Gift Tax & 10-Year Rule in Japan for Foreign Residents (2026) | TaxMatch Japan

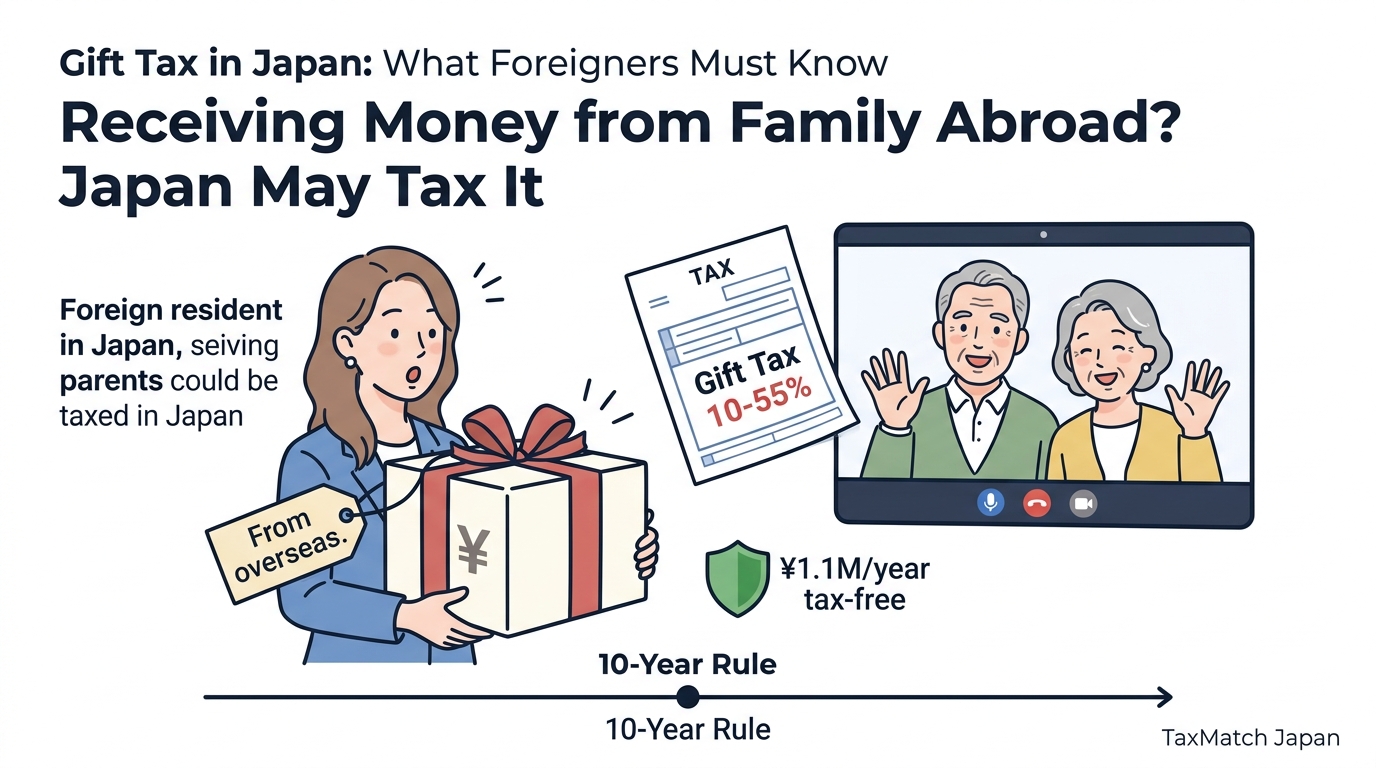

Japan’s gift tax (贈与税 / zoyo-zei) catches many foreign residents off guard for one simple reason: in Japan, it is the recipient who pays the tax, not the donor. Receive a wire transfer from your parents overseas, accept help with a house down payment, or let your spouse transfer savings into your account, and you may owe the Japanese government up to 55% of the value. Whether you are taxed on gifts from abroad depends entirely on your visa type and how long you have lived here — cross the wrong threshold, and overseas gifts that were previously exempt become fully taxable. This guide explains the full framework for 2026, including the scheduled abolition of the education fund exemption in March 2026.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Gift tax rules involve complex residency-based thresholds and are subject to legislative amendments. Always consult a qualified tax professional (税理士 / zeirishi) for advice specific to your situation.

Need a bilingual tax accountant? Get matched with a gift and inheritance tax specialist — free.

Receiving money from family abroad? Japan may tax it

Table of Contents

1. Gift Tax Basics

Under Japan’s Calendar Year Taxation System (暦年課税制度), the NTA assesses tax on the total value of all gifts received by an individual between January 1 and December 31.

The Annual Exemption

Every recipient is entitled to a basic annual exemption of 1,100,000 yen. Key points:

- The exemption is per recipient, not per donor

- You can receive up to 1.1M yen total from multiple donors without tax

- A donor can give 1.1M yen to unlimited recipients (e.g., 1.1M each to 10 grandchildren = 11M yen tax-free)

- If total gifts are at or below 1.1M yen, no tax return is required

Recipient-Based Taxation

Unlike the US or UK where gift tax falls on the donor, Japan taxes the recipient. This means foreign residents in Japan can trigger tax obligations simply by receiving money from overseas family members who have no connection to Japan whatsoever.

Deemed Gifts (みなし贈与)

The NTA’s definition of “gift” extends well beyond cash transfers:

- Forgiveness of a debt

- Transfer of property at significantly below market value

- Using another person’s funds to acquire an asset in your name

- Life insurance proceeds where the premium payer differs from both the insured and the beneficiary

Filing Deadline

Gift tax returns must be filed between February 1 and March 15 of the year following the gift. Payment is generally required as a lump sum, though installment plans are available with formal application and collateral.

2. Progressive Rate Structure

Japan applies two rate schedules depending on the relationship between donor and recipient:

Special Rate (特例税率) vs. General Rate (一般税率)

- Special Rate: Applies to gifts from lineal ascendants (parents, grandparents) to adult descendants (age 18+). More favorable rates.

- General Rate: Applies to all other gifts (from non-relatives, siblings, spouses, or to minor descendants). Steeper rates at lower thresholds.

| Taxable Amount (after 1.1M exemption) | General Rate | Special Rate |

|---|---|---|

| Up to 2,000,000 | 10% | 10% |

| 2,000,001 – 3,000,000 | 15% | 15% |

| 3,000,001 – 4,000,000 | 20% | 15% |

| 4,000,001 – 6,000,000 | 30% | 20% |

| 6,000,001 – 10,000,000 | 40% | 30% |

| 10,000,001 – 15,000,000 | 45% | 40% |

| 15,000,001 – 30,000,000 | 50% | 45% |

| 30,000,001 – 45,000,000 | 55% | 50% |

| Over 45,000,000 | 55% | 55% |

Calculation Example

A 25-year-old foreign resident receives 10,000,000 yen from their overseas parent:

- Taxable base: 10,000,000 – 1,100,000 = 8,900,000 yen

- Parent to adult child → Special Rate applies

- 8,900,000 falls in the 30% bracket (deduction: 900,000 yen)

- Tax = (8,900,000 x 30%) – 900,000 = 1,770,000 yen

3. The 10-Year Rule for Foreigners

The most critical factor determining whether a foreign resident owes gift tax on overseas assets is the interplay between their visa type and duration of domicile.

Table 1 vs. Table 2 Visas

| Category | Visa Types | Gift Tax Implication |

|---|---|---|

| Table 1 (Work/Temporary) | Engineer, Specialist in Humanities, Business Manager, Intra-company Transferee, HSP, Student | If domicile < 10 years in past 15 years → limited liability (Japan-situs assets only) |

| Table 2 (Settlement/Permanent) | Permanent Resident, Spouse of Japanese National, Long-Term Resident | Immediate unlimited liability on worldwide assets, regardless of duration |

How It Works

- Table 1 visa + domicile < 10 years: You are a “Temporary Foreigner.” Gift tax applies only to assets located within Japan. Overseas gifts from non-resident foreign donors are entirely exempt.

- Table 2 visa (any duration): Unlimited worldwide gift tax liability from day one.

- Table 1 visa + domicile > 10 years in past 15: You lose Temporary Foreigner status and face unlimited worldwide liability.

Warning: The Permanent Resident Visa Trap

Switching from a Table 1 work visa to a Table 2 Permanent Resident visa — often done to secure a mortgage — immediately triggers unlimited worldwide gift tax liability, even if you have been in Japan for only 3 years. This is an irreversible change for gift and inheritance tax purposes.

4. Taxable Scope by Scenario

Scenario A: Short-Term Foreign Professional (Table 1, 3 years)

Parents in the US send $100,000 to the engineer’s US brokerage account.

Result: No Japanese gift tax. Temporary Foreigner status + non-resident donor + overseas asset = completely exempt.

Warning: The Routing Trap

If those same parents wire the $100,000 directly into the engineer’s Japanese bank account, it instantly becomes a Japan-situs asset. Regardless of Temporary Foreigner status, Japan-situs assets are always taxable. The engineer would owe gift tax on the amount exceeding 1.1M yen.

Scenario B: Long-Term PR Visa Holder (Table 2, 8 years)

Receives a 200,000 EUR inheritance advance deposited into a European bank by a German parent.

Result: Fully taxable in Japan. Table 2 visa immediately triggers worldwide taxation. The location of the asset (Germany) and the residence of the donor (Germany) are legally irrelevant.

Scenario C: Spousal Transfer (Table 2)

Japanese spouse transfers 15,000,000 yen to foreign spouse’s individual Japanese bank account.

Result: Taxable. Spousal transfers exceeding 1.1M yen are gifts under the General Rate Schedule (spousal transfers do not qualify for the Special Rate). The foreign spouse owes gift tax unless the residential property spousal exemption applies.

5. Common Gift Scenarios

Parents Sending Money for a House Down Payment

If the recipient has unlimited tax liability (Table 2 visa or 10+ years on Table 1) and the funds arrive in Japan, this is a taxable gift. To mitigate, the family should formally utilize the Housing Acquisition Fund Exemption (see Section 6), which requires strict documentation and property standards.

Inheritance Advances from Overseas

Many Western countries (especially the US with its $13.61M lifetime unified credit) allow large tax-free lifetime gifts. Japan does not recognize foreign lifetime exemptions. An inheritance advance received by an unlimited-liability taxpayer is a standard gift taxed at rates up to 55%.

Spousal Account Transfers

Japanese banks do not offer joint accounts. If one spouse systematically transfers surplus savings to the other spouse’s account for “joint” savings, the NTA views this as a series of taxable gifts. Only funds used immediately for daily living expenses (groceries, rent, utilities) are exempt.

RSUs and Stock from Foreign Parent Companies

RSU grants from a foreign employer are not gifts — they are taxed as employment income at progressive rates upon vesting. However, if an overseas relative directly transfers private company shares to a Japan-resident family member, that is a taxable gift.

6. Tax-Free Gifts & Exemptions

Housing Acquisition Fund (住宅取得等資金の非課税)

Parents or grandparents can gift funds tax-free for the purchase, construction, or major renovation of a primary residence in Japan:

| Property Standard | Tax-Free Limit |

|---|---|

| General housing | 5,000,000 yen |

| High-quality housing (ZEH, earthquake-resistant, barrier-free) | 10,000,000 yen |

Combined with the annual 1.1M exemption, up to 11,100,000 yen can be transferred tax-free in one year. Key conditions:

- Recipient must be 18+ and a lineal descendant

- Recipient’s annual income must be 20M yen or less

- Floor area: 40-240 sqm, located in Japan

- Must occupy by March 15 of the following year

- Cannot purchase from spouse or related party

- Tax return must be filed even if the exemption reduces tax to zero

Educational Funds (教育資金一括贈与) — ABOLISHED March 2026

Warning: Expiring March 31, 2026

The lump-sum educational fund exemption (up to 15,000,000 yen per grandchild via a dedicated trust account) is being permanently abolished upon expiration on March 31, 2026. No new tax-free educational trusts can be established after this date. Existing trusts established before the deadline will be grandfathered.

As an alternative, the government is expanding the tax-free NISA framework to minors (ages 0-17) with an annual investment limit of 600,000 yen.

Wedding and Childcare Funds (結婚・子育て資金)

Up to 10,000,000 yen tax-free (sub-limit of 3,000,000 yen for wedding expenses) through a dedicated account at a financial institution. This exemption has been extended through 2026. Unused funds when the recipient turns 50 are retroactively subject to gift tax.

Ordinary Living and Education Expenses

Direct payments for necessary living and educational expenses between family members with a duty of mutual support are inherently non-taxable — but only if consumed immediately. A parent paying a university’s tuition invoice directly is tax-free. Wiring 5M yen to a child’s account “for living expenses” and having the child save the surplus is a taxable gift.

Gift tax planning requires precise timing and documentation. A bilingual tax accountant can help you utilize exemptions correctly. Get matched free →

7. Spousal Deduction (配偶者控除)

The “Oshidori Zoyo” (おしどり贈与 / mandarin duck gift) allows a spouse to deduct up to 20,000,000 yen from the value of a gift consisting of residential property or funds specifically for purchasing residential property.

Requirements

- Married for at least 20 continuous years

- The gift must be domestic residential property (or funds to acquire it)

- The recipient must live in the property as their primary residence

- Once-in-a-lifetime — can only be used once per marriage

- Tax return must be filed (even if tax is zero)

Combined with the annual 1.1M exemption, the maximum tax-free spousal transfer is 21,100,000 yen in a single year.

8. Settlement at Time of Inheritance (相続時精算課税制度)

This alternative system allows large lifetime gifts with deferred taxation — but it is an irrevocable election that permanently replaces the Calendar Year system for the specific donor-recipient pair.

How It Works

- Recipient must be 18+ receiving from a donor aged 60+

- Cumulative lifetime special deduction of 25,000,000 yen per donor

- Amounts exceeding 25M are taxed at a flat 20%

- Upon the donor’s death, all gifts under this system are added back to the estate for inheritance tax calculation

- Gift values are locked at the time of the original gift, not at death

- Any 20% gift tax paid is credited against the final inheritance tax

2024/2026 Upgrade: New Annual Deduction

Recent tax reforms added a separate 1,100,000 yen annual deduction within the Settlement System. Gifts below this threshold are exempt from gift tax and are not added back to the inheritance estate upon death — closing a significant prior disadvantage.

Tip

The Settlement System is highly effective for transferring rapidly appreciating assets (real estate in growth areas, pre-IPO equity). By gifting early, you freeze the valuation for inheritance tax purposes, shielding all subsequent appreciation from the 55% maximum inheritance tax rate.

9. International Complications

The Scarcity of Gift Tax Treaties

Japan has only one gift tax treaty: the US-Japan Estate, Inheritance, and Gift Tax Treaty of 1954. Transfers involving the UK, Canada, Australia, EU countries, and all other nations have no treaty protection for gift taxes.

US-Japan Treaty Mechanisms

- Credit System: Japanese gift tax paid reduces US gift/estate tax on the same asset dollar-for-dollar

- Situs Rules: Treaty establishes where an asset is legally located (real estate = physical location, shares = country of incorporation)

- Unified Credit Extension: Japanese nationals can claim a pro-rata share of the US lifetime unified credit ($13.61M in 2024, scheduled to halve in 2026)

Unilateral Foreign Tax Credits

For non-US jurisdictions, Japan offers a domestic foreign tax credit (Article 21-8) if you paid an equivalent overseas tax. However, the credit is capped at the ratio of foreign-sourced taxable value to total taxable value.

Valuation of Overseas Assets

- Currency conversion: Use the TTM (Telegraphic Transfer Middle) rate on the exact date the gift is received

- Annual average rates cannot be used

- Overseas real estate: Must use Fair Market Value (not foreign tax assessments); independent appraisal required

- Yen depreciation can push a modest overseas transfer into higher tax brackets

10. Common Mistakes

Mistake 1: Assuming Gift Tax Is the Donor’s Problem

The problem: Coming from a donor-tax jurisdiction (US, UK) and failing to realize that receiving a wire transfer triggers your own Japanese filing obligation. Non-compliance exposes you to delinquent taxes, heavy penalty surcharges (up to 20%), and multi-year NTA audits.

Mistake 2: Disguising Gifts as “Loans”

The problem: Structuring an intra-family transfer as a “loan” without formal documentation, realistic interest rates, or an actual repayment schedule. The NTA reclassifies the entire principal as a taxable gift. Eventual forgiveness of the “loan” triggers an additional deemed gift.

Mistake 3: The Name-Borrowing Account Trap (名義預金)

The problem: Parents opening accounts in children’s names and making periodic deposits below the 1.1M threshold. If the child does not manage the account, control the passbook/hanko, or freely spend the funds, the NTA rules that no gift occurred. The total balance is classified as the parent’s hidden asset and subject to inheritance tax at death.

Mistake 4: Switching to a PR Visa Without Understanding the Consequences

The problem: Acquiring a Table 2 Permanent Resident visa (often for mortgage eligibility) without realizing it immediately triggers unlimited worldwide gift and inheritance tax liability.

Mistake 5: Failing to File When Using Exemptions

The problem: Assuming that if the exemption reduces your tax to zero, no return is needed. For the Housing Acquisition Fund exemption, the spousal deduction, and other exemptions, a tax return must be filed by March 15. Failure to file strips the exemption retroactively.

Summary

- Japan taxes the recipient, not the donor — annual exemption is 1,100,000 yen

- Progressive rates reach 55% on gifts exceeding 45M yen

- Table 1 visa holders with < 10 years domicile pay tax only on Japan-situs assets

- Table 2 visa holders face worldwide gift tax from day one

- Housing exemption: up to 10M yen (high-quality housing) + 1.1M annual = 11.1M tax-free

- Education fund exemption: abolished March 31, 2026

- Spousal deduction: up to 20M yen (20+ years married, residential property)

- Japan has only one gift tax treaty (with the US)

Need help with gift tax planning? Get matched with an English-speaking tax accountant who specializes in wealth transfers and inheritance — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

Do foreigners pay gift tax in Japan?

Yes, foreigners in Japan may be subject to gift tax. If either the donor or recipient has a domicile in Japan, gift tax can apply to worldwide assets. The scope depends on the residency duration and status of both parties under the 10-year rule.

What is the gift tax rate in Japan?

Japan’s gift tax rates are progressive, ranging from 10% to 55%. The annual basic exemption is ¥1.1 million per recipient. Gifts exceeding this amount are taxed at rates that increase with the value of the gift.

How much can I gift tax-free in Japan?

Each person can receive up to ¥1.1 million per year in gifts tax-free under the basic exemption. Additionally, special exemptions exist for educational funds (up to ¥15 million), marriage/childcare funds (up to ¥10 million), and housing acquisition funds (up to ¥10 million depending on conditions).