Other country-pair guides: India-Japan DTAA · Canada-Japan · Australia-Japan

The UK-Japan Tax Treaty prevents double taxation on your income, investments, and pensions. But it doesn’t protect your ISA or SIPP. Here’s what the treaty actually covers — and the gaps that can cost you.

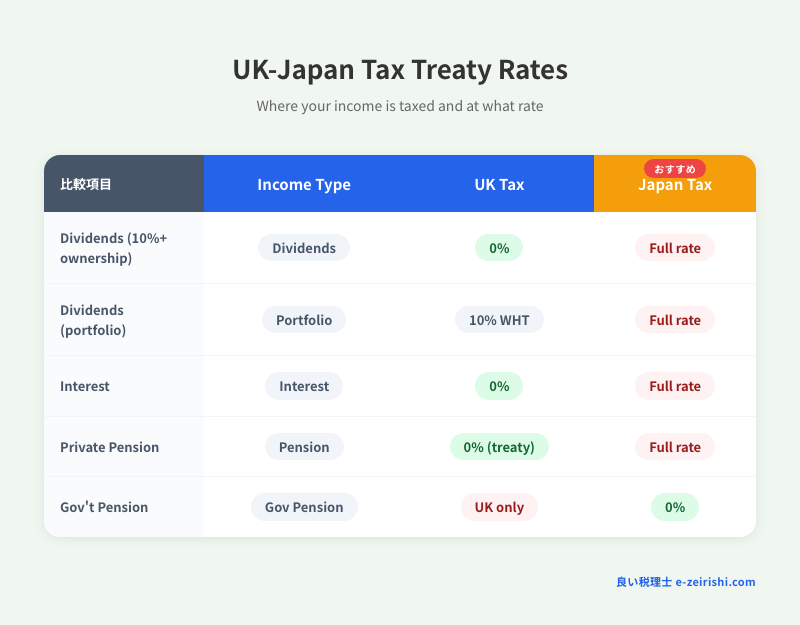

UK-Japan Treaty: Where each income type is taxed

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Treaty interpretation depends on specific circumstances and may be affected by MLI modifications. Always consult qualified professionals — a Japanese tax accountant (zeirishi) and a UK chartered accountant — for advice on your particular situation.

Need a bilingual tax accountant who understands the UK-Japan treaty?

Get matched with a specialist — free.

The Convention between the United Kingdom and Japan for the Elimination of Double Taxation and the Prevention of Fiscal Evasion has been in effect since 2006 and was subsequently modified by the Multilateral Instrument (MLI). It covers income tax, corporation tax, capital gains tax (UK side), and income tax, corporation tax, inhabitant taxes, and enterprise tax (Japan side).

This guide provides a practical, article-by-article breakdown of the treaty provisions most relevant to British individuals living and working in Japan, including the critical gaps where the treaty offers no protection.

Quick Summary: UK-Japan Treaty Rates

- Dividends (parent-subsidiary, 10%+ ownership, 6+ months): 0%

- Dividends (portfolio / general): 10%

- Interest: 0% (profit-linked interest: 10%)

- Royalties: 0%

- Private pensions: residence country only

- Government pensions: source country only

- Capital gains (stocks): residence country only

- Capital gains (real estate): situs country

- NOT covered: ISA tax-free status, SIPP recognition, NI credits

Table of Contents

- Treaty Overview & MLI Modifications

- Dividend Taxation

- Interest & Royalties

- Pension Rules: The Public vs Private Split

- Employment Income & 183-Day Rule

- Capital Gains: Stock vs Real Estate vs REHC

- How to Claim Relief: UK Side

- How to Claim Relief: Japan Side

- Tax Year Mismatch Problem

- What the Treaty Does NOT Cover

- Frequently Asked Questions

1. Treaty Overview & MLI Modifications

The UK-Japan tax treaty was signed on February 2, 2006, and entered into force on October 12, 2006. It replaced the earlier 1969 convention. Both the UK and Japan are signatories to the OECD’s Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting (the MLI), which modifies the treaty in several important ways.

Key MLI Changes

- Principal Purpose Test (PPT): Treaty benefits can be denied if one of the principal purposes of an arrangement was to obtain the benefit. This is an anti-avoidance measure

- Permanent Establishment (PE): Modified definition may affect commissionnaire arrangements and split contracts

- Mutual Agreement Procedure (MAP): Enhanced dispute resolution, including mandatory binding arbitration for certain cases

- Dual residence tiebreaker: For entities (not individuals), requires mutual agreement rather than place of effective management

Taxes Covered

| UK Taxes Covered | Japan Taxes Covered |

|---|---|

| Income tax | Income tax (所得税) |

| Corporation tax | Corporation tax (法人税) |

| Capital gains tax | Inhabitant taxes (住民税) |

| — | Enterprise tax (事業税) |

Note that National Insurance contributions (UK) and social insurance premiums (Japan) are not covered by the tax treaty. These are governed by the separate UK-Japan Social Security Agreement.

2. Dividend Taxation

The treaty provides two rates for dividends depending on the ownership stake:

| Scenario | Withholding Rate | Conditions |

|---|---|---|

| Parent-subsidiary | 0% | Beneficial owner holds 10%+ of voting shares for 6+ months before dividend date |

| Portfolio / general | 10% | All other dividend payments |

How This Works in Practice

For most individual British investors receiving dividends from UK companies while living in Japan:

- The UK can withhold up to 10% at source (though the UK currently does not impose withholding tax on dividends to individuals — companies may have different treatment)

- Japan taxes the dividend at your marginal income tax rate, or at 20.315% if you elect separate taxation for listed stock dividends

- Any UK tax withheld can be credited against your Japanese tax liability via the foreign tax credit

UK Dividend Note: Unlike many countries, the UK does not currently impose withholding tax on dividends paid to non-resident individuals. This means in practice, UK dividends received by a British citizen in Japan may only be taxed by Japan. However, if you own shares in a UK company that pays dividends through a custodian or platform, verify whether any withholding occurs at the platform level.

3. Interest & Royalties

Interest: 0% Rate

Under the UK-Japan treaty, interest payments are generally exempt from withholding tax in the source country:

- Standard rate: 0% — no withholding in the country of origin

- Exception: Profit-linked interest (interest whose amount is determined by reference to the debtor’s profits) is subject to a 10% withholding rate

- Interest is taxed in the recipient’s country of residence at normal rates

For British citizens in Japan, this means interest from UK bank accounts and bonds should not be subject to UK withholding. Japan will tax the interest as part of your worldwide income.

Royalties: 0% Rate

Royalty payments between the UK and Japan are completely exempt from source-country withholding:

- Covers literary, artistic, scientific work, patents, trademarks, know-how

- No withholding in the source country

- Taxed only in the country of residence

This is favorable compared to many other treaties. For example, the US-Japan treaty imposes 0% on royalties as well, but some other countries maintain higher withholding rates.

4. Pension Rules: The Public vs Private Split

The pension articles are among the most practically important — and most misunderstood — provisions of the UK-Japan treaty. The treaty creates a clear division between private and government pensions.

Article 17: Private Pensions

Private pensions, annuities, and similar payments are taxable only in the country of residence. For a British citizen living in Japan, this covers:

- UK State Pension: Despite being a government-administered scheme, the State Pension falls under Article 17 (private pension rules), not Article 18 (government service pensions). It is taxed only in Japan

- Workplace pensions: Defined benefit and defined contribution schemes from private employers — taxed only in Japan

- Personal pensions and SIPPs: Taxed only in Japan

Important Distinction: The UK State Pension is a social security benefit, not a government service pension. It falls under the private pension article (Article 17) and is taxed only in Japan. Many people incorrectly assume it is a “government pension” and should be taxed in the UK — this is wrong under the treaty.

Article 18: Government Service Pensions

Pensions paid for past government service (civil service pensions, Armed Forces pensions, NHS pensions paid by the government) are taxed only in the paying country (UK) — unless the recipient is a national of the other country (Japan).

- Former UK civil servants living in Japan: pension taxed in UK only

- If the recipient has acquired Japanese nationality: Japan can tax the pension

- Japan exempts the income from Japanese taxation (for non-Japanese nationals)

The 25% Lump Sum Problem

Warning: Japan Does Not Recognize the 25% Tax-Free Lump Sum

The UK allows pension holders to take up to 25% of their pension pot as a Pension Commencement Lump Sum (PCLS), completely tax-free in the UK. However:

- The treaty does not require Japan to honor UK domestic tax exemptions

- Japan’s NTA treats the lump sum as taxable income — either as retirement income (退職所得) or temporary income (一時所得)

- Since the UK does not tax the lump sum, there is no foreign tax credit available in Japan

- Result: the lump sum is taxed at Japan’s rates with no offset

Planning note: Consider taking the lump sum before establishing Japan tax residence, or during a period of non-residence in Japan.

5. Employment Income & 183-Day Rule

The treaty’s employment article (Article 14) establishes that employment income is generally taxable in the country where the work is performed. The 183-day rule provides an exemption for short-term assignments.

The Rule: Three Cumulative Conditions

Employment income earned in the host country is exempt from host-country tax if all three conditions are met:

| Condition | Requirement |

|---|---|

| 1. Duration | Present in the host country for ≤183 days in any rolling 12-month period |

| 2. Employer residence | Remuneration paid by an employer who is NOT a resident of the host country |

| 3. PE/fixed base | Remuneration is NOT borne by a PE or fixed base of the employer in the host country |

If any one condition is not met, the exemption fails and the host country can tax the employment income.

Rolling 12-Month Period — Not Calendar Year

The UK-Japan treaty uses a rolling 12-month period for counting the 183 days. This is stricter than a calendar-year test. Example: if you spend 100 days in Japan from August to December 2025 and 90 days from January to April 2026, you have exceeded 183 days in a 12-month window (August 2025–July 2026) even though you stayed under 183 in each calendar year.

Director’s Fees

Article 15 provides a separate rule for directors: fees paid to a director of a company resident in one country by a resident of the other may be taxed in the company’s country of residence. This overrides the employment article for board-level compensation.

6. Capital Gains: Stock vs Real Estate vs REHC

The treaty distinguishes between different types of capital gains, assigning taxing rights based on the nature of the underlying asset.

Stocks and Movable Property

Capital gains from the alienation of movable property (stocks, bonds, personal property) are taxable only in the country of residence of the seller. For a UK citizen living in Japan:

- Selling UK stocks while resident in Japan → taxed in Japan only

- Japan’s rate for listed securities: 20.315% (15.315% income tax + 5% resident tax)

- UK cannot apply CGT (you are treaty-non-resident in the UK)

Real Estate

Capital gains from real property may be taxed in the country where the property is located (the situs rule):

- Selling UK property from Japan: UK Non-Resident CGT applies. Japan also taxes as worldwide income (after 5 years). Foreign tax credit eliminates double taxation

- Selling Japan property: Japan taxes the gain. If the UK also considers you resident (SRT), the foreign tax credit applies

Real Estate Holding Companies (REHC)

The treaty contains an important anti-avoidance provision: if you sell shares in a company where more than 50% of its value derives from real property situated in one country, that country may tax the gain as if it were a direct real estate sale.

Example: You own shares in a Japanese KK (kabushiki kaisha) that holds a portfolio of Tokyo apartments. The apartments represent 80% of the company’s asset value. If you sell your shares, Japan can tax the gain under the REHC rule, even though you’re technically selling shares (normally taxed in residence country only).

For a comprehensive guide on capital gains, see our Capital Gains Tax Guide.

7. How to Claim Relief: UK Side

If you remain liable for UK tax on certain income (e.g., UK property, government pension) while also paying Japanese tax, you can claim foreign tax credit relief on the UK side.

Forms and Process

- Register for Self Assessment with HMRC if not already registered

- File a Self Assessment tax return (SA100)

- Complete the SA106 Foreign pages — this is where you report foreign income and claim credit for foreign taxes paid

- Refer to HMRC Helpsheet HS263 (“Calculating Foreign Tax Credit Relief”) for the detailed computation

Credit Limitations

- The foreign tax credit is limited to the UK tax attributable to that specific foreign income

- You cannot use excess foreign tax credits to reduce UK tax on UK-source income

- The credit is calculated on a source-by-source, category-by-category basis

- Unrelieved foreign tax cannot be carried forward in the UK (unlike Japan)

Treaty Relief vs. Unilateral Relief

The UK provides two mechanisms for avoiding double taxation:

- Treaty relief: Based on the UK-Japan treaty — may exempt certain income entirely or limit withholding rates

- Unilateral relief: Available under UK domestic law (TIOPA 2010) even for income types not covered by the treaty

- You can claim whichever gives the better result, but not both on the same income

8. How to Claim Relief: Japan Side

Japan’s foreign tax credit (外国税額控除) allows you to credit UK taxes paid against your Japanese tax liability.

The Formula

The maximum credit is calculated as:

Key points:

- The credit cannot exceed the amount of Japanese tax attributable to foreign-source income

- Separate limits apply for income tax and resident tax

- If the foreign tax exceeds the income tax credit limit, the excess can be applied against resident tax (up to a separate limit)

Filing Requirements

- Attach the foreign tax credit schedule (外国税額控除に関する明細書) to your 確定申告 (kakutei shinkoku)

- Provide documentation of UK tax paid (Self Assessment statement, withholding certificates)

- Filing deadline: March 15 of the year following the tax year

Carry-Forward

Unlike the UK, Japan allows 3-year carry-forward of excess foreign tax credits. If your UK tax paid exceeds the credit limit in a given year, you can apply the excess against Japanese tax in the following 3 years. This is particularly useful when:

- You have a spike in UK tax (e.g., selling UK property) that exceeds Japan’s credit limit for that year

- Tax year mismatches cause timing differences

For more details, see our Foreign Tax Credit Guide.

9. Tax Year Mismatch Problem

One of the most overlooked practical challenges in UK-Japan tax compliance is the misaligned tax year.

| Country | Tax Year | Filing Deadline |

|---|---|---|

| UK | April 6 – April 5 | January 31 (online) / October 31 (paper) |

| Japan | January 1 – December 31 | March 15 |

Practical Implications

The Overlap Problem

Consider UK rental income earned in February 2026:

- For Japan: falls in the 2026 tax year (Jan–Dec 2026), filed by March 15, 2027

- For UK: falls in the 2025/26 tax year (Apr 6, 2025–Apr 5, 2026), filed by January 31, 2027

When claiming Japan’s foreign tax credit, you need to match the UK tax paid on this income to the correct Japanese tax year. Since the UK tax return covers a different period, you may need to pro-rate the UK tax attributable to the overlapping months.

Best Practices

- Maintain monthly or quarterly records of income and tax payments in both countries

- When filing in Japan (March 15 deadline), the UK tax return for the overlapping period may not yet be finalized — use estimates and amend if needed

- Japan’s 3-year carry-forward on foreign tax credits provides a buffer for timing mismatches

- Keep all UK HMRC correspondence and Self Assessment statements for at least 7 years

10. What the Treaty Does NOT Cover

Understanding the treaty’s limitations is just as important as knowing its benefits. Several areas critical to British citizens in Japan fall outside the treaty’s protection.

ISA Tax-Free Status

Not Protected by the Treaty

The UK-Japan treaty does not require Japan to recognize the tax-free status of Individual Savings Accounts (ISAs). The ISA wrapper is a UK domestic tax benefit. Japan treats all ISA income — dividends, interest, and capital gains — as fully taxable, exactly as if the investments were held in a standard account.

SIPP Recognition

While the treaty ensures that pension income is taxed only in the residence country, it does not require Japan to treat SIPPs as equivalent to Japanese public pensions (公的年金). Japan classifies SIPP distributions as miscellaneous income (雑所得), not pension income. This means:

- No favorable pension income deduction

- Taxed at your marginal rate

- The 25% tax-free lump sum from a SIPP is taxable in Japan

National Insurance Contributions

NI contributions and Japanese social insurance premiums are not covered by the tax treaty. These are governed by the separate UK-Japan Social Security Agreement, which:

- Prevents dual contributions (up to 5 years, extendable to 8)

- Does NOT totalize pension qualifying periods

- Does not affect NI credits for child benefit or caring responsibilities

Inheritance and Gift Tax

The UK-Japan treaty covers only income and capital gains taxes. Japan’s inheritance tax (相続税) and gift tax (贈与税) are not covered. There is no separate UK-Japan inheritance/gift tax treaty. Given Japan’s worldwide estate taxation after the 10-year domicile threshold, this is a significant gap for long-term British residents with substantial assets.

Stamp Duty and Transaction Taxes

UK Stamp Duty Land Tax (SDLT) and Japan’s registration and license tax (登録免許税) and real estate acquisition tax (不動産取得税) are not covered by the treaty.

Summary: UK-Japan Tax Treaty Key Points

- Treaty provides 0% withholding on interest and royalties — among the most favorable rates globally

- Dividends: 0% for parent-subsidiary (10%+ ownership), 10% for portfolio

- Private pensions (including UK State Pension): taxed in Japan only

- Government pensions: taxed in UK only (unless Japanese national)

- Stock gains: residence country only. Real estate gains: situs country

- 183-day rule uses rolling 12-month period — stricter than calendar year

- UK relief: SA106 + Helpsheet HS263. Japan relief: foreign tax credit with 3-year carry-forward

- Treaty does NOT protect: ISA status, SIPP recognition, NI totalization, inheritance/gift tax

Need help applying the UK-Japan treaty to your situation?

Get matched with an English-speaking tax accountant who specializes in cross-border taxation — completely free.

Or message us directly: WhatsApp

Frequently Asked Questions

Does the UK-Japan tax treaty prevent double taxation completely?

The treaty provides mechanisms to eliminate double taxation on most income types through reduced withholding rates and foreign tax credits. However, it does not cover all situations. ISA income, inheritance/gift tax, and social security contributions are outside the treaty’s scope. You may need to rely on domestic relief provisions (UK unilateral relief or Japan’s foreign tax credit) for income not explicitly covered.

Is the UK State Pension taxed in the UK or Japan?

The UK State Pension is classified as a private pension under Article 17 of the treaty (not a government service pension under Article 18). It is taxed only in Japan if you are a Japan tax resident. You should apply to HMRC for exemption from UK tax on your State Pension payments by completing form DT-Individual.

Do I need to file a UK Self Assessment while living in Japan?

You need to file a UK Self Assessment if you have UK-source income that remains taxable in the UK (such as rental income, government pension, or UK employment income). If all your income is exempt from UK tax under the treaty, you may not need to file, but it can be beneficial to file to formally claim treaty relief and maintain a clean tax record with HMRC.

How do I handle the different UK and Japan tax year periods?

The UK tax year runs April 6 to April 5, while Japan’s runs January 1 to December 31. When claiming foreign tax credits, you need to match income and tax payments across these misaligned periods. Keep monthly records of income and tax in both countries, and use pro-rata calculations when necessary. Japan’s 3-year carry-forward of excess foreign tax credits helps manage timing differences.