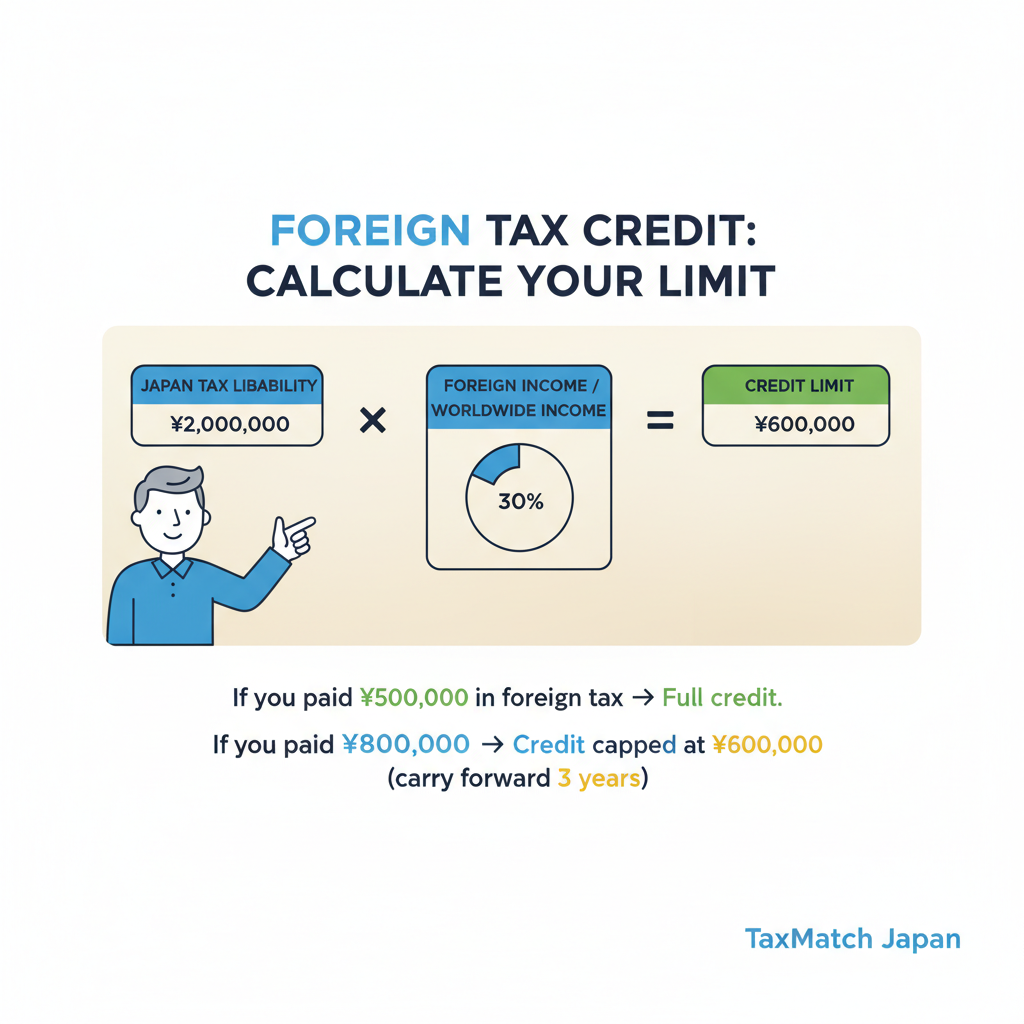

The Credit Limit Formula: A Critical Calculation

Japan does not allow you to credit all foreign taxes paid without limit. The credit is capped at the amount of Japan income tax attributable to your foreign-source income:

📌 The Credit Limit Formula

Credit Limit = Japan National Income Tax × (Net Foreign-Source Income ÷ Net Worldwide Income)

Practical example:

- Total Japan income tax liability: ¥3,000,000

- Foreign-source income: ¥5,000,000 out of total worldwide income of ¥15,000,000

- Credit limit: ¥3,000,000 × (5,000,000 ÷ 15,000,000) = ¥1,000,000

- If foreign taxes paid = ¥800,000: full credit allowed (¥800K < ¥1M limit)

- If foreign taxes paid = ¥1,500,000: only ¥1,000,000 credited; ¥500,000 excess carries forward

⚠️ Key Limitation: Only National Income Tax, Not Local Tax

The credit limit is calculated against national income tax (所得税) only. Japan’s 10% local inhabitant tax (住民税) is calculated separately and cannot be offset by foreign tax credits. This means even with a full FTC, you will always owe some Japan tax if you have Japan-source income subject to local tax.

Our specialists ensure you claim every credit and avoid paying tax twice on the same income.

Maximize Your Foreign Tax Credits →Free matching · No obligation · English support

The 3-Year Carryforward for Excess Credits

If your foreign taxes paid exceed the credit limit in any given year, the excess is not simply lost. Under Article 95-4, you can carry forward unused credits for up to 3 years.

This carryforward is particularly important for:

- US citizens who accumulate large FTC pools from high US tax payments on investment income

- Expats with variable income who had high foreign income in one year but lower Japan tax liability

- RSU holders who paid large foreign taxes at vesting but have lower Japan-source income relative to the foreign tax amount

To preserve carryforward credits, you must file the FTC claim on your Japan tax return even in years where the full credit cannot be used. Failure to file the claim results in permanent loss of the carryforward.

Which Foreign Taxes Are Creditable?

Not every tax paid to a foreign government qualifies for Japan’s FTC. The NTA has strict criteria:

| Tax Type | Creditable? | Notes |

|---|---|---|

| Foreign national income tax | ✅ Yes | Core qualifying tax (US federal income tax, UK income tax, Indian income tax, etc.) |

| Foreign state/prefectural income tax | ✅ Yes | US state income taxes, German Länder taxes, etc. |

| Withholding tax on dividends (treaty rate) | ✅ Yes | Must not exceed the treaty rate; excess withholding is not creditable |

| Withholding tax on interest | ✅ Yes | Subject to treaty rate limits |

| Foreign inheritance/gift tax | ❌ No | Not an income tax — separate credit rules apply |

| Foreign consumption/VAT/GST | ❌ No | Not an income tax; cannot be credited |

| Foreign social security taxes | ❌ No | Not an income tax (though totalization agreements apply separately) |

| Withholding tax exceeding treaty rate | ❌ No | Must request refund from source country; excess not creditable in Japan |

Exchange Rate: The TTM vs. TTB/TTS Choice

Foreign-currency income must be converted to Japanese yen for Japan tax purposes. The NTA allows three exchange rate options, and your choice can significantly affect your credit calculation:

| Rate Type | Definition | Best Used For |

|---|---|---|

| TTM (Telegraphic Transfer Middle Rate / 仲値) | Mid-point between buying and selling rates | Most income types; the standard choice for consistency |

| TTB (Telegraphic Transfer Buying Rate) | Rate at which your bank buys foreign currency (lower than TTM) | Foreign income received as cash; can reduce yen-equivalent income |

| TTS (Telegraphic Transfer Selling Rate) | Rate at which your bank sells foreign currency (higher than TTM) | Foreign currency expenditures; can increase yen-equivalent deductions |

📌 The Exchange Rate Strategy

For dividend income received in USD, using the TTB rate (which is lower than TTM) reduces the yen-equivalent income declared in Japan — lowering your Japan tax while potentially also reducing the credit limit. The optimal choice depends on your specific situation. Importantly, once you choose a rate method, consistency matters — switching methods opportunistically across years can attract NTA scrutiny.

Foreign Tax Credit for Dividend Income

Dividends from foreign companies are a common source of double taxation for Japan residents. Here’s how the FTC applies:

The Withholding Tax Layer

Most countries withhold tax on dividends paid to foreign recipients. Under Japan’s tax treaties, the maximum withholding rate is typically 10-15% (e.g., US-Japan treaty: 10% for portfolio dividends; 5% for 10%+ shareholdings). If the foreign company withholds at a higher rate than the treaty allows, the excess is not creditable in Japan — you must claim a refund directly from the foreign tax authority.

Filing Sequence for Dividends

- Confirm the treaty withholding rate for your dividend source country

- Verify the actual withholding amount on your brokerage statement

- Convert the gross dividend to yen at the TTM rate on payment date

- Declare the gross dividend as foreign income in Japan (not net after withholding)

- Claim the creditable withholding tax (up to treaty rate) as FTC on your Japan return

- If excess withholding exists, file a refund claim with the source country

Foreign Tax Credit for RSU Income

RSU (Restricted Stock Unit) income that spans both Japan and foreign residence periods requires careful FTC handling:

📌 RSU FTC Example

Scenario: You received 1,000 RSUs granted over a 3-year vesting period. You worked 18 months in Japan and 18 months in the US. Shares vest at ¥10M total value. Your employer withholds US federal tax of $30,000 (approx. ¥4.5M) on the full grant value. Japan claims 50% (18/36 months) = ¥5M as Japan-taxable salary income.

FTC Calculation:

- Japan-taxable RSU income: ¥5,000,000

- Pro-rated US tax attributable to Japan portion: $15,000 (50% of $30,000) = approx. ¥2,250,000

- Japan income tax on RSU income (assume 33% effective rate): approx. ¥1,650,000

- FTC claim: ¥1,650,000 (limited by Japan tax on foreign portion — cannot exceed Japan tax owed)

- Remaining US tax: credit claimed on US return for Japan taxes paid on the Japan portion

Filing Sequence for RSU FTC

- Obtain the employer’s RSU proration calculation

- File Japan tax return (March 15) declaring Japan-source RSU income and claiming FTC for pro-rated foreign taxes

- Obtain Japan tax payment certificate (納税証明書)

- File home country return claiming FTC for Japan taxes paid on home-country-allocated RSU income

Non-Permanent Residents: The Remittance-Proportional FTC

Foreign residents who qualify as Non-Permanent Residents (NPR) — those who have lived in Japan for 5 years or fewer out of the past 10 years — have a special FTC calculation that mirrors their limited tax exposure:

📌 NPR Remittance-Proportional Credit

NPRs only pay Japan tax on foreign income that is either: (1) sourced in Japan, or (2) remitted to Japan. They do not pay Japan tax on foreign income that stays offshore.

As a result, the FTC available to NPRs is proportional to the remitted amount. If you earned $100,000 of US dividends and remitted $40,000 to Japan, only 40% of the US withholding taxes paid become available as FTC in Japan. The remaining 60% of foreign taxes cannot be credited in Japan (since Japan didn’t tax that income) — but may be creditable in the US.

How to File: The Mechanics

Required Forms and Attachments

- 確定申告書 (Annual Income Tax Return): The main return; you must opt for the general calculation method (一般用), not the simplified salary worker version

- 外国税額控除に関する明細書 (FTC Detail Statement): Lists each country, income amount, and foreign tax paid

- Foreign tax payment certificates: Proof of actual taxes paid in the foreign country (e.g., Form 1042-S, brokerage 1099-DIV, or equivalent)

- Exchange rate documentation: TTM rates for each transaction date (available from major Japanese bank websites)

Filing Timeline

| Date | Action |

|---|---|

| January 1 – February | Collect all foreign income statements, brokerage reports, and tax certificates |

| February 16 – March 15 | Japan tax filing period; submit return with FTC detail statement and supporting documents |

| March 15 (or later if extended) | Pay any Japan tax owed (net after FTC); excess refunded within 1-2 months |

| After March 15 | Obtain Japanese 納税証明書 (tax payment certificate) for home country FTC claims |

📝 FTC Checklist

- List all foreign income sources and corresponding foreign taxes withheld/paid

- Verify withholding tax rates against applicable treaty rates; identify any excess withholding

- Calculate credit limit using the formula (Japan tax × foreign income ÷ worldwide income)

- Choose exchange rate method (TTM recommended for consistency) and document rates

- Complete 外国税額控除に関する明細書 and attach to Japan tax return

- Track any excess credits for carryforward; retain documentation for 3 years

- Obtain Japan 納税証明書 after payment for home country FTC claims

Foreign income and complex Japan tax questions?

TaxMatch Japan connects you with bilingual tax specialists who handle foreign tax credits as part of their daily practice — completely free matching service.

Or reach us directly on LINE

This article is for informational purposes only and does not constitute tax or legal advice. Foreign tax credit rules are complex and fact-specific. Please consult a qualified licensed tax accountant (zeirishi) for personalized guidance specific to your situation.

Frequently Asked Questions

What is the foreign tax credit in Japan?

The foreign tax credit (gaikoku zeikin kojo) allows Japan tax residents to offset Japanese income tax by the amount of tax already paid to foreign governments on the same income, preventing double taxation on foreign-source income.

How do I claim a foreign tax credit on my Japanese return?

Report the foreign tax paid on your annual tax return (kakutei shinkoku) using the Foreign Tax Credit calculation form. You need documentation proving the foreign tax was paid, including foreign tax returns and payment receipts.

Can I carry forward unused foreign tax credits in Japan?

Yes. If your foreign tax credit exceeds the allowable limit in a given year, you can carry forward the excess for up to 3 years. Similarly, if your limit exceeds the credit used, the unused limit can be carried forward for 3 years.