Year-End Tax Adjustment in Japan for Foreigners: Complete Guide (2025-2026)

Every December, millions of employees in Japan receive a small but welcome surprise in their paycheck: a tax refund. This is the result of year-end tax adjustment (年末調整 / nenmatsu chosei) — the process where your employer recalculates your income tax for the year and settles the difference between what was withheld and what you actually owe. If you are a foreign employee in Japan, your HR department probably hands you a stack of Japanese forms every November and expects them back in a week. This guide explains what is actually happening, what changed in the 2025-2026 tax reforms, and how to make sure you are not leaving money on the table.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax rules and rates may change. Always consult a qualified tax professional (zeirishi) for advice specific to your situation.

Need a bilingual tax accountant? Get matched with a specialist — free.

Table of Contents

- How Year-End Tax Adjustment Works

- Who Is NOT Eligible for Year-End Adjustment

- The Key Difference: Gross Income vs Net Income

- 2025-2026 Tax Reform Changes

- The 5 Forms You Need to Submit

- Overseas Dependents: The 380,000 Yen Remittance Rule

- What Year-End Adjustment Does NOT Cover

- Timeline: What Happens When

- Common Mistakes Foreigners Make

- Frequently Asked Questions

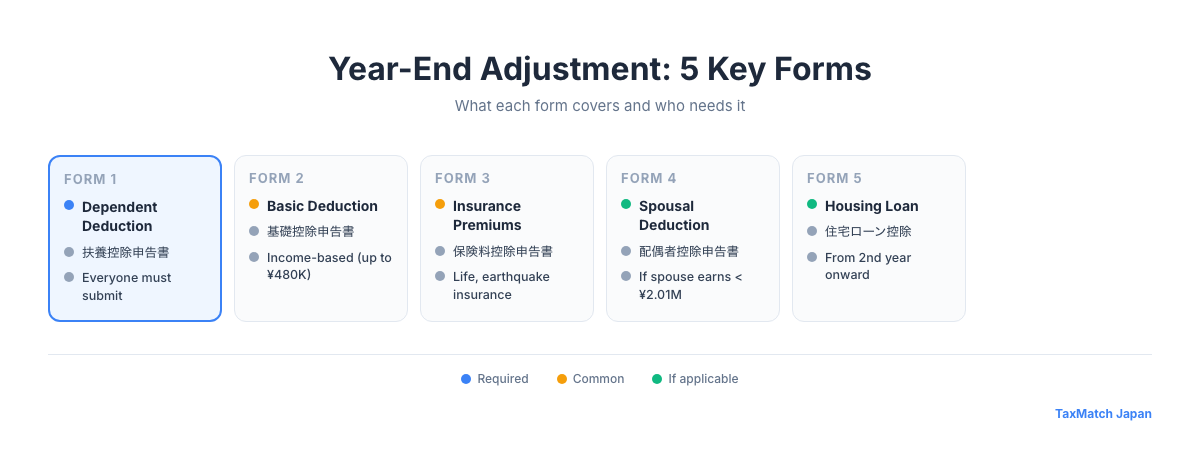

Year-End Adjustment: 5 key forms at a glance

1. How Year-End Tax Adjustment Works

Here is the basic concept: every month, your employer withholds income tax from your paycheck. But these monthly deductions are estimates. They are calculated based on standard tax tables and do not account for your full picture — your actual dependents, insurance premiums paid, life changes during the year, and so on.

At the end of the year, your employer recalculates your tax using your actual figures for the full calendar year. The result is one of two outcomes:

| Scenario | What Happens | How Common |

|---|---|---|

| Over-withheld | You get a refund in your December (or January) paycheck | Very common (~80% of employees) |

| Under-withheld | An additional amount is deducted from your paycheck | Less common |

Most employees get money back. Typical refunds range from 10,000 to 50,000 yen, though it can be significantly more if you have dependents or insurance deductions you had not previously declared.

Think of it this way: Monthly withholding is like paying estimated bills throughout the year. Year-end adjustment is the final settlement — your employer does the math and gives you back whatever you overpaid.

2. Who Is NOT Eligible for Year-End Adjustment

Not everyone qualifies. You will need to file your own tax return (確定申告 / kakutei shinkoku) instead if any of the following apply:

- Your annual salary exceeds 20,000,000 yen — high earners must file individually

- You have two or more employers — only your primary employer does the adjustment; you must file a return to combine all income

- You have side income exceeding 200,000 yen — freelance work, rental income, crypto gains, etc. See our side job tax guide for details

- You are employed by an overseas company that does not withhold Japanese income tax

- You are leaving Japan mid-year — you need to file a departure-year tax return before you go

If none of these apply and you are a regular employee at a Japanese company, your employer handles everything. You just need to submit the right forms.

3. The Key Difference: Gross Income (収入) vs Net Income (所得)

This is the number one mistake foreigners make on year-end adjustment forms. Japanese tax forms ask for both 収入 (shuunyuu) and 所得 (shotoku), and they are not the same thing.

- 収入 (Gross income) = Your total salary before any deductions. This is the big number on your pay stubs.

- 所得 (Net income) = Gross income minus the employment income deduction (給与所得控除 / kyuuyo shotoku koujo)

The employment income deduction is an automatic deduction the tax system applies to salaried workers. You do not need receipts — it is a formula. Here is how it works for 2025-2026:

| Gross Salary (収入) | Employment Income Deduction |

|---|---|

| Up to 1,625,000 yen | 550,000 yen |

| 1,625,001 – 1,800,000 yen | Gross x 40% – 100,000 yen |

| 1,800,001 – 3,600,000 yen | Gross x 30% + 80,000 yen |

| 3,600,001 – 6,600,000 yen | Gross x 20% + 440,000 yen |

| 6,600,001 – 8,500,000 yen | Gross x 10% + 1,100,000 yen |

| Over 8,500,000 yen | 1,950,000 yen (cap) |

Minimum deduction: 550,000 yen — even if you only earn a small amount, at least 550,000 yen is deducted.

Example

If your gross salary is 6,000,000 yen:

- Employment income deduction = 6,000,000 x 20% + 440,000 = 1,640,000 yen

- Net income (所得) = 6,000,000 – 1,640,000 = 4,360,000 yen

Warning

When a form asks for your 所得, write 4,360,000 — not 6,000,000. Getting this wrong will mess up every deduction calculation that follows.

4. 2025-2026 Tax Reform Changes

The Japanese government passed significant tax reforms effective from 2025. These are the changes that directly affect your year-end adjustment:

Basic Deduction Increase

| Item | Before (2024) | After (2025-2026) |

|---|---|---|

| Basic deduction (基礎控除) | 480,000 yen | 580,000 yen |

| Special additional exemption (temporary) | — | 20,000 yen (2025 only) |

| Total basic deduction | 480,000 yen | 580,000-600,000 yen |

The basic deduction applies to everyone with taxable income under 24,000,000 yen. This increase alone reduces your income tax by roughly 10,000-20,000 yen depending on your tax bracket.

The “103万 Wall” Becomes the “160万 Wall”

For years, part-time workers in Japan carefully kept their annual earnings under 1,030,000 yen (the so-called “103万 wall”) to avoid income tax. The math was simple: 650,000 (old employment deduction) + 480,000 (old basic deduction) = 1,030,000 yen of tax-free earnings.

With the 2025-2026 reforms:

- Employment income deduction minimum: 550,000 yen

- New basic deduction: 580,000 yen

- Special additional exemption (2025): 20,000 yen

- New tax-free threshold: approximately 1,600,000 yen

If you have a spouse working part-time, this change means they can earn significantly more before triggering income tax. However, note that the social insurance wall (1,060,000 yen) and spouse deduction limits are separate thresholds that have not changed as much.

Section Summary

- Basic deduction increased from 480,000 to 580,000 yen (plus a temporary 20,000 yen for 2025)

- The tax-free earnings threshold for part-time workers rose from ~1,030,000 to ~1,600,000 yen

- Social insurance thresholds remain separate — check with your employer

5. The 5 Forms You Need to Submit

Every November, your HR department will give you forms to fill out. Here is what each one does:

1. Dependents Declaration (扶養控除等申告書)

Everyone must submit this. It declares your dependents (children, parents, spouse with low income) and your own status (disability, single parent, student). Even if you have zero dependents, you still need to submit this form — without it, your employer cannot perform year-end adjustment at all.

2. Basic Deduction Declaration (基礎控除申告書)

Declares your estimated total income for the year so the correct basic deduction amount can be applied. For most employees earning under 24,000,000 yen, you will get the full 580,000 yen deduction.

3. Spouse Deduction Declaration (配偶者控除等申告書)

If your spouse earns income, this form determines whether you qualify for the spouse deduction or the spouse special deduction. Your spouse’s income level determines the deduction amount. Note: forms 2 and 3 are often combined on the same physical sheet.

4. Insurance Premium Deduction Declaration (保険料控除申告書)

This is where you declare:

- Life insurance premiums (生命保険料) — max deduction ~120,000 yen

- Earthquake insurance premiums (地震保険料) — max deduction 50,000 yen

- National pension (kokumin nenkin) or national health insurance (kokumin kenko hoken) paid out-of-pocket — fully deductible

- iDeCo contributions — fully deductible

You need to attach the original certificates (控除証明書) that your insurance companies mail to you in October-November. Do not throw these away.

5. Housing Loan Deduction Declaration (住宅借入金等特別控除申告書)

If you purchased a home and this is your second year or later of claiming the housing loan deduction, submit this form with the bank’s year-end loan balance certificate. The first year requires a full tax return — you cannot claim it through year-end adjustment.

Not sure which forms apply to you? A bilingual tax specialist can walk you through it. Get matched free →

6. Overseas Dependents: The 380,000 Yen Remittance Rule

This section is critical for foreigners who financially support family members back home. Claiming overseas dependents can save you serious money — but the documentation requirements are strict, and they got stricter in 2024.

The Rules

For overseas dependents aged 16-29 or 70+: You can claim them as dependents with relatively straightforward documentation — proof of relationship and proof of remittance.

For overseas dependents aged 30-69: Since 2024, you must meet at least one of these conditions:

- The dependent has been a student abroad for the year

- The dependent has a disability

- You sent at least 380,000 yen to that specific dependent during the year

That third condition is the one that applies to most foreigners supporting working-age parents or siblings overseas.

Documentation You Need

| Document | What It Proves | Notes |

|---|---|---|

| Relationship certificate (親族関係書類) | Family relationship | Birth certificate, family register, etc. |

| Japanese translation | — | Required for all non-Japanese documents |

| Remittance records (送金関係書類) | You sent money to them | Bank transfer receipts, Wise/Revolut records |

Common Pitfalls

Send money to individual accounts, not joint accounts. If you are claiming your mother and father as separate dependents, you need to show separate remittances to each person. Sending 760,000 yen to a joint account does not count as 380,000 yen to each. Send 380,000+ yen to your mother’s account and 380,000+ yen to your father’s account.

Use traceable transfer services. Cash carried in a suitcase or sent through informal channels does not produce acceptable documentation. Use bank wire transfers, Wise, Revolut, or similar services that provide clear transaction records showing the sender, recipient, amount, and date.

Get translations done early. Relationship documents (birth certificates, marriage certificates, family registers) from your home country need Japanese translations. You do not need a certified translator — you can do it yourself — but it takes time. Do not wait until November.

The Tax Savings Are Significant

| Number of Overseas Dependents (age 30-69) | Taxable Income Reduction | Approximate Tax Savings (20% bracket) |

|---|---|---|

| 1 dependent | 380,000 yen | ~76,000 yen |

| 2 dependents | 760,000 yen | ~152,000 yen |

| 3 dependents | 1,140,000 yen | ~228,000 yen |

These savings include both income tax and residence tax reductions. If you are already sending money home anyway, making sure you have the paperwork to claim the deduction is essentially free money.

Section Summary

- Overseas dependents aged 30-69 require 380,000 yen in remittance per person per year

- Send to individual accounts, not joint accounts, and use traceable transfer services

- Potential savings: 76,000+ yen per dependent per year (income tax + residence tax combined)

7. What Year-End Adjustment Does NOT Cover

Even though year-end adjustment handles a lot, there are several deductions and situations it cannot process. For these, you need to file your own tax return (確定申告) separately, typically by March 15th of the following year:

- Medical expenses deduction — if your household spent over 100,000 yen on medical costs

- Furusato nozei (hometown tax) with 6 or more municipalities — 5 or fewer can use the one-stop exception, but 6+ requires a tax return

- First-year housing loan deduction — only the first year requires a tax return; subsequent years go through year-end adjustment

- Foreign tax credits — if you paid taxes to another country on the same income

- Side income or freelance income — any income not from your primary employer

- Capital gains from stock sales or cryptocurrency

- Charitable donations (other than furusato nozei one-stop)

Pro tip: Even if your employer does year-end adjustment, you can still file a tax return afterward to claim additional deductions. The tax return will override the year-end adjustment results and recalculate your final tax.

8. Timeline: What Happens When

| When | What to Do |

|---|---|

| October | Insurance companies mail you deduction certificates (控除証明書). Watch your mailbox carefully. |

| Early November | HR distributes year-end adjustment forms |

| Mid-November | Deadline to submit forms to HR (varies by company, but typically around Nov 15-30) |

| Late November – December | Your employer calculates the adjustment |

| December paycheck (or January) | You receive your refund (or additional deduction) |

| January | Your employer issues your withholding tax certificate (源泉徴収票 / gensen choshuhyo) |

| February 16 – March 15 | Tax return filing period (only if you need to file separately) |

The 源泉徴収票 is important. This single-page document summarizes your entire year’s income, deductions, and taxes paid. Keep it safe. You will need it if you file a tax return, apply for a loan, or deal with immigration paperwork.

9. Common Mistakes Foreigners Make

1. Not Claiming Overseas Dependents

This is the biggest missed opportunity. Many foreigners send money home to parents or siblings every month but never claim them as dependents because they assume it only applies to family living in Japan. It does not. Overseas dependents are absolutely claimable — you just need the documentation.

2. Confusing Gross Income and Net Income on Forms

As explained above, writing your gross salary (収入) where the form asks for net income (所得) will inflate your reported income and potentially reduce or eliminate deductions. Double-check which field you are filling in. The difference can be over 1,000,000 yen.

3. Losing Insurance Deduction Certificates

Those thin envelopes from your insurance companies in October? They contain the certificates you need to claim deductions for life insurance, earthquake insurance, and iDeCo. If you throw them away or lose them, you will need to request reissues — which takes weeks and may not arrive before your company’s deadline.

Set a reminder for October: “Check mail for insurance certificates. Do not throw away any envelopes from insurance companies.”

4. Both Spouses Claiming the Same Child

If both you and your spouse work, only one of you can claim a child as a dependent. You cannot both claim the same child on your respective year-end adjustment forms. Decide in advance which spouse will claim — typically the higher earner, since the deduction saves more money in a higher tax bracket.

5. Not Submitting the Dependents Form at All

Some foreigners with no dependents skip the form entirely, assuming it does not apply to them. This is a mistake. Without submitting the Dependents Declaration (扶養控除等申告書), your employer is legally required to withhold tax at the higher “Otsu” (乙) column rate instead of the standard “Ko” (甲) rate. This means significantly more tax withheld — and no year-end adjustment at all.

6. Ignoring the Process Because “My Company Handles It”

Your company handles the calculation, but you are responsible for providing accurate information on the forms. If you submit blank or incorrect forms, your employer will calculate based on what you gave them — which means zero deductions beyond the basics.

Key Takeaways

- Year-end adjustment is your one chance each year to get your taxes right without filing a return yourself

- The biggest missed opportunity for foreigners is not claiming overseas dependents

- Always submit the Dependents Declaration, even if you have zero dependents

- Keep all insurance certificates that arrive in October-November

Confused by the forms? Not sure what you can claim? Get matched with an English-speaking tax accountant — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

What is nenmatsu chosei (year-end adjustment)?

Nenmatsu chosei (年末調整) is Japan’s year-end tax adjustment process where employers recalculate the exact income tax liability for each employee and reconcile it against the monthly withholdings made throughout the year. Any overpayment is refunded and any underpayment is collected.

Do foreigners need year-end adjustment in Japan?

Yes, if you are employed in Japan and earn ¥20 million or less annually, your employer will perform year-end adjustment for you. This eliminates the need to file your own tax return unless you have additional income sources, medical expense deductions, or your first year of mortgage deduction.

What deductions are included in year-end adjustment?

Year-end adjustment covers: basic deduction, spousal deduction, dependent deduction, social insurance deduction, life insurance deduction, earthquake insurance deduction, housing loan deduction (2nd year onward), and small enterprise mutual aid deduction. Medical expense deduction and charitable donations require a separate tax return.