KK vs GK: Starting a Company in Japan as a Foreigner (2026)

Every year, thousands of foreign residents in Japan take the leap from employee or freelancer to business owner. Whether you are launching a startup, formalizing a consulting practice, or structuring a business to qualify for a Business Manager visa, the first major decision you face is: what type of company should you form? Japan offers two main corporate structures — the Kabushiki Kaisha (KK) and the Godo Kaisha (GK). Choosing the wrong one can cost you unnecessary fees, create governance headaches, or even complicate your visa renewal.

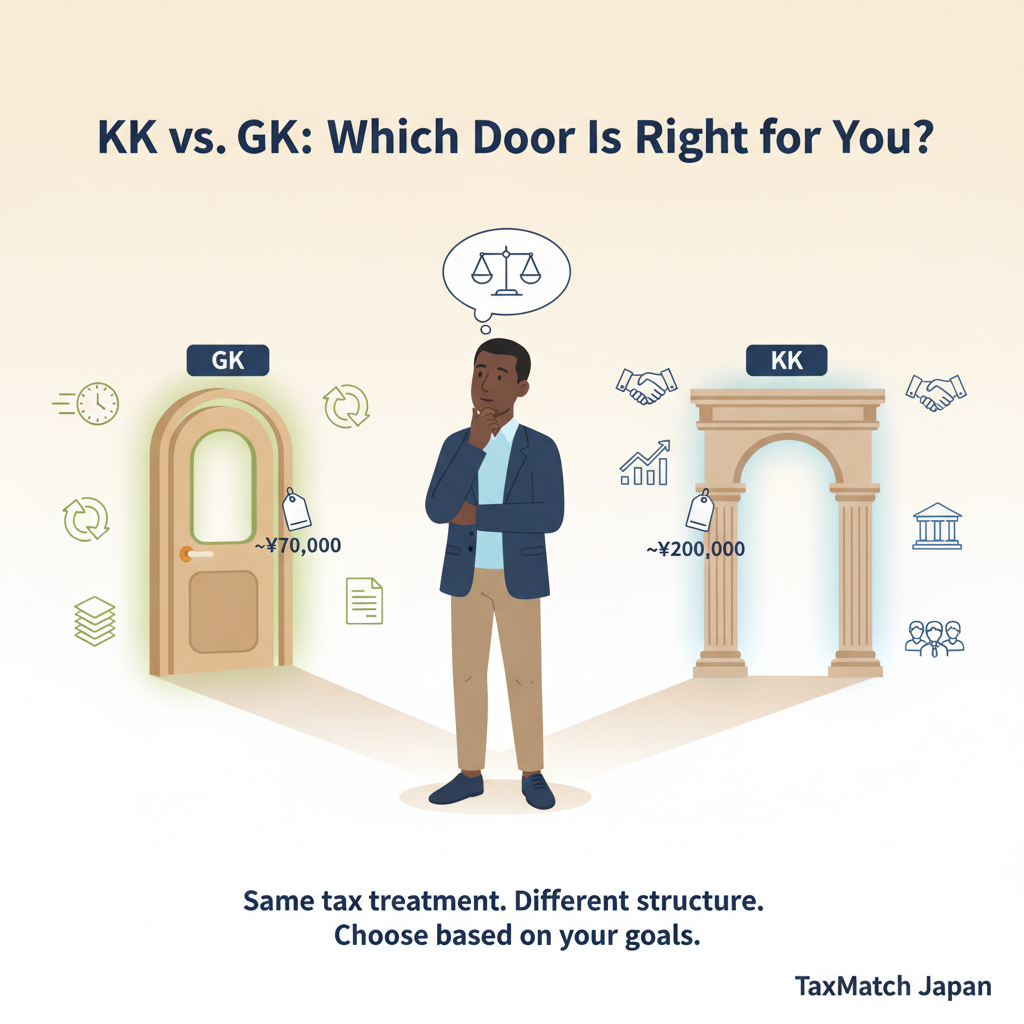

KK vs GK: Which door is right for you?

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax rules and rates may change. Always consult a qualified tax professional (zeirishi) for advice specific to your situation.

Need a bilingual tax accountant? Get matched with a specialist — free.

Table of Contents

- The Business Structure Ladder in Japan

- GK (Godo Kaisha): The Lean Option

- KK (Kabushiki Kaisha): The Standard Corporation

- KK vs GK: Side-by-Side Comparison

- Tax Comparison: GK and KK Are Identical

- Business Manager Visa Considerations

- Practical Setup Steps

- When to Hire a Tax Accountant

- Frequently Asked Questions

1. The Business Structure Ladder in Japan

Before diving into KK vs GK, it helps to understand the three levels of business structure available to foreigners in Japan:

Kojin Jigyo (個人事業主) — Sole Proprietorship

The simplest option. You file a one-page notification at the tax office and start operating under your own name. There is no separate legal entity — you and the business are the same.

Best for: Freelancers earning under 7-8 million yen per year who already hold a valid work visa (e.g., Engineer/Specialist in Humanities, Spouse visa). For a detailed comparison of sole proprietorship vs incorporation, see our sole proprietor vs corporation guide.

Limitation: You cannot sponsor a Business Manager visa as a sole proprietor. If your visa status depends on running a business, you need to incorporate.

Godo Kaisha (GK) — The LLC Equivalent

A separate legal entity with limited liability, similar to a US LLC or UK LLP. It is the faster and cheaper incorporation option.

Kabushiki Kaisha (KK) — The Corporation

Japan’s most recognized corporate structure, equivalent to a US C-Corp or UK Ltd. It carries the highest prestige and is the default choice for companies that plan to scale.

The progression most foreign entrepreneurs follow is: start as Kojin Jigyo, incorporate as a GK when revenue grows or a visa requires it, then convert to a KK if the business scales significantly.

2. GK (Godo Kaisha): The Lean Option

The Godo Kaisha was introduced in Japan’s 2006 Companies Act and is modeled after the American LLC. It is designed for smaller, owner-operated businesses that want limited liability without heavy governance requirements.

Setup Costs

| Item | Cost |

|---|---|

| Registration tax (登録免許税) | 60,000 yen |

| Company seal (inkan) set | 5,000 – 15,000 yen |

| Articles of organization | No notarization required |

| Judicial scrivener fee (optional) | 50,000 – 80,000 yen |

| Total (DIY) | ~70,000 yen |

| Total (with professional help) | ~130,000 – 160,000 yen |

Advantages

- Low cost: Registration tax is just 60,000 yen — one-third of a KK

- No notarization needed: Articles of organization do not need to be notarized, saving both time and the 52,000 yen notary fee

- Flexible profit distribution: Profits can be distributed in any ratio agreed upon by the members, regardless of capital contribution. This is a major advantage for partnerships where one person contributes expertise and another contributes capital

- Simpler governance: No board of directors, no shareholder meetings, no statutory auditor required

- Faster to establish: The entire process can be completed in 1-2 weeks

- Same tax treatment: A GK is taxed identically to a KK under Japanese corporate tax law

Disadvantages

- Lower name recognition: Many Japanese businesses and banks are less familiar with the GK structure. Some older or more traditional companies may view it as less serious

- Harder to raise investment: Venture capital firms and angel investors strongly prefer KK structures because of the share-based equity system

- Conversion cost: If you later decide to convert to a KK, it requires a full organizational change (組織変更) process that costs approximately 100,000 – 200,000 yen in fees and takes several weeks

- Member-managed by default: All members (investors) have management rights unless the articles specify otherwise, which can create conflicts

3. KK (Kabushiki Kaisha): The Standard Corporation

KK vs GK: Setup Cost Breakdown

The Kabushiki Kaisha is Japan’s flagship corporate structure. The vast majority of Japanese companies — from Toyota to the ramen shop down the street — are KKs. It is the default, trusted, and universally recognized business form.

Setup Costs

| Item | Cost |

|---|---|

| Registration tax (登録免許税) | 150,000 yen (or 0.7% of capital, whichever is higher) |

| Notarization of articles (定款認証) | 30,000 – 52,000 yen |

| Revenue stamps (if paper filing) | 40,000 yen (0 yen if electronic) |

| Company seal (inkan) set | 5,000 – 15,000 yen |

| Judicial scrivener fee (optional) | 60,000 – 100,000 yen |

| Total (DIY, electronic) | ~200,000 – 220,000 yen |

| Total (with professional help) | ~250,000 – 350,000 yen |

Advantages

- Maximum credibility: The “株式会社” (KK) prefix or suffix on your company name carries weight with banks, clients, landlords, and government agencies

- Easier hiring: Japanese job seekers strongly prefer working for a KK. If you plan to hire local staff, this matters

- Investment-ready: KKs issue shares, making equity financing, stock options, and eventual M&A straightforward

- Banking: Some banks are more willing to open corporate accounts for KKs than GKs, particularly for foreign-owned entities

- Visa applications: While immigration law does not technically require a KK, some immigration officers view KK applications more favorably (see the visa section below)

Disadvantages

- Higher setup cost: Roughly 3x more expensive than a GK to establish

- Notarization required: Articles of incorporation must be notarized at a public notary office, adding time and cost

- Stricter governance: Annual shareholder meetings are required, even if you are the sole shareholder. Changes to the articles of incorporation require special resolutions

- Rigid profit distribution: Dividends must be distributed in proportion to shareholding — no flexibility like the GK offers

- Minimum annual tax: Even with zero profit, you owe a minimum of ~70,000 yen in local per-capita taxes (均等割). This applies to GKs as well

Section Summary

- GK setup: ~70,000 yen (DIY) vs KK setup: ~200,000 yen (DIY) — roughly 3x difference

- GK offers flexibility and speed; KK offers credibility and investment readiness

- Both provide limited liability and identical tax treatment

4. KK vs GK: Side-by-Side Comparison

KK vs GK: Quick Comparison for foreign entrepreneurs

| Factor | GK (Godo Kaisha) | KK (Kabushiki Kaisha) |

|---|---|---|

| Registration tax | 60,000 yen | 150,000 yen+ |

| Total setup cost (DIY) | ~70,000 yen | ~200,000 yen |

| Notarization | Not required | Required (~30,000-52,000 yen) |

| Setup time | 1-2 weeks | 2-4 weeks |

| Legal liability | Limited | Limited |

| Corporate tax rate | Same as KK | ~15-23.2% national + local |

| Profit distribution | Flexible (any ratio) | Proportional to shares only |

| Governance | Minimal | Shareholder meetings, board optional |

| Name recognition | Lower | Highest |

| Hiring appeal | Moderate | Strong |

| Investor friendliness | Low | High |

| Business Manager visa | Acceptable | Preferred |

| Conversion | Can convert to KK later | N/A |

Rule of thumb: Choose a GK if you are a solo founder or small partnership focused on keeping costs low. Choose a KK if you plan to hire Japanese employees, raise external investment, or want maximum credibility from day one.

5. Tax Comparison: GK and KK Are Identical

This surprises many people: there is zero tax difference between a GK and a KK. Both are treated as ordinary corporations (普通法人) under Japanese tax law and are subject to the same rates and rules.

Corporate Tax Rates (2026)

| Taxable Income | National Corporate Tax |

|---|---|

| Up to 8 million yen (SMEs) | 15% |

| Over 8 million yen | 23.2% |

When you add local corporate taxes (事業税, 住民税), the effective combined rate is approximately 30-34% depending on your prefecture and city.

Officer Compensation (役員報酬) — The Key Tax Strategy

The single most important tax planning tool for small corporation owners in Japan is officer compensation (役員報酬). As a director of your own company, you pay yourself a fixed monthly salary. This salary is:

- Deductible for the corporation (reduces corporate taxable income)

- Taxed as employment income on your personal return (which qualifies for the generous employment income deduction — 給与所得控除)

By carefully setting your officer compensation level, you can split income between the corporate and personal tax brackets to minimize total tax. A skilled tax accountant can optimize this split and potentially save you 500,000 to 1,000,000+ yen per year compared to a naive approach.

Warning

Important rule: Officer compensation must be set at the start of the fiscal year and kept constant for the entire year (定期同額給与). You cannot change it mid-year without tax consequences.

Need help setting the optimal officer compensation for your company? A bilingual tax specialist can help. Get matched free →

Consumption Tax (消費税)

Both GKs and KKs are exempt from consumption tax for up to two fiscal years after incorporation if:

- Capital is 10 million yen or less at the start of the fiscal year

- Taxable sales in the base period are under 10 million yen

This is one of the reasons some sole proprietors incorporate — to reset the consumption tax clock. However, recent rule changes (the Invoice System introduced in October 2023) have reduced this advantage for businesses with registered invoice numbers.

When Does Incorporating Save Money?

As a general rule, incorporation starts saving you tax when your business profit exceeds approximately 7-8 million yen per year. Below that level, the sole proprietor structure with Blue Form (青色申告) deductions is often more tax-efficient once you factor in the corporation’s minimum taxes and additional compliance costs. For a deeper analysis, see our sole proprietor vs corporation comparison.

Section Summary

- GK and KK have identical tax treatment — same corporate tax rates, same deduction rules

- Officer compensation is the most powerful tax planning tool for company owners

- Incorporation typically saves money when business profit exceeds ~7-8 million yen/year

6. Business Manager Visa Considerations

For many foreign entrepreneurs, the Business Manager visa (経営・管理ビザ) is the primary reason for incorporating. You cannot obtain this visa as a sole proprietor.

Key Requirements

- Capital investment: Typically 5 million yen or more, OR employment of two or more full-time residents of Japan

- Physical office: A dedicated office space with a real lease agreement. A home office or virtual office usually does not qualify

- Business plan: A credible, detailed business plan showing how the company will sustain itself

- Your role: You must be engaged in managing the business, not performing labor that could be done on a different visa category

Does KK vs GK Matter for Visa Applications?

Legally, immigration law does not specify KK or GK. Both are valid corporate structures for a Business Manager visa.

In practice, however, many immigration lawyers recommend a KK for first-time applicants because:

- Immigration officers are more familiar with KKs and may scrutinize GK applications more closely

- The perception of seriousness is higher with a KK

- If your business plan involves hiring employees or B2B contracts with Japanese companies, a KK strengthens the overall application

That said, thousands of Business Manager visas are granted to GK owners every year. If the cost difference matters to you and your business plan is solid, a GK is perfectly acceptable.

Capital Requirement Nuance

The 5 million yen capital does not need to stay in the company account permanently. It must be deposited and shown in a bank statement at the time of incorporation. After incorporation, you can use it for legitimate business expenses (office lease deposits, equipment, initial inventory, etc.).

However, immigration may check your company’s financial statements at renewal time. If the capital has been spent with no revenue to show for it, visa renewal becomes difficult.

7. Practical Setup Steps

Here is the step-by-step process for incorporating either a GK or KK in Japan:

Step 1: Prepare Your Company Seal (Inkan)

Every Japanese company needs at least one registered seal. Most companies order a set of three:

- Daihyo-in (代表印): The official registered company seal, used for contracts and legal filings

- Ginko-in (銀行印): The bank seal, used for financial transactions

- Kaku-in (角印): The square company stamp, used on invoices and routine documents

Order these online or at a local seal shop. Budget 5,000 – 15,000 yen for a set. Delivery takes 2-5 business days.

Step 2: Draft Articles of Incorporation (定款)

This document defines your company’s name, address, business purpose, fiscal year, capital amount, and governance structure.

- For a KK: The articles must be notarized at a public notary office (公証役場). If filed electronically, you save the 40,000 yen revenue stamp fee

- For a GK: No notarization required. The articles are filed directly with the Legal Affairs Bureau

Step 3: Deposit Capital

Open a personal bank account (if you do not already have one) and deposit the capital amount. The bank will not create a corporate account yet — you deposit into your personal account and obtain a deposit certificate (払込証明書) showing the amount and date.

For Business Manager visa applicants, 5 million yen is the standard minimum.

Step 4: Register at the Legal Affairs Bureau (法務局)

Submit your application package to the Legal Affairs Bureau (法務局) that covers your company’s registered address. The package includes:

- Application form

- Articles of incorporation (notarized, for KK)

- Capital deposit certificate

- Seal registration form

- Director consent forms

- Other supporting documents

Processing typically takes 7-10 business days. Your company officially exists on the date you submit the application (not the date it is processed).

Step 5: Post-Registration Notifications

After receiving your registration certificate, you must notify several government offices within specified deadlines:

| Notification | Deadline | Office |

|---|---|---|

| Corporate establishment notification (法人設立届出書) | Within 2 months | Tax office (税務署) |

| Blue form application (青色申告承認申請書) | Within 3 months | Tax office |

| Salary payer notification (給与支払事務所の届出) | Within 1 month | Tax office |

| Social insurance enrollment | Within 5 days | Pension office (年金事務所) |

| Labor insurance enrollment | Within 10 days (if hiring) | Labor Standards Office |

Warning

Missing these deadlines can result in penalties or the loss of valuable tax benefits (especially the Blue Form application). Mark these deadlines on your calendar immediately after registration.

Step 6: Open a Corporate Bank Account

This is often the most frustrating step for foreign business owners. Japanese banks are cautious about opening corporate accounts, especially for newly established companies with foreign directors.

Tips for a smoother experience:

- Apply at the branch nearest your registered office

- Bring all registration documents, your residence card, and your seal

- Prepare a clear business description in Japanese

- Consider online banks (e.g., GMO Aozora, PayPay Bank) as a backup — they tend to be more welcoming to new companies

- Expect the process to take 2-4 weeks

8. When to Hire a Tax Accountant

You can technically handle company formation yourself, especially for a GK. Many judicial scriveners (司法書士) offer affordable incorporation packages that handle the paperwork.

However, a tax accountant (税理士) becomes essential at these points:

- Setting officer compensation: Getting this wrong in your first fiscal year can cost you hundreds of thousands of yen in excess tax. A tax accountant calculates the optimal split between corporate and personal income based on your projected revenue

- First tax filing: Corporate tax returns in Japan are significantly more complex than personal returns. Most small companies file with professional help

- Consumption tax planning: Deciding whether and when to register as an invoice issuer requires careful analysis

- Visa renewals: Immigration often requests financial statements and tax certificates. A tax accountant ensures these documents are clean and consistent

The cost for a tax accountant to handle a small corporation’s monthly bookkeeping and annual tax filing typically ranges from 15,000 to 50,000 yen per month, depending on transaction volume and complexity. For an English-speaking tax accountant specializing in foreign-owned companies, expect the higher end of that range. See our tax accountant pricing guide for detailed fee breakdowns.

The investment typically pays for itself through optimized officer compensation alone.

Final Thoughts

- Start with a GK if you are cost-conscious, running a small operation, and do not need to impress Japanese corporate clients or investors. You can always convert to a KK later.

- Start with a KK if you plan to hire Japanese employees, pursue B2B contracts with larger Japanese companies, seek investment, or want the strongest possible foundation for a Business Manager visa application.

- Either way, the tax treatment is identical, and both structures provide limited liability protection. The real differences are cost, credibility, and flexibility.

Planning to start a company in Japan? Get matched with an English-speaking tax accountant who specializes in company formation — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

What is the difference between KK and GK in Japan?

A Kabushiki Kaisha (KK) is a stock company similar to a corporation, while a Godo Kaisha (GK) is a membership company similar to an LLC. KK offers higher credibility and easier fundraising; GK offers lower setup costs, simpler governance, and flexible profit distribution among members.

Which is better for foreigners: KK or GK?

For most small businesses and startups, a GK is more practical due to lower setup costs (¥60,000 vs ¥200,000+) and simpler management. Choose a KK if you plan to raise external investment, want higher brand credibility in Japan, or anticipate going public. Both qualify for Business Manager Visa.

How much does it cost to register a GK vs KK?

A GK costs approximately ¥60,000 in registration tax with no articles of incorporation certification fee. A KK costs approximately ¥200,000 in registration tax plus ¥50,000 for notarized articles of incorporation, totaling about ¥250,000. Professional fees for either are typically ¥100,000-300,000 additional.