The Australia-Japan Tax Treaty determines how your dividends, interest, pensions, and capital gains are taxed across both countries. Here’s the practical guide — including the franking credit trap and superannuation gaps.

Franked vs Unfranked: How imputation breaks for Japan residents

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax treaty interpretation can vary between the ATO and Japan’s National Tax Agency (NTA). Cross-border taxation depends on your specific circumstances. Always consult qualified professionals — a Japanese tax accountant (zeirishi) and an Australian tax adviser — before making decisions based on treaty provisions.

Quick Summary — Key Treaty Points

- The treaty was signed in 2008 and modified by the MLI (effective 2019)

- Dividend rates: 15% (portfolio), 5% (10%+ ownership), 0% (80%+ ownership with conditions)

- Interest: 10% | Royalties: 5%

- Franking credits are NOT recognized by Japan — the biggest trap for Australian investors

- Superannuation is NOT explicitly covered by the treaty

- No provision for deducting SG contributions from Japanese income (unlike France-Japan treaty)

Need help with Australia-Japan cross-border tax?

Get matched with a bilingual tax accountant — free.

The Agreement between Australia and Japan for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income is the legal framework governing how income is taxed when it crosses the Australia-Japan border. For the approximately 105,000 Australians living in Japan (Canadian counterpart: see our Canada-Japan tax treaty guide), understanding this treaty is essential for effective tax planning.

This guide focuses on the practical implications of each treaty provision — not just what the treaty says, but what it means for your tax return, your investment decisions, and your retirement planning.

Table of Contents

- Treaty Overview & MLI Modifications

- Dividends: Franked vs Unfranked

- Interest & Royalties

- Employment Income & 183-Day Rule

- Capital Gains: Stocks vs Real Estate vs REHC

- Superannuation Under the Treaty

- How to Claim Relief: ATO Side (FITO)

- How to Claim Relief: Japan Side (Foreign Tax Credit)

- What the Treaty Does NOT Cover

- FAQ

1. Treaty Overview & MLI Modifications

The current Australia-Japan tax treaty was signed on January 31, 2008, and entered into force on January 1, 2009, replacing the original 1969 agreement. The treaty follows the OECD Model Tax Convention structure, with modifications reflecting both countries’ tax policy priorities.

MLI (Multilateral Instrument) Impact

Both Australia and Japan are signatories to the OECD’s Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting (commonly called the MLI). The MLI modifications to the Australia-Japan treaty became effective on January 1, 2019.

Key MLI changes affecting this treaty:

- Principal Purpose Test (PPT): Added an anti-avoidance rule. Treaty benefits can be denied if one of the principal purposes of an arrangement was to obtain those benefits. This replaces the previous limitation-on-benefits (LOB) approach.

- Permanent Establishment (PE): Tighter definition of what constitutes a PE, including anti-fragmentation rules and expanded commissionaire arrangements.

- Dual Resident Entities: Resolved by mutual agreement rather than place of effective management.

- MAP (Mutual Agreement Procedure): Enhanced provisions for resolving disputes between the ATO and Japan’s NTA.

Covered Taxes

The treaty covers the following taxes:

| Country | Taxes Covered |

|---|---|

| Australia | Income tax (including resource rent taxes), fringe benefits tax |

| Japan | Income tax (所得税), corporation tax (法人税), residence tax (住民税), enterprise tax (事業税) |

Note that Japan’s consumption tax and Australia’s GST are not covered by the treaty.

Section Summary

- Current treaty: signed 2008, effective January 1, 2009

- MLI modifications effective January 1, 2019

- MLI added Principal Purpose Test and tighter PE definitions

- Covers income tax, corporation tax, residence tax, and enterprise tax

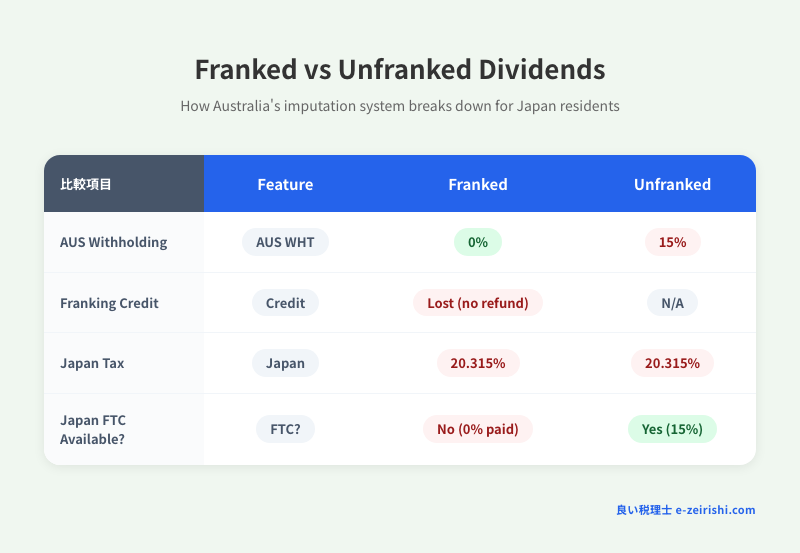

2. Dividends: Franked vs Unfranked

Dividend taxation is the area where the Australia-Japan tax relationship is most unique — and most problematic — due to Australia’s dividend imputation (franking) system.

Treaty Withholding Rates on Dividends

| Dividend Type | Treaty Withholding Rate | Japan Tax Treatment | Effective Total Tax |

|---|---|---|---|

| Unfranked, portfolio (<10% ownership) | 15% | Taxable at marginal rate (credit for 15%) | Marginal rate (no double tax) |

| Unfranked, 10%+ ownership | 5% | Taxable at marginal rate (credit for 5%) | Marginal rate (no double tax) |

| Unfranked, 80%+ ownership | 0% | Taxable at marginal rate (no credit) | Marginal rate only |

| Franked (any ownership) | 0% (AUS domestic law) | Fully taxable at 20.315%+ | 30% corporate + 20.315% = 44%+ |

The Franking Credit Trap — Explained

This deserves special attention because it is the most common — and most costly — misunderstanding for Australians in Japan.

How franking credits work in Australia: When an Australian company pays a dividend out of profits that have already been taxed at the 30% corporate rate, the dividend carries a “franking credit” representing the tax already paid. Australian resident shareholders include the grossed-up dividend in their income and receive a tax offset for the franking credit.

What happens when you become a Japan resident:

- Australia: Fully franked dividends paid to non-residents are exempt from Australian withholding tax (0% rate) under domestic law. The franking credit is not refundable to non-residents.

- Japan: Japan does not have a franking/imputation system and does not recognize Australian franking credits. The dividend you receive is taxed in full — either at the flat 20.315% rate for listed share dividends, or at your marginal rate if you elect aggregate taxation.

Numerical example:

| Step | Amount (AUD) |

|---|---|

| Company pre-tax profit | $100 |

| Australian corporate tax (30%) | −$30 |

| Dividend paid to you (fully franked) | $70 |

| Australian withholding tax (0% for franked) | $0 |

| Japan tax on $70 at 20.315% | −$14.22 |

| Foreign tax credit in Japan | $0 (no AUS tax was withheld) |

| Net cash received | $55.78 |

| Total effective tax rate on $100 profit | 44.22% |

Compare this to an Australian resident who would pay only their marginal rate minus the franking credit offset — potentially as low as 0% for a low-income earner.

Warning

There is no way to recover the lost franking credits while you are a Japan resident. The treaty does not address this issue, and Japan’s tax law does not have any mechanism to credit corporate tax paid by a foreign company on your behalf. This is a structural disadvantage that cannot be avoided through filing procedures — it requires portfolio restructuring.

Section Summary

- Unfranked dividends: treaty rates work as expected (15%/5%/0% withholding, Japan credits it)

- Franked dividends: 0% AUS withholding but fully taxable in Japan with no credit for corporate tax

- Total effective tax on franked dividends can reach 44%+ (30% corporate + 20.315% Japan)

- No treaty or domestic law solution — portfolio restructuring is the only mitigation

3. Interest & Royalties

Interest (Article 11)

Interest arising in Australia and paid to a Japan resident is subject to a maximum withholding rate of 10% under the treaty. Interest paid to government entities (including the Bank of Japan and the Reserve Bank of Australia) is exempt (0%).

Common sources of Australian interest income for Japan residents include:

- Term deposits and savings accounts at Australian banks

- Australian government bonds

- Mortgage offset account interest (if treated as interest income)

Warning — Domestic Rate vs Treaty Rate

Australia’s domestic withholding rate on interest paid to non-residents is 10% (which matches the treaty rate). However, if your bank does not have your current overseas address and treaty benefit claim on file, they may apply the default rate or even the higher domestic rate. Always ensure your financial institution has been notified of your non-resident status and Japan residency.

Royalties (Article 12)

Royalties arising in Australia and paid to a Japan resident are subject to a maximum withholding rate of 5% under the treaty. This is significantly lower than Australia’s domestic rate.

“Royalties” under the treaty includes payments for the use of or the right to use:

- Copyright (literary, artistic, scientific works)

- Patents, trademarks, designs, models, plans

- Industrial, commercial, or scientific equipment

- Industrial, commercial, or scientific experience (know-how)

Section Summary

- Interest: 10% treaty rate (matches AUS domestic rate for non-residents)

- Royalties: 5% treaty rate

- Ensure your Australian bank has your non-resident status on file

4. Employment Income & 183-Day Rule

Employment income is generally taxable in the country where the work is physically performed (Article 14). If you work in Japan, Japan taxes your salary. If you work in Australia during a business trip, Australia can tax the portion attributable to those days.

The 183-Day Exemption

A short-term business visitor may be exempt from taxation in the country of work if all three conditions are met:

- Present in the country for no more than 183 days in any 12-month period beginning or ending in the fiscal year

- The remuneration is paid by an employer who is not a resident of the country of work

- The remuneration is not borne by a permanent establishment (PE) of the employer in the country of work

All three conditions must be satisfied simultaneously. Failing even one means the exemption does not apply.

MLI Impact on the 183-Day Rule

The MLI has not changed the fundamental 183-day rule, but the anti-fragmentation rules for PE determination mean that what used to be considered separate activities may now be aggregated when assessing whether a PE exists. This can affect condition 3 for short-term business visitors whose employers have any operations in the host country.

Director’s Fees

Fees and other payments received as a member of the board of directors of a company are taxable in the country where the company is resident, regardless of where the services are performed. If you are on the board of an Australian company while living in Japan, Australia can tax those fees.

Section Summary

- Employment income taxed where work is performed

- 183-day exemption: all 3 conditions must be met (presence, employer residency, no PE bearing cost)

- MLI anti-fragmentation rules may affect PE assessment

- Director’s fees taxable where the company is resident

5. Capital Gains: Stocks vs Real Estate vs REHC

Capital gains taxation under the treaty depends on the type of asset being disposed of.

Capital Gains by Asset Type

| Asset Type | Which Country Taxes? | Key Notes |

|---|---|---|

| Real property (immovable property) | Country where property is located | Australia taxes gains on Australian property; Japan taxes gains on Japanese property |

| Shares in a Real Estate Holding Company (REHC) | Country where the real estate is located | If >50% of share value derives from real property, treated as real property gain |

| Business property of a PE | Country where PE is located | Includes alienation of the PE itself |

| Shares (general — not REHC) | Country of residence only | If you are Japan-resident, Japan taxes; Australia generally cannot (important for share portfolios) |

| Other property | Country of residence only | Catch-all provision |

Key Point — Australian Shares Held by Japan Residents

Under the treaty, gains from selling ordinary Australian shares (not REHCs) are taxable only in Japan. Australia should not impose CGT on these gains if you are a Japan tax resident. However, Australia’s domestic law override for non-resident CGT means that in practice, the ATO may still seek to tax certain gains — particularly on assets that have a connection to Australian business activities. The treaty should override domestic law, but enforcement can be complex.

FRCGW (Foreign Resident Capital Gains Withholding)

When a non-resident sells Australian real property (or shares in REHCs) with a market value of A$750,000 or more, the buyer must withhold 15% of the purchase price and remit it to the ATO. This applies even if the actual CGT liability is much lower. You can apply for a variation to reduce the withholding if you can demonstrate a lower expected tax liability.

Section Summary

- Real property gains: taxed where the property is located

- REHC shares (>50% real property value): treated as real property

- General shares: taxable only in country of residence (Japan)

- FRCGW: 15% withholding on property sales of A$750K+ (variation possible)

6. Superannuation Under the Treaty

This is one of the most problematic gaps in the Australia-Japan tax relationship. The treaty contains standard provisions for pensions and annuities (Article 17), but does not explicitly address Australian superannuation as a category.

What the Treaty Says About Pensions

Under Article 17, pensions (other than government pensions) paid to a resident of a contracting state are generally taxable only in the state of residence. Government pensions (Article 18) are generally taxable only in the paying state, unless the recipient is a resident and national of the other state.

The Superannuation Gap

The problem is that Australian superannuation does not fit neatly into the treaty’s pension provisions because:

- The treaty was drafted primarily with traditional pensions in mind — periodic payments in retirement

- Superannuation is a trust-based compulsory savings system with multiple access points (pension, lump sum, transition-to-retirement)

- The treaty does not define “superannuation” or provide specific rules for trust-based retirement vehicles

Japan’s NTA therefore treats super based on its structural characteristics — as an insurance-type private retirement savings vehicle based on its trust structure.

SG Contributions: The Missing Deduction

Perhaps the most practically significant gap is the treaty’s silence on Superannuation Guarantee (SG) contributions. Some tax treaties (notably the Japan-France treaty) explicitly allow residents to deduct mandatory foreign social insurance contributions from their taxable income. The Australia-Japan treaty has no such provision.

This means that if your employer makes SG contributions while you work in Japan, the NTA may treat those contributions as taxable employment income. The treaty offers no relief from this treatment.

Warning

The SG contribution issue is one of the most under-recognized tax risks for Australians in Japan. If your employer is making SG contributions (currently 11.5% of salary in 2025-26, rising to 12% from July 2026), the NTA could assess those contributions as taxable employment income. This can result in a significant additional tax liability that neither you nor your employer may have anticipated. The back-assessment period extends up to 5-7 years.

Section Summary

- Treaty covers “pensions” but does NOT explicitly address superannuation

- NTA treats super as trust-type retirement savings

- NO provision for deducting SG contributions from Japanese income (unlike France-Japan treaty)

- SG contributions risk being taxed as employment income with up to 7-year back-assessment

7. How to Claim Relief: ATO Side (FITO)

When Australian-sourced income is also taxed in Japan, the ATO provides relief through the Foreign Income Tax Offset (FITO).

FITO Basics

- Available for foreign tax paid on income that is also assessable in Australia

- For amounts of A$1,000 or less: you can claim the offset without calculating the limit

- For amounts over A$1,000: you must calculate the foreign income tax offset limit using the formula in Division 770 of the ITAA 1997

- The offset is non-refundable — it can reduce your Australian tax to zero but cannot generate a refund

- Excess credits cannot be carried forward to future years

FITO Calculation

The FITO limit is calculated as:

FITO Limit = Australian tax payable × (Net foreign income / Total assessable income)

You can claim the lesser of the actual foreign tax paid and the FITO limit.

Practical Tip: When FITO Is Insufficient

If Japan’s tax rate on certain income exceeds Australia’s rate, the FITO will not fully eliminate double taxation. In this case, the excess Japanese tax becomes a cost. This is most commonly an issue with:

- Employment income (Japan’s top marginal rate of 55.945% exceeds Australia’s 47%)

- Short-term capital gains (Japan: 39.63%, Australia: marginal rate)

Section Summary

- FITO: non-refundable offset, limited to Australian tax on that foreign income

- Claims under A$1,000: no limit calculation needed

- Excess credits cannot be carried forward

- When Japan’s rate exceeds Australia’s, some double taxation is unavoidable

8. How to Claim Relief: Japan Side (Foreign Tax Credit)

When you are a Japan tax resident and pay tax in Australia, Japan provides relief through the foreign tax credit (外国税額控除) system.

Basic Mechanism

Japan’s foreign tax credit allows you to credit Australian tax paid against your Japanese tax liability. The credit is applied at the national income tax level first, with any excess applied to residence tax (住民税).

Credit Limit Formula

Credit Limit = Japanese tax × (Foreign-sourced income / Total worldwide income)

You can credit the lesser of the actual Australian tax paid and this calculated limit.

Treaty Rate Limitation

Japan only credits foreign tax up to the treaty-permitted rate. This is critical:

| Scenario | AUS Withholding | Treaty Rate | Japan Credits | Lost |

|---|---|---|---|---|

| Interest (bank applies domestic rate) | 30% | 10% | 10% | 20% |

| Interest (bank applies treaty rate) | 10% | 10% | 10% | 0% |

| Unfranked dividend (portfolio) | 30% | 15% | 15% | 15% |

| Unfranked dividend (treaty claimed) | 15% | 15% | 15% | 0% |

Warning

If Australian tax is withheld at a rate higher than the treaty rate, Japan will only credit up to the treaty rate. The excess is lost. You must either (a) ensure your Australian institutions apply the treaty rate, or (b) file an Australian tax return and claim a refund of the excess withholding from the ATO. For details on the credit calculation, see our Foreign Tax Credit Guide.

Filing Procedure

To claim the foreign tax credit in Japan:

- File a kakutei shinkoku (確定申告) by March 15 of the following year

- Attach Form 外国税額控除に関する明細書 (Statement on Foreign Tax Credits)

- Provide evidence of Australian tax paid (withholding statements, AUS tax return)

Section Summary

- Japan credits Australian tax paid, limited to treaty-permitted rates

- Excess withholding beyond treaty rate is not credited — you lose it

- Credit applied to national income tax first, then residence tax

- File by March 15 with supporting documents

9. What the Treaty Does NOT Cover

Understanding the treaty’s gaps is just as important as understanding its provisions. Several significant issues affecting Australians in Japan fall outside the treaty’s scope:

1. Franking Credits

The treaty does not address or provide relief for Australia’s dividend imputation system. Japan does not credit or recognize franking credits. This is a structural gap, not an oversight — Japan simply does not have an imputation system, and the treaty does not require it to give credit for Australian corporate tax embedded in dividends.

2. SG Contribution Deduction

Unlike some treaties (e.g., Japan-France), the Australia-Japan treaty does not include a provision allowing residents to deduct mandatory foreign social insurance contributions. This means SG contributions made by your employer while you work in Japan may be treated as taxable employment income with no offsetting deduction.

3. Negative Gearing

The treaty has no provision addressing cross-border rental losses. Australia restricts non-resident loss offsets under domestic law, and Japan’s 2021 reform blocks overseas wooden building depreciation deductions. The treaty cannot override either country’s domestic anti-avoidance provisions in this area.

4. HECS-HELP

HELP debt repayment obligations are a domestic Australian matter entirely outside the treaty’s scope. The treaty does not affect Australia’s right to require overseas residents to report worldwide income for HELP repayment calculation purposes.

5. Medicare Levy

The Medicare Levy and Medicare Levy Surcharge are treated as income tax for some purposes but are not specifically addressed by the treaty. The exemption for non-residents is available under Australian domestic law, not the treaty.

6. CGT 50% Discount

The removal of the CGT discount for non-residents on post-May 2012 assets is an Australian domestic law change. The treaty does not guarantee access to the discount and cannot override this restriction.

Warning

Many Australians assume the tax treaty protects them from all forms of double taxation and unfavorable tax treatment. In reality, the treaty’s scope is limited to allocating taxing rights and reducing withholding rates. Domestic law changes in either country can significantly affect your tax position in ways the treaty does not address.

Section Summary

- NOT covered: franking credits, SG deduction, negative gearing, HECS-HELP, Medicare Levy, CGT discount

- These gaps are significant and can result in unexpected tax costs

- Domestic law changes in either country operate independently of the treaty

Cross-border tax is complex. A bilingual tax accountant can make it manageable.

Frequently Asked Questions

Q: Does the treaty prevent Australia from taxing my Japanese salary?

A: Yes, if you are a Japan tax resident and perform all work in Japan, the treaty allocates the right to tax your employment income exclusively to Japan. Australia should not tax your Japanese salary. However, unlike the US savings clause, Australia’s residency-based taxation means that if you are still considered an Australian tax resident (even while living in Japan), Australia may seek to tax your worldwide income. Establishing non-residency with the ATO is essential.

Q: I hold ASX-listed shares. Will Australia tax my capital gains if I sell while living in Japan?

A: Under the treaty, gains from selling ordinary shares (not shares in a Real Estate Holding Company) are taxable only in the country of residence — Japan. Australia should not impose CGT on these gains. However, you should ensure you have properly established non-residency with the ATO. Note that the CGT 50% discount is not available on shares acquired after May 8, 2012, for non-residents, which affects the Australian side if non-residency is later disputed.

Q: How do I apply for the reduced treaty withholding rate on Australian dividends?

A: For unfranked dividends, you should contact your Australian share registry or broker and provide evidence of your Japan tax residency. They may require a Declaration of Tax Treaty Status or equivalent form. For managed funds, contact the fund manager directly. Some institutions apply treaty rates automatically when they have your overseas address on file; others require a specific request. For franked dividends, no action is needed — the 0% withholding rate applies automatically under Australian domestic law.

Q: Can the Social Security Agreement help me qualify for the Japanese pension?

A: Yes. The Australia-Japan Social Security Agreement allows you to combine Australian and Japanese contribution periods to meet the 10-year minimum requirement for Japan’s National Pension (国民年金). For example, if you have 6 years of Japanese pension contributions and 5 years of Australian employment, the combined 11 years meets the 10-year threshold. Note that the pension amount is calculated based only on actual Japanese contributions — totalization helps you qualify but does not increase the payment amount.