Side Job Tax Rules in Japan for Foreigners: Complete Guide (2026)

If you’re working in Japan and thinking about picking up a side gig — freelancing, teaching English on weekends, selling on Mercari, or doing remote work for an overseas client — the money part is only half the equation. You also need to understand the tax rules. And for foreigners, there’s an extra layer: visa restrictions. Get this wrong and you could owe back taxes, face penalties, or in the worst case, jeopardize your visa status. Get it right and you’ll keep more of what you earn.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax rules and rates may change. Always consult a qualified tax professional (zeirishi) for advice specific to your situation.

Need a bilingual tax accountant? Get matched with a specialist — free.

Table of Contents

- Visa First: Can You Legally Do a Side Job?

- The 200,000 Yen Rule: What It Really Means

- Income Classification: Why It Matters

- Blue Tax Return (青色申告): The Biggest Tax Advantage

- Expense Deductions: What You Can Write Off

- Filing Your Tax Return

- Social Insurance: Does Your Side Job Affect It?

- Common Mistakes (And How to Avoid Them)

- When to Hire a Tax Accountant

- Frequently Asked Questions

The ¥200,000 Rule: Two different tax treatments

1. Visa First: Can You Legally Do a Side Job?

Before we talk taxes, let’s talk legality. Your visa type determines whether you can do side work at all.

Most work visas in Japan (Engineer/Specialist in Humanities/International Services, Instructor, etc.) only permit you to work for the employer listed on your visa application. To do any work outside that, you need permission.

Permission to Engage in Activity Other Than That Permitted (資格外活動許可)

There are two types:

| Type | Who It’s For | What It Allows |

|---|---|---|

| Blanket permission (包括許可) | Students, dependents | Part-time work up to 28 hours/week (40 hrs during school breaks) |

| Individual permission (個別許可) | Work visa holders | Specific side activities approved case-by-case |

If you’re on a work visa and want to freelance, teach privately, or do contract work on the side, you need to apply for individual permission at your regional immigration bureau. The application is free and typically takes 2-4 weeks.

Spouse visa (配偶者ビザ) and permanent residency holders have no work restrictions — you can do whatever you want.

The Consequences of Working Without Permission

Warning

This is not something to take lightly:

- Current penalties: Up to 3 years in prison and/or a fine of up to 3,000,000 yen

- From June 2025: Penalties increase to up to 5 years in prison and/or 5,000,000 yen in fines

- Your visa can be revoked and you may face deportation

Even if you’re “just” tutoring a few students for cash, doing it without proper authorization is illegal. Get the permission first.

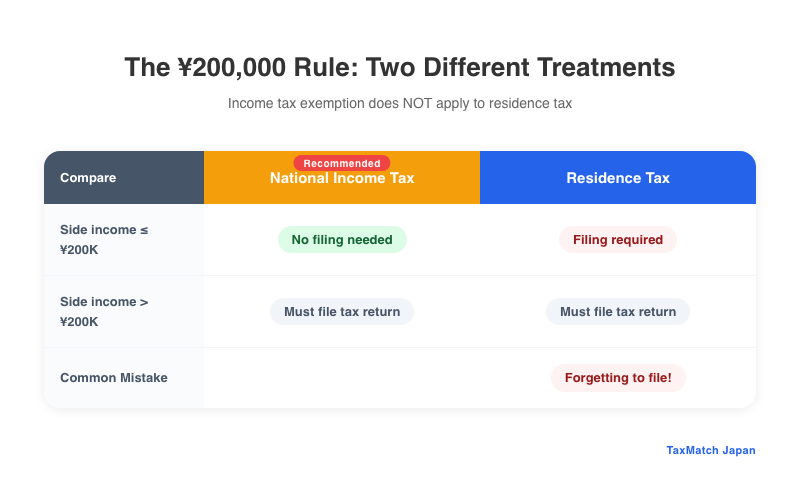

2. The 200,000 Yen Rule: What It Really Means

You’ve probably heard this one: “If your side income is under 200,000 yen, you don’t need to file taxes.” This is half true and half dangerous.

Here’s what the rule actually says:

If you are a salaried employee whose employer handles year-end adjustment (年末調整), and your other income is 200,000 yen or less, you are exempt from filing a national income tax return (確定申告).

The critical details:

- It’s 200,000 yen of INCOME, not revenue. Income means revenue minus expenses. If you earned 500,000 yen freelancing but had 350,000 yen in legitimate expenses, your income is 150,000 yen — under the threshold.

- This only applies to national income tax. It does NOT apply to residence tax.

- Residence tax has NO exemption threshold. Even if your side income is 1 yen, you are technically required to file a residence tax return (住民税の申告) with your municipal office.

Example

| Amount | |

|---|---|

| Freelance revenue | 480,000 yen |

| Expenses (laptop, software, internet) | -300,000 yen |

| Side income | 180,000 yen |

| Need to file income tax return? | No (under 200,000 yen) |

| Need to file residence tax return? | Yes (any amount) |

Warning

This is the most common mistake foreigners make. They hear “200,000 yen rule,” skip all filing, and then get hit with a residence tax bill plus penalties a year later. More on this in the mistakes section.

3. Income Classification: Why It Matters

How your side income is classified determines what deductions you can take and how much tax you’ll pay. The two main categories for side work are:

Miscellaneous Income (雑所得)

This is the default classification for most side gigs. If you’re doing occasional freelance work, selling items online, or earning affiliate income, it’s probably 雑所得.

- Pros: Simple reporting, minimal bookkeeping

- Cons: Cannot use the Blue Tax Return (no special deductions), losses cannot offset your salary income

Business Income (事業所得)

If your side work is substantial and ongoing, it may qualify as business income. This opens the door to much better tax treatment.

To qualify as business income, you generally need:

- Annual revenue exceeding 3,000,000 yen (this is a key threshold the tax office uses)

- Proper bookkeeping — organized records of income and expenses

- Continuity and regularity — not a one-off gig but an ongoing business activity

- Profit-making intent — you’re trying to run a real business, not just a hobby

| Factor | Miscellaneous Income (雑所得) | Business Income (事業所得) |

|---|---|---|

| Typical revenue | Under ~3,000,000 yen/year | Over ~3,000,000 yen/year |

| Blue Tax Return eligible | No | Yes |

| Loss offset against salary | No | Yes |

| Bookkeeping required | Basic records | Double-entry (for full deduction) |

| Special deductions available | No | Up to 650,000 yen |

Why this matters: If you earn 2,000,000 yen from a side business and classify it as business income with a Blue Tax Return, you could save roughly 200,000+ yen in taxes compared to reporting it as miscellaneous income. That’s real money.

Section Summary

- Most casual side gigs are classified as miscellaneous income (雑所得)

- Substantial, ongoing side businesses can qualify as business income (事業所得) — unlocking the Blue Tax Return

- The classification difference can save you 200,000+ yen per year in taxes

4. Blue Tax Return (青色申告): The Biggest Tax Advantage

If your side income qualifies as business income, the Blue Tax Return (青色申告) is the single most powerful tax-saving tool available to you. For a comprehensive overview, see our freelancer and self-employed tax guide.

The Three Tiers

| Deduction | Requirement |

|---|---|

| 100,000 yen | Simple bookkeeping (single-entry) |

| 550,000 yen | Double-entry bookkeeping, paper filing |

| 650,000 yen | Double-entry bookkeeping + e-Tax filing (or electronic record keeping) |

The 650,000 yen deduction means that amount is subtracted from your taxable income before calculating taxes. At a combined income tax + residence tax rate of ~30%, that’s roughly 195,000 yen in annual tax savings.

How to Apply

You must submit the Blue Tax Return Application (青色申告承認申請書) to your tax office:

- New business: Within 2 months of starting your business

- Existing business switching from white to blue: By March 15 of the year you want to start using it

Example timeline: If you start freelancing in April 2026, you must submit the application by June 2026. If you want to use Blue Tax Return for the 2027 tax year, submit by March 15, 2027.

You also need to submit a Business Opening Notification (開業届) — this is a one-page form available at any tax office or via e-Tax.

Other Blue Tax Return Benefits

Beyond the income deduction:

- Loss carryforward: If your side business has a loss, you can carry it forward for up to 3 years and offset future profits

- Loss offset: Losses from your side business can offset your salary income, potentially reducing your overall tax bill

- Family employee salaries: If your spouse or family members help with the business, their salaries become deductible expenses (with proper documentation)

5. Expense Deductions: What You Can Write Off

Whether you report as miscellaneous income or business income, you can deduct legitimate business expenses. This directly reduces your taxable income.

Common Deductible Expenses for Side Workers

| Expense | Examples | Notes |

|---|---|---|

| Equipment | Laptop, camera, phone | Items over 100,000 yen must be depreciated over multiple years |

| Software & subscriptions | Adobe, Zoom, cloud storage | Fully deductible if used for business |

| Communication | Internet, mobile phone | Apply home office ratio (see below) |

| Transportation | Train fare, gas for client visits | Keep receipts or IC card records |

| Office supplies | Pens, notebooks, printer ink | Fully deductible |

| Professional development | Books, courses, seminars | Must relate to your business |

| Rent | Home office portion | Apply home office ratio |

| Utilities | Electricity | Apply home office ratio |

| Outsourcing | Subcontractor fees, design work | Keep invoices |

| Marketing | Website hosting, ads | Fully deductible |

Home Office Ratio (家事按分)

If you work from home, you can deduct a portion of your rent, internet, and electricity as business expenses. The key is the home office ratio (家事按分) — the percentage of your home used for business.

How to calculate it:

- By space: If your apartment is 50 sqm and your workspace is 10 sqm, your ratio is 20%

- By time: If you use your internet 4 hours/day for business out of 12 hours total usage, your ratio is 33%

Typical acceptable ranges:

| Ratio | Tax Office View |

|---|---|

| 10-30% | Generally accepted without question |

| 30-50% | May be questioned; have documentation ready |

| Over 50% | Raises red flags — you’ll need strong justification |

Example: Your rent is 120,000 yen/month and you use 25% of your apartment for your side business. Monthly deduction: 30,000 yen. Annual deduction: 360,000 yen. At a ~30% tax rate, that’s 108,000 yen in tax savings per year.

Keep records. Take a photo of your workspace, note the dimensions, and keep a simple log of your work hours. The tax office rarely audits small side businesses, but if they do, documentation is your best friend.

Not sure which expenses you can deduct? A bilingual tax specialist can help maximize your deductions. Get matched free →

6. Filing Your Tax Return

When to File

The tax filing period for the previous year’s income is February 16 to March 15 each year. For example, income earned in 2026 is reported between February 16 and March 15, 2027. See our step-by-step filing guide for the full process.

If you owe additional tax and file late, you’ll face:

- Late filing penalty (無申告加算税): 15-20% of the tax owed

- Late payment interest (延滞税): ~2.4% for the first 2 months, then ~8.7% annually

How to File

Option 1: e-Tax (recommended)

Japan’s online filing system. You’ll need a My Number card and a card reader (or a smartphone with NFC). Filing via e-Tax is one of the requirements for the full 650,000 yen Blue Tax Return deduction.

Option 2: Paper filing

Pick up forms at your local tax office, fill them out, and submit in person or by mail.

Option 3: Visit the tax office

During filing season, tax offices set up help desks. Lines can be very long, but staff will walk you through the process. Some offices have English support, but don’t count on it.

The Privacy Trick: Choosing 普通徴収

Here’s something many foreigners don’t know: if you don’t want your employer to find out about your side income, there’s a specific box to check on your tax return.

When you file, there’s a section about how to pay residence tax on your side income. You have two options:

- 特別徴収 (Special Collection): Added to your payroll deduction. Your employer sees a higher residence tax amount and may figure out you have side income.

- 普通徴収 (Ordinary Collection): You receive a separate bill at home and pay it yourself. Your employer sees no change.

Check the box for 普通徴収 (ordinary collection) on your tax return. It’s in the “住民税に関する事項” section. This keeps your side income residence tax separate from your employer.

Note: Not all municipalities honor this request perfectly, but most do. If privacy is critical, confirm with your city office that they support separate collection.

7. Social Insurance: Does Your Side Job Affect It?

This depends on your employment status:

If You’re a Company Employee (会社員)

Your social insurance (shakai hoken) is NOT affected by side income. Shakai hoken premiums are calculated based on your salary from your employer only. Freelance income, rental income, and other side earnings are not included in the calculation.

This is good news — your side hustle won’t increase your health insurance or pension premiums.

Exception: If you have a second employment relationship (i.e., you’re on the payroll of two companies), both employers must enroll you in shakai hoken if you meet the eligibility requirements at both. This is rare for side gigs.

If You’re Self-Employed (National Health Insurance)

If you’re on National Health Insurance (国民健康保険 / NHI), your premiums ARE based on your total income, including side income. More income means higher NHI premiums.

For NHI subscribers, side income of 1,000,000 yen could increase your annual premiums by roughly 100,000 yen depending on your municipality’s rate.

Section Summary

- Company employees (shakai hoken): side income does NOT affect premiums

- Self-employed (NHI): side income DOES increase premiums

- Choose 普通徴収 on your tax return to keep side income private from your employer

8. Common Mistakes (And How to Avoid Them)

Mistake 1: Not Filing Residence Tax

The problem: You earn 150,000 yen from a side gig, hear about the “200,000 yen rule,” and file nothing.

What happens: You skipped the income tax return (which is fine), but you also skipped the residence tax return (which is NOT fine). Your municipality doesn’t know about this income, so they calculate your residence tax too low. When they eventually find out — and they usually do — you’ll owe back taxes plus penalties.

The fix: If your side income is under 200,000 yen and you don’t file an income tax return, go to your municipal office and file a residence tax return (住民税の申告). It’s a simple form.

Even easier fix: Just file a regular income tax return via e-Tax for everything. It covers both income tax and residence tax in one shot, and you might even get a small refund.

Mistake 2: Working Without Visa Permission

The problem: You start tutoring on the side without applying for 資格外活動許可, thinking “nobody checks.”

What happens: Immigration does check, especially during visa renewals. Your side income shows up on your tax records, which are cross-referenced with your visa status. Even if you’ve been paying taxes perfectly, working without permission is a separate immigration violation.

The fix: Apply for permission BEFORE you start any side work. It’s free and straightforward.

Mistake 3: Mixing Personal and Business Expenses

The problem: You use one bank account and one credit card for both personal spending and business expenses.

What happens: At tax time, you can’t clearly separate what’s deductible and what’s not. You either miss legitimate deductions (costing you money) or accidentally claim personal expenses (risking an audit).

The fix: Open a separate bank account for your side business. Use a dedicated credit card or payment method for business purchases. This makes bookkeeping dramatically easier.

Mistake 4: Claiming an Unreasonable Home Office Ratio

The problem: You work from a corner of your living room but claim 60% of your rent as a business expense.

What happens: If audited, the tax office will reject the deduction and you’ll owe back taxes plus penalties. A 60% ratio for someone with a primary employer doing side work on evenings and weekends is simply not credible.

The fix: Be honest and conservative. For most side workers, 10-25% is a defensible range. Document your workspace and hours.

Mistake 5: Forgetting to Apply for Blue Tax Return in Advance

The problem: You’ve been freelancing all year and want the 650,000 yen deduction, but you never filed the application.

What happens: You can’t use the Blue Tax Return retroactively. The application must be submitted by March 15 of the year you want to use it (or within 2 months of starting a new business).

The fix: If you’re planning to start a side business, file the opening notification (開業届) and Blue Tax Return application at the same time. They’re both one-page forms.

9. When to Hire a Tax Accountant

For simple side gigs earning under 500,000 yen, you can probably handle the filing yourself with free tools like the NTA’s online filing system.

But consider hiring a tax accountant (税理士) if:

- Your side income exceeds 1,000,000 yen and you want to maximize deductions

- You’re deciding between 雑所得 and 事業所得 and want professional guidance on classification

- You have income from multiple countries (e.g., remote work for an overseas client) and need help with foreign tax credits

- You’re setting up a Blue Tax Return for the first time and want to make sure your bookkeeping is correct

- You’ve received a notice from the tax office and aren’t sure how to respond

- You want to incorporate your side business into a company (合同会社 or 株式会社)

A bilingual tax accountant who understands both Japanese tax law and the unique situations foreigners face can easily save you more than their fee in avoided mistakes and optimized deductions. See our pricing guide for typical fee ranges.

Need help with your side job taxes? Get matched with an English-speaking tax accountant who understands freelance and side business tax rules — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

Are side jobs taxed in Japan?

Yes, all income from side jobs is subject to Japanese income tax. If your side income exceeds ¥200,000 per year and your main employer handles year-end adjustment, you must file your own tax return (kakutei shinkoku).

Do I need to file a tax return for side income in Japan?

You must file a tax return if your side income exceeds ¥200,000 per year and your main employment income is covered by year-end adjustment. Below ¥200,000, you may be exempt from filing for income tax purposes, but you still need to report it for residence tax.

What is the ¥200,000 side income exemption?

If your total side income (miscellaneous income, business income, etc.) is ¥200,000 or less per year and your main employment income is handled through year-end adjustment, you are exempt from filing an income tax return. However, this exemption does not apply to residence tax — you must still report side income to your municipality.