Leaving Japan: Complete Tax & Financial Checklist for Foreign Residents | TaxMatch Japan

Leaving Japan involves a surprisingly complex series of tax and financial obligations — many with strict deadlines and significant financial consequences if missed. This is the complete checklist every foreign resident needs before their departure date.

Planning to leave Japan? Get expert guidance on pre-departure tax planning — free matching service.

Get Matched Free →Most foreign residents assume leaving Japan is simply a matter of canceling their residence registration and booking a flight. In reality, your Japan tax obligations can extend years beyond your departure date — and failing to handle them correctly before you leave can result in penalties, withheld refunds, or even legal complications. This checklist covers everything from 6 months before departure through your final tax filing.

Leaving Japan? Here is your tax checklist

Step 1: Check Your Tax Status on Departure

Leaving Japan: Tax Timeline — What to do and when

Are You a Tax Resident Until You Leave?

Japan taxes individuals as residents if they have a 住所 (jūsho) — their permanent, primary place of living — in Japan. You are a Japan tax resident from the day you arrive until the day you formally depart. This means:

- All worldwide income earned up to your departure date must be declared in Japan

- Income earned after your departure date (if you are no longer a Japan resident) is generally not subject to Japan income tax

- Japan-source income earned after departure (e.g., rental from Japan property, Japan company dividends) remains subject to Japan withholding tax

Non-Permanent Resident vs. Permanent Resident Status

If you have lived in Japan for 5 years or fewer out of the past 10 years, you are a Non-Permanent Resident (NPR). Under NPR status, only Japan-source income and foreign income remitted to Japan is taxed. This distinction matters for your final year tax return — ensure you understand which income you need to declare.

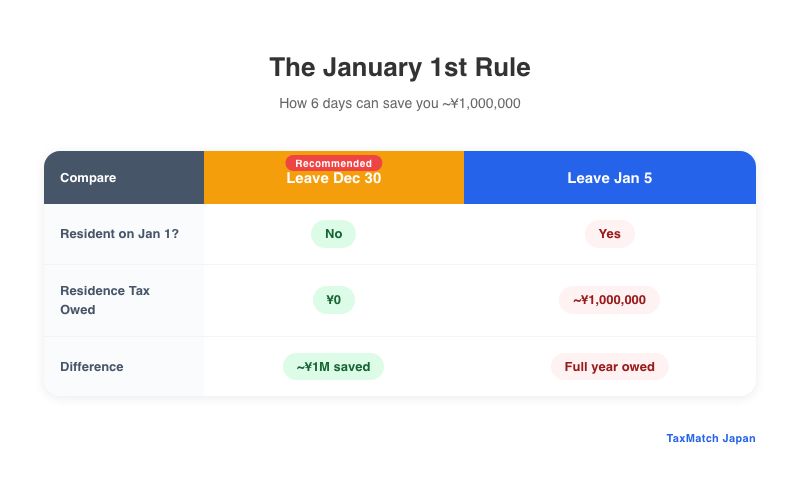

Step 2: The January 1 Rule — Timing Your Departure

The January 1st Rule: How 6 days can save you ~¥1,000,000

📌 One of the Most Valuable Tax Planning Moves: Leave Before December 31

Japan’s local inhabitant tax (住民税) is assessed based on whether you are a Japan resident as of January 1 of the tax year. If you are registered as a Japan resident on January 1, you owe the full year’s local inhabitant tax (typically 10% of the prior year’s income) — even if you leave Japan on January 2nd.

If you depart Japan before December 31, you will not be a Japan resident on the next January 1, and you will not owe local inhabitant tax for the upcoming year. For someone earning ¥10M annually, this saves approximately ¥1,000,000. On investment gains or RSU income in the millions, the savings can be dramatically higher.

Example: The Cost of a January vs. December Departure

| Depart December 30, 2025 | Depart January 5, 2026 | |

|---|---|---|

| Japan residency on January 1, 2026 | No | Yes |

| Local inhabitant tax for 2026 (on 2025 income) | Not owed | Full year owed (~¥1M on ¥10M income) |

| Difference | ~¥1,000,000 savings by leaving 6 days earlier | |

Step 3: Exit Tax — Do You Qualify?

Japan’s exit tax (国外転出時課税) applies if you meet both conditions:

- Asset threshold: You hold ¥100 million or more in specified financial assets (stocks, mutual funds, bonds — NOT real estate or cash)

- Residency duration: You have held a Table 2 visa (Permanent Resident, Spouse of Japanese National, Long-Term Resident) for a cumulative total of 5+ years out of the past 10 years

If you meet both conditions, see our dedicated Exit Tax guide for full details on calculation, deferral options, and planning strategies. Key point: appoint a tax representative (納税管理人) before leaving Japan to preserve your deferral options.

Step 4: Final Japan Tax Return (準確定申告 or 確定申告)

Who Must File a Final Return?

You must file a Japan income tax return for your final year of residence if:

- You had income beyond employment income subject to year-end adjustment (年末調整)

- You had freelance, investment, or rental income

- You are claiming the exit tax deduction or any special deductions

- You overpaid taxes and want a refund (highly recommended — most departing employees are due refunds)

Filing Deadline for Departing Residents

| Situation | Filing Deadline |

|---|---|

| Standard departing resident (appoint tax representative) | March 15 of the following year (same as regular filing) |

| Departing without tax representative | Before your departure date (you must file and pay all tax before boarding) |

| Deceased (準確定申告 / Quasi-Final Return) | Within 4 months of the date of death |

⚠️ Appoint a Tax Representative — This Is Not Optional If You Want a Refund

A 納税管理人 (tax representative) is a Japan-based person (typically your accountant, or a trusted individual) who manages your tax obligations after you leave. Without one, you must file and settle all taxes before departure — and the NTA will use an asset valuation date 3 months before your departure (not your actual departure date), which may result in higher taxes on appreciated assets. With a tax representative, you file by March 15 of the following year using actual departure-date values.

Step 5: Pension Lump-Sum Withdrawal (脱退一時金)

If you contributed to Japan’s national pension (国民年金) or employee’s pension (厚生年金) as a foreign resident, you are entitled to a lump-sum withdrawal (脱退一時金) after leaving Japan — provided you do not have Japanese nationality and have not met the full pension eligibility requirements.

Eligibility and Amount

| Factor | Details |

|---|---|

| Minimum contribution period | 6 months of contributions |

| Maximum claimable period | 60 months (5 years) for 国民年金; 60 months for 厚生年金 |

| Application window | Within 2 years of leaving Japan (after losing Japan residency) |

| Withholding tax rate | 20.42% withheld at source by the Japan Pension Service (日本年金機構) |

| Refund of withholding | You can claim a refund of 80% of the withheld tax by filing a designated form within 1 year of the payment decision |

📌 The 80% Tax Refund: How It Works

When you receive your lump-sum payment, 20.42% is withheld. However, for amounts covered by a tax treaty or where the effective tax rate should be lower, you can immediately apply to recover 80% of the withheld amount — meaning your net effective tax is approximately 4% of the lump-sum. This refund claim must be filed within 1 year of the pension service’s payment decision. Miss this window and the withheld tax is forfeited.

Action: Appoint a tax representative to handle the refund claim after you leave, and ensure they have power of attorney to receive correspondence from the Japan Pension Service.

Countries with Social Security Totalization Agreements

If your country has a totalization agreement with Japan (including the US, UK, Germany, Australia, Canada, South Korea, China, and others), pension periods in Japan may be combined with your home country for eligibility purposes. In some cases, claiming the lump-sum withdrawal forfeits your ability to use Japan pension years in home-country totalization. Seek advice before applying.

Step 6: National Health Insurance (NHI) and Employee Health Insurance

Canceling NHI (国民健康保険)

If you are on NHI (self-employed or not covered by employer), cancel your NHI enrollment at your local municipal office (市区町村) on or around your departure date. Bring your NHI card. You will receive a statement of cancellation which may be needed for your tax return.

Employee Health Insurance (健康保険)

If you are employed, your employer handles health insurance termination when your employment ends. However, if your employment ends before your departure, you may choose to continue enrollment (任意継続) for up to 2 years. The premium is the full amount (approximately double what you paid as an employee) — this is rarely worthwhile for departing residents.

Outstanding NHI Premiums

Any unpaid NHI premiums remain legally owed after departure. Unpaid amounts can be collected from your tax refunds and may affect visa applications for future Japan re-entry.

Step 7: Banking and Investment Accounts

Japanese Bank Accounts

You are technically not allowed to maintain Japan bank accounts as a non-resident (though in practice, accounts are often maintained for months or years). Options:

- Close the account before departure: Simplest option; transfer funds overseas and close

- Maintain the account: Inform your bank of your change to non-resident status; they will convert it to a non-resident account. Allowed under most banks’ policies. Required for pension lump-sum refund deposits and tax refunds.

- Do NOT simply leave without notifying the bank: Interest accruals and eventual dormancy fees create complications

NISA Accounts

⚠️ NISA Loses Tax-Free Status When You Leave Japan

Japan’s NISA tax-exempt status applies only to Japan residents. When you depart Japan and lose resident status, your NISA account must be closed or transferred to a regular taxable account within 3 months of your departure. If you fail to notify your NISA provider, they will automatically convert your NISA to a taxable account — and any future gains will be taxed. Critically, unrealized gains in your NISA at the time of conversion become taxable when you eventually sell.

iDeCo (Individual Defined Contribution Pension)

iDeCo contributions must stop when you lose Japan resident status. Your accumulated iDeCo balance remains invested until you reach the eligible withdrawal age (currently 60-75, depending on enrollment duration). You cannot make withdrawals as a non-resident in most circumstances. Consult your iDeCo provider for your options.

Japanese Brokerage Accounts

Most Japanese securities companies will close brokerage accounts for non-residents. You must sell or transfer your holdings before departure, or arrange a transfer to a foreign brokerage. Note: selling Japanese securities before departure triggers Japan capital gains tax in the usual way (20.315%).

Step 8: Residence Deregistration (転出届)

File a 転出届 (tenshutsu todoke) — moving-out notification — at your local municipal office. This:

- Cancels your residence registration (住民票)

- Returns your Residence Card (在留カード) — it is cut or cancelled at the airport upon departure

- Triggers the start of your non-resident status for municipal tax purposes

- Can be done up to 2 weeks before your departure date, or on the day you leave

⚠️ Do Not Deregister Too Early

Some residents deregister months before departure to avoid local inhabitant tax. Japanese authorities view this as tax avoidance if your actual residence remains in Japan. The standard approach is to deregister on or near your actual departure date. Tax authorities can challenge deregistrations that do not reflect actual departure.

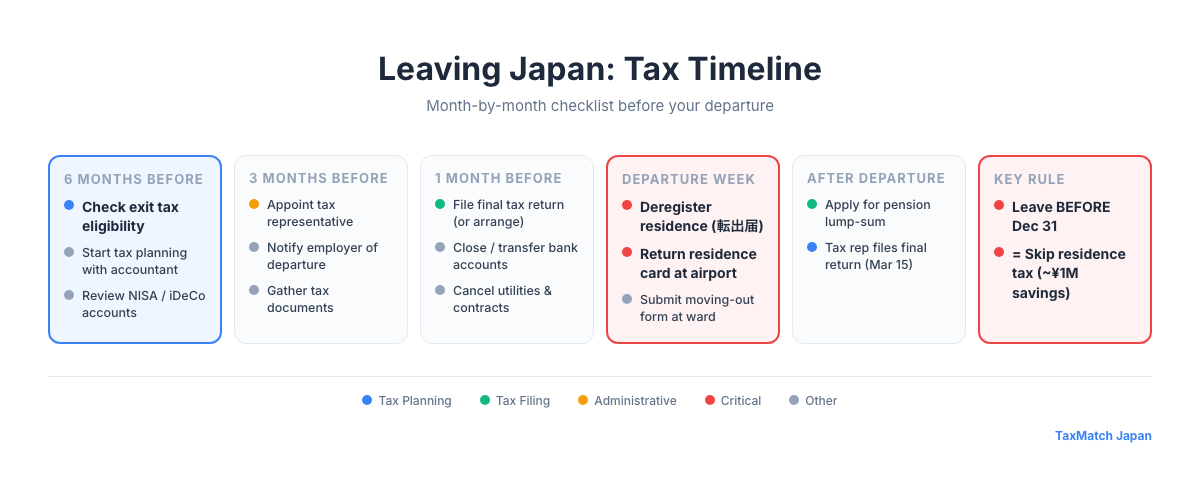

Month-by-Month Departure Timeline

| Timing | Actions |

|---|---|

| 6 months before | Assess exit tax exposure (¥100M threshold check). Review NISA, iDeCo, brokerage accounts. Calculate cost of January 1 departure timing. Consider pension lump-sum eligibility. |

| 3 months before | Appoint a tax representative (納税管理人). Notify employer of departure date. Begin estate/asset valuation if exit tax applies. Start unwinding or transferring financial accounts. |

| 1 month before | Close or convert NISA account. Notify bank of non-resident status change. Close brokerage account or arrange overseas transfer. Cancel utility subscriptions and recurring payments. |

| Departure week | File 転出届 at municipal office. Return Residence Card at airport. Collect all tax documents for final year return. |

| By March 15 (following year) | File final Japan income tax return (via tax representative). Pay any taxes owed. Claim exit tax deferral if applicable. Apply for pension lump-sum withdrawal. |

| Within 1 year of pension payment | Apply for 80% refund of withheld pension lump-sum tax (via tax representative). |

4 Common Mistakes When Leaving Japan

- Leaving without appointing a tax representative — Forces you to file and pay all taxes before boarding, often at unfavorable valuations. And you lose deferral rights for exit tax.

- Forgetting the 2-year pension lump-sum window — Many expats leave, forget about it, and miss the 2-year deadline. At 5 years of contributions, this can be ¥500,000–¥2,000,000+ depending on your contribution history.

- Not closing or converting NISA within 3 months — The automatic conversion to a taxable account creates complex tax complications and costs future gains their tax-free status permanently.

- Ignoring the January 1 rule — Departing in early January instead of late December costs a full year of local inhabitant tax (10% of prior year income). For high earners, this mistake costs millions of yen for a few days of difference.

📝 Complete Pre-Departure Checklist

- Check exit tax eligibility (¥100M threshold + Table 2 visa 5-year rule)

- Consider departure timing — leave before December 31 to avoid January 1 local tax liability

- Appoint a 納税管理人 (tax representative) before departing

- File final Japan tax return by March 15 (via representative)

- Apply for pension lump-sum withdrawal within 2 years of departure

- Apply for 80% refund of withheld pension tax within 1 year of payment decision

- Close or convert NISA account within 3 months of departure

- Notify bank of non-resident status; maintain account if needed for refunds

- Close or transfer brokerage account

- File 転出届 (deregistration) at local municipal office near departure date

- Collect all Japan tax documents (源泉徴収票, 納税証明書) before leaving

Leaving Japan? Don’t navigate this alone.

TaxMatch Japan connects you with tax specialists who handle departing resident cases regularly — completely free matching service.

Or reach us directly on LINE

This article is for informational purposes only and does not constitute tax or legal advice. Tax obligations for departing Japan residents are complex and individual circumstances vary significantly. Please consult a qualified licensed tax accountant (zeirishi) for personalized guidance specific to your situation.

Frequently Asked Questions

What taxes do I need to pay when leaving Japan?

Before leaving Japan, you must settle your final income tax (via kakutei shinkoku), remaining residence tax payments, and national health insurance premiums. If you have financial assets over ¥100 million and lived in Japan 5+ years, exit tax may also apply.

Do I need to file a final tax return when leaving Japan?

Yes, if you earned income during the year of departure. You should file a ‘departure year’ tax return (junbi kakutei shinkoku) before leaving, or appoint a tax agent (nozei kanrinin) who will file on your behalf after your departure.

What is a tax agent (nozei kanrinin) in Japan?

A nozei kanrinin is a tax representative who handles your Japanese tax obligations after you leave the country. They can file tax returns, receive refunds, and pay outstanding taxes on your behalf. You must register them at your local tax office before departure.