Overseas Asset Reporting (CRS & OAR) in Japan for Foreign Residents (2026) | TaxMatch Japan

If you are a foreign resident in Japan with overseas bank accounts, brokerage portfolios, real estate, retirement accounts, or crypto-assets totaling more than 50 million yen, you have a legal obligation to report them to the National Tax Agency every year. The Overseas Asset Report (国外財産調書 / kokugai zaisan chousho) is not optional — and with the CRS data exchange now feeding your offshore account balances directly to the NTA, the agency already knows what you have. Filings hit a record 14,544 in 2025, with total disclosed wealth surging 26.3% to 8.19 trillion yen. This guide explains every reporting requirement for 2026.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Overseas asset reporting rules are subject to legislative amendments. Always consult a qualified tax professional (税理士 / zeirishi) for advice specific to your situation.

Need a bilingual tax accountant? Get matched with an international tax specialist — free.

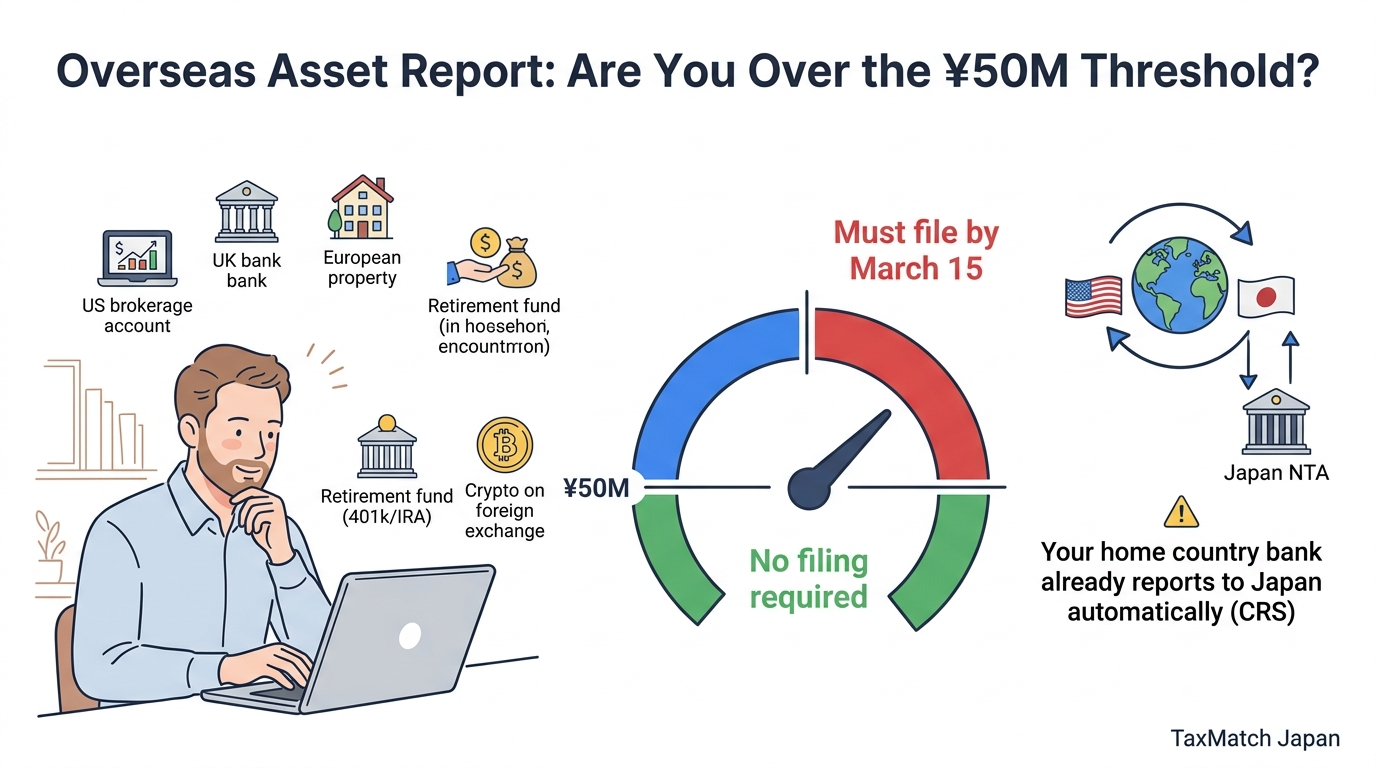

Overseas Asset Report: Are you over the ¥50M threshold?

Table of Contents

1. Overseas Asset Report (OAR) Requirements

The OAR (国外財産調書 / kokugai zaisan chousho) is Japan’s primary tool for tracking offshore wealth. You must file it if both conditions are met:

- You are a Permanent Tax Resident of Japan (Japanese nationals, or foreign nationals who have lived in Japan for more than 5 years within the past 10 years)

- Your total overseas assets exceed 50 million yen as of December 31

Tip

Non-Permanent Residents (NPRs) — foreign nationals who have lived in Japan for 5 years or less within the past 10 years — are exempt from the OAR, regardless of how much offshore wealth they hold. However, the moment you transition to Permanent Tax Resident status, the reporting obligation kicks in immediately.

Filing Deadline

The OAR deadline has been permanently decoupled from the March 15 income tax deadline. The current statutory deadline is June 30 of the year following the December 31 assessment date. For example, assets held as of December 31, 2026 must be reported by June 30, 2027.

Why the Threshold Is Catching More People

The sustained depreciation of the yen has dramatically inflated the yen-denominated value of foreign assets. A US brokerage account worth $300,000 that was comfortably below the 50 million yen threshold a few years ago now easily exceeds it at current exchange rates — without the owner acquiring any new assets. The NTA has confirmed a 9.8% year-over-year increase in OAR filings, indicating that the reporting net is expanding rapidly.

2. What You Must Report

The NTA’s definition of “overseas assets” is exhaustively broad. You must disclose the type, quantity, location, and valuation of each asset.

Reportable Asset Categories

| Category | Examples |

|---|---|

| Financial accounts | Foreign bank accounts, brokerage accounts, money market accounts |

| Securities | Foreign-issued stocks, bonds, mutual funds, ETFs |

| Real estate | Overseas residential and commercial property, land |

| Retirement accounts | US 401(k), IRA, UK SIPP, Australian superannuation (vested balance) |

| Life insurance | Foreign life insurance policies (cash surrender value) |

| Crypto-assets | Crypto held on foreign exchanges, decentralized protocols, offshore wallets |

| Tangible assets | Vehicles, precious metals in foreign vaults, vessels |

Warning

Foreign retirement accounts (401(k), IRA, etc.) must be reported even if the funds are locked and cannot be withdrawn without penalty. The NTA does not distinguish between accessible and inaccessible funds — if the account has a vested cash value, it must be declared. State-backed public pensions (Social Security, UK State Pension) without a distinct account balance are generally excluded.

3. CRS Automatic Data Exchange

The Common Reporting Standard (CRS) is the OECD framework that enables tax authorities worldwide to automatically share financial account data. It is the primary engine behind NTA enforcement of the OAR.

How CRS Works

- Financial institutions in 100+ participating jurisdictions identify accounts held by foreign tax residents

- They report account balances, interest, dividends, and gross sale proceeds to their local tax authority

- That authority transmits the data to the account holder’s country of tax residence (Japan)

- The NTA cross-references CRS data against your filed OAR and income tax return

Key CRS partner jurisdictions include the UK, Australia, Singapore, Hong Kong, Switzerland, and the entire EU. If you have an account in any of these countries, the NTA already knows about it.

CARF: Crypto-Asset Reporting Framework (2026)

Starting January 2026, Japan fully integrates the Crypto-Asset Reporting Framework (CARF) into its compliance infrastructure. Under CARF, foreign crypto exchanges must report:

- Gross proceeds from crypto sales

- Volume of crypto-to-crypto exchanges

- Transfers to external hardware wallets

This closes a massive historical loophole. Crypto-assets held on foreign exchanges are no longer invisible to the NTA.

4. Property & Debt Report (財産債務調書 / Zaisan Saimu Chousho)

The Property and Debt Report (PDR) is a separate reporting obligation that captures both domestic and foreign assets. It serves as a comprehensive wealth tracker for inheritance tax planning purposes.

Who Must File

You must file the PDR by June 30 if you meet either criterion:

- Income + Assets Test: Annual income exceeds 20 million yen AND total worldwide assets are 300 million yen or more (or financial securities alone are 100 million yen or more)

- Wealth Test: Total worldwide assets are 1 billion yen or more, regardless of income

OAR vs. PDR: Key Differences

| Feature | OAR (国外財産調書) | PDR (財産債務調書) |

|---|---|---|

| Focus | International tax evasion | Wealth tracking & inheritance |

| Threshold | Overseas assets > 50M yen | Income > 20M + assets > 300M, or assets > 1B |

| Scope | Foreign assets only | Worldwide assets (domestic + foreign) |

| Deadline | June 30 | June 30 |

If you qualify for both, your foreign assets will appear on both reports. The NTA cross-references them internally — any discrepancy triggers an immediate desk audit.

5. US FBAR & FATCA Interaction

For US citizens and Green Card holders living in Japan, the compliance environment is uniquely complex because the same assets can trigger reporting obligations in both countries simultaneously.

Triple Reporting Overlap

| Report | Authority | Threshold | Scope | Deadline |

|---|---|---|---|---|

| Japan OAR | NTA | > 50M yen (year-end snapshot) | All overseas assets incl. real estate | June 30 |

| US FBAR | FinCEN | > $10,000 (max at any time) | Financial accounts only (excludes real estate) | Apr 15 (auto-ext. Oct 15) |

| US FATCA | IRS | Varies ($400K-$600K for expats) | Financial accounts + securities | Apr 15 (with Form 1040) |

Key Discrepancies

- Real estate: Direct foreign real estate must be reported on Japan’s OAR but is excluded from FBAR and FATCA

- Valuation timing: Japan OAR uses a December 31 snapshot; FBAR uses the maximum value at any point during the year

- Exchange rates: Japan mandates the TTB rate from Japanese banks; the US Treasury specifies its own year-end rate

- The same account will yield different base values on Japanese and US forms

Tip

US citizens in Japan should maintain dual sets of translated accounting records. Keep Japanese TTB rate conversions separate from US Treasury rate conversions to avoid cross-border audit risks when the different figures are compared.

6. Valuation Methods

The NTA has strict rules for how different asset types must be valued. Generalized estimates are not accepted.

Currency Conversion: The TTB Mandate

All foreign currency assets must be converted to yen using the Telegraphic Transfer Buying (TTB) rate — the rate at which a Japanese bank buys foreign currency — as of December 31. If December 31 is a holiday, use the last preceding business day’s rate.

Warning

You cannot use the mid-market rate, the TTS (selling) rate, annual average rates, or historical rates from when you purchased the asset. Using the wrong exchange rate can trigger the 5% punitive penalty addition if it results in under-reporting.

Valuation by Asset Type

| Asset Type | Valuation Method |

|---|---|

| Listed securities, mutual funds | Closing market price on final trading day of the year |

| Bank accounts | Balance as of December 31, converted at TTB rate |

| Real estate | Fair Market Value (FMV) — not foreign municipal tax assessments |

| Retirement accounts (401k, IRA, SIPP) | Entire vested balance at TTB rate |

| Life insurance | Cash surrender value (not death benefit) |

| Crypto-assets | Market price on December 31 on the exchange used |

| Unvested RSUs / unexercised options | Generally not reportable until vested |

For overseas real estate, the favorable Japanese domestic assessed values (路線価 / rosenka) do not apply. You must use actual Fair Market Value based on independent appraisals or comparable sales data.

7. Penalties & Incentive Structure

The NTA uses a calibrated system of penalties and incentives to enforce compliance with the OAR.

Criminal Liability

Failure to file the OAR, or deliberately filing fraudulent data, can result in a fine of up to 500,000 yen or imprisonment for up to 1 year.

The 5% Addition/Reduction Mechanism

The true enforcement power lies in how the OAR interacts with standard tax penalties when the NTA discovers undeclared offshore income:

| Scenario | Effect on Penalty |

|---|---|

| Asset was properly reported on OAR | 5% reduction in under-reporting penalty (e.g., 15% → 10%) |

| Asset was omitted from OAR | 5% addition to under-reporting penalty (e.g., 15% → 20%) |

| Deliberate concealment | Heavy Penalty Tax: 35-40% of unpaid tax |

The asymmetric incentive makes compliance significantly more advantageous than non-compliance. Filing the OAR properly can reduce your penalties by 5%, while failing to file increases them by 5%.

Overseas asset reporting is high-stakes. A bilingual tax accountant who handles international clients can ensure you’re fully compliant. Get matched free →

8. Enforcement Trends (2026)

The NTA’s enforcement posture has fundamentally shifted from passive collection to proactive, data-driven detection.

Automated CRS Cross-Referencing

The NTA ingests millions of CRS records from 100+ jurisdictions and runs algorithmic comparisons against domestic OAR filings. If a Swiss bank account appears in the CRS data but is absent from your OAR, an automated alert is generated for the international taxation division. In one prominently cited case, the NTA used CRS data to detect an executive’s hidden overseas account, leading to severe penalty assessments.

CARF: The Next Audit Frontier

With CARF fully operational in 2026, foreign crypto exchanges now transmit transaction data directly to the NTA. The agency is expected to initiate retroactive audits targeting individuals who accumulated digital wealth outside traditional banking but failed to declare it.

Focus Areas

- High-net-worth individuals with complex offshore structures

- Expatriates with undeclared retirement account balances

- Digital economy participants (crypto traders, online creators)

- Wire transfers exceeding 1 million yen (automatically reported to NTA by receiving banks)

9. Common Mistakes

Mistake 1: Omitting Retirement Accounts

The problem: Assuming foreign retirement accounts (401(k), IRA, superannuation) are exempt because they are locked or tax-deferred in the home country. The NTA makes no such distinction — if it has a vested cash value, it must be reported.

Mistake 2: Using the Wrong Exchange Rate

The problem: Converting assets using the mid-market rate, TTS rate, or the rate from the date of asset purchase. The NTA strictly requires the TTB rate as of December 31.

Mistake 3: Using Home-Country Property Tax Assessments

The problem: Reporting overseas real estate using foreign municipal assessments (US county assessment, UK council tax band) that understate fair market value. The NTA requires FMV, not assessed values.

Mistake 4: The “Leaving Soon” Fallacy

The problem: Assuming the NTA will not pursue enforcement after you leave Japan. The NTA has a 7-year statute of limitations for international tax evasion and uses mutual assistance clauses in tax treaties to pursue liabilities internationally. The requirement to appoint a tax representative ensures a domestic legal conduit remains in place.

Mistake 5: Ignoring Equity Compensation Cross-Referencing

The problem: Assuming the NTA cannot see your foreign brokerage account. Japanese subsidiaries of foreign companies must file Form 9(3) annually, detailing all stock-based compensation (RSUs, options, ESPPs) granted to Japan-resident employees. The NTA cross-references these filings against your OAR and income tax return.

Summary

- Permanent Tax Residents with overseas assets exceeding 50 million yen must file the OAR by June 30

- CRS and CARF mean the NTA already has your offshore financial data — filing protects you from penalties

- Use the TTB rate on December 31 for all currency conversions

- Report retirement accounts, life insurance, and crypto — not just bank and brokerage accounts

- US citizens must navigate triple reporting: OAR + FBAR + FATCA

- Proper OAR filing earns a 5% penalty reduction; omission triggers a 5% penalty increase

10. When to Hire a Tax Accountant

The OAR and PDR are high-stakes compliance documents where mistakes are caught automatically by CRS algorithms. Consider hiring a bilingual tax accountant (税理士) if:

- You’re approaching or have crossed the 50 million yen threshold

- You hold complex asset types — retirement accounts, foreign real estate, crypto, equity compensation

- You’re a US citizen navigating simultaneous OAR, FBAR, and FATCA obligations

- You’re transitioning from NPR to Permanent Tax Resident and need to understand what triggers worldwide reporting

- You need proper FMV appraisals for overseas real estate

- You’ve received a notice from the NTA about discrepancies in your filings

Need help with overseas asset reporting? Get matched with an English-speaking tax accountant who handles international compliance — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

Do I need to report overseas assets in Japan?

Yes, if you are a permanent tax resident of Japan and hold overseas assets exceeding ¥50 million at the end of the year, you must file an Overseas Asset Report (kokugai zaisan chosho) by March 15. Separate reporting may also be required for overseas income exceeding ¥20 million.

What is the ¥50 million overseas asset reporting threshold?

If your total overseas assets (including bank accounts, securities, real estate, and other assets outside Japan) exceed ¥50 million as of December 31, you must file the Overseas Asset Report. Non-compliance can result in penalties and disadvantageous treatment for underreported income.

What is CRS and how does it affect foreigners in Japan?

CRS (Common Reporting Standard) is an international framework for automatic exchange of financial account information between countries. Japanese financial institutions report accounts held by foreign tax residents to the NTA, which shares this data with the account holder’s home country, and vice versa.