US Citizens in Japan — Complete Tax Guide (2026)

The most comprehensive English guide to navigating the US-Japan dual tax system — because being American in Japan means filing with two of the world’s most aggressive tax agencies.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. US-Japan cross-border taxation is highly complex and depends on your specific circumstances. Always consult qualified professionals — a Japanese tax accountant (zeirishi) and a US CPA/EA — for advice on your particular situation.

US citizen looking for a bilingual tax accountant in Japan? Get matched with a specialist — free.

Get Matched Free →Approximately 76,000 US citizens live in Japan. Every single one is required to file taxes with both the IRS and Japan’s National Tax Agency (NTA) — regardless of whether they owe anything. This dual obligation creates a minefield of compliance requirements that can cost thousands of dollars in penalties if mishandled.

This guide covers the six critical areas every American in Japan must understand: the structural double taxation problem, FATCA/FBAR reporting, RSU taxation, retirement account traps, investment pitfalls (PFIC), and practical filing advice.

Table of Contents

FBAR vs FATCA: Two reports, two agencies

1. The Double Taxation Problem: FEIE vs FTC

The US is one of only two countries in the world (alongside Eritrea) that taxes based on citizenship, not residence. This means that as a US citizen living in Japan, you owe taxes to both countries on your worldwide income.

To prevent true double taxation, US tax law provides two main relief mechanisms:

Foreign Earned Income Exclusion (FEIE)

Filed using IRS Form 2555, FEIE lets you exclude a certain amount of foreign-earned income from US taxation:

- 2024 exclusion limit: $126,500

- 2025 exclusion limit: $130,000

- Only applies to earned income (salary, self-employment). Does NOT cover dividends, interest, rental income, or capital gains

FEIE vs FTC, FBAR, PFIC — our specialists handle the full complexity of US-Japan dual filing.

Get Matched with a US Tax Specialist in Japan →Free matching · No obligation · English support

Foreign Tax Credit (FTC)

Filed using IRS Form 1116, FTC lets you credit taxes paid to Japan dollar-for-dollar against your US tax liability:

- Applies to both earned and passive income

- Unused credits can be carried back 1 year or forward up to 10 years

- Works for all income types including dividends, capital gains, and rental income

Bottom Line: For Americans in Japan, FTC is almost always the better choice.

Japan’s combined tax rate (income tax + resident tax + reconstruction surcharge) reaches up to 55.94% — significantly higher than the US maximum federal rate of 37%. By choosing FTC, you generate massive excess credits that carry forward for 10 years, effectively making your US tax bill $0 while building a credit reserve for future use.

FEIE wastes those high Japanese taxes — they generate zero US credit, making them “lost money” from a tax planning perspective.

FEIE vs FTC: Practical Comparison by Income Level

| Annual Income (USD) | FTC Result | FEIE Result | Recommendation |

|---|---|---|---|

| ~$80,000 | US tax = $0. Small excess FTC carries forward. | US tax = $0. No credit generated. | FTC preferred (builds future credit reserve) |

| ~$130,000 | US tax = $0. Large excess FTC generated. | US tax = $0. High Japanese taxes wasted. | FTC strongly preferred |

| $150,000+ | US tax = $0. FTC covers all income types. | US tax due on amount exceeding $130K limit. | FTC essential |

The Child Tax Credit Bonus

If you have children under 17, choosing FTC over FEIE unlocks the Child Tax Credit — up to $2,200 per child (2025), with up to $1,700 refundable. With FEIE, your taxable earned income drops to zero, disqualifying you from the refundable portion. With FTC, your income base is preserved, meaning the IRS will actually send you a check.

Important: If you’ve been using FEIE and want to switch to FTC, be aware of the 5-year lockout rule — once you revoke FEIE, you cannot re-elect it for 5 tax years without IRS permission.

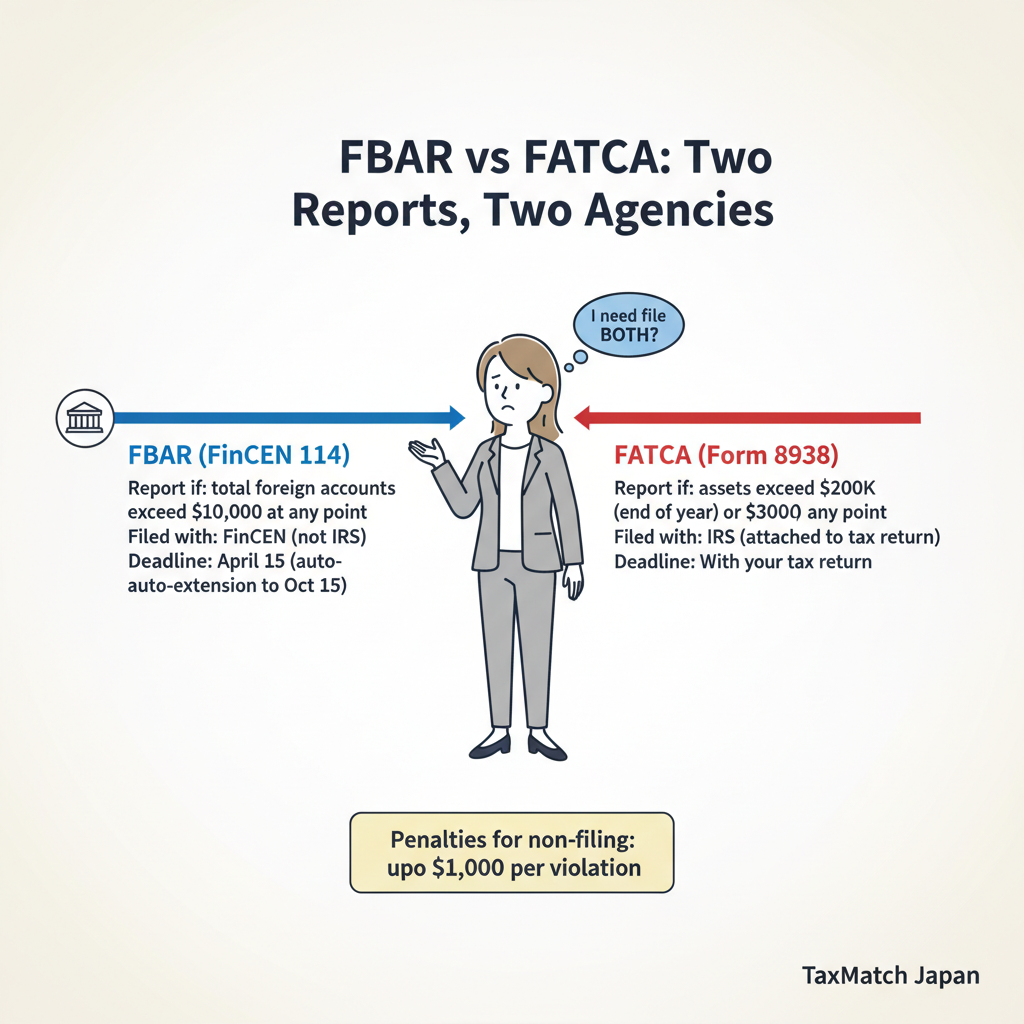

2. FATCA and FBAR: Financial Account Reporting

Beyond income taxes, US citizens must report their foreign financial accounts to two separate agencies through two separate forms. This is not about paying additional tax — it’s about disclosure. But the penalties for non-compliance are devastating.

FBAR vs FATCA: Key Differences

| Feature | FBAR (FinCEN Form 114) | FATCA (IRS Form 8938) |

|---|---|---|

| Filed with | FinCEN (Treasury Dept) via BSA E-Filing | IRS (attached to Form 1040) |

| Threshold (abroad) | $10,000 aggregate at any point in the year | Single: $200K year-end / $300K any time Joint: $400K year-end / $600K any time |

| What’s reported | Bank accounts, securities accounts, pension accounts | All of the above + foreign stocks, partnership interests, financial instruments |

| Deadline | April 15 (auto-extension to Oct 15) | Same as Form 1040 (June 15 for expats) |

| Penalty (non-willful) | Up to $16,536 per violation | $10,000 per form |

| Penalty (willful) | 50% of account balance or $165,353 (whichever is greater) | $50,000+ |

What Counts as a Reportable Account in Japan?

Almost everything:

- Savings and checking accounts (futsuu yokin, teiki yokin)

- Securities/brokerage accounts (SBI, Rakuten, etc.)

- iDeCo and corporate pension accounts

- Life insurance policies with cash value (yoro hoken, gakushi hoken)

- Your spouse’s accounts if you are a joint owner or have signature authority

The $10,000 FBAR threshold has not been adjusted for inflation since the 1970s. In practice, virtually every working American in Japan exceeds it.

Real Case: Kurotaki v. United States

In 2023, the IRS assessed approximately $10 million in FBAR penalties against a US permanent resident (green card holder) living in Japan who failed to report foreign accounts. The taxpayer argued he didn’t understand the English-language reporting requirements. The court found this constituted “reckless disregard” — a form of willfulness — and upheld the penalties. Ignorance of the law is not a defense.

If You’ve Missed Past Filings: Streamlined Filing Compliance Procedures

If you’ve been living abroad and didn’t know about FBAR/FATCA requirements, do not panic — but also do not quietly file past returns on your own. The IRS offers the Streamlined Foreign Offshore Procedures (SFOP), which allows you to:

- File 3 years of amended tax returns + 6 years of FBARs

- Submit a certification that your non-compliance was non-willful

- Pay zero FBAR penalties (for US-abroad filers)

This program is the safest path to compliance. Use it before the IRS contacts you — once they do, Streamlined is no longer available.

3. RSU and Stock Option Taxation

If you work at a US tech company or multinational, your RSUs create a complex dual-taxation scenario. Both the IRS and Japan’s NTA want to tax the same income.

How RSUs Are Taxed in Both Countries

| Event | Japan Tax Treatment | US Tax Treatment |

|---|---|---|

| Vesting | Employment income (salary) at FMV, converted to JPY at TTM rate. Taxed up to 55.9%. | Ordinary income at FMV in USD. Taxed up to 37%. |

| Sale | Capital gains at flat 20.315% on (sale price – vest price). | Short/long-term capital gains on (sale price – vest price). |

Eliminating Double Taxation: The Treaty Resourcing Rule

The US-Japan Tax Treaty includes a resourcing rule (Article 23) that is essential for avoiding double taxation on RSUs. When both countries tax the same RSU income, you can “re-source” the income on your US return to claim Japan’s high taxes as a Foreign Tax Credit.

This is reported on Form 1116 under the special category “Certain income re-sourced by treaty.” The result: your US tax on RSU income drops to zero, fully offset by the FTC from Japan.

Critical Warning: W-8BEN vs W-9

US citizens must never submit Form W-8BEN to their US brokerage, even though they live outside the US. W-8BEN is for non-US persons. As a US citizen, you must always file Form W-9 regardless of your country of residence. Submitting a false W-8BEN can constitute perjury.

4. IRA, 401(k), and Retirement Account Traps

US retirement accounts that work beautifully under American tax law can become nightmares when you move to Japan.

Traditional IRA / 401(k) Withdrawals

Under the US-Japan Tax Treaty, private pension distributions (IRA, 401k) from the US are generally taxable in your country of residence — meaning Japan has primary taxing authority. Japan classifies these withdrawals as “miscellaneous income” or “temporary income” (ichiji shotoku).

The good news: Japan only taxes the earnings portion, not your original contributions. If classified as temporary income, you get a ¥500,000 special deduction, and only 50% of the remainder is taxed. This can significantly reduce the bite.

The burden: You must prove the contribution vs. earnings split yourself. US brokerages don’t track this for Japanese tax purposes. Keep meticulous records of all IRS Form 5498s and account statements.

The Roth IRA Trap

Japan does NOT recognize Roth IRA’s tax-free status.

While Roth IRA withdrawals are completely tax-free in the US, Japan’s NTA does not honor this. If you withdraw from a Roth IRA while living in Japan, the earnings portion is fully taxable as miscellaneous or temporary income.

Worse: since the US doesn’t tax Roth withdrawals, you have no US tax to offset with FTC. The Japanese tax becomes a pure cost with no relief.

Best practice: If possible, liquidate Roth IRA earnings before moving to Japan to capture the US tax-free benefit. Once you’re a Japanese tax resident, the opportunity is lost.

US-Japan Social Security Agreement (Totalization)

The bilateral social security agreement prevents double payment of social insurance premiums:

- US employees dispatched to Japan for 5 years or less can stay in the US Social Security system and be exempt from Japanese pension

- Requires Form J/USA 6 (Certificate of Coverage) from the US Social Security Administration

- Pension contribution periods in both countries can be totalized to meet the qualifying period for benefits in either country

5. Investment Pitfalls: PFIC, NISA, and iDeCo

The PFIC Problem: Why You Can’t Buy Japanese Mutual Funds

This is arguably the single biggest financial trap for Americans in Japan. Under US tax law, any foreign fund where 75%+ of income is passive (interest, dividends, capital gains) is classified as a Passive Foreign Investment Company (PFIC).

This means every Japanese mutual fund and ETF is automatically a PFIC in the eyes of the IRS.

The consequences are severe:

- Gains taxed at the highest marginal rate (37%) instead of favorable capital gains rates

- Punitive interest charges applied retroactively over the holding period

- IRS Form 8621 required for each PFIC holding, every year — professional preparation can cost $500-1,000+ per form

What About NISA?

NISA’s tax-free benefit only applies to Japanese taxes. The US doesn’t recognize it. If you buy mutual funds in a NISA account, you get hit with PFIC treatment on the US side while gaining nothing extra on the Japan side (since capital gains are already tax-free in NISA for everyone).

The only viable NISA strategy for Americans: Use the Growth Investment category to buy individual Japanese stocks only (Toyota, Sony, Nintendo, etc.) — operating companies are NOT PFICs. This gives you Japan’s tax-free benefit without triggering US PFIC rules.

iDeCo: Proceed with Extreme Caution

Whether iDeCo is PFIC-exempt under Treasury Regulation 26 CFR 1.1298-1(c)(4) is unresolved among tax professionals. The US-Japan Tax Treaty lacks the clear pension deferral language found in US-UK and US-Canada treaties.

Conservative approach: If you use iDeCo at all, select only capital-preservation products (fixed deposits) to avoid PFIC-classified investment trusts inside the account.

Where Should Americans Invest?

| Investment | PFIC Risk | Recommendation |

|---|---|---|

| US-domiciled ETFs (VTI, VOO, etc.) via US brokerage | None | Best option |

| Individual Japanese stocks | None (operating companies) | OK |

| Individual US stocks via US brokerage | None | OK |

| Japanese mutual funds / Japanese ETFs | PFIC | Avoid |

| NISA with mutual funds | PFIC | Avoid |

| iDeCo with investment trusts | Uncertain / likely PFIC | Avoid or use fixed deposits only |

6. How to File: Practical Steps and Costs

The Filing Sequence (Critical)

The order matters. Getting it wrong makes accurate FTC calculation impossible.

Step 1 (January – March 15): Complete your Japanese tax return first. Work with your Japanese zeirishi to file by the March 15 deadline. Lock in your exact Japanese tax liability.

Step 2 (April – June 15): Share your confirmed Japanese tax data with your US CPA or EA. They use this to calculate Form 1116 (FTC) and offset your US liability. File by June 15 (automatic expat extension).

Step 3 (Throughout the year): File FBAR by April 15 (auto-extended to October 15). File state returns if applicable.

Do You Need Both a Japanese Zeirishi AND a US CPA?

Yes, in almost all cases. Licensing restrictions make this non-negotiable:

- Only a licensed zeirishi can prepare and file Japanese tax returns

- Only a US CPA, EA, or tax attorney can represent you before the IRS

- Very few professionals hold both licenses

The ideal setup is either (a) an international tax firm with both on staff, or (b) separate professionals who coordinate with each other.

Cost Estimates for US-Japan Dual Filing

| Service | Estimated Cost | Notes |

|---|---|---|

| US Side (CPA / Expat Tax Firm) | ||

| Federal return (Form 1040 + FTC) | $530 – $700 | Basic expat return |

| FBAR filing | $115+ | Extra per additional accounts |

| State tax return | $175+ per state | If residency obligation remains |

| PFIC reporting (Form 8621) | $665 – $1,000+ per form | Per fund held. Costs can exceed investment gains. |

| Streamlined Procedures | $1,600+ | Multi-year catch-up package |

| Japan Side (Zeirishi) | ||

| Bilingual boutique firm | ¥150,000 – ¥400,000 | Best fit for most Americans |

| Local firm (Japanese only) | ¥50,000 – ¥200,000 | Requires interpreter |

| Big 4 / international firm | ¥500,000 – ¥1,500,000 | Usually employer-paid for assignees |

Total annual compliance cost for a typical American in Japan with moderate complexity: $2,000 – $4,000+. This is the hidden “cost of being American abroad” that should be factored into your financial planning before relocating.

Key Takeaways

- Choose FTC over FEIE in almost all cases. Japan’s high taxes generate massive excess credits.

- File FBAR every year if your Japanese accounts exceed $10,000 total at any point. The penalties for missing this are catastrophic.

- Never buy Japanese mutual funds or ETFs. They are PFICs under US law and will cost you more in compliance than they earn.

- Do not withdraw from a Roth IRA while living in Japan. Japan taxes the earnings, and there’s no FTC offset.

- File Japan first, then the US. The sequence is essential for correct FTC calculation.

- Budget $2,000-4,000+/year for dual-country tax compliance.

Need a bilingual tax accountant who understands US-Japan cross-border issues? TaxMatch Japan is free for clients.

Get Matched Free →Disclaimer: This article is for informational purposes only and does not constitute tax advice. US-Japan tax situations are highly individual. Always consult qualified tax professionals — both a Japanese zeirishi and a US CPA/EA — before making tax decisions. Information is current as of 2026 and subject to change.

Frequently Asked Questions

Do US citizens in Japan have to file US taxes?

Yes. US citizens are required to file US federal tax returns regardless of where they live. If you live in Japan, you must report your worldwide income to both the IRS and Japanese tax authorities, though tax treaties and exclusions help prevent double taxation.

Should I use FEIE or FTC in Japan?

The Foreign Tax Credit (FTC) is generally more beneficial for US citizens in Japan because Japanese tax rates are typically higher than US rates. The Foreign Earned Income Exclusion (FEIE) excludes up to ~$126,500 (2025) of earned income but cannot be used to offset Japanese taxes already paid.

What is PFIC and why should Americans in Japan avoid Japanese mutual funds?

PFIC (Passive Foreign Investment Company) rules impose punitive US tax treatment on foreign mutual funds. Japanese investment trusts (toushin) are classified as PFICs, resulting in extremely high US tax rates and complex reporting requirements. US citizens in Japan should generally use US-based brokerages and ETFs instead.