RSU & Stock Option Tax in Japan — Complete Guide for Foreigners

RSU & Stock Option Tax: The two tax events you need to know

Everything foreign residents need to know about RSU and stock option taxation in Japan — from the moment shares vest to how to avoid double taxation legally.

Receiving RSUs or stock options from a foreign company in Japan? Get matched with a bilingual specialist — free.

Get Expert Help Free →If you work at GAFAM, a major bank, or any multinational company in Japan, RSUs (Restricted Stock Units) and stock options are likely a meaningful part of your compensation. The moment those shares vest, Japan’s National Tax Agency (NTA) is paying close attention — even if the shares land in your US brokerage account.

This guide covers everything you need to know: how RSUs and stock options are taxed, how proration works for multi-country situations, the powerful Non-Permanent Resident strategy, and the filing requirements that trip up even sophisticated expats.

RSU Tax in Japan: The vesting surprise

How Are RSUs Taxed in Japan?

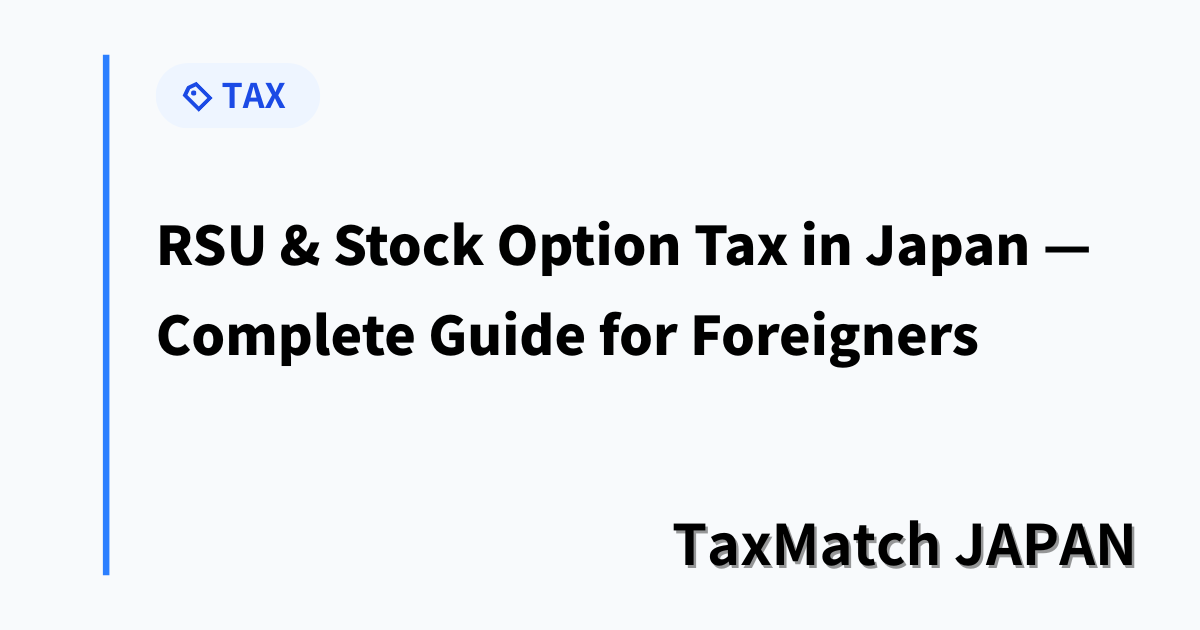

Japan taxes RSUs as employment income (給与所得) at the moment shares vest — not when you sell them. This catches many expats off guard.

📌 Key Point: Vesting = Taxable Event

The day your RSU restrictions lift and shares are delivered to your account is when Japan taxes you — regardless of whether you sell the shares, hold them, or they subsequently drop in value. The taxable amount is calculated as: Fair Market Value (FMV) on vesting date × number of shares vested, converted to JPY at the TTM rate on that date.

Tax Rates: Up to 55.945%

RSU income is added to your other salary and taxed at Japan’s progressive income tax rates. Combined with local inhabitant tax, effective rates for high earners are brutal:

| Taxable Income (after deductions) | National Tax Rate | Combined Rate (incl. local tax + reconstruction surcharge) |

|---|---|---|

| Up to ¥1,950,000 | 5% | ~15.1% |

| ¥1.95M – ¥3.3M | 10% | ~20.2% |

| ¥3.3M – ¥6.95M | 20% | ~30.4% |

| ¥6.95M – ¥9M | 23% | ~33.5% |

| ¥9M – ¥18M | 33% | ~43.7% |

| ¥18M – ¥40M | 40% | ~50.8% |

| Over ¥40M | 45% | ~55.9% |

One important relief: the employment income deduction (給与所得控除) applies to RSU income. For high earners, this is capped at ¥1.95 million. Still, the deduction meaningfully reduces the taxable base compared to some other countries.

Avoid double taxation on your equity compensation with professional cross-border tax planning.

Get Expert Help with RSU & Stock Option Tax →Free matching · No obligation · English support

What Happens When You Sell the Shares?

After the vesting tax is paid, the shares are treated as acquired at their vesting-date FMV. If you later sell at a higher price, the gain is taxed as capital gains at a flat 20.315% (15% national + 5% local inhabitant tax + 0.315% reconstruction surcharge). Any foreign exchange gain from currency movements is also included.

Stock Options: Qualified vs. Non-Qualified

The tax treatment of stock options in Japan depends entirely on whether they qualify under Japan’s special tax-exempt option rules (租税特別措置法). Almost all options granted by foreign parent companies do not qualify — here’s why that matters:

| Feature | Non-Qualified Stock Options (most expats) | Tax-Qualified Options (Japanese companies) |

|---|---|---|

| Taxable event #1 | At exercise: FMV – strike price taxed as salary income (up to 56%) | None at exercise (deferred) |

| Taxable event #2 | At sale: gain taxed at 20.315% | At sale: all gain taxed at 20.315% |

| Applies to foreign company grants? | ✅ Yes — almost always | ❌ Rarely (requires Japanese securities custody) |

⚠️ Why Foreign Company Options Rarely Qualify

To qualify for Japan’s tax-exempt treatment, shares must be custodied at a Japanese securities company. Options from GAFAM or other US multinationals are held at brokers like Morgan Stanley, E*TRADE, or Charles Schwab — so they cannot meet this requirement. You will almost certainly be taxed at exercise.

Multi-Country Proration: Japan Only Taxes the Japan Portion

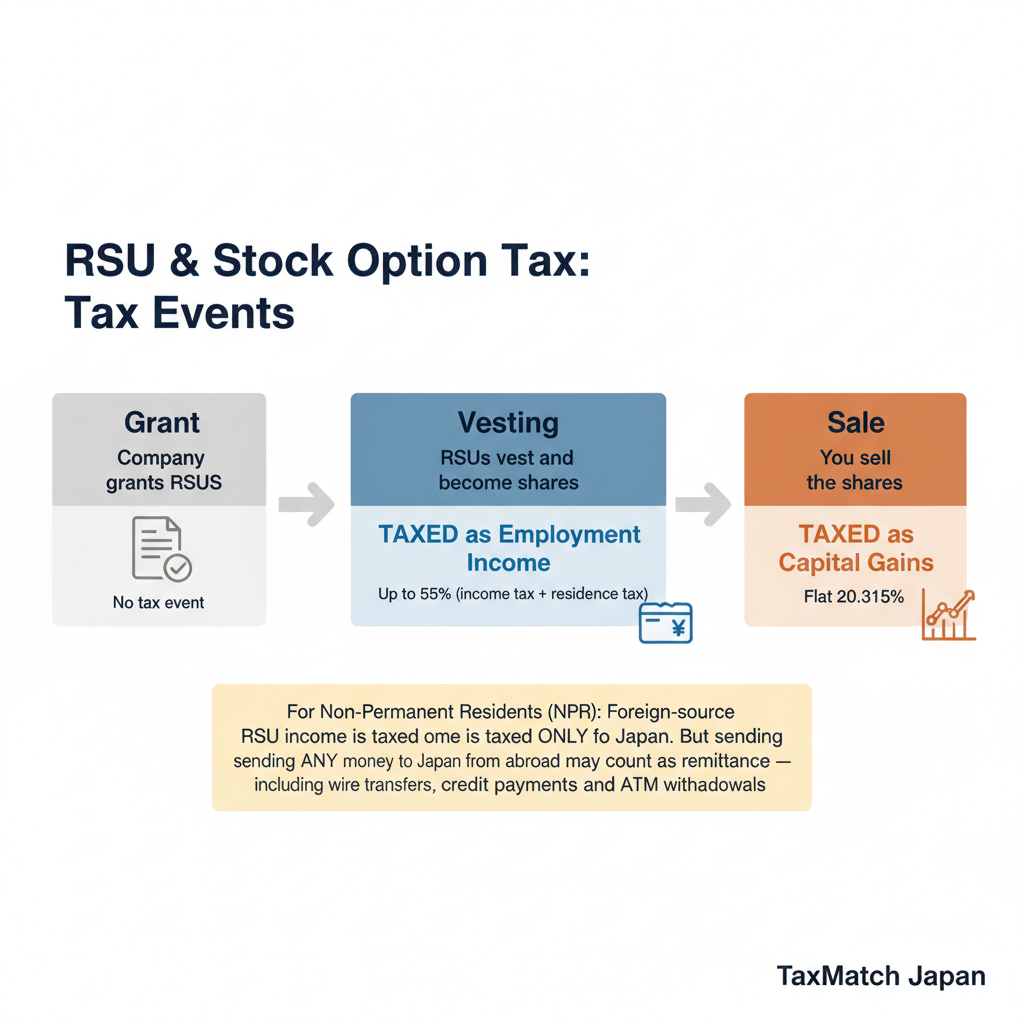

If your RSU grant spanned employment in multiple countries, Japan taxes only the portion earned while you were physically working in Japan. This is called time-basis source allocation (按分計算).

The Proration Formula

Under Income Tax Act Article 161, the Japan-source portion of your RSU income is calculated as:

Japan-Source RSU Income = Total Vesting Value × (Days Worked in Japan During Vesting Period ÷ Total Vesting Period Days)

Example: A ¥10M RSU grant vests after 4 years (1,460 days). You spent the first 3 years in the US, then the last 1 year in Japan. Japan taxes: ¥10M × (365 ÷ 1,460) = ¥2.5M. The remaining ¥7.5M is foreign-source income.

What happens to that ¥7.5M foreign-source portion depends entirely on your residency status in Japan.

Real-World Scenario: Tech Worker with RSUs in Japan

Profile: Raj (not his real name) is an Indian national on a Highly Skilled Professional (HSP) visa. He transferred internally from his US-based employer’s headquarters to their Tokyo office 2 years ago. His compensation includes a base salary paid by the Japanese subsidiary, plus RSU grants from the US parent company that vest quarterly.

The situation: Raj’s RSU grant was ¥12M total over 4 years. He spent 2 years in the US before transferring. His first vesting event in Japan was ¥3M worth of shares.

How it works:

- Japan-source portion: ¥3M × (days in Japan during vesting period ÷ total vesting days). Since only half the vesting period was spent in Japan → approximately ¥1.5M is Japan-source income

- Foreign-source portion: The remaining ¥1.5M was earned while working in the US

- NPR advantage: Since Raj has been in Japan for only 2 years, he qualifies as a Non-Permanent Resident. The ¥1.5M foreign-source portion is not taxed in Japan — as long as he doesn’t remit it

- The trap Raj almost fell into: He regularly used his US credit card for daily purchases in Tokyo. This would have counted as “remittance” and triggered tax on his foreign-source RSU income. After consulting a specialist, he switched to using only his Japanese bank account for Japan-based spending

Tax savings: By properly structuring his remittances, Raj saved approximately ¥450,000 in Japanese income tax on his first year’s vesting alone. Over his full NPR window (5 years), the cumulative savings could reach ¥2–3M.

In a similar situation with RSUs from a foreign employer? Get matched with a bilingual specialist who handles multi-country equity compensation.

Get Expert Help Free →The Non-Permanent Resident Strategy

This is the most powerful — and most frequently misunderstood — tax planning tool available to foreign expats in Japan.

Who is a Non-Permanent Resident (NPR)?

If you are a non-Japanese national who has lived in Japan for 5 years or less within the preceding 10 years, you are classified as a Non-Permanent Resident. NPRs pay Japanese tax only on:

- Japanese-source income (regardless of where it’s paid)

- Foreign-source income that is paid in Japan or remitted to Japan

This means that the ¥7.5M foreign-source RSU income from the example above can be completely tax-free in Japan — as long as it stays in your overseas account and you don’t remit it.

The Remittance Trap — The Rule That Catches Everyone

⚠️ Critical Warning: “Remittance” Is Broader Than You Think

Japan’s remittance rules treat the following all as “remittance from overseas” in the year foreign-source income is earned:

- Wire transfers from a foreign account to a Japanese account

- Using a foreign credit or debit card to pay for groceries, restaurants, or anything in Japan

- Withdrawing cash from a Japanese ATM using your foreign bank card

If you earn ¥7.5M in foreign-source RSU income and send ¥2M to Japan for rent that year, the NTA will tax ¥2M of that income — even if you didn’t intend to “use” the RSU money.

| Scenario | Foreign-Source RSU Income | Remittances to Japan | Amount Taxed in Japan |

|---|---|---|---|

| Low remittance | ¥10M | ¥2M | ¥2M |

| Full remittance | ¥5M | ¥5M | ¥5M |

| Income exceeds remittance | ¥3M | ¥10M | ¥3M |

| No foreign-source income | ¥0 | ¥10M | ¥0 |

Double Taxation: How Tax Treaties Help

US Citizens and Green Card Holders

The US taxes citizens on worldwide income. When your RSU vests in Japan, Japan takes first priority (primary taxing right on the Japan-source portion). You then claim a Foreign Tax Credit (Form 1116) on your US return to offset the Japanese tax paid. This generally brings your US liability to zero — but only for the Japan-source portion.

The Stock Option Timing Mismatch (Critical for US Taxpayers)

For stock options, Japan taxes at exercise while the US typically tracks the vesting date for proration. This mismatch can create situations where you pay US tax at vesting and Japanese tax at exercise years later — making FTC timing extremely complex. Document everything meticulously.

UK and Indian Nationals

Both the UK and India operate similar proration frameworks under their respective treaties with Japan. India additionally requires filing Form 67 before the Indian ITR deadline to claim FTC for Japanese taxes paid — failure to meet this deadline results in permanent loss of the credit.

RSU Income: How multi-country proration works

Navigating RSU taxation across two countries?

TaxMatch Japan connects you with bilingual tax specialists experienced in multi-country equity compensation — free to use. Get matched now → or reach us on WhatsApp

Filing Requirements (Kakutei Shinkoku)

When Do You Need to File?

If your RSUs are granted directly by a foreign parent company, your Japanese employer typically cannot withhold tax on the vesting income — they don’t control the shares. This means you must file your own final tax return (確定申告) if:

- You have RSU or stock option income (almost always, this triggers a filing obligation)

- You sold shares and realized capital gains exceeding ¥200,000

- You want to claim a foreign tax credit

The NTA Already Knows

Many expats think they can “fly under the radar” with foreign equity income. They cannot. Since 2012, Japanese subsidiaries of foreign companies are legally required to file annual reports (法定調書) with the NTA detailing RSU grants and vestings for all Japan-based employees. The NTA cross-references these reports against individual tax returns.

Overseas Asset Reporting (国外財産調書)

If you have lived in Japan for more than 5 years (Permanent Resident for tax purposes), you must file an annual Overseas Asset Statement by June 30 if your foreign assets (including vested shares held in overseas accounts) exceed ¥50 million as of December 31. Penalties for non-disclosure are severe, including criminal sanctions.

5 Common Mistakes with RSU Taxes in Japan

Mistake 1: Thinking Tax Applies When You Sell, Not When You Vest

RSUs create a tax event at vesting. Period. Many expats wait until they sell and then face unexpected penalties of 15–20% for underpayment plus interest (延滞税) at up to 9% per year.

Mistake 2: Using Foreign Credit Cards in Japan (Remittance Trap)

NPRs who use their US Amex at Tokyo restaurants are unknowingly “remitting” foreign-source income to Japan, triggering taxation on their foreign RSU income. Track every overseas card transaction in years when you receive foreign-source RSU income.

Mistake 3: Phantom Income from Pre-IPO RSUs

If RSUs vest at a private (unlisted) company based on an internal valuation, you owe Japanese income tax on that internal FMV — in cash — even though you cannot sell the shares. This creates a severe liquidity crisis. Use “sell-to-cover” settings whenever possible.

Mistake 4: Missing the FTC Due to Timing Mismatches

If the timing window for claiming a foreign tax credit expires (Japan allows a 3-year window), you permanently lose the credit. File promptly and work with advisors who understand both Japanese and your home country’s tax calendars.

Mistake 5: Forgetting Foreign Exchange Gains

When you sell foreign-currency shares, the foreign exchange movement between the acquisition date and sale date creates taxable income. If USD/JPY moved from 100 to 150 during your holding period, even a “flat” stock price in USD represents a 50% gain in JPY — taxable as miscellaneous income (雑所得).

Smart Tax Planning for NPRs

Accelerate Vesting Before Your 5-Year Mark

If you have grants that will vest after you cross 5 years in Japan (moving from NPR to Permanent Resident for tax purposes), consider whether it’s possible to request accelerated vesting before that date. Foreign-source income on pre-5-year grants can potentially be sheltered from Japanese tax if managed carefully.

Use Furusato Nozei to Your Advantage

A large RSU vesting event dramatically increases your annual income, which in turn increases your Furusato Nozei (hometown tax donation) deduction capacity. By maxing out this deduction in the same year as a large vest, you can receive significant tax benefits — effectively getting substantial goods in return for hometown tax donations with only ¥2,000 out-of-pocket cost.

Sell-to-Cover: Protect Against Phantom Income

Configure your equity plan to automatically sell enough shares on vesting to cover your Japanese income tax liability. This prevents the nightmare scenario of a stock price dropping between vesting and when you have enough cash to pay taxes.

2025 Tax Reform Impacts

The FY2025 tax reform (effective 2026 filing year) increases the basic deduction and minimum employment income deduction, slightly reducing the burden for all taxpayers. More significantly, a minimum tax on ultra-high incomes was introduced: for individuals with income exceeding ¥330 million, a 22.5% minimum rate applies to the excess, which can impact executives with large RSU vestings that previously benefited entirely from the lower capital gains rate on share sales.

📝 Summary: RSU & Stock Option Taxes in Japan

- RSUs are taxed as salary income at vesting — not at sale

- Non-Permanent Residents (under 5 years) can shelter foreign-source RSU income — but only if not remitted to Japan

- Multi-country grants require proration — Japan taxes only the Japan-earned portion

- Foreign company options are almost always non-qualified — exercise triggers salary-rate tax

- The NTA receives reports from your employer’s Japan subsidiary — don’t assume non-disclosure is safe

- File a final tax return (確定申告) by March 15 for any year with RSU vesting or option exercise

Ready to get your RSU taxes right?

TaxMatch Japan connects you with licensed zeirishi experienced in multi-country equity compensation — completely free.

Or reach us directly on WhatsApp

This article is for informational purposes only and does not constitute tax advice. Tax rules are complex and depend on individual circumstances. Consult a qualified licensed tax accountant (zeirishi) for personalized guidance.

Frequently Asked Questions

How are RSUs taxed in Japan?

RSUs are taxed as employment income at the time of vesting in Japan. The taxable amount is the fair market value of the shares on the vesting date. This is subject to progressive income tax rates of 5-45% plus 2.1% reconstruction surtax and 10% residence tax.

Do I pay tax on RSU vesting in Japan?

Yes. When RSUs vest, the fair market value of the shares is treated as employment income and taxed accordingly. If you later sell the shares at a gain, you also pay a separate 20.315% capital gains tax on the appreciation after vesting.

How do I avoid double taxation on RSUs in Japan?

If your RSUs were partially earned while working outside Japan, you may be able to apportion the income based on the ratio of days worked in Japan vs. abroad during the vesting period. Tax treaties between Japan and your home country may also provide relief through foreign tax credits.