Real Estate Tax in Japan for Foreign Property Owners & Investors (2026) | TaxMatch Japan

Whether you are buying your first apartment in Tokyo, investing in a rental property in Osaka, or selling real estate you have held for years, Japan imposes taxes at every stage of the property lifecycle — acquisition, annual holding, income generation, and sale. For foreign owners, the rules carry additional layers: withholding obligations for non-residents, 2026 reforms targeting offshore investors, and capital gains calculations that differ dramatically depending on how long you have owned the property. Get the timing wrong on a sale, and your tax rate can more than double. This guide covers everything you need to know.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Real estate tax rules are subject to legislative amendments, including the 2026 Tax Reform Outline. Always consult a qualified tax professional (税理士 / zeirishi) for advice specific to your situation.

Need a bilingual tax accountant? Get matched with a real estate tax specialist — free.

Property in Japan: 4 tax layers you need to know

Table of Contents

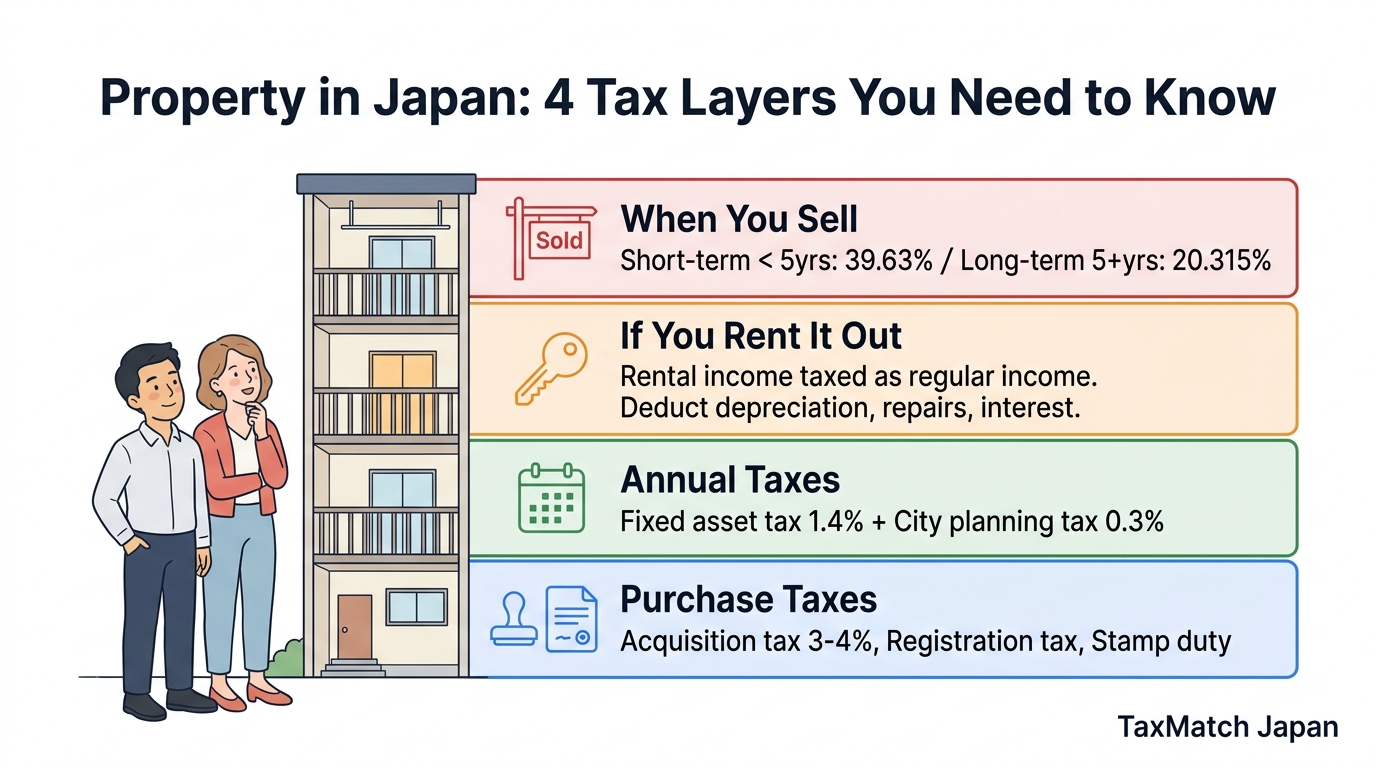

1. Taxes at Purchase

Buying property in Japan triggers three separate taxes at the point of acquisition. These are one-time costs that must be factored into your purchase budget.

Real Estate Acquisition Tax (不動産取得税 / Fudosan Shutoku Zei)

This prefectural tax is levied on the assessed value of the property (not the purchase price).

| Property Type | Standard Rate | Reduced Rate (current) |

|---|---|---|

| Land | 4% | 3% (reduced rate extended through 2026) |

| Residential buildings | 4% | 3% |

| Non-residential buildings | 4% | 4% (no reduction) |

For residential land, the assessed value base is further reduced to 50% of the assessed value, effectively halving the tax. Additional exemptions apply for new residential properties meeting certain floor area requirements (50-240 sqm).

Registration and License Tax (登録免許税 / Touroku Menkyo Zei)

This national tax is paid when registering the property transfer at the Legal Affairs Bureau (法務局). Rates depend on the type of registration:

| Registration Type | Standard Rate | Reduced Rate |

|---|---|---|

| Ownership transfer (sale) | 2.0% | 1.5% (land, through March 2026) |

| Ownership preservation (new build) | 0.4% | 0.15% (qualifying housing) |

| Mortgage registration | 0.4% | 0.1% (qualifying housing) |

Stamp Duty (印紙税 / Inshi Zei)

Revenue stamps must be affixed to the property purchase contract. The amount depends on the contract value:

| Contract Value | Stamp Duty |

|---|---|

| 10M – 50M yen | 10,000 yen |

| 50M – 100M yen | 30,000 yen |

| 100M – 500M yen | 60,000 yen |

| 500M – 1B yen | 160,000 yen |

Tip

Electronically executed contracts are exempt from stamp duty. If your real estate purchase agreement is executed digitally (and not printed), no revenue stamps are required.

2. Annual Holding Taxes

Once you own property in Japan, you pay annual taxes based on the municipal assessed value — not the market price. These taxes are due every year regardless of whether you live in or rent the property.

Fixed Asset Tax (固定資産税 / Kotei Shisan Zei)

A municipal tax levied on the owner registered as of January 1 each year.

- Standard rate: 1.4% of the assessed value (評価額 / hyoukagaku)

- Assessed values are typically 60-70% of market value and revised every 3 years

- Residential land under 200 sqm receives a 1/6 reduction (small residential land exemption)

- Residential land 200-330 sqm receives a 1/3 reduction

- New residential buildings receive a 50% reduction for 3-5 years (depending on structure)

City Planning Tax (都市計画税 / Toshi Keikaku Zei)

An additional municipal tax levied on properties within urbanization promotion areas (which includes most major city areas).

- Maximum rate: 0.3% of assessed value

- Residential land under 200 sqm receives a 1/3 reduction

Combined annual tax: For most urban residential properties, the effective annual holding tax is approximately 1.7% of assessed value (1.4% + 0.3%), which translates to roughly 1.0-1.2% of market value after the assessment discount.

Tip

Fixed asset tax bills arrive in April-June and can typically be paid in four quarterly installments. If you are a non-resident owner, you must designate a Tax Representative (納税管理人) in Japan to receive and pay these bills on your behalf.

3. Rental Income Taxation

Rental income from Japanese property is classified as real estate income (不動産所得) and taxed as part of your comprehensive income at progressive rates.

Calculating Taxable Rental Income

Taxable rental income = Gross rental revenue minus allowable deductions:

| Deductible Expense | Notes |

|---|---|

| Building depreciation | Straight-line method; useful life depends on structure type (RC: 47 years, wood: 22 years) |

| Mortgage interest | Interest portion of loan payments |

| Property management fees | Management company fees, condo association fees |

| Repairs and maintenance | Routine repairs (major renovations must be capitalized) |

| Fixed asset tax & city planning tax | Annual holding taxes are deductible |

| Insurance premiums | Fire, earthquake insurance |

| Travel expenses | Related to property management (for non-resident owners visiting Japan) |

Tax Rates on Rental Income

Rental income is added to your other income and taxed at Japan’s progressive rates (5% to 45% national, plus 10% residence tax, plus 2.1% reconstruction surtax). The combined marginal rate can reach approximately 55.945% at the top bracket.

For non-residents, rental income is Japan-source income and must be declared. If a property management company collects rent on behalf of a non-resident owner, they must withhold 20.42% of the gross rent before remitting it.

Blue Return Filing (青色申告)

Landlords who file a blue return (青色申告 / aoiro shinkoku) can claim an additional special deduction of up to 650,000 yen (if filing electronically) on their real estate income. This requires maintaining double-entry bookkeeping records.

4. Capital Gains on Sale

Capital gains on real estate are taxed separately from other income at fixed rates. The rate depends entirely on how long you have owned the property — and the difference is enormous.

Short-Term vs. Long-Term Capital Gains

| Holding Period | Classification | Tax Rate (National + Local + Surtax) |

|---|---|---|

| 5 years or less as of Jan 1 of the sale year | Short-term (短期) | 39.63% (30.63% national + 9% local) |

| More than 5 years as of Jan 1 of the sale year | Long-term (長期) | 20.315% (15.315% national + 5% local) |

| More than 10 years (primary residence) | Reduced long-term | 14.21% on first 60M yen of gain |

Warning: The January 1 Rule

The 5-year holding period is measured as of January 1 of the year of sale, not the actual sale date. If you purchased a property on March 1, 2021 and sell it on March 2, 2026, you might assume you have held it for over 5 years. But as of January 1, 2026, you have owned it for only 4 years and 10 months — making it a short-term gain taxed at 39.63% instead of 20.315%. Timing your sale carefully can nearly halve your tax bill.

Calculating Capital Gains

Capital gain = Sale price – (Acquisition cost + Transfer expenses)

- Acquisition cost: Purchase price + acquisition taxes + agent commissions + renovation costs (capitalized)

- Building depreciation: The building portion of acquisition cost must be reduced by accumulated depreciation

- Transfer expenses: Broker commissions, demolition costs, stamp duty on the sale contract

- If you cannot prove the original acquisition cost, the NTA allows you to use 5% of the sale price as a deemed cost — but this almost always results in a much larger taxable gain

Primary Residence Exemption (3,000万円特別控除)

If you sell your primary residence (マイホーム), you can deduct up to 30,000,000 yen from the capital gain. This exemption is available regardless of holding period, but it cannot be used more than once every 3 years, and the property must have been your actual home (not an investment property).

5. Non-Resident Owner Issues

Foreign nationals who own Japanese real estate but do not reside in Japan face additional compliance requirements and withholding obligations.

Withholding on Sale Proceeds

When a non-resident sells real property in Japan, the buyer (or the buyer’s agent) is generally required to withhold 10.21% of the sale price and remit it to the NTA on behalf of the seller. This applies even if the sale results in a loss. The seller can recover the overpayment by filing a tax return.

Withholding on Rental Income

Property management companies collecting rent for non-resident owners must withhold 20.42% of gross rental income before remitting to the owner.

Tax Representative Requirement

Non-resident property owners must appoint a Tax Representative (納税管理人 / nozei kanrinin) in Japan who will:

- Receive and pay annual fixed asset tax and city planning tax bills

- File income tax returns for rental income

- Handle correspondence with the tax office

Non-resident property ownership requires careful tax planning. A bilingual tax accountant can handle your filings and tax representative duties. Get matched free →

6. 2026 Tax Reform Changes

The 2026 Tax Reform Outline introduces several significant changes affecting real estate taxation for foreign owners.

Consumption Tax on Brokerage Services

Under the 2026 reforms, Japan is applying the national 10% consumption tax to real estate brokerage services rendered to non-resident buyers and sellers. Previously, these services were treated as export transactions (zero-rated). This directly increases transaction costs for offshore investors by the full brokerage commission multiplied by 10%.

Stricter Real Estate Valuation

Following a landmark 2022 Supreme Court decision, the NTA is empowered to reject standard assessed valuations (路線価 / rosenka) and demand Fair Market Value appraisals if a property was purchased close to the time of a wealth transfer (inheritance or gift) for the purpose of reducing taxable value. This directly impacts estate planning strategies involving Japanese real estate.

Rental Property Valuation Reforms

The 2026 reforms close valuation loopholes for fractionalized real estate and certain rental properties. These must now be valued based on the ordinary transaction price, preventing the use of complex ownership structures to artificially depress reportable values.

7. Practical Scenarios

Scenario A: Expat Buying a Primary Residence in Tokyo

Profile: American engineer on a work visa, buying a 60M yen apartment in Minato-ku for personal use.

Acquisition costs:

- Real estate acquisition tax: ~600,000 – 900,000 yen (depending on assessed value and exemptions)

- Registration tax: ~450,000 yen (1.5% of land assessed value + 0.15% of building)

- Stamp duty: 30,000 yen

- Agent commission: ~1.98M yen (3% + 60,000 + consumption tax)

Annual holding costs: Fixed asset + city planning tax of approximately 200,000 – 400,000 yen/year.

On sale (after 6+ years): If selling for 70M yen with a 10M yen gain, the primary residence exemption (30M yen) completely eliminates the tax liability.

Scenario B: Non-Resident Investor with Rental Property

Profile: British investor, non-resident, owns a 30M yen rental apartment in Osaka generating 1.8M yen/year gross rent.

Rental income taxation:

- Gross rent: 1,800,000 yen

- Deductions (depreciation, management fees, taxes, insurance): ~900,000 yen

- Net taxable income: ~900,000 yen

- The management company withholds 20.42% of gross rent (~367,560 yen)

- Filing a tax return allows claiming deductions and recovering the excess withholding

Scenario C: Timing a Sale to Avoid Short-Term Capital Gains

Profile: Foreign investor purchased an apartment on April 15, 2021. Wants to sell for a 15M yen gain.

- Sell in 2026: As of January 1, 2026, ownership = 4 years 8 months → short-term → tax = 15M x 39.63% = 5,944,500 yen

- Sell in 2027: As of January 1, 2027, ownership = 5 years 8 months → long-term → tax = 15M x 20.315% = 3,047,250 yen

- Savings by waiting: approximately 2.9 million yen

Summary

- Budget 5-8% of purchase price for acquisition taxes and fees

- Annual holding taxes are approximately 1.0-1.2% of market value

- Hold property for more than 5 years (measured from Jan 1) to cut capital gains tax nearly in half

- The 30M yen primary residence exemption eliminates capital gains tax on most home sales

- Non-residents face 10.21% withholding on sales and 20.42% on rental income

- Always appoint a Tax Representative if you are a non-resident owner

8. Common Mistakes

Mistake 1: Selling Too Early

The problem: Selling just before the 5-year mark (as measured from January 1) and paying the 39.63% short-term rate instead of 20.315%.

The fix: Always calculate the holding period as of January 1 of the sale year, not the actual sale date. Waiting a few months can save millions of yen.

Mistake 2: Not Filing as a Non-Resident

The problem: Assuming withholding by the buyer or management company is “final” and not filing a return. Non-residents can often recover significant overpaid tax by filing and claiming proper deductions.

Mistake 3: Losing Acquisition Cost Documentation

The problem: Without proof of the original purchase price, the NTA defaults to 5% of the sale price as cost basis, dramatically inflating your taxable gain.

The fix: Preserve all purchase contracts, receipts for renovations, and agent commission invoices indefinitely.

Mistake 4: Ignoring Building Depreciation

The problem: Failing to claim depreciation on the building portion reduces your rental income deductions. Conversely, forgetting that accumulated depreciation reduces your cost basis on sale can lead to an unexpected capital gains tax bill.

Mistake 5: Assuming Assessed Value Equals Market Value

The problem: Using the municipal assessed value (評価額) as the property’s value for financial planning. Assessed values are typically 60-70% of actual market value.

9. When to Hire a Tax Accountant

Real estate transactions involve multiple tax types across different government agencies. Consider hiring a bilingual tax accountant (税理士) if:

- You are buying your first property and want to understand total acquisition costs and available exemptions

- You own rental property and need to optimize deductions (depreciation, blue return)

- You are selling property and need to determine whether you qualify for the primary residence exemption or long-term capital gains rate

- You are a non-resident owner and need a tax representative in Japan

- You need to coordinate with home-country tax obligations (foreign tax credits, treaty benefits)

- You are planning estate or inheritance strategies involving Japanese real estate

Need help with real estate tax in Japan? Get matched with an English-speaking tax accountant who specializes in property transactions — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

What taxes do foreigners pay on property in Japan?

Foreigners pay the same property taxes as Japanese nationals: fixed asset tax (1.4% of assessed value), city planning tax (up to 0.3%), real estate acquisition tax (3-4% on purchase), registration and license tax, and stamp duty. Income tax applies to rental income, and capital gains tax applies on sale.

How is property tax calculated in Japan?

Annual fixed asset tax is 1.4% of the government-assessed value (which is typically 50-70% of market value). City planning tax adds up to 0.3%. Residential land receives a reduction (1/6 for small plots up to 200㎡). The combined annual tax is typically 1.4-1.7% of assessed value.

Do non-residents pay real estate tax in Japan?

Yes. Non-residents who own property in Japan must pay fixed asset tax and city planning tax. If they earn rental income, they must file Japanese tax returns. A 20.42% withholding tax is applied to rent payments made to non-resident landlords, which can be offset against actual tax liability.