Non-Permanent Resident (NPR) & Remittance Rule in Japan (2026) | TaxMatch Japan

Japan’s Non-Permanent Resident (NPR) status is one of the most valuable — and most misunderstood — tax benefits available to foreign professionals living in Japan. If you have been in Japan for 5 years or less (within the past 10 years), your foreign-source income is only taxed when you “remit” it to Japan. This can shield millions of yen in offshore dividends, rental income, and legacy capital gains from Japan’s tax rates, which can exceed 55%. But the rules are fiendishly complex: using a foreign credit card to buy coffee in Tokyo counts as a remittance, the NTA does not care that the money you transferred was “old savings,” and one wrong move during your transition year can trigger worldwide taxation on everything. This guide explains exactly how it works.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. NPR rules involve highly nuanced statutory interpretation. Always consult a qualified tax professional (税理士 / zeirishi) for advice specific to your situation.

Need a bilingual tax accountant? Get matched with an international tax specialist — free.

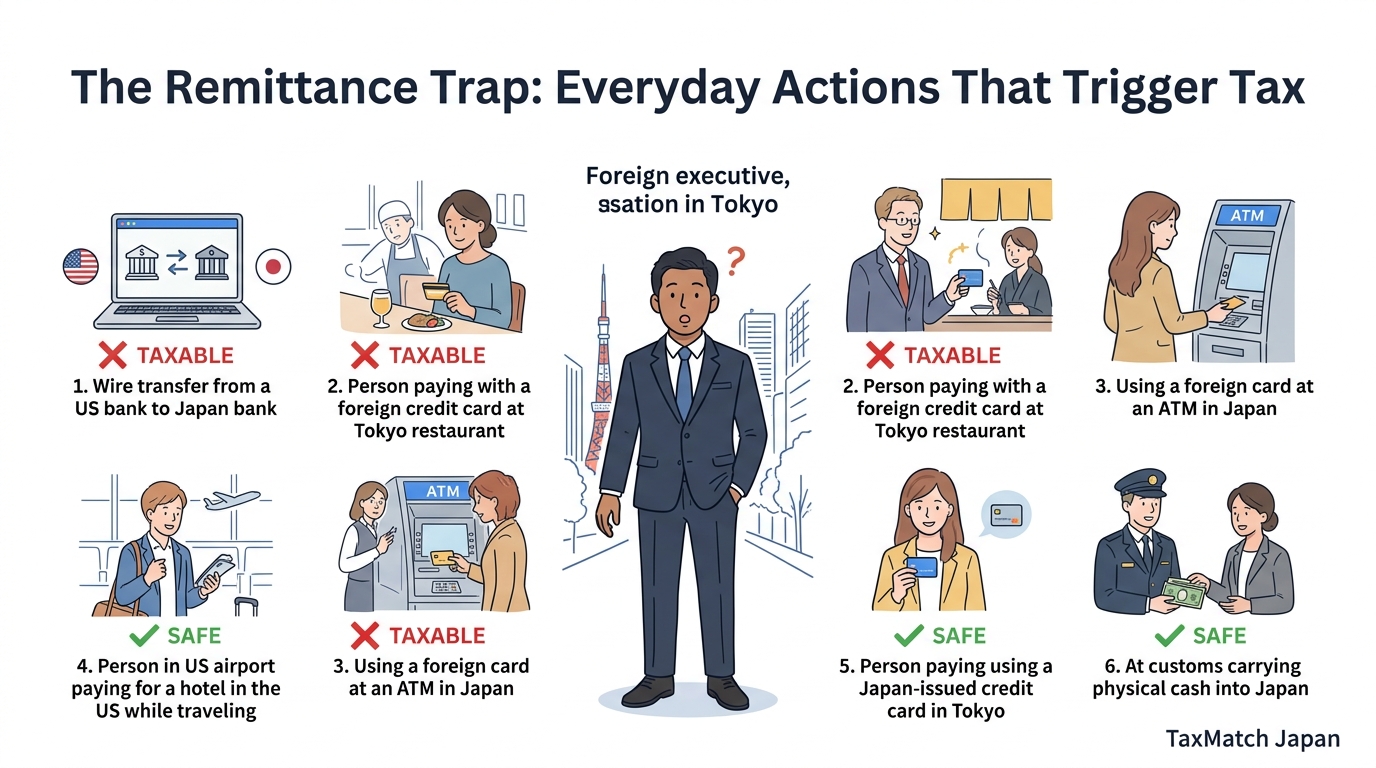

The Remittance Trap: Everyday actions that trigger tax

Table of Contents

- NPR Definition & the 5-Year Rule

- Three Tax Residency Categories

- Remittance Rule Mechanics

- The Matching & Fungibility Problem

- Impact on RSUs, Capital Gains, Dividends & More

- Planning Strategies

- Transition to Permanent Resident Status

- Enforcement & CRS

- Common Mistakes

- When to Hire a Tax Accountant

- Frequently Asked Questions

1. NPR Definition & the 5-Year Rule

To qualify as a Non-Permanent Resident for tax purposes, you must meet all three conditions:

- You have established a domicile (住所 / jusho) in Japan (or have lived here for 1+ years)

- You do not hold Japanese nationality (dual citizens with Japanese nationality do not qualify)

- You have maintained a domicile or residence in Japan for 5 years or less within the past 10 years

The 10-Year Lookback Window

The 5-year threshold is calculated on a rolling 120-month window, counting the exact accumulation of months spent as a resident — not calendar years. This creates important implications for returning expats:

Example

If you lived in Japan for 3 years, left for 4 years, and returned on a new assignment, your previous 3 years still count within the 10-year lookback window. You will only have 2 more years of NPR status before crossing the 5-year threshold.

Immigration vs. Tax Status

A critical distinction: immigration “Permanent Resident” status and tax “Permanent Tax Resident” status are completely separate concepts. You can hold a PR immigration visa and still be an NPR for tax purposes if you have been in Japan less than 5 years. Conversely, you can be a Permanent Tax Resident on a temporary work visa if you have exceeded the 5-year threshold.

2. Three Tax Residency Categories

Japan classifies all individuals into three categories with vastly different scopes of taxable income:

| Status | Qualification | Taxable Income Scope |

|---|---|---|

| Non-Resident | No domicile in Japan; resided < 1 year | Japan-source income only |

| Non-Permanent Resident (NPR) | Non-Japanese national; domicile ≤ 5 yrs out of trailing 10 yrs | Japan-source + remitted foreign-source |

| Permanent Tax Resident | Japanese national, or domicile > 5 yrs out of trailing 10 yrs | Worldwide income (all sources, all locations) |

The NPR advantage lies in the conditional exemption of foreign-source income: as long as offshore earnings stay offshore, they escape Japan’s marginal rates of up to 55.945%.

3. Remittance Rule Mechanics

Under Article 7 of the Income Tax Act, NPRs are taxed on foreign-source income that is “paid in Japan or remitted to Japan from abroad.” The legal definition of “remittance” is far broader than most expats expect.

What Counts as a Remittance

| Action | Remittance? |

|---|---|

| Wire transfer from overseas bank to Japanese bank | Yes |

| Using a foreign credit/debit card to buy anything in Japan | Yes |

| ATM withdrawal in Japan using a foreign bank card | Yes |

| Repaying a Japanese loan from an overseas account | Yes |

| Using a foreign credit card while traveling abroad | No |

| Physical cash brought into Japan on your person | No (subject to customs rules) |

Warning: The Credit Card Trap

Using Apple Pay linked to a US Chase card, a UK Monzo card, or any foreign-issued payment method to buy anything in Japan — even a coffee — constitutes a taxable remittance if you have concurrent offshore income. This is the single most common way NPRs accidentally trigger tax liabilities.

4. The Matching & Fungibility Problem

This is the most dangerous trap in the NPR system, and the one that destroys the most expat wealth.

The Fatal “Old Savings” Myth

Many NPRs believe they can remit “old savings” (money earned before moving to Japan) tax-free. This is wrong. Because currency is fungible (interchangeable), the NTA does not trace the specific origin of remitted funds. Instead, it uses a strict statutory matching formula that automatically deems any remittance to be current-year foreign income.

How the Matching Formula Works

Under Enforcement Decree Article 17, remittances are matched against income in this strict order:

- Pool A — Non-Foreign Source Income paid abroad: If your employer pays part of your Japan-sourced salary into an overseas account, this already-taxed income acts as a “buffer.” Remittances are offset against this first, triggering no additional tax.

- Pool B — Foreign Source Income: Any remaining remittance above the buffer is matched against current-year foreign-source income (dividends, rental income, offshore capital gains). This portion becomes taxable.

- If Pool B is zero: If you have zero foreign-source income in the current year, the taxable remittance is zero — regardless of amount.

Three Scenarios

| Scenario | Offshore Salary Buffer | Foreign Income | Remittance | Taxable Amount |

|---|---|---|---|---|

| No buffer | 0 | 3M yen | 1M yen | 1M yen |

| With buffer | 2.5M yen | 3M yen | 5M yen | 2.5M yen (5M – 2.5M buffer) |

| Zero foreign income | 0 | 0 | 50M yen | 0 yen |

Matching is strictly confined to the calendar year (January 1 – December 31). A remittance on December 31 triggers matching against current-year income, while the same transfer on January 1 is matched only against the new year’s income.

5. Impact on RSUs, Capital Gains, Dividends & More

Whether income is “Foreign Source” or “Domestic Source” is the linchpin of NPR taxation. Many expats get this wrong because intuition does not match the statutory rules.

RSUs and Stock Options

The NTA sources equity compensation based on where the work was performed during the vesting period — not where the company is headquartered or where the shares are held.

Example: A 1,000-day vesting period. You lived abroad for the first 600 days, then moved to Japan for the final 400 days.

- 60% Foreign Source — shielded from Japanese tax unless remitted

- 40% Domestic Source — fully taxable in Japan immediately upon vesting, even if shares go to a US brokerage

Capital Gains on Foreign Securities

Warning: The Capital Gains Trap

Capital gains sourcing depends entirely on when the asset was acquired:

- Acquired before moving to Japan: Foreign Source — gains are shielded unless remitted

- Acquired after becoming a Japanese tax resident: Domestic Source — gains are immediately taxable at 20.315%, regardless of remittance

Active trading on a US brokerage while living in Japan will generate Domestic Source gains on every position opened after arrival, completely nullifying the NPR benefit for those trades.

Dividends and Interest

Dividends from foreign corporations and interest from overseas bank accounts are Foreign Source Income. They accumulate tax-free in offshore accounts as long as no remittances are made. However, they create matching risk if any funds are brought into Japan.

Foreign Rental Income

Rental income from property located outside Japan is Foreign Source Income. Deductions (mortgage interest, depreciation) can reduce the net amount. However, a foreign rental loss cannot offset Japanese domestic income.

Foreign Pensions

Most foreign pension distributions are Foreign Source Income under the “miscellaneous income” category. However, US Social Security is a critical exception: under the US-Japan tax treaty, US Social Security paid to a Japan resident is re-sourced as Domestic Income and fully taxable regardless of remittance.

NPR tax planning is high-stakes and highly technical. A bilingual tax accountant can help you structure your finances to maximize the benefit. Get matched free →

6. Planning Strategies

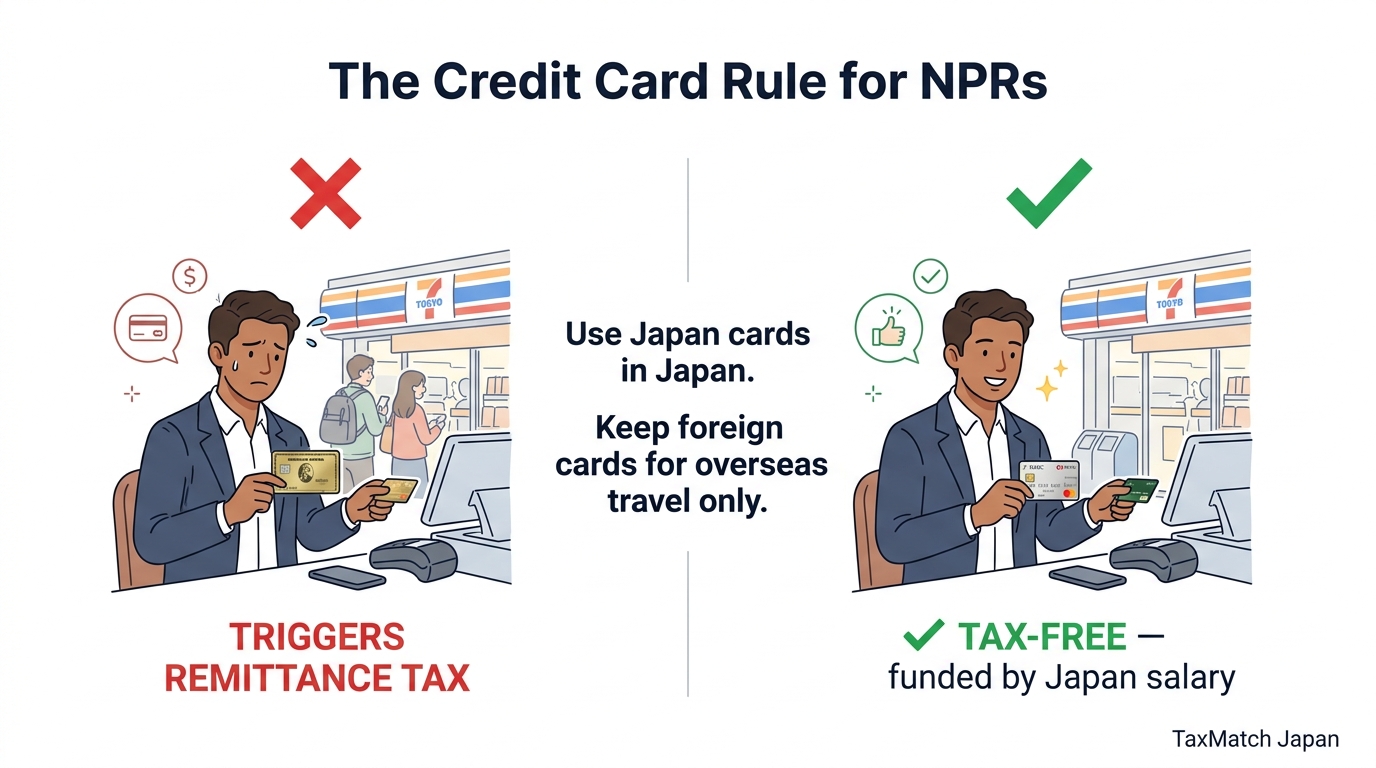

The Credit Card Rule for NPRs

Strategy 1: Pre-Arrival Capital Injection

Before establishing residency (or before any foreign income is generated), transfer a large sum to your Japanese bank account. With zero foreign income in that tax year, the remittance cannot be matched against anything — creating a tax-free domestic cash buffer for your entire NPR period.

Strategy 2: Credit Card Segregation

Stop using foreign credit cards in Japan immediately. Get a Japan-issued credit card linked to a Japanese bank account. Route all domestic spending through the Japanese card. Reserve foreign cards exclusively for purchases made while traveling outside Japan (which do not count as remittances).

Strategy 3: The Offshore Salary Buffer

If your employer can pay part of your Japan-sourced salary directly into your overseas bank account, this creates “Non-Foreign Source Income paid abroad.” This pool acts as a shield: you can remit an equal amount back to Japan later without triggering the matching formula against your passive foreign income.

Strategy 4: Pre-Transition Asset Liquidation

Before crossing the 5-year threshold, consider liquidating pre-arrival foreign securities with large unrealized gains. If you make zero remittances in that calendar year, the gains are completely tax-free in Japan. You can immediately repurchase the same assets, effectively “stepping up” your cost basis to current market value before becoming subject to worldwide taxation.

Strategy 5: Strategic Timing of Sales

Since matching is strictly calendar-year based, time large remittances for years when you have low or zero foreign-source income. Delay asset sales to years when you can avoid concurrent remittances.

7. Transition to Permanent Resident Status

The moment you exceed 60 months of Japanese residency within the trailing 120-month window, you automatically become a Permanent Tax Resident. This transition almost always occurs mid-year.

Mid-Year Split Taxation

Under Article 8 of the Income Tax Act, the transition year is split into two distinct periods:

| Period | Tax Status | What’s Taxable |

|---|---|---|

| Jan 1 to exact 5-year anniversary | NPR | Japan-source + remitted foreign-source only |

| 5-year anniversary to Dec 31 | Permanent Tax Resident | All worldwide income |

The two periods have separate walls: a remittance made in Period 2 does not retroactively tax foreign income earned in Period 1.

Tip

Execute all offshore income recognition (dividend distributions, asset sales, trust distributions) before your 5-year anniversary date. Make zero remittances during Period 1 to shield those earnings. After the transition, worldwide taxation applies regardless.

Resetting the NPR Clock

To reset the 5-year counter, you must physically and legally abandon your Japanese domicile and remain a non-resident long enough to clear the 10-year lookback window. A brief sabbatical or one-year overseas transfer will not suffice — your prior years still count upon return.

8. Enforcement & CRS

The era of “benign neglect” regarding offshore income is over. The NTA actively monitors NPR compliance through modern data-sharing infrastructure.

CRS Data Matching

The NTA receives automatic financial account data from 100+ jurisdictions via the Common Reporting Standard. If your CRS report shows overseas dividend income but your Japanese return declares zero foreign income, the discrepancy is flagged automatically. The NTA then cross-references domestic bank records for inward wire transfers and applies the matching formula retroactively.

Wire Transfer Monitoring

Domestic banks automatically report all inbound transfers exceeding 1,000,000 yen to the NTA. Large remittances during years with declared foreign income invite scrutiny.

Tribunal Precedent: No “Un-Remitting”

A landmark National Tax Tribunal ruling established that a remittance cannot be reversed. In the case, an NPR transferred funds to Japan, realized the tax consequences, and immediately sent the money back offshore. The Tribunal ruled that the initial transfer permanently triggered the remittance tax at the moment of entry into Japan. Sending the money back does not “un-remit” it.

9. Common Mistakes

Mistake 1: The Fungibility Trap

The problem: Assuming that transferring “old savings” from before you moved to Japan is tax-free. The NTA ignores the origin of funds and automatically matches remittances against current-year foreign income.

Mistake 2: The Credit Card Trap

The problem: Routinely using Apple Pay linked to a US card, a UK debit card, or any foreign payment method for domestic purchases. Every transaction counts as a remittance.

Mistake 3: The Capital Gains Trap

The problem: Assuming NPR status shields all overseas brokerage activity. Assets acquired after becoming a Japanese tax resident generate Domestic Source gains — immediately taxable regardless of remittance.

Mistake 4: Mismanaging the Mid-Year Transition

The problem: Failing to realize the exact date of the 5-year anniversary and executing asset sales or large remittances after crossing the threshold, triggering worldwide taxation.

Mistake 5: Phantom RSU Sourcing

The problem: Miscalculating the Japan-workday ratio during multi-year RSU vesting periods. Relying on the foreign employer’s tax documents without applying Japanese geographic day-count sourcing rules practically guarantees an audit adjustment.

Summary

- NPR status shields foreign-source income from Japanese tax unless remitted

- Remittance = wire transfers, foreign credit card use in Japan, ATM withdrawals

- The NTA matches remittances against current-year foreign income — “old savings” are not exempt

- RSU sourcing depends on where you worked during the vesting period

- Capital gains on assets acquired after moving to Japan are Domestic Source (fully taxable)

- The transition to Permanent Tax Resident occurs on the exact 60th month, usually mid-year

- CRS data means the NTA already knows about your offshore accounts

10. When to Hire a Tax Accountant

NPR tax planning requires precision timing and deep knowledge of income sourcing rules. Consider hiring a bilingual tax accountant (税理士) if:

- You have significant offshore income (dividends, rental, capital gains) and need to structure remittances carefully

- You receive RSUs or stock options from a foreign employer and need accurate Japan-workday sourcing calculations

- You are approaching the 5-year threshold and need a pre-transition liquidation and remittance strategy

- You have been using foreign credit cards in Japan and need to assess your remittance exposure

- You need to calculate the offshore salary buffer to optimize the Enforcement Decree Article 17 matching

- You are a returning expat who lived in Japan previously and need to calculate your remaining NPR runway

Need help with NPR tax planning? Get matched with an English-speaking tax accountant who specializes in expatriate taxation — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

What is the remittance rule for non-permanent residents?

Non-permanent residents of Japan (foreigners who have lived in Japan for 5 years or less within the past 10 years) are taxed on foreign-source income only to the extent it is remitted (sent) to Japan. Foreign income kept overseas is generally not subject to Japanese tax.

Does using a foreign credit card in Japan trigger the remittance rule?

This is a gray area. The NTA has not issued definitive guidance, but using a foreign credit card for purchases in Japan could potentially be considered a remittance. Conservative tax planning suggests treating foreign credit card use in Japan as a remittance.

How long does non-permanent resident status last?

Non-permanent resident status applies for the first 5 years of residence within any rolling 10-year period. Once you exceed 5 years of residence within the past 10 years, you automatically become a permanent tax resident and are taxed on worldwide income regardless of remittance.