Other country guides: Indian Citizens Tax in Japan · Canadian · Australian

Are you a British citizen living in Japan? You must navigate two of the world’s most complex tax systems simultaneously. The UK’s Statutory Residence Test, Japan’s Non-Permanent Resident rules, pension lump sum traps, and the ISA problem can all cost you thousands if you get them wrong. Here’s the complete guide to UK-Japan dual tax obligations — from treaty rates to pension traps to the ISA surprise.

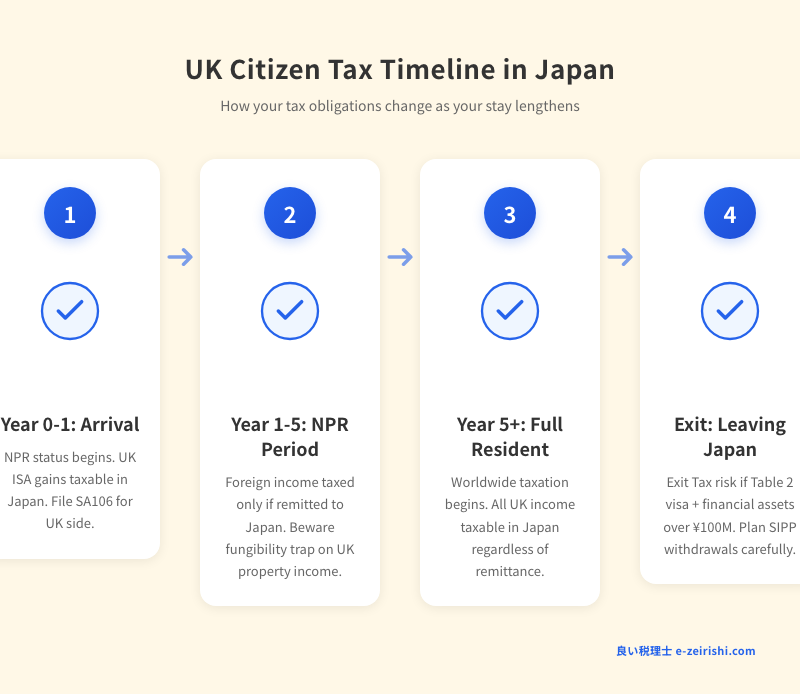

UK Tax Timeline: How obligations change with your stay length

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. UK-Japan cross-border taxation is highly complex and depends on your specific circumstances. Always consult qualified professionals — a Japanese tax accountant (zeirishi) and a UK chartered accountant — for advice on your particular situation.

British citizen looking for a bilingual tax accountant in Japan?

Get matched with a specialist — free.

British citizens form a significant community in Japan, working across finance, education, IT, and professional services. Unlike US citizens, the UK does not tax based on citizenship — but HMRC may still consider you UK tax resident under the Statutory Residence Test even while you live in Japan. Add Japan’s own residency-based worldwide taxation, pension cross-border pitfalls, and the fact that Japan does not recognize your ISA or SIPP, and you have a genuinely complex compliance landscape.

This guide covers every critical area: residency rules on both sides, treaty rates, pension traps, ISA taxation, property income, capital gains, exit tax, social security, and the practical mechanics of eliminating double taxation.

Quick Summary for UK Citizens in Japan

- UK does not tax by citizenship, but the SRT may still classify you as UK resident

- Japan’s Non-Permanent Resident (NPR) status shields foreign-source income for the first 5 years — unless remitted

- Treaty rates: dividends 0%/10%, interest 0%, royalties 0%

- Your ISA is NOT tax-free in Japan — all gains and dividends are taxable

- UK pension 25% tax-free lump sum is NOT recognized by Japan’s NTA

- UK-Japan social security agreement has NO totalization — protect your NI record

- Exit tax applies if you hold >¥100M in financial assets after 5+ years on a Table 2 visa

Table of Contents

- How UK-Japan Tax Residency Works

- UK-Japan Tax Treaty: What Income Is Taxed Where

- Employment Income & the 183-Day Rule

- UK Pensions in Japan: The 25% Lump Sum Trap

- ISA: Why Your Tax-Free Savings Aren’t Tax-Free in Japan

- UK Property Income & the Remittance Trap

- Capital Gains: Stocks vs Real Estate

- Exit Tax: The ¥100M Threat for Long-Term Residents

- Eliminating Double Taxation

- Social Security: The Missing Totalization Problem

- Non-Dom Abolition & Japan’s NPR: Comparison

- Frequently Asked Questions

1. How UK-Japan Tax Residency Works

Understanding your tax residency status in both countries is the foundation of everything else. The UK and Japan use fundamentally different tests, and it is possible to be considered resident in both — or neither — if you are not careful.

UK Side: The Statutory Residence Test (SRT)

Since April 2013, the UK has used the Statutory Residence Test to determine tax residency. It operates through a series of tests applied in order:

- Automatic overseas test: You are automatically non-resident if you were UK resident in none of the previous 3 tax years and spend fewer than 46 days in the UK, OR were resident in one or more of the previous 3 years and spend fewer than 16 days in the UK

- Automatic UK test: You are automatically UK resident if you spend 183+ days in the UK, or your only home is in the UK

- Sufficient ties test: If neither automatic test applies, the number of UK ties (family, accommodation, work, 90-day, country) combined with days spent determines your status

Key Point for Brits in Japan: Even if you live full-time in Japan, retaining a UK home, having a spouse in the UK, or spending more than a few weeks visiting can trigger UK residence under the sufficient ties test. Maintain a record of your UK days meticulously.

Japan Side: Resident, Non-Permanent Resident, Non-Resident

Japan classifies individuals into three categories based on domicile (jusho) and length of stay:

| Status | Criteria | Taxable Scope |

|---|---|---|

| Non-Resident | No domicile or residence in Japan | Japan-source income only |

| Non-Permanent Resident (NPR) | Domicile in Japan, no Japanese nationality, ≤5 years domicile in past 10 | Japan-source + foreign-source if remitted |

| Permanent Resident | Domicile in Japan, >5 years domicile in past 10 (or Japanese national) | Worldwide income |

For most British citizens arriving in Japan, the first 5 years offer significant protection: foreign-source income (UK rental income, UK dividends, UK capital gains on non-Japan assets) is only taxed if remitted to Japan. After crossing the 5-year threshold, Japan taxes your worldwide income regardless of remittance.

Dual Residence Tiebreaker

If you qualify as resident in both the UK and Japan simultaneously, the UK-Japan Tax Treaty provides tiebreaker rules (Article 4). The treaty looks at, in order: permanent home, centre of vital interests, habitual abode, and nationality. For most Brits living and working in Japan full-time, the treaty will assign residence to Japan.

2. UK-Japan Tax Treaty: What Income Is Taxed Where

The UK-Japan Tax Treaty (Convention for the Elimination of Double Taxation, as modified by the MLI) provides specific rules for each income type. Here are the key treaty rates:

| Income Type | Treaty Rate / Rule | Notes |

|---|---|---|

| Dividends (parent-subsidiary, 10%+ ownership) | 0% | Ownership held 6+ months |

| Dividends (portfolio / general) | 10% | Withholding in source country |

| Interest | 0% | Exception: profit-linked interest taxed at 10% |

| Royalties | 0% | Exempt from source-country withholding |

| Employment income | Residence country | Subject to 183-day rule exemption |

| Private pensions | Residence country only | Article 17 — UK cannot withhold |

| Government pensions | Source country only | Article 18 — unless recipient has Japanese nationality |

| Capital gains (stocks) | Residence country only | Movable property rule |

| Capital gains (real estate) | Country where property located | Both countries may tax |

For a detailed analysis of every treaty article, see our UK-Japan Tax Treaty Practical Guide.

3. Employment Income & the 183-Day Rule

If you are employed in Japan by a Japanese company, your salary is taxed in Japan under normal rules. The treaty’s 183-day rule becomes relevant if you are sent to Japan temporarily by a UK employer or work in both countries.

The Three Conditions for Exemption

Under the UK-Japan treaty, employment income may be exempt from tax in the host country if all three of the following conditions are met:

- The employee is present in the host country for no more than 183 days in any rolling 12-month period (note: this is a rolling period, not a calendar year)

- The remuneration is paid by, or on behalf of, an employer who is not a resident of the host country

- The remuneration is not borne by a permanent establishment or fixed base of the employer in the host country

Warning: Rolling 12-Month Period

Unlike treaties with some other countries, the UK-Japan treaty uses a rolling 12-month period, not the calendar year or fiscal year. This means HMRC and the NTA can look at any consecutive 12-month window to determine whether you exceed 183 days. A common trap: spending 100 days in Japan from September to December of one year and 100 days from January to April of the next year — within the calendar year limit, but exceeding 183 days in a rolling 12-month window.

Practical Implications

If you fail any single condition, the host country can tax your employment income. For a UK employee seconded to Japan, this typically means:

- If you stay in Japan >183 days in any 12-month window: Japan taxes your salary

- If a Japanese subsidiary bears the cost of your salary: Japan taxes your salary (regardless of days)

- UK relief is then available via the foreign tax credit mechanism

4. UK Pensions in Japan: The 25% Lump Sum Trap

UK pensions are one of the most complex cross-border issues for British citizens in Japan. The treaty distinguishes between private and government pensions, and Japan’s NTA takes a markedly different view of the UK’s tax-free lump sum than HMRC does.

Private Pensions (State Pension, Workplace Pensions, Private Pensions)

Under Article 17 of the UK-Japan Tax Treaty, private pensions — including the UK State Pension, occupational pensions, and personal pensions — are taxed only in the country of residence. If you live in Japan, this means:

- The UK cannot withhold tax on your State Pension payments

- You must declare the pension income on your Japanese tax return

- Japan taxes it as miscellaneous income (雑所得) under its normal progressive rates

Government Pensions (Civil Service, Armed Forces)

Article 18 provides a different rule: government pensions for past government service are taxed only in the UK — unless you are a Japanese national. This means:

- Former civil servants, MOD personnel, and NHS pension recipients continue paying UK tax on these pensions

- Japan exempts this income from Japanese taxation

- If you have acquired Japanese nationality, the exemption no longer applies and Japan may tax the pension

The 25% Tax-Free Lump Sum Problem

Critical Trap

The UK allows you to take up to 25% of your pension pot as a tax-free lump sum (Pension Commencement Lump Sum). However, Japan’s National Tax Agency does NOT recognize this UK tax exemption. Japan will treat the lump sum as either:

- Retirement income (退職所得) if it qualifies under Japan’s retirement income rules

- Temporary income (一時所得) in other cases

In either case, it is taxable in Japan. Planning the timing of your lump sum withdrawal relative to your Japan residency status is essential.

SIPP (Self-Invested Personal Pension)

SIPPs add another layer of complexity. Japan does not recognize SIPPs as equivalent to Japan’s public pension system (公的年金). Instead, SIPP distributions are treated as miscellaneous income (雑所得) in Japan, taxed at your marginal rate. The favorable tax treatment that SIPPs enjoy in the UK — tax-free growth, 25% tax-free lump sum — is entirely irrelevant to the Japanese tax calculation.

Planning Tip: If you are still within your NPR 5-year window, SIPP withdrawals may be classified as foreign-source income. If you do not remit the funds to Japan, they may escape Japanese taxation during this period. Consult a specialist before making withdrawals.

5. ISA: Why Your Tax-Free Savings Aren’t Tax-Free in Japan

Individual Savings Accounts (ISAs) are one of the UK’s most popular tax shelters — Cash ISAs, Stocks & Shares ISAs, and Lifetime ISAs. In the UK, all income and capital gains within an ISA wrapper are completely tax-free.

Japan does not care.

Warning: ISA Tax-Free Status Not Recognized

Japan’s National Tax Agency does not recognize the ISA wrapper. For Japanese tax purposes, all dividends, interest, and capital gains generated within your ISA are fully taxable — exactly as if the investments were held in a standard brokerage account. This applies to:

- Cash ISA interest: Taxable as interest income in Japan

- Stocks & Shares ISA dividends: Taxable as dividend income

- ISA capital gains: Taxable at Japan’s 20.315% rate on listed securities

The NPR Window

During your first 5 years in Japan (NPR status), ISA income may be classified as foreign-source income. If you do not remit the proceeds to Japan, you may be able to defer Japanese taxation. However, once you become a permanent tax resident (after 5 years), all ISA income becomes taxable regardless of remittance.

Practical Advice

- You can keep your existing ISA — you just cannot add new contributions while non-UK resident

- Track all dividends, interest, and realized gains for your Japanese tax return

- Consider whether the administrative burden of tracking ISA income justifies holding the ISA vs. restructuring your portfolio

- Japan’s NISA offers a similar (though more limited) tax-free wrapper for investments held at Japanese brokerages

6. UK Property Income & the Remittance Trap

Many British citizens in Japan retain rental property in the UK. The tax treatment depends on your Japan residency status.

During NPR Status (First 5 Years)

UK rental income is classified as foreign-source income for Japanese tax purposes. Under NPR rules, it is only taxable in Japan if remitted to Japan. This creates a planning opportunity — but also a trap.

The Fungibility Rule (Remittance Trap)

Japan’s NTA applies a fungibility rule to determine whether foreign-source income has been remitted. If you have a UK bank account that receives both rental income and salary, and you transfer any money from that account to Japan, the NTA may deem that rental income has been remitted. The key points:

- Mixing foreign-source income with other funds in a single account creates remittance risk

- The NTA does not apply strict FIFO/LIFO ordering — commingled funds are treated as partially foreign-source

- Best practice: Maintain separate UK bank accounts for rental income and other funds

After 5 Years (Permanent Resident)

Once you exceed the 5-year NPR threshold, UK rental income becomes taxable in Japan regardless of remittance. You must report it on your Japanese tax return. The UK will also tax it under Non-Resident Landlord (NRL) scheme rules. Double taxation is eliminated via the foreign tax credit.

UK-Side Obligations

Even while living in Japan, you remain liable for UK income tax on UK rental income. The Non-Resident Landlord (NRL) scheme requires your letting agent (or tenant, if direct) to withhold 20% basic rate tax. You can apply to HMRC for approval to receive rents gross using form NRL1.

7. Capital Gains: Stocks vs Real Estate

The treaty and domestic law create different rules depending on the asset type.

Stocks and Movable Property

Under the UK-Japan treaty, capital gains from selling stocks and other movable property are taxed only in the country of residence. For a UK citizen resident in Japan:

- Gains on UK stocks: taxed in Japan only (at 20.315% for listed securities)

- No UK Capital Gains Tax (CGT) applies while you are treaty-resident in Japan

- During NPR period: gains on UK stocks may be foreign-source and remittance-dependent

Real Estate

Capital gains from real estate are taxed in the country where the property is located:

- UK property: Subject to UK CGT (Non-Resident Capital Gains Tax applies since April 2015 for residential, April 2019 for all UK property)

- Japan property: Subject to Japanese capital gains tax (short-term 39.63% / long-term 20.315%)

- If both countries tax the gain, the foreign tax credit eliminates double taxation

Real Estate Holding Companies (REHC)

If you sell shares in a company where more than 50% of its assets consist of Japanese real estate, Japan can tax the gain under the treaty. This anti-avoidance rule prevents using corporate structures to convert real estate gains into stock gains.

For a complete guide to capital gains taxation in Japan, see our Capital Gains Tax Guide.

8. Exit Tax: The ¥100M Threat for Long-Term Residents

Japan’s exit tax (国外転出時課税) applies to individuals who leave Japan after meeting specific criteria. It is particularly relevant for British citizens who have accumulated significant investment portfolios during their time in Japan.

Who Is Affected?

The exit tax applies if all of the following are true:

- You hold a Table 2 visa (spouse visa, permanent resident, long-term resident) — work visa holders on Table 1 are generally exempt

- You have resided in Japan for 5 or more of the past 10 years

- Your financial assets (stocks, bonds, derivatives, mutual funds) exceed ¥100 million (approximately £530,000) on the date of departure

What Is Taxed?

The exit tax treats your financial assets as if they were sold at fair market value on the date you leave Japan. Unrealized gains are taxed at 15.315% (income tax + reconstruction surcharge). Resident tax does not apply.

Planning Tip: If you plan to return to Japan within 5 years, you can apply for a tax deferral. If you re-establish tax residence within 5 years (extendable to 10 years with approval), the exit tax is cancelled. Provide collateral to the NTA to secure the deferral.

For full details, see our Exit Tax Guide.

9. Eliminating Double Taxation

When the same income is taxed by both the UK and Japan, you need to claim relief in one or both countries. The mechanism differs on each side.

UK Side: Self Assessment & SA106

To claim credit for Japanese taxes paid against your UK tax liability:

- File a Self Assessment tax return

- Complete the SA106 Foreign pages to report foreign income and claim foreign tax credit

- Refer to HMRC Helpsheet HS263 for guidance on calculating the credit

- The credit is limited to the UK tax attributable to that specific foreign income — you cannot use excess Japanese tax credits to reduce UK tax on UK income

Japan Side: Foreign Tax Credit (外国税額控除)

To claim credit for UK taxes paid against your Japanese tax liability:

- File the foreign tax credit schedule with your Japanese tax return (確定申告)

- The credit is calculated using the standard formula: Japan tax × (foreign-source income / worldwide income)

- Unused credits can be carried forward for 3 years

For a detailed walkthrough, see our Foreign Tax Credit Guide.

The Tax Year Mismatch Problem

Warning: Misaligned Tax Years

The UK tax year runs April 6 to April 5. The Japanese tax year runs January 1 to December 31. This creates practical complications:

- UK income earned January–March falls in the previous UK tax year but the current Japanese tax year

- Matching tax paid and credits claimed across misaligned periods requires careful record-keeping

- You may need to split annual UK income pro rata when claiming Japanese foreign tax credits

10. Social Security: The Missing Totalization Problem

The UK and Japan have a bilateral Social Security Agreement that prevents dual social security contributions. However, this agreement has a critical gap compared to agreements Japan has with other countries.

What the Agreement Does

- Prevents dual contributions: If sent to Japan temporarily (up to 5 years, extendable to 8), you can remain in the UK National Insurance system and be exempt from Japanese pension contributions

- Similarly, Japanese workers sent to the UK temporarily can remain in the Japanese system

- Coverage certificates are issued by HMRC International Caseworker to prove exemption

What the Agreement Does NOT Do

Critical Gap: No Totalization of Pension Periods

Unlike Japan’s agreements with the US, Germany, France, and many other countries, the UK-Japan agreement does NOT include totalization of pension qualification periods. This means:

- Years of contributions in Japan cannot be counted toward qualifying for the UK State Pension (you need 10+ years of NI contributions for any State Pension, 35 years for the full amount)

- Years of NI contributions cannot be counted toward Japan’s pension eligibility (10-year minimum)

- If you spend 15 years in Japan contributing to Japan’s pension, then return to the UK with only 8 years of NI contributions, you will have no UK State Pension entitlement

Protecting Your UK State Pension

This gap makes it essential for British citizens in Japan to maintain their UK National Insurance record:

- Class 2 voluntary NI contributions: Available if you were employed or self-employed in the UK immediately before leaving. Currently approximately £3.45/week

- Class 3 voluntary NI contributions: Available to anyone. Currently approximately £17.45/week

- Apply via HMRC form CF83

- Check your NI record online at gov.uk/check-national-insurance-record

Important: During the period you are exempt from Japanese pension contributions under the bilateral agreement, you are prohibited from voluntarily enrolling in the Japanese pension system. This makes maintaining your UK NI contributions even more critical during temporary postings.

11. Non-Dom Abolition & Japan’s NPR: Comparison

The UK abolished its historic non-domicile (non-dom) tax regime in April 2025, replacing it with the Foreign Income and Gains (FIG) regime. For British citizens considering a move between the UK and Japan, it is worth comparing these two systems.

| Feature | UK FIG Regime (from April 2025) | Japan NPR Status |

|---|---|---|

| Duration | 4 years from arrival in the UK | 5 years (aggregate domicile in past 10 years) |

| Eligibility | New UK residents (non-UK resident for previous 10 years) | Non-Japanese nationals with domicile in Japan, ≤5 years in past 10 |

| Foreign income protection | 100% exempt (not remittance-based) | Foreign-source income taxed only if remitted to Japan |

| Remittance basis | No (full exemption regardless of remittance) | Yes (foreign-source income taxed when remitted) |

| After expiry | Worldwide taxation (arising basis) | Worldwide taxation (regardless of remittance) |

| Annual fee | None (old non-dom had £30k/£60k charge) | None |

Key Difference: The UK’s FIG regime provides a complete exemption on foreign income for 4 years regardless of remittance. Japan’s NPR is remittance-based — you can bring foreign-source income to Japan, but you’ll be taxed on it. For someone moving from the UK to Japan, the NPR offers an extra year (5 vs 4) but with the remittance condition attached.

Summary for UK Citizens in Japan

- Check your UK residence status under the SRT — you may still be UK tax resident

- Japan’s NPR status protects foreign-source income from tax for up to 5 years (if not remitted)

- UK private pensions are taxed in Japan only; government pensions in the UK only

- The UK 25% tax-free lump sum is taxable in Japan — plan the timing carefully

- ISA income is fully taxable in Japan — the wrapper is irrelevant

- Separate your UK bank accounts to avoid the remittance/fungibility trap

- Pay voluntary NI contributions to protect your UK State Pension

- Use SA106 (UK) and the foreign tax credit schedule (Japan) to eliminate double taxation

- Exit tax applies at >¥100M financial assets after 5+ years on Table 2 visa

Need help with UK-Japan tax planning?

Get matched with an English-speaking tax accountant who understands cross-border issues — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

Do UK citizens pay tax in both the UK and Japan?

It depends on your residence status. If you are treaty-resident in Japan and non-resident in the UK under the SRT, most of your income will be taxed only in Japan. However, UK property income, government pensions, and certain other UK-source income may still be taxable in the UK. The UK-Japan Tax Treaty and foreign tax credits prevent true double taxation on the same income.

Is my ISA tax-free in Japan?

No. Japan does not recognize the ISA wrapper. All dividends, interest, and capital gains generated within your ISA are fully taxable in Japan. During your first 5 years (NPR status), ISA income may be treated as foreign-source income and taxable only if remitted. After 5 years, it is taxable regardless.

Can I count my Japan pension contributions toward my UK State Pension?

No. The UK-Japan Social Security Agreement does not include totalization of pension periods. Your years of contributions in Japan cannot count toward the UK State Pension qualifying period. You should pay voluntary Class 2 or Class 3 NI contributions to maintain your UK pension entitlement.

Is my UK pension 25% tax-free lump sum taxable in Japan?

Yes. Japan does not recognize the UK’s Pension Commencement Lump Sum as tax-free. It will be treated as retirement income or temporary income (ichiji shotoku) in Japan, subject to Japanese tax. If you are still in your NPR window, timing the withdrawal carefully may reduce or defer the Japanese tax obligation.