Discovering that you should have filed a Japanese tax return — months or even years ago — is a stomach-drop moment. You’re not the first foreign resident in Japan to find yourself here, and you almost certainly will not be the last. The good news is that Japan’s National Tax Agency (NTA) actually rewards voluntary disclosure with significantly lower penalties than waiting for them to come knocking. The bad news is that those penalties compound quickly, and a 2026 reform pushed the higher-end rates even higher.

This guide walks through everything a foreigner — current resident, recent leaver, or someone who never realized they had a filing obligation — needs to understand about overdue tax returns in Japan: who owes what, how the penalty math works in 2026, how far back the NTA can reach, and what to do this week if you’ve just realized you’re behind.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax rules and rates may change. Always consult a qualified tax professional (zeirishi) for advice specific to your situation.

Need a bilingual tax accountant?

Get matched with a specialist — free.

Table of Contents

- Who Needs to File an Overdue Tax Return in Japan?

- Statute of Limitations: 5 Years, 7 Years, and the Edge Cases

- Failure-to-File Penalty (Mukoshin Kasanzei): 2026 Rates

- Delinquency Tax (Entaizei): The Interest Clock

- How to File a Period-Past Return (Kigen-go Shinkoku)

- Voluntary Disclosure vs. Waiting for the Audit

- Special Situations for Foreign Residents

- Tax Representative for Departed Residents (Nozei Kanrinin)

- How to Reduce or Avoid Japan Overdue Tax Penalties

- Frequently Asked Questions

- Get Expert Help With Overdue Filings

1. Who Needs to File an Overdue Tax Return in Japan?

Japan’s annual income tax filing season (kakutei shinkoku) runs from February 16 to March 15 each year for the prior calendar year’s income — every deadline is mapped in our Japan Tax Calendar 2026, and the on-time filing mechanics are covered in Tax Filing Guide for Foreigners. If your tax situation required a return and you missed that window — for any year, no matter how long ago — you have an overdue filing obligation.

For foreign residents, the filing requirement is broader than many people realize. You generally must file if any of the following applies:

- You earned employment income that wasn’t fully covered by year-end adjustment (nenmatsu chosei). This includes anyone with side income, two employers, or salary exceeding ¥20 million.

- You received non-Japanese-source income above ¥200,000 during a year when you were classified as a Permanent Resident or Non-Permanent Resident (after the 5-year mark), and that income was either paid in or remitted to Japan.

- You realized capital gains on Japanese stocks (outside a tokutei kouza with withholding), real estate, or cryptocurrency (whose rules changed in the 2026 reform).

- You operated a sole proprietorship or had freelance income above ¥480,000 (the basic deduction threshold).

- You sold real estate in Japan, even if at a loss, since the transaction must be declared.

- You received gift or inheritance amounts above the relevant exemption, requiring a separate gift tax (zoyo-zei) or inheritance tax (sozoku-zei) return.

Missing any of these returns creates an overdue filing — what Japanese tax law calls mushinkoku (failure to file) when you never filed at all, or kigen-go shinkoku (period-past filing) when you eventually file after the deadline.

Common foreigner scenarios we see

The Foreign Lead intake at TaxMatch Japan regularly surfaces the same overdue patterns:

- The “side income that grew” case — someone started freelancing on the side while employed, never filed because they thought year-end adjustment covered everything, and now have three years of unreported income.

- The “I left Japan without finishing” case — a foreign resident left Japan mid-year, never filed the partial-year return, and is now receiving notices forwarded from their old address.

- The “I didn’t know about foreign income” case — a Permanent Resident realized only after a few years that worldwide income — including dividends and interest from a home-country brokerage — must be reported.

- The “RSU/stock comp” case — equity compensation vested and was sold, but the employer didn’t withhold or report it correctly, leaving a meaningful underreport.

If any of these patterns matches your situation, the next sections will tell you what’s actually at stake.

Important: Even if you’re no longer in Japan, the obligation does not expire just because you left. The NTA can — and does — issue determinations against former residents using addresses on file, and treaty-based information exchange means foreign financial data increasingly reaches Japanese tax authorities. Section 8 covers what to do if you’ve already departed.

2. Statute of Limitations: 5 Years, 7 Years, and the Edge Cases

The first practical question most overdue filers ask is: how far back can they come after me? Japan’s General Tax Act (Kokuzei Tsusoku-ho) sets clear statute-of-limitations rules — though there are important exceptions foreigners often miss.

The Standard Periods

| Situation | Statute of Limitations | Source |

|---|---|---|

| Normal underreport or failure to file | 5 years | Act Art. 70 |

| Deliberate concealment or fraud (itsuwari sono ta no fusei) | 7 years | Act Art. 70-5 |

| Refund claims (you’re owed money) | 5 years | Act Art. 56 |

The clock starts on the day after the statutory filing deadline. For 2024 income tax — normally due March 17, 2025 (March 15 fell on a Saturday) — the NTA can assess additional tax up until March 18, 2030 in normal cases, and March 18, 2032 in fraud cases.

What Counts as “Fraud” for the 7-Year Window?

The 7-year window is reserved for itsuwari sono ta no fusei na koui — typically translated as “false or other improper conduct.” Case law and NTA practice draw a line between:

- Mere failure to file — usually 5 years, even if substantial income went unreported, as long as there’s no active concealment.

- Active concealment — using shell accounts, false invoices, fabricated documentation, or deliberately moving assets to obscure them — triggers the 7-year reach.

Most overdue foreign filers fall squarely on the 5-year side. If you forgot, didn’t understand the obligation, or didn’t realize a particular income stream was reportable, that’s failure to file, not fraud — though it still carries the penalty tax discussed in Section 3.

Inheritance and Gift Tax Are Different

Inheritance tax has its own 5-year (or 7-year, with concealment) clock starting from the deadline 10 months after death. Gift tax follows the same general framework but runs from the filing deadline of the year following the gift. If you’re dealing with an overdue inheritance return, consult a specialist — late inheritance filings carry their own procedural quirks, and the assets being valued may have moved significantly since the date of death.

3. Failure-to-File Penalty (Mukoshin Kasanzei): 2026 Rates

The mukoshin kasanzei — failure-to-file additional tax — is the headline penalty for filing late. As of the post-Reiwa-5 reform (applicable to filings for tax year 2023 onward), the rate depends both on how you came to file and on how much tax was owed.

The Three Penalty Tiers

The single most important number is this: voluntary filing before the NTA contacts you triggers a flat 5% penalty. Waiting until they notice can easily push that to 20–30% of the unpaid tax — six times more.

| Trigger | Tax ≤ ¥500,000 | ¥500,000 – ¥3,000,000 | Tax > ¥3,000,000 |

|---|---|---|---|

| Voluntary filing before any NTA notice | 5% | 5% | 5% |

| After audit notice, before assessment | 10% | 15% | 25% |

| After NTA determination or assessment | 15% | 20% | 30% |

Numbers are the additional tax expressed as a percentage of the unpaid principal tax. They are separate from and on top of the original tax owed, and they do not replace the interest discussed in Section 4.

The Total-Forgiveness Path

There is a narrow path to escape the penalty entirely. If all four of the following hold, no mukoshin kasanzei is assessed at all:

- You file the overdue return within one month of the original deadline.

- You pay the full tax owed by the original payment deadline (which is the same as the filing deadline for income tax).

- The NTA judges that you had a genuine intention to file on time (e.g., natural-disaster disruption, severe illness, mailing error with documentary evidence).

- You have no failure-to-file or heavy additional tax penalty in the prior 5 years.

In practice, most overdue cases miss the 1-month window and don’t qualify. But for someone who realizes their mistake in mid-April for a March 17 deadline, this provision can completely erase the penalty.

Heavy Additional Tax (Juukasanzei): The 40% Cliff

If the NTA determines you engaged in active concealment — falsifying records, hiding income through opaque accounts, or otherwise meeting the high bar for itsuwari sono ta no fusei — the failure-to-file penalty is replaced by a much heavier heavy additional tax (juukasanzei) of 40% of the unpaid tax. There is no voluntary-disclosure reduction for this tier, and the 7-year statute window applies.

Foreigners who simply didn’t understand the system are virtually never assigned juukasanzei — but anyone who is tempted to “clean up” old returns by selectively under-reporting should understand that doing so moves you from the 5% lane to the 40% lane. Honest, full disclosure is always the cheaper path.

4. Delinquency Tax (Entaizei): Japan’s Overdue Interest Clock

The second layer of the overdue cost is entaizei — delinquency tax, which functions as interest on the unpaid principal. It applies to every day from the original payment deadline until you actually pay.

2026 Rates

For 2026, the rates announced by Japan’s Ministry of Finance are:

| Period from Original Deadline | 2026 Annual Rate |

|---|---|

| Day 1 through Day 60 (within 2 months) | 2.8% |

| Day 61 onward (over 2 months) | 9.1% |

These rates are set annually using a formula tied to short-term lending rates plus statutory add-ons. They have crept upward in recent years — 2023 was 2.4% / 8.7%, 2024 was 2.4% / 8.7%, 2025 was 2.4% / 8.7%, and 2026 stepped up to 2.8% / 9.1%. Historical years use the rates in effect when the original deadline passed, not today’s rates.

How the Math Compounds

Entaizei is calculated on a daily basis, but only the principal tax is subject to it — not the penalty additional tax itself. A worked example:

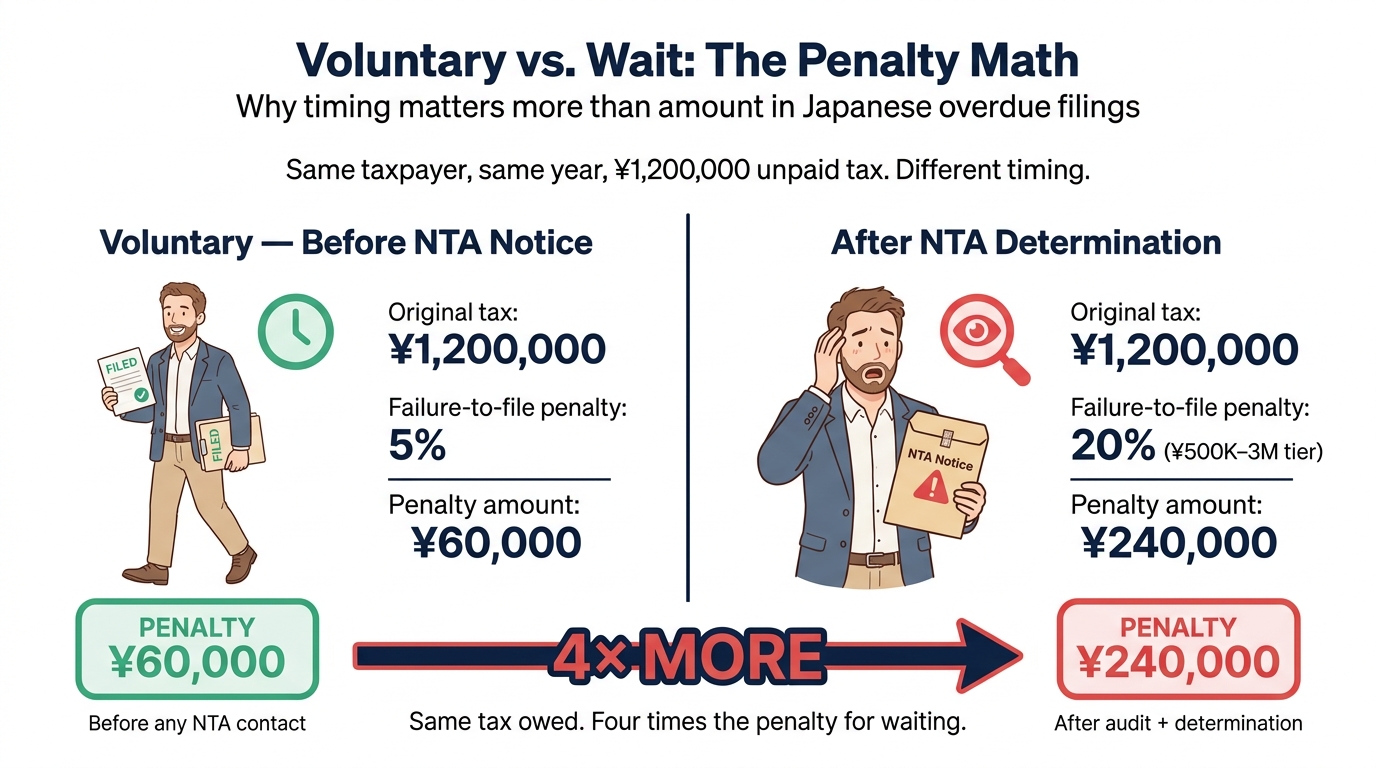

Scenario: A foreign resident owed ¥1,200,000 in income tax for tax year 2024 (deadline March 17, 2025) and files on June 1, 2026 — about 14 months late, voluntarily, before any NTA contact.

- Original tax: ¥1,200,000

- Failure-to-file penalty (5% voluntary, ¥1.2M tier): ¥60,000

- Entaizei — first 60 days at 2.4% (2025 rate): ¥1,200,000 × 2.4% × 60/365 = ¥4,734

- Entaizei — days 61 to end of 2025 at 8.7%: ¥1,200,000 × 8.7% × 230/365 ≈ ¥65,797

- Entaizei — Jan 1 to June 1, 2026 at 9.1%: ¥1,200,000 × 9.1% × 152/365 ≈ ¥45,470

- Total interest: ~¥116,000

- Grand total: ~¥1,376,000

Had the same taxpayer waited until the NTA opened an audit and then settled, the 5% penalty would have become 20% (¥240,000 instead of ¥60,000), and interest would have continued to accrue. The voluntary-disclosure premium for waiting six more months: roughly ¥230,000 on a single year.

Rounding and Minor Amounts

Entaizei is rounded down to the nearest ¥1,000 below ¥1,000. If the calculated interest is under ¥1,000, no entaizei is assessed at all. For very small underpayments, this can mean the penalty is effectively just the failure-to-file tax — but for any meaningful liability, interest dominates the late cost.

5. How to File a Period-Past Return (Kigen-go Shinkoku)

A late return — formally a kigen-go shinkoku — is filed almost identically to an on-time return. The form is the same (Shinkokusho Form B for individuals), the supporting documents are the same, and you can submit it through the same channels.

The Practical Steps

- Gather records for the year(s) in question. This means employer-issued gensen choshu-hyo (withholding tax statements), brokerage statements, real estate transaction documents, foreign income records, and any deductible-expense receipts. For years more than 3–4 years past, your former employer may no longer have your gensen choshu-hyo readily available — request it as early as possible.

- Recreate the return for each year separately. Each tax year is filed individually. Use that year’s tax forms and that year’s tax rates and deduction thresholds — they change slightly year to year.

- Calculate the tax owed using the regular income tax brackets in force for that year. Don’t forget special tables for capital gains and other separated-tax categories.

- File the return. You can file via:

- e-Tax — Japan’s online filing system, available for prior-year returns as long as your My Number card and reader (or a smartphone-based equivalent) is set up.

- Paper filing by mail or hand-delivery to your local tax office. This is often the more practical route for multi-year overdue filings because supplementary documentation is easier to manage on paper.

- Pay the tax owed. The NTA will calculate the failure-to-file additional tax and the delinquency tax separately and bill you with a fukatsushi. You can usually pay by bank transfer, convenience store payment (for amounts under ¥300,000), credit card (with a surcharge), or direct withdrawal.

Multi-Year Overdue Filings

If you owe returns for several years, file them in chronological order — earliest first. Two reasons:

- Some deductions (like loss carry-forwards from real estate or business activity) require the loss to be declared in the year incurred for it to carry forward. Filing out of order can forfeit deductions.

- The NTA processes them as a single overdue cleanup, and the failure-to-file penalty is applied per year per return — not as one consolidated penalty.

Expect the process to take several weeks per year if you’re going through a tax accountant, and longer if you’re navigating the documentation yourself in Japanese.

Special Form: Modified Return (Shusei Shinkoku)

If you filed an original return but underreported, the correct form is a shusei shinkoku (modified return), not a kigen-go shinkoku. The penalty framework is similar but uses the kashou shinkoku kasanzei (underreporting additional tax) instead of mukoshin kasanzei — rates of 10% (over ¥500K), 15% (over the larger of ¥500K or original tax × 50%). Voluntary disclosure before any audit notice can reduce or eliminate this penalty as well.

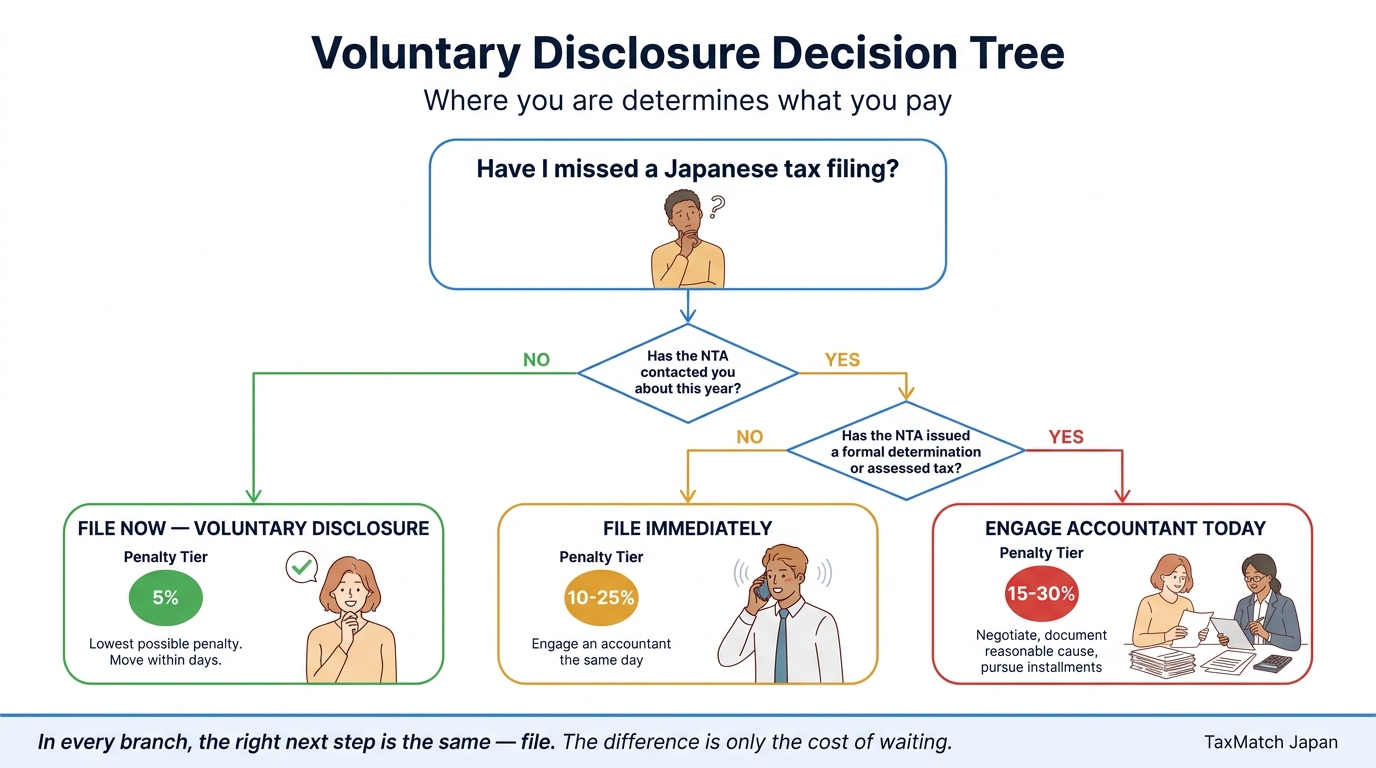

6. Voluntary Disclosure vs. Waiting for the Audit

The single largest variable in your final tax bill is whether you file before the NTA notices, or after. The math from Section 3 makes this concrete: a typical foreign resident’s penalty triples or quadruples by waiting until contact.

What Triggers an NTA Audit Notice?

A few common triggers for the NTA noticing unreported foreign-resident income:

- Treaty-based exchange of information. US-Japan, UK-Japan, and many other treaties contain Article 26 (Exchange of Information) provisions. The NTA receives flagged data on Japanese residents’ foreign financial accounts via these channels — including under the Common Reporting Standard (CRS) and FATCA.

- Real estate transactions on record. Property registrations are public, and any sale generates a paper trail that the NTA can — and does — cross-check against filed returns.

- Employer reporting mismatches. If your employer reported an RSU vest, bonus, or termination payment to the NTA but it never appeared on a return, you may be flagged for review.

- Bank reporting. Domestic Japanese banks report account openings, large transfers, and foreign-source remittances above certain thresholds. Treaty mechanisms increasingly feed equivalent data from overseas.

These mechanisms have all expanded significantly in the past decade. The “they’ll never notice” calculation that may have applied in 2010 is materially weaker in 2026.

The Voluntary Disclosure Premium

To put it in one sentence: a Foreign Lead client who voluntarily disclosed three years of unreported brokerage income on a ¥4M-cumulative liability paid about ¥200K in failure-to-file penalties; a comparable case that came to us after an NTA query letter ended up paying close to ¥1M in penalties on the same principal. The math is rarely close.

If you’re reading this guide, the right move is almost always: file voluntarily, file accurately, and file soon.

What “Voluntary” Means in Practice

The 5% voluntary tier applies only if you file before the NTA gives you formal notice of an upcoming audit — the jizen tsuchi (advance notice). Once that letter arrives, you’ve moved to the 10–25% tier even if you haven’t been audited yet. There is no “I was about to file” exception once the notice is received.

This is why we recommend that anyone who suspects they may be behind file a return — even a rough first draft followed by an amendment — before checking any other administrative item, ahead of any reasonable suspicion that they could be selected.

7. Special Situations for Foreign Residents

Four overdue-filing scenarios show up disproportionately often for foreigners. The underlying tax rules are covered in detail in dedicated guides — here we focus on what makes each scenario overdue and where to read the full treatment.

Left Japan Without Filing a Final Return

A mid-year departure normally requires either a partial-year final return before leaving, or appointment of a Nozei Kanrinin (Section 8) to file from Japan after you’ve gone. Skipping both — common for sudden job moves — leaves the obligation overdue and the NTA assessing against your last known address. Engaging a Japan-resident tax representative now gives the NTA a domestic channel and usually unlocks a more constructive resolution.

→ Full pre-departure framework: Leaving Japan: Complete Tax & Financial Checklist · Japan Exit Tax for Foreigners

Non-Permanent Resident Who Remitted Foreign Income

The Non-Permanent Resident (NPR) regime taxes foreign-source income only when remitted to Japan. The frequent overdue trigger: NPRs assume “no foreign income is taxable” rather than “only the remitted portion is taxable.” Anything wired in, paid via a foreign card chargeable to a non-Japan account, or otherwise brought into the country is fully taxable in the year of remittance — and reconstructing what counted as a remittance is often the hardest part of the cleanup.

→ Full NPR framework: Non-Permanent Resident & Remittance Rule in Japan

RSUs or Foreign Equity Compensation

Equity compensation from a foreign parent company is fully taxable in Japan at vesting (RSUs) or exercise (options), whether or not you sold any shares. US, UK, and other foreign parents frequently fail to withhold or report Japanese income tax on these awards — leaving the employee with an undeclared liability they may not realize exists. Retrospective math can be material: 1,000 RSUs vesting at ¥50,000/share is a ¥50M income inclusion in that year alone.

→ Full equity comp framework: RSU & Stock Option Tax in Japan

Foreign Brokerage Account

Permanent Residents and post-5-year NPRs must report worldwide investment income — dividends, interest, and (depending on character) capital gains from any foreign brokerage. Many foreigners maintain a home-country account for years without realizing the obligation. A separate filing — the Zaisan Saimu Chosho (Statement of Foreign Assets) — applies when foreign assets exceed ¥50M at year-end, and underreports tied to undisclosed foreign assets carry a 10% penalty surcharge on top of the standard rates in Section 3.

→ Full overseas-asset framework: Overseas Asset Reporting (CRS & OAR) in Japan · Capital Gains Tax for Foreign Residents

8. Tax Representative for Departed Residents (Nozei Kanrinin)

If you have already left Japan and have overdue Japanese tax filings to address, you cannot simply submit a return from overseas. Japanese tax law requires non-residents with continuing Japanese tax obligations to appoint a Nozei Kanrinin — a tax representative resident in Japan who acts as the formal interface with the NTA.

What the Nozei Kanrinin Does

- Receives all NTA correspondence — including determinations, audit notices, and refunds — on your behalf.

- Files returns and modifications.

- Makes tax payments and receives refund deposits.

- Communicates with the assigned tax office in Japanese.

A Nozei Kanrinin is not legally responsible for your tax — you remain the taxpayer. The representative is purely an administrative agent.

Who Can Serve as Your Representative?

- An individual resident in Japan (most commonly a spouse, family member, or trusted friend in Japan).

- A Japanese tax accountant (zeirishi) — by far the more typical choice for foreigners with substantive overdue filings to manage.

The Appointment Procedure

- Complete the Nozei Kanrinin no Todokede-sho (Notice of Tax Representative Appointment) — Form 18 in NTA documentation.

- Submit to the tax office covering your last Japanese address (or, for those who never had one, your tax representative’s office).

- The appointment takes effect on the date received by the NTA — there is no review or approval process.

For overdue cases, the practical sequence is to engage a Japanese tax accountant first, who will then file the Nozei Kanrinin notification alongside the substantive overdue returns. Most bilingual accountants in Japan handle this routinely.

A Note on Payment Mechanics from Overseas

Even with a Nozei Kanrinin, paying Japanese tax from overseas is logistically clunky. Your representative typically handles payment via Japanese bank transfer using funds you remit to them in advance. International remittances and FX cost should be budgeted into the overall cleanup expense.

9. How to Reduce or Avoid Japan Overdue Tax Penalties

Once you’ve decided to address the overdue filings, several legitimate strategies can reduce the total cost.

File Voluntarily and Quickly

Already covered, but worth re-stating: the difference between the 5% voluntary tier and the 30% post-determination tier is six-fold. Speed is the single highest-leverage variable.

Pay the Tax Even If You Can’t Finalize the Return

If you have a rough sense of how much you owe but can’t yet complete a fully accurate return, you can make an estimated payment to start. While this won’t eliminate the failure-to-file penalty, it stops the entaizei interest clock on whatever portion of the principal you’ve paid. Given that 2026 interest is 9.1% annually after the 2-month mark, this is meaningful for larger liabilities.

Request an Installment Plan (Bunno)

For substantial liabilities, the NTA may grant a payment plan (bunno or nozei no yuyo) over up to one year, which lowers the applicable delinquency tax rate on the deferred portion (typically a 1.4% concessional rate vs. the standard 9.1%). The application is via Form 19 and requires documentation of financial hardship and good-faith effort.

Use Reasonable Cause Defenses

If your overdue filing was caused by a discrete external event — natural disaster, severe illness with documentation, demonstrable error by a third party — you can submit a seitou na riyu (reasonable cause) representation. Successful claims can reduce or eliminate the failure-to-file penalty. The bar is high and the NTA does not interpret “I didn’t know” as reasonable cause, but documented and extreme circumstances do qualify.

Engage a Tax Accountant Early

This is self-serving advice on a tax-accountant-matching website, but the data backs it: among Foreign Lead clients who engaged an accountant before filing an overdue return, average effective penalty rates ran 30–40% lower than those who filed solo and then engaged help during the assessment process. Accountants can:

- Identify deductions and offsets that reduce the underlying tax base.

- Communicate the reasonable-cause case credibly to the NTA in Japanese.

- Negotiate installment arrangements before delinquency tax accumulates further.

- Coordinate multi-year filings to optimize loss carryforwards.

For overdue cases above ¥500,000 in expected tax, the accountant fee will almost always be smaller than the penalty avoidance.

10. Frequently Asked Questions

Will I be deported or have visa issues for filing an overdue Japanese tax return?

In nearly all cases, no. Tax filings and Immigration are administratively separate, and there is no automatic visa consequence for an overdue civil tax filing. The exception is criminal tax evasion (a separate category from civil failure to file), which can affect status of residence — but that requires deliberate fraud, not a missed filing. Many foreign residents handle multi-year overdue cleanups without any immigration impact.

What happens if I just ignore the overdue filing?

The NTA will eventually issue a kettei (determination) using whatever income information they have on file, often inflating the assessment because they default to a no-deductions calculation. The failure-to-file penalty climbs to the 15–30% tier, delinquency tax keeps running, and — for substantial unpaid liabilities — the NTA can pursue collection through bank account attachment, property liens, and asset seizure. For residents with assets in Japan or anyone who may want to return, ignoring is not a viable strategy.

Can the NTA come after me if I left Japan years ago?

Yes, within the 5-year statute (7-year for fraud). For residents who have moved to countries with active tax information-sharing treaties with Japan, the NTA can request enforcement assistance from the foreign tax authority — and increasingly does so for material liabilities. The cleaner path is voluntary cleanup before this escalation occurs.

I think I might owe but I’m not sure. Should I file?

If you have a credible reason to suspect a filing obligation, get a quick assessment from a bilingual tax accountant. Many — including all certified TaxMatch Japan partners — will do a 30-minute review at no cost to determine whether you have an actual obligation. The downside risk of filing when you didn’t need to is minimal; the downside risk of not filing when you needed to is six-fold higher penalties plus interest.

How long does it take to clean up multi-year overdue filings?

For a representative case (3–5 years overdue, moderate complexity, voluntary filing), expect 4–8 weeks from engagement to filing — driven mostly by gathering historical documents from former employers, brokerages, and banks. Complex international cases (foreign equity compensation, foreign brokerages, treaty positions) can take 3–4 months. The NTA processing time after filing is typically 4–8 weeks for the assessment.

Will filing one overdue return trigger a broader audit?

Filing an overdue return does not automatically trigger an audit, but it does invite review of the year being filed and — to a lesser extent — adjacent years. If you have other unfiled years, the safer move is to disclose them all together rather than file them serially. The NTA may notice the omission of a closely-adjacent year either way.

What’s the cheapest path if I owe a lot of back tax?

Three principles: (1) file voluntarily, immediately, even if rough — to lock in the 5% tier; (2) pay something against the principal to slow entaizei; (3) engage representation early to claim all available deductions and to pursue installment arrangements. In our experience, executing these three steps in the first week of awareness typically saves 25–40% on the final bill compared to delayed action.

Does the 5% voluntary-disclosure rate still apply if my employer caused the underreport?

If your employer issued an incorrect gensen choshu-hyo or failed to report a vest, the underlying obligation is still yours — but the situation can support a stronger reasonable-cause representation and, in cases where the employer’s error is documented, may reduce the penalty further. Discuss with a tax accountant before filing; the framing of the return matters.

11. Get Expert Help With Overdue Filings

Overdue Japanese tax filings are stressful, but they are resolvable, and the difference between handling them right and handling them poorly is meaningful — typically in the tens to hundreds of thousands of yen for moderate cases, and into seven figures for complex multi-year situations.

The single highest-leverage action is to engage a bilingual tax accountant immediately — before the NTA contacts you — and to file voluntarily within the 5% penalty tier. Every week of delay materially increases your total cost.

TaxMatch Japan maintains a vetted roster of bilingual tax accountants across Japan with specific experience in overdue foreign-resident filings, departed-resident cases, foreign equity compensation, and US/UK/EU treaty positions. Initial consultations are free, and matching takes 1–2 business days.

Related Guides

Tax Filing Guide for Foreigners

The on-time filing mechanics — every step to file kakutei shinkoku correctly

Japan Tax Calendar 2026

Every deadline foreigners need to know to avoid future overdue filings

Leaving Japan: Tax Checklist

Pre-departure final return + appointing a Nozei Kanrinin from overseas

NPR & Remittance Rule

What counts as a taxable remittance during Non-Permanent Resident years

Don’t wait for the NTA letter. Voluntary is 5%. Wait, and it’s 30%.

Get Matched with a Bilingual Tax Accountant →

Or message us directly on WhatsApp