Sole Proprietor vs. Corporation in Japan: Tax Comparison for Foreign Residents | TaxMatch Japan

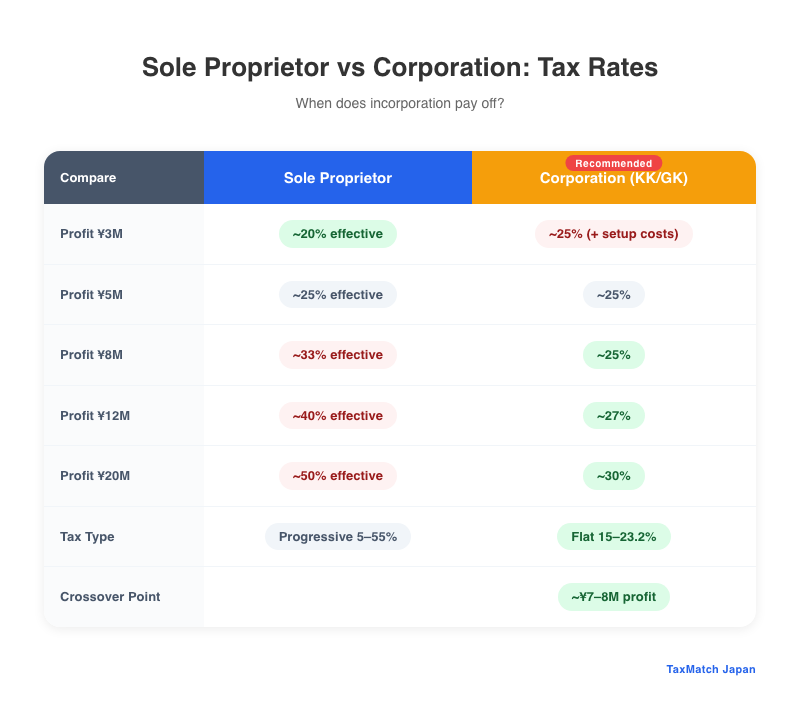

Sole Proprietor vs Corporation: Tax rate comparison by profit level

At some income level, incorporating your business in Japan saves significant tax. But the crossover point is not where most people think — and for foreigners, visa implications add a critical layer that changes everything.

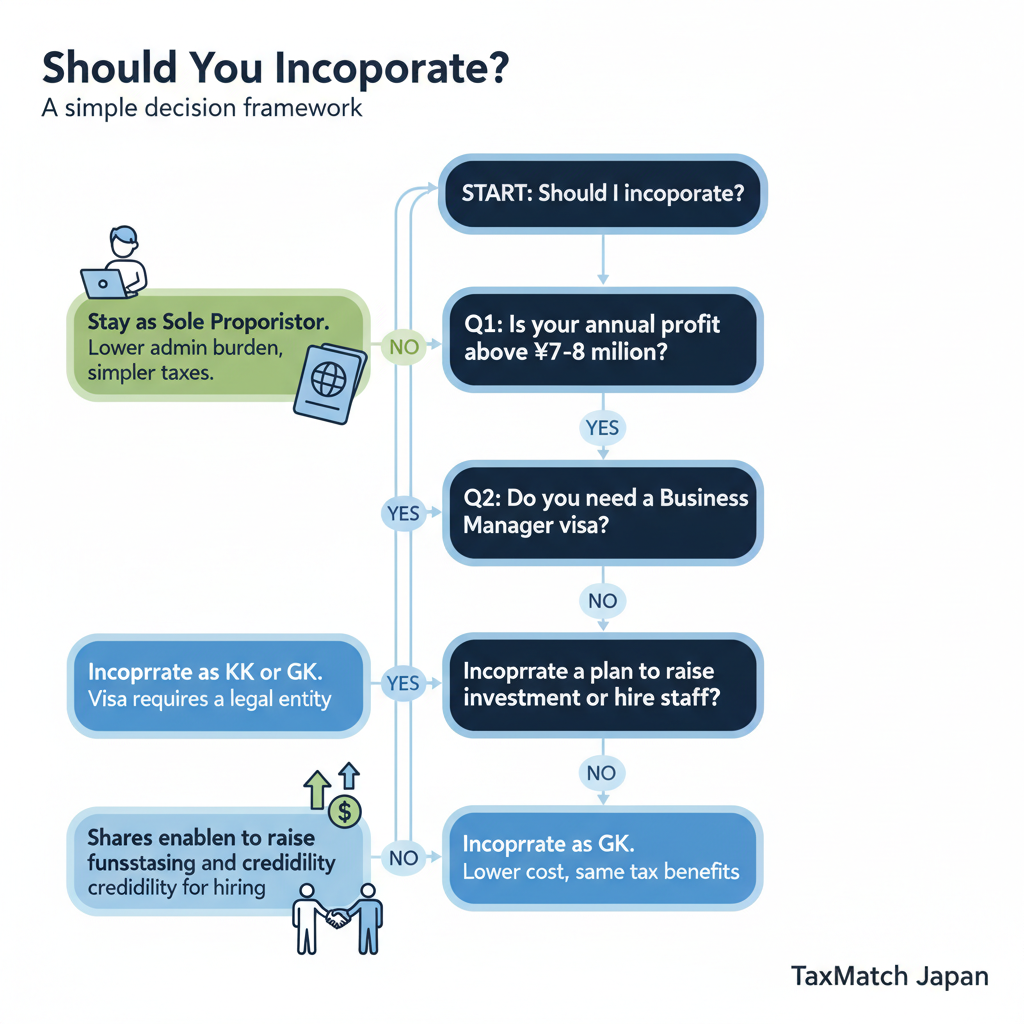

Should You Incorporate? A simple decision framework

Freelancing or building a business in Japan? Get matched with a bilingual tax specialist who works with foreign entrepreneurs — free.

Get Matched Free →The decision between operating as a sole proprietor (個人事業主) and incorporating as a Kabushiki Kaisha (KK) or Godo Kaisha (GK) is one of the most consequential choices a self-employed person in Japan makes. For Japanese nationals, the primary consideration is tax efficiency. For foreigners, there is an additional critical dimension: your visa status depends directly on how your business is structured.

Individual Tax Rates: The Starting Point

As a sole proprietor, your business profit is treated as personal income and taxed at Japan’s progressive individual rates:

| Taxable Income | National Tax Rate | Local Tax | Combined Effective Rate |

|---|---|---|---|

| Up to ¥1,950,000 | 5% | 10% | ~15% |

| ¥1,950,001 – ¥3,300,000 | 10% | 10% | ~20% |

| ¥3,300,001 – ¥6,950,000 | 20% | 10% | ~30% |

| ¥6,950,001 – ¥9,000,000 | 23% | 10% | ~33% |

| ¥9,000,001 – ¥18,000,000 | 33% | 10% | ~43% |

| ¥18,000,001 – ¥40,000,000 | 40% | 10% | ~50% |

| Over ¥40,000,000 | 45% | 10% | ~55% |

Note: A 2.1% reconstruction surtax applies to national income tax amounts, raising effective rates slightly above those shown above.

Blue Form Tax Return: The Sole Proprietor’s Best Friend

Sole proprietors who maintain proper bookkeeping can file under the 青色申告 (Blue Form / Aoiro Shinkoku) system, unlocking significant benefits:

- ¥650,000 special deduction (or ¥550,000 if you don’t file electronically) — a direct reduction from taxable income, not just a deduction at the marginal rate

- Business loss carryforward for up to 3 years — if you have a loss year, it offsets future profits

- Spousal wage deduction — pay your spouse a salary (up to market rate) as a legitimate business expense

- Accelerated depreciation for business assets up to ¥300,000

📌 Blue Form Application: Apply Immediately Upon Starting Business

To qualify for Blue Form tax benefits, you must file an application (青色申告承認申請書) with the NTA within 2 months of starting your business (or by March 15 for existing businesses). Many new entrepreneurs miss this deadline and wait a full year to access Blue Form benefits. Apply on day one.

Social Insurance as a Sole Proprietor

National Health Insurance (国民健康保険)

Sole proprietors pay NHI, which is income-based and varies by municipality. At ¥10M income, NHI premiums can reach ¥800,000–¥1,000,000 per year. NHI premiums are tax-deductible but the premium burden is significant for higher earners.

National Pension (国民年金)

Sole proprietors pay the fixed national pension premium: approximately ¥16,980/month (2024 rate) for both the proprietor and any household member enrolled. This is fully deductible from income.

The NHI Cap Advantage

NHI premiums are capped at roughly ¥1,040,000 per year (2024, varies by municipality). Above the income level that generates the maximum NHI premium, additional sole proprietor income generates no additional social insurance cost. This changes the incorporation calculus for very high earners.

Corporate Tax Rates: Japan’s Two-Tier System

When you incorporate, your company’s profits are taxed at corporate tax rates — significantly lower than individual rates at higher income levels:

| Company Size / Profit Level | National Corporate Tax | Local Corporate Tax (Approx.) | Effective Combined Rate |

|---|---|---|---|

| SME: First ¥8,000,000 profit | 15% | ~8% | ~23% |

| SME: Above ¥8,000,000 | 23.2% | ~9% | ~32% |

| Large company (capital >¥100M) | 23.2% flat | ~9% | ~32% |

The critical insight: on the first ¥8 million of corporate profit, the effective rate is approximately 23%, versus a combined individual rate of 43-50% at that income level. The tax saving on ¥8M retained in the company versus distributed as personal income can exceed ¥2,000,000 per year.

The Social Insurance Trap in Corporations

⚠️ Every Corporation Must Enroll in Social Insurance — Even With One Employee

Unlike sole proprietors, corporations are mandatory participants in Japan’s shakai hoken (社会保険) — employee health insurance and employees’ pension (厚生年金). This applies to every kabushiki kaisha and godo kaisha, even if the only “employee” is the sole director and owner. There is no opt-out.

The combined employer + employee contribution is approximately 28-30% of the director’s salary. On a ¥6,000,000 director salary:

- Employee (director) contribution: ~¥840,000/year

- Company (employer) contribution: ~¥840,000/year

- Total social insurance cost: ~¥1,680,000/year

The Director Salary Rule: Rigidity with Tax Logic

When you pay yourself a salary as a corporate director, Japan tax law requires it to follow the 定期同額給与 (teiki dōgaku kyūyo) rule — a fixed, equal amount paid at regular intervals (monthly). You generally cannot change your salary during the fiscal year unless a significant event occurs. The key implications:

- Director salary changes must be made within 3 months of the company’s fiscal year start

- Irregular payments to directors may be denied as deductible expenses by the NTA

- Set your salary conservatively at the year’s start — you can retain profits in the company but cannot easily pull extra cash out as salary mid-year

- Bonuses to directors are not deductible unless pre-approved by shareholders before the fiscal year begins (事前確定届出給与)

The Breakeven Point: When Does Incorporation Pay?

The widely cited rule of thumb in Japan is that incorporation becomes tax-advantageous at annual profit of approximately ¥7-8 million. The exact breakeven depends on your specific deduction profile, marital status, and whether you count the value of enhanced social insurance benefits.

| Annual Profit | As Sole Proprietor (Net after tax + NHI) | As Corporation + Director Salary (Net) | Advantage |

|---|---|---|---|

| ¥3,000,000 | ~¥2,300,000 | ~¥2,100,000 (incorporation costs eat gains) | Sole proprietor wins |

| ¥5,000,000 | ~¥3,400,000 | ~¥3,400,000 | Roughly equal |

| ¥8,000,000 | ~¥4,800,000 | ~¥5,400,000 | Corporation: +¥600K |

| ¥12,000,000 | ~¥6,500,000 | ~¥7,800,000 | Corporation: +¥1.3M |

| ¥20,000,000 | ~¥9,500,000 | ~¥13,000,000 | Corporation: +¥3.5M |

Note: These are illustrative estimates for single individuals. Actual figures depend on applicable deductions, location, NHI premiums, and social insurance calculations. Consult a tax accountant for precise analysis of your situation.

KK vs. GK: Which Corporate Structure for Foreigners?

| Kabushiki Kaisha (KK / 株式会社) | Godo Kaisha (GK / 合同会社) | |

|---|---|---|

| Setup cost | ~¥200,000 (registration tax + notary fees) | ~¥60,000 (registration tax only) |

| Ongoing compliance | Annual shareholder meeting, minutes, corporate registers required | Simpler — member agreement governs most decisions |

| Credibility | Higher — recognized corporate form; easier for enterprise clients | Lower perceived prestige; some enterprise clients require KK |

| Business Manager Visa | Accepted | Accepted (same visa eligibility) |

| Capital requirement | ¥1 minimum (but ¥30M for new Business Manager Visa from Oct 2025) | ¥1 minimum (same new ¥30M rule for Business Manager Visa) |

| Best for | B2B businesses; planning to seek outside investment; larger operations | Small owner-operated businesses; cost-conscious solo operators |

Visa Implications: The Foreign Entrepreneur’s Unique Constraint

For foreigners in Japan, the incorporation decision is inseparable from the visa question. This is the aspect most Japanese-focused tax guides miss entirely.

Freelancing on an Employment Visa

Most foreigners in Japan hold work visas tied to their employer. Working as a freelancer while on an employment visa is generally prohibited without separate permission (資格外活動許可). The visa specifies permitted activities, and freelancing or operating a business outside those activities is a visa violation.

The Business Manager Visa Requirement

To legally operate your own incorporated business as the primary director/manager, you typically need a Business Manager Visa (経営管理ビザ). Under rules implemented in October 2025, key requirements include:

- ¥30 million in capital (raised from ¥5M; a dramatic increase)

- 1 full-time employee (or equivalent office/business scale)

- 3-year grace period for businesses established before October 2025 under old rules

- JLPT N2 or equivalent Japanese language proficiency for new applicants

⚠️ The ¥30M Capital Rule Changes the Calculus Entirely

For most small business owners and freelancers, meeting the new ¥30M capital requirement is not feasible. This has effectively made the Business Manager Visa inaccessible for new small business applicants from October 2025 onward. Alternatives being explored include the Startup Visa (スタートアップビザ) available in select municipalities and the Digital Nomad Visa for remote workers employed by foreign companies.

The Consumption Tax (消費税) Wildcard

Both sole proprietors and corporations must register for consumption tax (消費税) once annual revenue exceeds ¥10 million in any of the past 2 years. The standard rate is 10%. Until registration is required, you are an 免税事業者 (tax-exempt business) — you do not charge or remit consumption tax, which creates a competitive advantage at lower revenue levels.

However, Japan’s Invoice System (インボイス制度), introduced October 2023, has complicated this: to issue tax-creditable invoices (適格請求書) to business clients, you must be a registered consumption taxpayer. B2B businesses serving other registered businesses face pressure to register even below the ¥10M threshold — registration costs roughly 4-6% of revenue in additional tax burden.

Decision Framework: Which Structure Is Right for You?

| Situation | Recommended Structure | Reason |

|---|---|---|

| Annual profit below ¥5M; just starting out | Sole Proprietor + Blue Form | Lower compliance costs; easier to manage; tax difference minimal |

| Annual profit ¥7M+ and growing; expect to scale | KK (Kabushiki Kaisha) | Corporate tax rate advantage; credibility with enterprise clients; future investment readiness |

| Solo B2B service provider; ¥7M+ profit; cost-conscious | GK (Godo Kaisha) | Same tax benefits as KK at lower setup/compliance cost |

| Foreign national needing Business Manager Visa; <¥30M capital | Research Startup Visa or Digital Nomad Visa; consult immigration specialist | Standard Business Manager Visa requirements may not be achievable |

| Foreign national employed by overseas company; working remotely in Japan | Consult specialist; may be able to remain on existing visa status | Visa category determines legal work permission; tax status follows from residency |

📝 Key Decision Checklist

- What is my current annual profit? (Below ¥5M: stay sole proprietor; ¥7M+: consider incorporating)

- What visa do I hold, and does it permit self-employment or company operation?

- Do my business clients require invoices? (Invoice system may force consumption tax registration)

- Have I filed a Blue Form application to maximize sole proprietor tax benefits?

- If incorporating: have I modeled the social insurance cost (28-30% of director salary) into the tax comparison?

- What is the optimal director salary for my visa status and total tax optimization?

Running a business in Japan as a foreigner?

TaxMatch Japan connects you with tax specialists who understand both the tax optimization and visa compliance dimensions — completely free matching service.

Or reach us directly on LINE

This article is for informational purposes only and does not constitute tax or legal advice. Tax rules and visa requirements are complex, change regularly, and depend heavily on individual circumstances. Please consult a qualified licensed tax accountant (zeirishi) and immigration specialist for personalized guidance specific to your situation.

Frequently Asked Questions

Should I incorporate in Japan or stay sole proprietor?

Generally, incorporation becomes advantageous when your annual profit exceeds approximately ¥8-10 million, as the corporate tax rate (about 23-30%) becomes lower than the top marginal income tax rate for sole proprietors (up to 55% including residence tax).

What are the tax advantages of a corporation in Japan?

Key advantages include: a flat corporate tax rate (vs. progressive individual rates), the ability to pay yourself a salary (with an employment income deduction), greater expense deduction flexibility, retirement allowance benefits, and easier succession planning.

How much does it cost to set up a company in Japan?

A Kabushiki Kaisha (KK/stock company) costs approximately ¥200,000-250,000 in registration fees, while a Godo Kaisha (GK/LLC) costs approximately ¥60,000-100,000. Both require capital (minimum ¥1 for a GK, though ¥5 million+ is recommended for Business Manager Visa holders).