Residence Tax in Japan for Foreigners: Complete Guide (2026)

Every June, thousands of foreigners in Japan open an envelope from their city office and get a surprise: a residence tax bill for hundreds of thousands of yen. Unlike income tax, which gets deducted from your paycheck in real time, residence tax is billed after the fact — and the timing catches many people off guard. This guide explains how residence tax works, why the timing is so confusing, and what you can do to reduce it.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax rules and rates may change. Always consult a qualified tax professional (zeirishi) for advice specific to your situation.

Need a bilingual tax accountant? Get matched with a specialist — free.

Table of Contents

Residence Tax: The delayed billing cycle

1. What Is Residence Tax (Juminzei)?

Residence tax (住民税 / juminzei) is a local tax paid to your city, town, or village in Japan. It is separate from national income tax. While income tax goes to the central government, residence tax funds local services like schools, garbage collection, roads, and public health.

Every person who lives in Japan and earns income is subject to residence tax. This includes foreign nationals on any visa type — work visa, spouse visa, student visa (if you have income), or permanent residency.

There are actually two components bundled together:

- Prefectural tax (都道府県民税) — paid to your prefecture (e.g., Tokyo-to, Osaka-fu)

- Municipal tax (市区町村民税) — paid to your city or ward

You will never see these billed separately. They arrive as a single “residence tax” bill.

2. How Residence Tax Is Calculated

Residence tax has two parts:

Income-Based Portion (所得割)

This is the big one. The standard rate is 10% of your taxable income from the previous year. It breaks down as:

- 6% to your municipality

- 4% to your prefecture

“Taxable income” here means your total income minus deductions (more on deductions later). It uses the same income figure as your income tax return but applies its own set of deduction amounts.

Per-Capita Levy (均等割)

This is a flat amount charged to everyone regardless of income. The standard amount is approximately 5,000 yen per year (typically 3,500 yen municipal + 1,500 yen prefectural). Some municipalities add a small surcharge, but the difference is minor.

Starting from the 2024 tax year, the national Forest Environment Tax (森林環境税) of 1,000 yen is also collected alongside the per-capita levy, bringing the typical total flat charge to about 5,000-6,000 yen.

Example Calculation

If you earn 5,000,000 yen per year (gross salary):

| Step | Amount |

|---|---|

| Gross salary | 5,000,000 yen |

| Employment income deduction | -1,440,000 yen |

| Social insurance deduction (est. ~15%) | -750,000 yen |

| Basic deduction | -430,000 yen |

| Taxable income for residence tax | ~2,380,000 yen |

| Income-based portion (10%) | 238,000 yen |

| Per-capita levy | ~5,000 yen |

| Total residence tax | ~243,000 yen/year (~20,250 yen/month) |

This is a simplified estimate. Your actual amount will vary based on your specific deductions.

If you earn 8,000,000 yen per year: Your residence tax would be roughly 410,000-430,000 yen per year, or about 35,000 yen per month.

Section Summary

- Residence tax is a flat 10% of taxable income plus a small per-capita levy (~5,000-6,000 yen)

- It is split between your municipality (6%) and prefecture (4%)

- For a 5M yen salary, expect roughly 243,000 yen/year; for 8M yen, roughly 410,000-430,000 yen/year

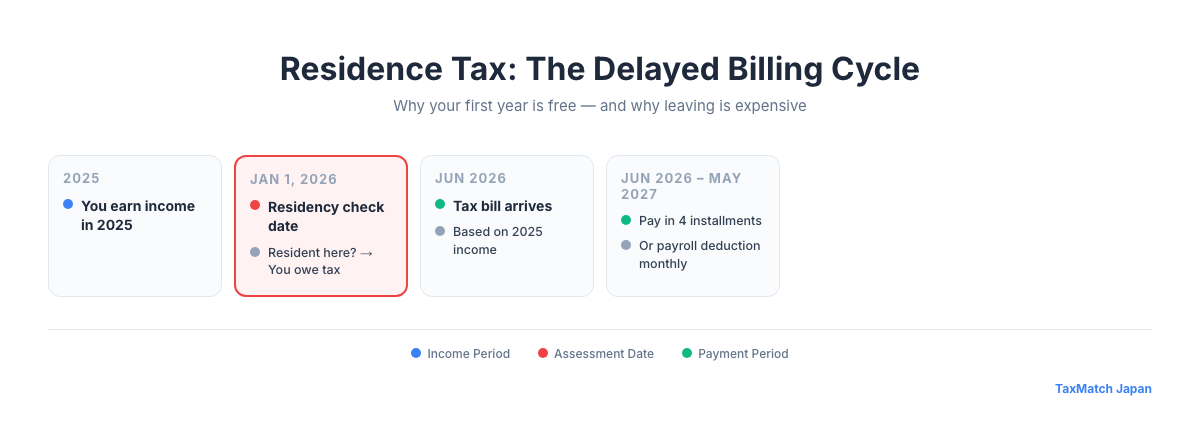

3. The January 1st Rule: Why the Timing Is So Confusing

Here is the single most important thing to understand about residence tax:

Residence tax is based on where you lived on January 1st of the current year, and it taxes your income from the previous calendar year.

This creates two situations that surprise foreigners constantly:

If You Just Arrived in Japan

If you moved to Japan in, say, March 2025, you will not owe any residence tax in 2025. Why? Because on January 1st, 2025, you were not a resident of any Japanese municipality. Your 2025 income will eventually be taxed, but not until June 2026.

This means your first year in Japan feels cheap. Your second year, when the bill finally arrives, feels like a shock.

If You Are Leaving Japan

If you lived in Japan on January 1st, 2026, you owe residence tax for the full year — even if you leave Japan in February. The tax is based on your 2025 income, and you are locked in once January 1st passes.

Many people leave Japan thinking they are done with Japanese taxes, only to receive a residence tax bill months later at an address they no longer live at (or forwarded to their home country). For a complete checklist of what to handle before departure, see our leaving Japan tax checklist.

Warning

January 1st is the “snapshot date.” If you are registered as a resident of a Japanese municipality on that date, you owe that municipality residence tax for the entire fiscal year. Plan your departure timing carefully — leaving before January 1st can save you roughly 10% of your previous year’s income.

4. Payment Timeline

Residence tax follows a delayed schedule:

| When | What Happens |

|---|---|

| January – December 2025 | You earn income |

| February – March 2026 | You (or your employer) files tax return for 2025 income |

| June 2026 | You receive your residence tax bill based on 2025 income |

| June 2026 – May 2027 | You pay the residence tax |

There are two payment methods:

Special Collection (特別徴収) — Payroll Deduction

If you are a company employee, your employer will deduct residence tax from your paycheck in 12 monthly installments from June through May of the following year. This is the most common method and requires no action on your part.

Your company receives the tax notice directly from your municipality.

Ordinary Collection (普通徴収) — Pay It Yourself

If you are self-employed, a freelancer, or your employer does not handle payroll deduction, you will receive a bill at your home address and pay in 4 quarterly installments:

| Installment | Due Date |

|---|---|

| 1st | End of June |

| 2nd | End of August |

| 3rd | End of October |

| 4th | End of January |

You can pay at convenience stores, banks, or by bank transfer. Many municipalities now accept credit card and smartphone payment (PayPay, LINE Pay, etc.).

Section Summary

- Residence tax for 2025 income arrives in June 2026 and is paid over 12 months (payroll) or 4 installments (self-pay)

- Employees pay via payroll deduction (special collection); freelancers and self-employed pay directly (ordinary collection)

- Multiple payment methods are available, including convenience stores, banks, and smartphone apps

5. Special Situations for Foreigners

Just Arrived in Japan

As explained above, if you arrived after January 1st, you will not receive a residence tax bill until June of the following year. Use this grace period wisely — set aside money monthly so the bill does not catch you off guard.

Pro tip: If you arrive in Japan in October 2025 and earn 1,500,000 yen by December 2025, you will owe roughly 80,000-100,000 yen in residence tax starting June 2026. Budget for it from day one.

Leaving Japan Mid-Year

This is where many foreigners run into trouble. If you are leaving Japan, you have two options:

Option A: Pay everything before you leave. Contact your city office and request to pay your remaining residence tax in a lump sum before your departure date. This is the cleanest approach.

Option B: Appoint a tax representative (納税管理人). If you cannot pay everything before leaving, you must file a Tax Representative Notification (納税管理人届出書) with your municipal office. This person (a friend, colleague, former employer, or tax accountant in Japan) will receive your tax bills and handle payment on your behalf.

Warning

If you do neither, the city office will send bills to your last known address. If they go unpaid, penalties will accrue, and it could cause problems if you ever return to Japan or need a certificate of tax payment. See our leaving Japan tax checklist for the full departure process.

Working Remotely for an Overseas Company

If you live in Japan and work remotely for a company outside Japan, you are still subject to residence tax on that income. Japan taxes based on where you live, not where your employer is located.

You will need to file your own income tax return (確定申告) and report your overseas income. Your residence tax will then be calculated based on that return, and you will pay via ordinary collection (the 4-installment method). For details on how to file, see our step-by-step tax return filing guide.

Important: If your overseas employer does not withhold Japanese taxes, you are responsible for both income tax and residence tax payments yourself.

Very Low Income

If your income is below a certain threshold, you may be exempt from part or all of residence tax. The exact threshold varies by municipality, but as a general guide:

- Per-capita levy exemption: Total income below roughly 450,000 yen (single, no dependents)

- Income-based exemption: Total income below roughly 450,000 yen (varies by municipality and number of dependents)

Students with minimal part-time income may qualify for these exemptions.

Confused about your residence tax obligations? A bilingual tax specialist can help. Get matched free →

6. How to Reduce Your Residence Tax

Since residence tax is 10% of taxable income, every deduction that lowers your taxable income also lowers your residence tax. Here are the most impactful ones:

1. Dependents Deduction (扶養控除)

If you financially support family members — including parents or siblings living overseas — you can claim a dependents deduction. Each qualifying dependent reduces your taxable income by 330,000 yen (for residence tax purposes). Specific amounts vary:

- General dependent (age 16-18, 23+): 330,000 yen

- Specific dependent (age 19-22): 450,000 yen

- Elderly dependent (age 70+, living together): 450,000 yen

- Elderly dependent (age 70+, living apart): 380,000 yen

For overseas dependents: You will need to provide remittance records proving you sent money to support them. Since 2024, overseas dependents aged 30-69 must meet specific income or remittance requirements to qualify.

2. Social Insurance Deduction (社会保険料控除)

All social insurance premiums you pay — health insurance, pension (kosei nenkin or kokumin nenkin), employment insurance — are fully deductible. This is usually the largest deduction for employees and can easily exceed 700,000 yen per year.

3. Medical Expenses Deduction (医療費控除)

If your household’s total medical expenses exceed 100,000 yen per year (or 5% of income if income is under 2,000,000 yen), you can deduct the excess. This includes dental work, hospital visits, prescription medication, and even some transportation costs to medical facilities.

4. iDeCo (個人型確定拠出年金)

Contributions to iDeCo, Japan’s individual defined-contribution pension plan, are fully deductible from your taxable income. The maximum contribution depends on your employment status:

- Company employees (with corporate pension): 144,000 yen/year

- Company employees (without corporate pension): 240,000 yen/year

- Self-employed: 816,000 yen/year

Contributing 240,000 yen/year to iDeCo would reduce your residence tax by 24,000 yen/year (240,000 x 10%).

5. Furusato Nozei (ふるさと納税)

Furusato nozei is Japan’s hometown tax donation program, and it is one of the most popular tax optimization tools in the country. Here is how it works:

- You donate to municipalities of your choice

- You receive gifts (local specialties like wagyu beef, rice, fruit, seafood)

- Your residence tax is reduced by the donation amount minus 2,000 yen

Example: If you donate 60,000 yen through furusato nozei, your residence tax drops by approximately 58,000 yen. You effectively get 58,000 yen worth of local products for just 2,000 yen out of pocket.

The maximum effective donation amount depends on your income and other deductions. For someone earning 5,000,000 yen with no dependents, the limit is roughly 60,000-67,000 yen.

For a detailed walkthrough of the entire process, including platforms, limits, and common traps, see our complete furusato nozei guide for foreigners.

6. Spouse Deduction (配偶者控除)

If your spouse earns under 480,000 yen/year (after the employment income deduction), you can claim a spouse deduction of 330,000 yen for residence tax purposes. A partial deduction is available if your spouse earns up to 1,330,000 yen.

Section Summary

- Every deduction that reduces taxable income also reduces residence tax by 10% of the deducted amount

- Key deductions: dependents (330,000+ yen each), social insurance (fully deductible), medical expenses, iDeCo, furusato nozei, and spouse deduction

- Furusato nozei is one of the most powerful tools — you redirect tax payments and receive gifts in return

7. What Happens If You Don’t Pay

Ignoring your residence tax bill is a bad idea. Here is the escalation:

- Late payment penalty (延滞金): Interest accrues from the day after the due date. The rate is approximately 2.4% for the first two months, then jumps to roughly 8.7% annually after that (rates are set each year).

- Reminder notices (督促状): Your city office will send increasingly urgent payment demands.

- Asset seizure (差押え): The municipality has the legal authority to seize your bank account, salary, or other assets. This is not theoretical — it happens. Foreign residents have had their bank accounts frozen for unpaid residence tax.

- Impact on visa renewal: While not an automatic disqualification, unpaid taxes can cause problems during visa renewal. Immigration may request a Certificate of Tax Payment (納税証明書), and an inability to provide one raises red flags.

- Problems if you return to Japan: Unpaid taxes remain on record. If you leave Japan with unpaid residence tax and return years later, the debt may still be waiting for you.

Warning

If you are struggling to pay, contact your city office immediately. Most municipalities offer installment plans for people experiencing financial hardship. They would rather work with you than chase you for payment.

8. When You Need a Tax Accountant’s Help

For many employed foreigners, residence tax is handled automatically through payroll deduction, and you may never need professional help. However, consider consulting a tax accountant (税理士 / zeirishi) if:

- You have income from multiple countries and need to understand how foreign tax credits apply

- You are leaving Japan and need to settle your tax obligations or set up a tax representative

- You are self-employed or freelancing and need to file your own tax return correctly

- You have overseas dependents and want to maximize your deduction claims with proper documentation

- You received a large bonus, stock options, or RSUs and want to plan your tax strategy

- You received a tax notice you don’t understand — tax documents from the city office are entirely in Japanese

- You have unpaid taxes and need help negotiating a payment plan

A tax accountant can also run the numbers on optimization strategies like iDeCo and furusato nozei to make sure you are taking full advantage of available deductions. For guidance on typical fees, see our tax accountant pricing guide.

Need help with your residence tax? Get matched with an English-speaking tax accountant — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

What is residence tax in Japan?

Residence tax (juminzei) is a local tax of approximately 10% (6% prefectural + 4% municipal) levied on your previous year’s income. It is separate from national income tax and is paid to the municipality where you lived on January 1 of the tax year.

How is residence tax calculated for foreigners?

Residence tax is calculated at a flat rate of approximately 10% of your taxable income from the previous year, plus a per-capita levy of approximately ¥5,000. The same deductions available for income tax generally apply, though amounts may differ slightly.

Do I pay residence tax if I leave Japan mid-year?

If you were a resident of Japan on January 1, you are liable for the full year’s residence tax based on the previous year’s income, even if you leave Japan during the year. You should appoint a tax agent (nozei kanrinin) to handle payments after departure.