Hiring Employees & Payroll Tax in Japan for Foreign Business Owners (2026) | TaxMatch Japan

Hiring your first employee in Japan is a milestone — but it comes with a payroll compliance burden that catches most foreign business owners off guard. Between income tax withholding (源泉徴収), social insurance (社会保険), labor insurance (労働保険), and residence tax collection (住民税特別徴収), the true cost of an employee can exceed their gross salary by 15-17%. Miss an enrollment deadline by even a day, miscategorize a worker, or botch the year-end adjustment, and you face backdated premiums, penalties, and potential visa sponsorship problems. This guide walks you through every obligation for 2026.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Payroll regulations and social insurance rates change frequently. Always consult a qualified tax professional (税理士 / zeirishi) or certified social insurance and labor consultant (社会保険労務士 / sharoushi) for advice specific to your situation.

Need a bilingual tax accountant? Get matched with a payroll and employment tax specialist — free.

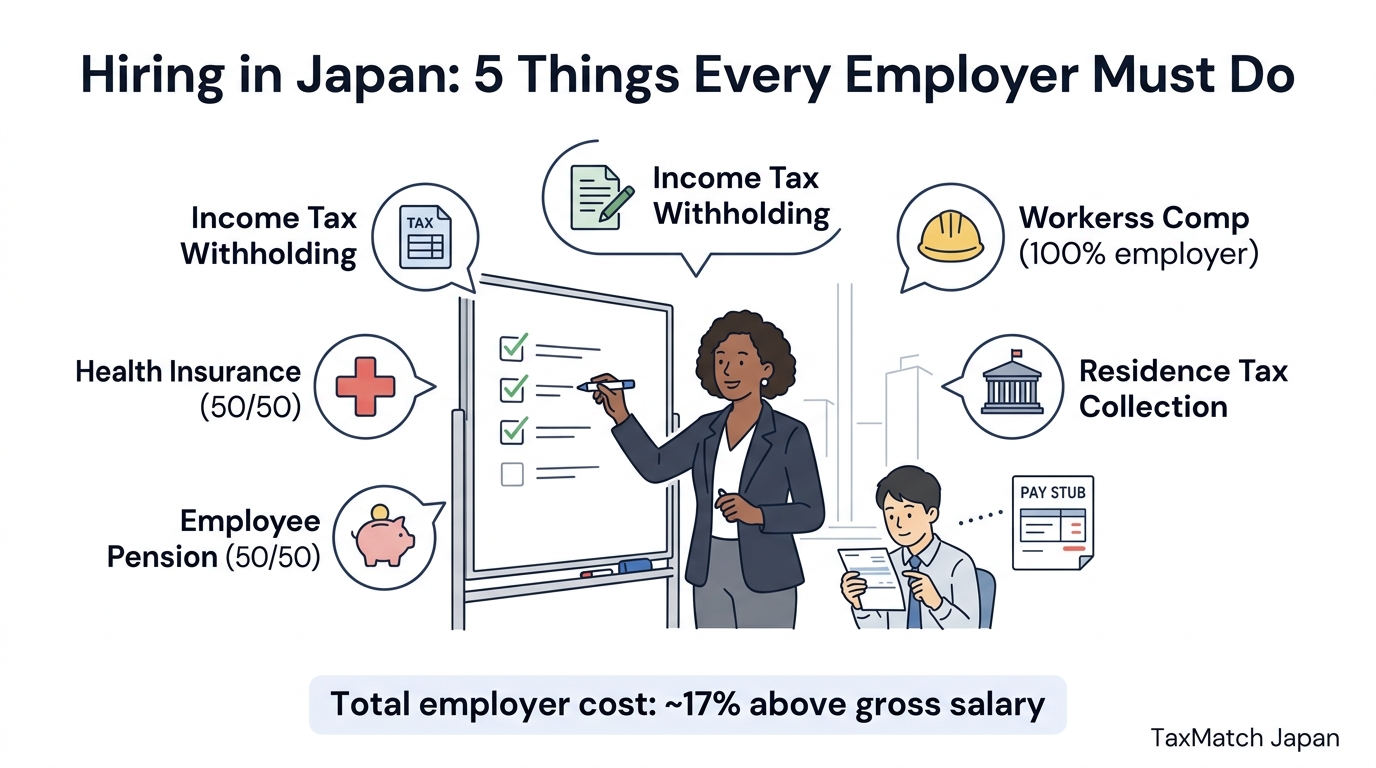

Hiring in Japan: 5 things every employer must do

Table of Contents

- Employer Obligations Overview

- Income Tax Withholding (源泉徴収)

- Social Insurance (健康保険 & 厚生年金)

- Labor Insurance (労災保険 & 雇用保険)

- Residence Tax Special Collection (住民税特別徴収)

- Hiring Foreign Nationals

- The Annual Payroll Calendar

- Cost Simulation: True Employer Burden

- Common Mistakes (And How to Avoid Them)

- When to Hire a Tax Accountant

- Frequently Asked Questions

1. Employer Obligations Overview

When you hire an employee in Japan, you become responsible for four distinct payroll compliance systems, each administered by a different government agency with its own deadlines, calculations, and reporting requirements.

| System | Components | Governing Agency | Cost Split |

|---|---|---|---|

| Income Tax Withholding (源泉徴収) | Progressive national income tax | National Tax Agency (NTA) | 100% employee |

| Social Insurance (社会保険) | Health + Pension | Japan Pension Service | 50/50 employer-employee |

| Labor Insurance (労働保険) | Workers’ Comp + Employment | MHLW / Hello Work | Mixed (see details) |

| Residence Tax (住民税) | Municipal + Prefectural | Local city/ward offices | 100% employee |

All incorporated entities (KK or GK) must enroll in social insurance from day one — even with a single employee-director. Sole proprietors must enroll once they have five or more regular employees.

Warning

Japan does not provide grace periods for new hires. Social insurance enrollment must be submitted within 5 days of the employment start date. Labor insurance enrollment must be filed within 10 days. Missing these deadlines delays the employee’s health insurance card and flags your company during audits.

2. Income Tax Withholding (源泉徴収 / Gensen Choshu)

Japan operates a Pay-As-You-Earn (PAYE) system. As the employer, you are the legally designated withholding agent and bear strict liability for calculating, deducting, and remitting income tax from each employee’s salary. The deadline is the 10th of the month following payment.

The Three Withholding Tax Columns

How much you withhold depends on which column (欄) of the NTA’s official Withholding Tax Tables applies to each employee:

| Column | Japanese Name | When It Applies | Rate Level |

|---|---|---|---|

| Column 1 | 甲欄 (Kou-ran) | Employee submitted Dependent Exemption form → primary employer | Lowest (includes exemptions) |

| Column 2 | 乙欄 (Otsu-ran) | No form submitted → secondary job | High (no exemptions) |

| Column 3 | 丙欄 (Hei-ran) | Day laborers / temp workers (contract < 2 months) | Simplified daily rate |

Tip

Collect the Dependent Exemption form (扶養控除等申告書) from every primary employee before running the first payroll — even if they have zero dependents. Without this form, you must apply the much higher Otsu-ran rates, severely cutting into the employee’s take-home pay.

2026 Progressive Income Tax Rates

The underlying national income tax brackets (reflected in the monthly withholding tables) are as follows:

| Taxable Income (JPY) | Marginal Rate |

|---|---|

| Up to 1,950,000 | 5% |

| 1,950,001 – 3,300,000 | 10% |

| 3,300,001 – 6,950,000 | 20% |

| 6,950,001 – 9,000,000 | 23% |

| 9,000,001 – 18,000,000 | 33% |

| 18,000,001 – 40,000,000 | 40% |

| Over 40,000,000 | 45% |

A 2.1% Special Reconstruction Surtax is added on top of the calculated income tax through 2037. The standard basic deduction is 620,000 yen but phases out for incomes above 23.5 million yen.

Year-End Adjustment (年末調整 / Nenmatsu Chousei)

Unlike many Western countries, Japan requires employers to perform the annual tax reconciliation for most employees. If an employee earns less than 20 million yen and has no significant secondary income, the employer must:

- Recalculate the total annual income tax in December

- Process deductions (life insurance, earthquake insurance, spousal, dependent, mortgage interest, etc.)

- Refund overpayments or collect shortfalls in the December/January paycheck

- Issue a Withholding Certificate (源泉徴収票 / gensen choshu-hyo) by January 31

This means most salaried employees in Japan never file their own tax return — the employer handles everything.

Non-Resident Employees

Employees classified as non-residents (generally less than one year in Japan) are excluded from progressive tax tables and the year-end adjustment. Instead, a flat 20.42% withholding rate applies to all Japan-sourced employment income with no deductions or exemptions allowed.

3. Social Insurance (健康保険 & 厚生年金 / Shakai Hoken)

Social insurance is the most expensive employer obligation — and the one most likely to shock foreign business owners accustomed to different systems. The employer and employee each pay roughly half of the total premium.

How Premiums Are Calculated

Premiums are not based on each month’s actual salary. Instead, Japan uses the Standard Monthly Remuneration (標準報酬月額 / hyoujun hoshu geppaku) system:

- Every July, submit the Santei Kiso Todoke (算定基礎届) averaging April-May-June pay

- This average is mapped to a standardized bracket

- The bracket determines premiums from September through August of the following year

- Bonuses are assessed separately at time of payout

2026 Premium Rates

| Component | Total Rate | Employer Share | Employee Share |

|---|---|---|---|

| Health Insurance (健康保険) | ~10.28%* | 5.14% | 5.14% |

| Nursing Care (介護保険, ages 40-64) | 1.62% | 0.81% | 0.81% |

| Employees’ Pension (厚生年金) | 18.30% | 9.15% | 9.15% |

| Childcare Premium (子ども・子育て拠出金) | 0.36% | 0.36% | 0% |

| Child Support Fund (new 2026) | 0.23% | 0.115% | 0.115% |

*Health insurance rates vary by prefecture and insurer. The rate shown is the 2026 Kyokai Kenpo benchmark rate.

Part-Time Employee Coverage Expansion

As of 2026, companies with 51 or more enrolled employees must enroll part-time workers who meet all four criteria:

- Work at least 20 hours per week

- Base monthly salary is at least 88,000 yen (excluding overtime, bonuses, commuting)

- Expected employment duration exceeds 2 months

- Not a day student

Warning

Crossing the 51-employee threshold forces your company to absorb approximately 15% additional labor cost for part-time workers who become eligible for social insurance. The government plans to eventually eliminate the company-size threshold entirely, extending this to all employers by 2035.

4. Labor Insurance (労災保険 & 雇用保険 / Roudou Hoken)

Labor insurance operates separately from social insurance and uses a unique annual estimation and reconciliation cycle rather than monthly premium billing.

Workers’ Compensation (労災保険 / Rousai Hoken)

Workers’ compensation covers medical expenses, lost wages, and disability or death benefits from work-related or commuting accidents.

- 100% employer-funded — nothing is deducted from employees

- Rate determined by industry risk: 0.25% to 8.8% of total payroll

- Office work: approximately 0.3%

- Construction, manufacturing, forestry: significantly higher

Employment Insurance (雇用保険 / Koyou Hoken)

Employment insurance funds unemployment benefits, childcare leave stipends, and worker reskilling programs. For 2026, the MHLW reduced the rates:

| Industry Type | Total Rate | Employee Share | Employer Share |

|---|---|---|---|

| General business (tech, retail, services) | 1.35% | 0.50% | 0.85% |

| Construction | 1.65% | 0.60% | 1.05% |

Annual Renewal (年度更新 / Nendo Koushin)

Labor insurance operates on an annual estimation cycle. Between June 1 and July 10 each year, employers must:

- Calculate the exact total wages paid in the previous fiscal year (April-March)

- Reconcile against the estimated premium paid at the start of that year

- Project wages for the upcoming year and pay the new estimated premium

If your workforce grew rapidly, you may owe a large reconciliation deficit plus the new estimated premium, creating a significant cash-flow hit in July.

5. Residence Tax Special Collection (住民税特別徴収)

Residence tax (住民税 / juuminzei) is a flat 10% on taxable income, assessed by local municipalities. It operates on a severely lagging timeline that confuses many foreign employers and employees.

How It Works

- Based entirely on the previous calendar year’s income

- Determined by where the employee is registered as of January 1

- In May, the municipal office sends the employer a notice with exact monthly deduction amounts

- The employer deducts and remits from June through May of the following year

- Payment must be remitted to each employee’s municipality by the 10th of the following month

Tip

If employees live in multiple municipalities, you must remit separately to each city/ward office. This adds significant logistical complexity for companies with geographically dispersed teams. Consider using payroll software that automates multi-municipality remittance.

When Employees Leave Japan

When a foreign employee departs Japan permanently, the employer must:

- Collect the remaining balance of the current residence tax cycle as a lump sum from the final paycheck

- Ensure the employee appoints a Tax Representative (納税管理人 / nozei kanrinin) to receive and pay tax bills for the current year’s income (billed the following June)

6. Hiring Foreign Nationals

Employing foreign nationals adds immigration compliance on top of standard payroll obligations. Getting this wrong can jeopardize your company’s ability to sponsor future visas.

Visa Alignment

The employee’s Status of Residence must precisely match their actual job duties. Assigning an “Engineer/Specialist in Humanities” visa holder to manual labor or unapproved tasks is a serious violation that can lead to visa revocation and criminal penalties for the employer.

Mandatory Notifications

Both the employer and the foreign employee must submit the Notification of the Contracting Organization (契約機関に関する届出) to the Immigration Services Agency within 14 days of hiring or termination. This requires:

- The company’s 13-digit corporate number

- Date of hiring/termination

- Employee’s residence card details

My Number (マイナンバー) Handling

You must collect the employee’s 12-digit My Number for social insurance, employment insurance, and tax filings. However, Japan’s privacy law imposes strict requirements:

- Explicitly notify employees of the statutory purpose for collection

- Store My Number data separately from general HR records

- Use encrypted storage accessible only to designated payroll administrators

- Never use My Number as a general employee ID

Warning

Unauthorized sharing, leakage, or misuse of My Number data carries severe civil and criminal penalties. Requesting another person’s number without statutory authorization is prohibited by law.

Equal Treatment Requirements

Japanese labor law applies equally to all workers regardless of nationality. Employers are prohibited from confiscating passports or residence cards, and must provide identical statutory benefits (health insurance, paid leave, workers’ comp, dismissal protections) to foreign and Japanese employees alike.

Payroll compliance for foreign employers is complex. A bilingual tax accountant can handle your withholding, social insurance filings, and year-end adjustments. Get matched free →

7. The Annual Payroll Calendar

Japan’s payroll cycle is not a simple monthly routine — it has critical seasonal deadlines that carry severe penalties if missed.

| Month | Key Deadline | Action Required |

|---|---|---|

| January | Jan 31 | Issue Withholding Certificates (源泉徴収票) to all employees; file salary payment reports to municipalities |

| Feb-Mar | Feb 16 – Mar 15 | Individual tax filing period (for high earners, employees with secondary income) |

| April | Apr 1 | New fiscal year begins; revised insurance rates and labor law changes take effect |

| May | Mid-May | Receive residence tax notices from municipalities with new deduction amounts |

| June | June payroll | Start new 12-month residence tax deduction cycle |

| July | Jul 10 | Labor Insurance annual renewal (Nendo Koushin); Social Insurance standard remuneration report (Santei Kiso Todoke) |

| September | Sept payroll | Apply new Social Insurance premium brackets (locked for 12 months) |

| December | Dec payroll | Year-End Tax Adjustment (年末調整) — reconcile annual income tax, process deductions, refund/collect differences |

| Monthly | 10th of following month | Remit withheld income tax and residence tax |

| Monthly | End of following month | Social insurance premiums due via direct debit |

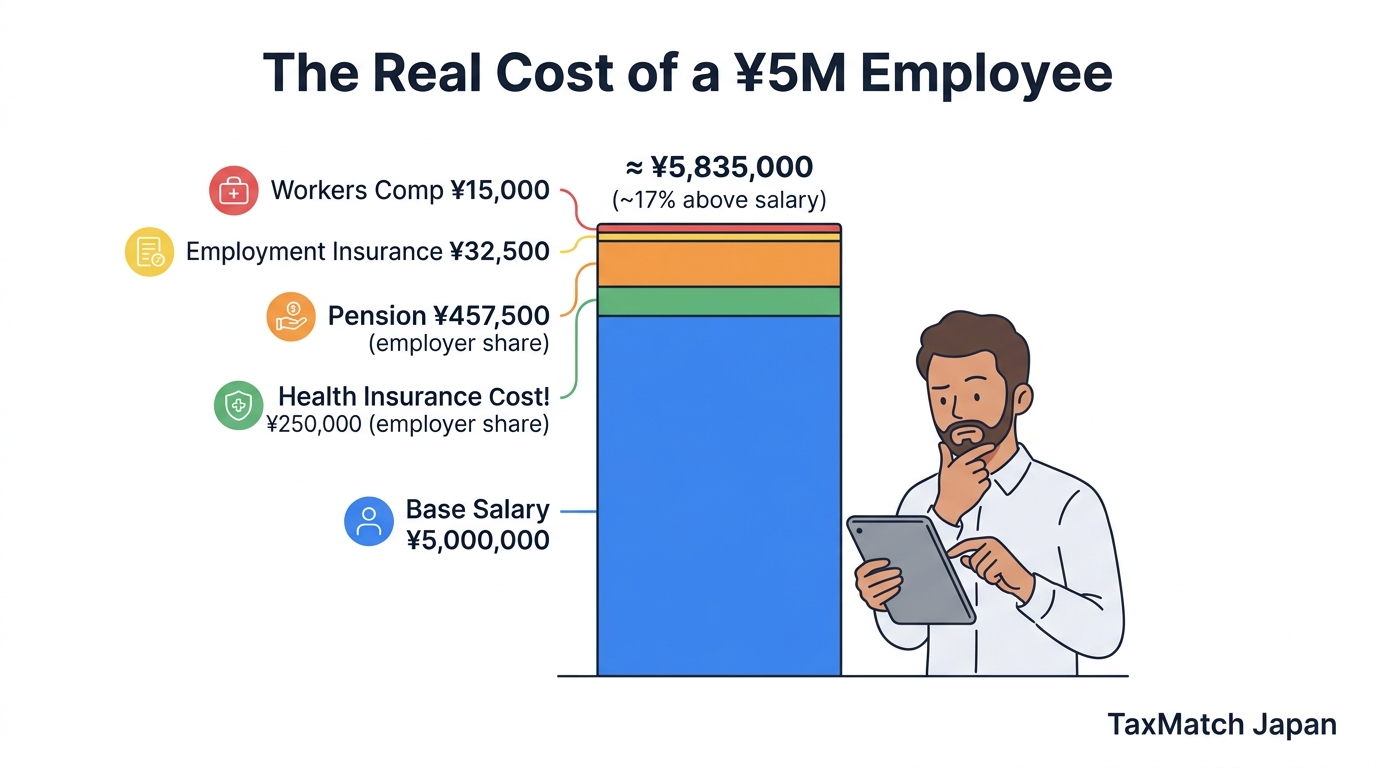

8. Cost Simulation: True Employer Burden

The real cost of a ¥5M employee

The biggest budgeting mistake foreign employers make is equating headcount cost with gross salary. Here is the real cost of a standard employee earning 5,000,000 yen per year (approximately 416,667 yen/month) in 2026:

| Cost Category | Who Pays | Rate | Annual Cost (JPY) |

|---|---|---|---|

| Base Gross Salary | — | — | 5,000,000 |

| Health Insurance | 50/50 | 5.14% | 257,000 |

| Nursing Care (age 40+) | 50/50 | 0.81% | 40,500 |

| Employees’ Pension | 50/50 | 9.15% | 457,500 |

| Childcare Premium | Employer only | 0.36% | 18,000 |

| Child Support Fund | 50/50 | 0.115% | 5,750 |

| Employment Insurance | Employer portion | 0.85% | 42,500 |

| Workers’ Comp (office) | Employer only | 0.30% | 15,000 |

| TOTAL EMPLOYER COST | ~16.7% | 5,836,250 |

Key Takeaway

A 5,000,000 yen salary actually costs the employer approximately 5,836,250 yen — a 16.7% markup. Budget approximately 115-117% of gross salary for total employer cost. Social insurance premiums are collected via direct debit and failure to maintain sufficient cash flow can result in bank account garnishment by the Japan Pension Service.

9. Common Mistakes (And How to Avoid Them)

Mistake 1: Misclassifying Workers as Independent Contractors

The problem: To avoid the ~16% social insurance markup, some employers classify workers as independent contractors (業務委託 / gyomu itaku) instead of employees (雇用契約 / koyo keiyaku).

The consequences: Japan applies a strict “economic reality” test. If the worker has fixed hours, uses company equipment, takes direct instructions, and cannot refuse assignments, they are legally an employee. Reclassification during an audit means up to 2 years of backdated social insurance premiums — both the employer’s and the employee’s portions — plus penalties and late fees.

Mistake 2: Wrong Withholding Tax Column

The problem: Failing to collect the Dependent Exemption form and accidentally taxing primary employees under the higher Otsu-ran column, or vice versa.

The fix: Build the form into your onboarding checklist and collect it before the first payroll run. Even employees with zero dependents must submit this form.

Mistake 3: Incorrect Overtime Calculations

The problem: Japan mandates escalating, compounding overtime multipliers that foreign payroll systems often handle incorrectly:

- Standard overtime (beyond 8 hrs/day or 40 hrs/week): 1.25x

- Holiday work: 1.35x

- Late-night work (10 PM – 5 AM): additional 0.25x premium

- Late-night overtime: multipliers stack to 1.5x

The fix: Use Japan-localized payroll software that handles compounding multipliers. The 2026 Labor Standards Act reforms also introduce a 14-day consecutive work limit and mandatory 11-hour inter-shift rest periods.

Mistake 4: Missing Social Insurance Enrollment Deadlines

The problem: Social insurance enrollment must be submitted within 5 days of the employment start date. Missing this delays the employee’s health insurance card and flags your company.

The fix: Have enrollment forms pre-prepared and submit them on the employee’s first day.

Mistake 5: Ignoring Departure Obligations for Foreign Employees

The problem: When a foreign employee leaves Japan, they owe residence tax in arrears — both the remaining current cycle and the unbilled tax on the current year’s income.

The fix: Collect remaining residence tax as a lump sum from the final paycheck, and ensure the departing employee appoints a Tax Representative before leaving Japan.

10. When to Hire a Tax Accountant

You can manage basic payroll with localized software for a small team, but seriously consider hiring a bilingual tax accountant (税理士) or labor consultant (社会保険労務士) if:

- You’re hiring your first employee and need to set up withholding, social insurance, and labor insurance registrations correctly from day one

- You have foreign national employees and need to navigate visa reporting, My Number compliance, and non-resident tax rules

- You’re approaching the 51-employee threshold and need to plan for expanded part-time social insurance coverage

- You need to perform the Year-End Adjustment and process complex deductions (mortgage interest, insurance premiums, dependent changes)

- An employee is leaving Japan and you need to handle lump-sum residence tax collection and tax representative appointment

- You received a notice from the Pension Service or Labor Standards Office about enrollment or compliance issues

- You want to ensure your contractor classifications will withstand an audit

A bilingual tax accountant who understands the challenges foreign employers face can save you far more than their fee in avoided penalties, correct insurance enrollments, and proper year-end adjustments. See our pricing guide for typical fee ranges.

Need help with payroll and employment tax? Get matched with an English-speaking tax accountant who handles employer obligations — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

What payroll taxes do employers pay in Japan?

Employers in Japan pay approximately 15-16% of each employee’s salary in social insurance contributions (health insurance, pension, unemployment insurance, workers’ compensation, and nursing care insurance). These are in addition to the employee’s own contributions of approximately 14-15%.

How does social insurance work for foreign employees?

Foreign employees in Japan are enrolled in the same social insurance system as Japanese employees. This includes health insurance, employees’ pension, employment insurance, and workers’ compensation. Totalization agreements with certain countries prevent double coverage.

What are the costs of hiring an employee in Japan?

Beyond the gross salary, employers should budget an additional 15-16% for social insurance, plus costs for workers’ compensation insurance, commuting allowances, and potential bonuses (typically 2-4 months’ salary per year). Total employer cost is typically 130-145% of the base salary.