Are you an Australian living in Japan? (For Canadians, see our Canadian Citizens Tax in Japan guide. For Indians, see our Indian Citizens Tax in Japan guide.) From superannuation headaches to franking credit losses to HECS-HELP obligations, here’s everything you need to know about managing your tax obligations across both countries.

Australian Expat Tax Checklist: 4 key obligations

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Australia-Japan cross-border taxation is complex and depends on your specific circumstances. Treaty interpretation can vary between the ATO and Japan’s National Tax Agency (NTA). Always consult qualified professionals — a Japanese tax accountant (zeirishi) and an Australian tax adviser — before making decisions based on treaty provisions.

Quick Summary — Key Points for Australians in Japan

- Australia taxes based on residency (not citizenship) — you can become an Australian non-resident and stop filing Australian income tax returns

- Japan does not recognize Australian franking credits — franked dividends that are tax-free in Australia become fully taxable in Japan at 20.315%

- Superannuation is not specifically covered by the tax treaty — Japan’s NTA treats it as a trust-type retirement savings vehicle

- The Social Security Totalization Agreement works between Australia and Japan — you can combine pension periods

- HECS-HELP debts follow you overseas — new 2025-2026 rules require annual income reporting to the ATO

- CGT 50% discount is not available for non-residents on assets acquired after May 8, 2012

Need a bilingual tax accountant who understands Australia-Japan cross-border tax?

Get matched with a specialist — free.

With over 105,000 Australians living in Japan as of 2025 — and that number growing at 1.4% annually — the Australia-Japan tax relationship has become one of the most important cross-border tax corridors in Asia-Pacific. Whether you came to Japan on a working holiday visa, transferred with your employer, or started a business, your tax obligations span both countries and involve a surprising number of traps for the unwary.

This guide covers every major issue facing Australians in Japan, from the day-to-day (how your salary is taxed) to the strategic (should you keep contributing to super or switch to iDeCo?).

Table of Contents

- Tax Residency: Australia’s Subjective Tests vs Japan’s 5-Year Rule

- Australia-Japan Tax Treaty: What’s Taxed Where

- The Franking Credit Problem

- Superannuation in Japan: The Complete Guide

- Capital Gains: CGT Discount Loss & FRCGW

- Australian Property & Negative Gearing

- HECS-HELP: New Rules for Overseas Residents (2025-2026)

- Medicare Levy Exemption

- Eliminating Double Taxation

- Social Security: Totalization Works!

- FAQ

1. Tax Residency: Australia’s Subjective Tests vs Japan’s 5-Year Rule

The foundation of your tax obligations is tax residency. Unlike the United States (which taxes citizens worldwide regardless of where they live), Australia taxes based on residency. If you can establish that you are an Australian non-resident for tax purposes, you are generally only liable for Australian tax on Australian-sourced income.

Australia’s Four Residency Tests

The ATO uses four statutory tests to determine tax residency. You are a resident if you satisfy any one of them:

- Resides Test — The primary test. Based on the ordinary meaning of “resides in Australia.” Factors include physical presence, family location, economic ties, and intention to return.

- Domicile Test — If your domicile is in Australia, you are a resident unless the ATO is satisfied that your “permanent place of abode” is outside Australia. The landmark Harding v Commissioner of Taxation (2019) case clarified that a permanent place of abode overseas can establish non-residency even if you maintain an Australian domicile.

- 183-Day Test — If you are present in Australia for 183 days or more in a tax year, you are a resident unless you can demonstrate that your usual place of abode is outside Australia and you have no intention of taking up residence.

- Commonwealth Superannuation Fund Test — Applies to Commonwealth government employees contributing to specific super funds. Rarely relevant for private-sector workers.

Key Point

The Australian government has been working on a proposed “bright-line” 183-day test that would replace the subjective tests with a clearer, objective standard. However, as of early 2026, this legislation has not yet been enacted. The current subjective tests remain in force. If you are planning a move to Japan, do not rely on the proposed bright-line test — assess your position under the existing four-test framework.

Japan’s Residency Framework

Japan classifies individuals into three categories for tax purposes:

| Category | Criteria | Taxable Income |

|---|---|---|

| Non-Permanent Resident (NPR) | Foreign national, lived in Japan <5 of past 10 years, no permanent visa | Japan-sourced income + foreign income remitted to Japan |

| Permanent Resident | 5+ years in Japan (of past 10) or permanent visa | Worldwide income |

| Non-Resident | No address/domicile in Japan | Japan-sourced income only |

For a detailed explanation of the 5-year rule and the NPR remittance-based system, see our Japan Tax Residency & 5-Year Rule Guide.

Dual Residency Tie-Breaker

If you are a tax resident of both countries simultaneously, the Australia-Japan Tax Treaty (Article 4) provides tie-breaker rules. These are applied in order: (1) permanent home, (2) centre of vital interests, (3) habitual abode, (4) nationality, and finally (5) mutual agreement between tax authorities.

In practice, most Australians who have moved to Japan with their family, have an apartment or house, and work in Japan will be treated as Japan-resident under the tie-breaker.

Section Summary

- Australia taxes by residency, not citizenship — you can stop being an Australian tax resident

- The four ATO tests are subjective — the proposed bright-line test is not yet law

- Japan’s NPR status gives you up to 5 years of favorable treatment on foreign income

- The treaty tie-breaker resolves dual residency based on permanent home and vital interests

2. Australia-Japan Tax Treaty: What’s Taxed Where

The Agreement between Australia and Japan for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income was signed in 2008 and entered into force on January 1, 2009. It has been further modified by the Multilateral Instrument (MLI), which came into effect for this treaty on January 1, 2019.

For the complete treaty analysis, see our dedicated Australia-Japan Tax Treaty Guide.

Treaty Withholding Rates at a Glance

| Income Type | Treaty Rate | Notes |

|---|---|---|

| Dividends (unfranked, portfolio <10%) | 15% | Standard rate for individual investors |

| Dividends (unfranked, 10%+ ownership) | 5% | Beneficial owner holds 10%+ of voting shares |

| Dividends (unfranked, 80%+ ownership) | 0% | Conditions apply (6-month holding, etc.) |

| Dividends (franked) | 0% | Exempt under AUS domestic law for non-residents |

| Interest | 10% | 0% for government entities |

| Royalties | 5% | — |

Warning

These are the treaty rates — the maximum that Australia can withhold at source. You may need to file a treaty benefit claim with the ATO or your financial institution to receive these reduced rates instead of the default domestic rates.

3. The Franking Credit Problem

This is arguably the single biggest tax surprise for Australians who move to Japan. Australia’s dividend imputation system — where corporate tax paid by a company flows through to shareholders as franking credits — does not translate across borders.

How It Works in Australia

When an Australian company pays a fully franked dividend, it has already paid 30% corporate tax on that profit. Australian resident shareholders receive a franking credit that offsets their personal tax liability. For investors in lower tax brackets, this can even result in a refund of excess franking credits.

What Happens When You Move to Japan

The moment you become a non-resident of Australia for tax purposes, the franking credit benefit disappears in two ways:

- Australia side: Fully franked dividends paid to non-residents are exempt from Australian withholding tax (0% rate) under domestic law. This sounds good — but you can no longer claim a refund of excess franking credits.

- Japan side: Japan does not recognize Australian franking credits. The dividend is treated as ordinary income and taxed at your marginal rate (up to 55.945% including residence tax and surtax). Even the standard 20.315% rate on listed stock dividends applies in full — there is no credit for Australian corporate tax already paid.

Warning

The net result: you receive a dividend that has already been taxed at 30% at the corporate level in Australia, but Japan taxes the full gross amount again. For a fully franked dividend of A$70, the underlying profit was A$100. Australia sees the A$30 corporate tax as the company’s tax and gives you 0% withholding. Japan taxes the A$70 you received (or the A$100 gross-up, depending on reporting) with no credit for the A$30. The total effective tax rate on that profit can exceed 50%.

Practical Strategies

- Review your Australian share portfolio before moving to Japan — consider whether holding high-yield franked dividend stocks still makes sense

- Consider growth-oriented investments that distribute minimal dividends while you are a Japan resident

- If you are still an NPR (first 5 years in Japan), dividends not remitted to Japan may not be taxable — but this is a complex area requiring careful planning

- Consult a cross-border specialist before restructuring investments

Section Summary

- Japan does NOT recognize Australian franking credits

- Fully franked dividends: 0% AUS withholding but fully taxable in Japan

- Total effective tax on franked dividends can exceed 50%

- Portfolio restructuring before the move is strongly recommended

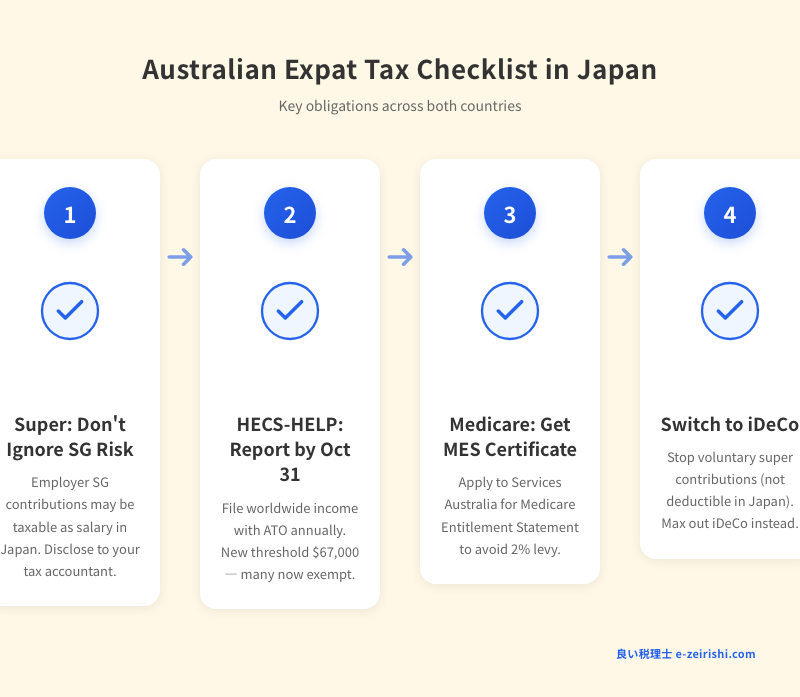

4. Superannuation in Japan: The Complete Guide

Superannuation is the most technically complex area for Australians in Japan. The Australia-Japan Tax Treaty does not explicitly mention superannuation, which creates uncertainty that has significant financial consequences.

How Japan’s NTA Treats Super

Japan’s National Tax Agency treats Australian superannuation as an “insurance-type private retirement savings” vehicle based on its trust structure. This classification determines the tax treatment at each stage:

During Accumulation (While Working in Japan)

This is the relatively good news. Investment gains that accrue inside your superannuation fund are not taxed annually in Japan. Unlike some countries that tax unrealized gains in foreign retirement accounts (notably the US with PFICs), Japan does not require you to report or pay tax on gains within your super fund until withdrawal.

Withdrawal Options and Tax Treatment

| Withdrawal Type | Japan Tax Category | Tax Treatment |

|---|---|---|

| Pension (periodic payments) | Miscellaneous Income (雑所得) | Taxed at marginal income tax rate, with limited deduction |

| Lump sum | Occasional Income (一時所得) | More favorable: subtract contributions, ¥500K deduction, then only 50% of remainder is taxable |

Key Point — Lump Sum Is Better

If you withdraw your super as a lump sum while a Japan tax resident, the tax calculation is: (Total withdrawal − Total contributions − ¥500,000) × 50%. Only this result is added to your taxable income. For a super balance that has grown significantly, this can result in substantially lower tax than periodic pension payments.

The SG Contribution Risk

This is the issue that catches most Australians off guard. If your Australian employer continues to make Superannuation Guarantee (SG) contributions on your behalf while you are working in Japan, Japan may treat those contributions as taxable employment income (給与所得).

Why? The Australia-Japan Tax Treaty does not have a provision that allows deduction of foreign social insurance contributions (unlike, for example, the Japan-France treaty which explicitly permits this). Without such a provision, the NTA’s position is that SG contributions are a form of remuneration — your employer pays money into a fund for your benefit, so it is income.

Warning — Back-Assessment Risk

If you have been working in Japan for several years and have not reported SG contributions as income, the NTA can assess you retroactively for up to 5-7 years. This can result in a significant back-tax bill plus penalties and interest. If your employer is making SG contributions while you work in Japan, consult a tax adviser immediately to assess your exposure.

SMSF (Self-Managed Super Fund) Reporting

If you have a Self-Managed Super Fund (SMSF), be aware that as trustee and beneficiary, the full balance of the fund counts toward the threshold for Japan’s Overseas Asset Report (国外財産調書). If your total overseas assets exceed ¥50 million (approximately A$500,000), you must file this report annually with the NTA by March 15.

For more on overseas asset reporting requirements, see our Overseas Asset Reporting Guide.

iDeCo vs. Voluntary Super Contributions

This is a critical strategic decision. While living in Japan:

| Feature | Voluntary Super Contributions | iDeCo (Japan) |

|---|---|---|

| Tax deductible in Japan? | No | Yes — fully deductible |

| Investment growth taxed? | No (in Australia) | No (in Japan) |

| Accessible before retirement? | Limited (preservation rules) | No (age 60+ only) |

| Annual contribution limit | A$30,000 (concessional) | ¥144,000–¥816,000/year (varies by category) |

Recommendation: Stop making voluntary super contributions while you are a Japan tax resident, and instead maximize your iDeCo contributions. Voluntary super contributions provide no tax benefit in Japan, while iDeCo contributions are fully deductible from your Japanese income tax.

The 6-Month Withdrawal Rule

If you decide to withdraw your super after leaving Australia, timing matters. If you withdraw within 6 months of becoming an Australian non-resident, Australian tax may be exempt on the withdrawal. After 6 months, the “Applicable Fund Earnings” (investment growth since you joined) becomes taxable in Australia, creating potential double taxation with Japan.

Section Summary

- Super is NOT explicitly covered by the tax treaty — NTA treats it as trust-type retirement savings

- Accumulation phase: no annual Japan tax on gains inside the fund

- Lump sum withdrawal gets favorable “occasional income” treatment in Japan

- SG contributions may be treated as taxable employment income — back-assessment risk of 5-7 years

- Stop voluntary super contributions; maximize iDeCo instead

5. Capital Gains: CGT Discount Loss & FRCGW

Two significant changes to Australian tax law have made Australian assets much less attractive for Japan-resident Australians.

Loss of the CGT 50% Discount

Australian resident individuals who hold assets for more than 12 months are entitled to a 50% CGT discount — effectively halving the tax on capital gains. However, for assets acquired after May 8, 2012, this discount is not available to non-residents.

If you became an Australian non-resident after acquiring shares or property, any capital gains on assets acquired after that date will be taxed on the full gain with no discount. Assets acquired before May 8, 2012 retain partial access to the discount through a proportioning method.

FRCGW (Foreign Resident Capital Gains Withholding)

When a foreign resident sells Australian real property with a market value of A$750,000 or more, the purchaser is required to withhold 15% of the purchase price and remit it to the ATO. This is not a final tax — it is a prepayment that is credited against your actual CGT liability when you file your Australian tax return.

However, the cashflow impact is significant. On a A$1.5 million property sale, A$225,000 is withheld at settlement. If your actual CGT liability is lower, you must file an Australian tax return and wait for the refund.

Warning — Japan Also Taxes the Gain

As a Japan tax resident (permanent resident status), you are liable for Japanese tax on your worldwide capital gains, including gains on Australian property. Japan taxes capital gains on real estate at 20.315% (for assets held 5+ years) or 39.63% (for assets held less than 5 years). You can claim a foreign tax credit in Japan for Australian CGT paid, but the credit is limited. See our Capital Gains Tax Guide for details.

Section Summary

- CGT 50% discount lost for non-residents on post-May 2012 assets

- FRCGW: 15% withholding on property sales of A$750K+

- Japan also taxes the gain at 20.315% (long-term) or 39.63% (short-term)

- Foreign tax credit available but limited

6. Australian Property & Negative Gearing

Negative gearing — borrowing to invest in property and deducting the rental loss against other income — is a quintessentially Australian tax strategy. For Japan residents, however, it is now effectively completely neutralized from both sides.

Australia Side

Non-residents can only offset rental losses against Australian-sourced income. If your only Australian income is from a single negatively geared property, the loss cannot be used against your Japanese salary or other foreign income. It carries forward against future Australian income only.

Japan Side

Japan’s 2021 tax reform banned the deduction of depreciation on overseas wooden buildings (the most commonly depreciated type of Australian residential property) against other income. Previously, Japanese tax residents could claim accelerated depreciation on older Australian wooden houses (useful life as short as 4 years for buildings over 22 years old) and offset the resulting paper loss against their Japanese salary income.

This loophole was widely used and was specifically targeted by the reform. The result: even if you have a genuine rental loss on your Australian property, you cannot use the depreciation component to reduce your Japanese tax bill.

Warning

The combined effect of Australian non-resident loss restrictions and Japan’s 2021 depreciation reform means that negative gearing provides no tax benefit in either country for Japan-resident Australians. If you are holding a negatively geared Australian property primarily for tax benefits, the economics have fundamentally changed.

Section Summary

- Australia: non-residents can only offset losses against Australian-sourced income

- Japan: 2021 reform banned depreciation deductions on overseas wooden buildings

- Negative gearing strategy is completely neutralized for Japan residents

7. HECS-HELP: New Rules for Overseas Residents (2025-2026)

If you have an outstanding HECS-HELP (now called HELP) debt, it follows you to Japan. The Australian government significantly reformed the HELP system in 2025-2026, and the changes directly affect overseas residents.

Key Changes (Effective 2025-2026)

| Item | Previous Rule | New Rule (2025-2026) |

|---|---|---|

| Automatic debt reduction | None | 20% reduction applied Jan 1, 2025 |

| Repayment threshold | A$54,435 | A$67,000 |

| Rate structure | Cliff-edge (sudden full percentage) | Marginal rate system (graduated) |

| Filing deadline (overseas) | October 31 | October 31 (unchanged) |

New Marginal Repayment Rates

| Worldwide Income (AUD) | Repayment Amount |

|---|---|

| Under $67,000 | Nil |

| $67,001 – $125,000 | 15 cents per dollar over $67,000 |

| $125,001 – $179,285 | $8,700 + 17 cents per dollar over $125,000 |

| $179,286+ | 10% of total income |

Key Point — Worldwide Income Reporting

Overseas residents must report their worldwide income to the ATO by October 31 each year, even if they have no other Australian tax obligations. Your Japanese salary, investment income, and any other worldwide income must be converted to AUD and reported. Failure to report can result in penalties and interest on your HELP debt.

Practical Impact for Australians in Japan

If your combined worldwide income (Japanese salary, Australian rental income, investment returns) exceeds A$67,000, you will have HELP repayment obligations. With the new marginal rate system, the old “cliff effect” (where earning A$1 over the threshold triggered a full percentage repayment) is eliminated — repayments now increase gradually.

The 20% automatic debt reduction applied in January 2025 means that your current balance may be significantly lower than you expect. Check your balance through myGov before planning any voluntary repayments.

Section Summary

- HELP debt follows you to Japan — overseas reporting mandatory

- 20% automatic debt reduction applied January 2025

- New marginal rate system replaces cliff-edge approach

- Report worldwide income to ATO by October 31 annually

8. Medicare Levy Exemption

Australian tax residents pay a 2% Medicare Levy plus potentially up to 1.5% Medicare Levy Surcharge (if you earn over A$93,000 and don’t have private health insurance). Non-residents who are not entitled to Medicare can claim an exemption from both.

How to Get the Exemption

- Obtain a Medicare Entitlement Statement (MES) from Services Australia. This confirms that you are not entitled to Medicare benefits.

- Apply via myGov — link your myGov account to Medicare, then request the MES online. Processing takes up to 8 weeks.

- Select “Exemption Category 2 (Foreign resident)” in your Australian tax return.

- Keep the MES — the ATO may request it to verify your exemption claim.

Warning — Apply Early

The MES application can take up to 8 weeks to process. If you need it for your Australian tax return, apply well before the filing deadline. You cannot claim the exemption without the MES.

Section Summary

- Non-residents not entitled to Medicare can claim exemption from the 2% levy + 1.5% surcharge

- Obtain a Medicare Entitlement Statement (MES) via myGov — allow 8 weeks

- Select Category 2 (Foreign resident) in your tax return

9. Eliminating Double Taxation

When the same income is taxed by both Australia and Japan, you need to use the available relief mechanisms to avoid paying tax twice. The two main tools are:

ATO Side: Foreign Income Tax Offset (FITO)

If you remain an Australian tax resident (or have Australian-sourced income that is also taxed in Japan), you can claim a Foreign Income Tax Offset (FITO) in your Australian tax return. The FITO is limited to the amount of Australian tax payable on that income — you cannot get a refund of Japanese tax through the FITO.

For FITO claims of A$1,000 or less, you can claim the offset without calculating the limit. For amounts over A$1,000, you must calculate the foreign income tax offset limit.

Japan Side: Foreign Tax Credit (外国税額控除)

If you are a Japan tax resident and have paid tax in Australia, you can claim a foreign tax credit in your Japanese tax return. The credit is limited to the lesser of:

- The actual foreign tax paid, OR

- The Japanese tax attributable to that foreign income (calculated by formula)

Warning — Treaty Rate Limit

Japan only credits foreign tax up to the treaty rate. If your Australian bank withholds interest at the domestic rate of 30% instead of the treaty rate of 10%, Japan will only give you a credit for 10%. The remaining 20% is wasted. Always ensure your Australian financial institutions apply the correct treaty withholding rates. See our Foreign Tax Credit Guide for the full calculation method.

For a comprehensive overview of double taxation mechanisms across multiple countries, see our Double Taxation Guide.

Section Summary

- ATO: Foreign Income Tax Offset (FITO) — limited to Australian tax on that income

- Japan: Foreign tax credit — limited to treaty rates

- Ensure Australian institutions apply treaty withholding rates to avoid wasted credits

10. Social Security: Totalization Works!

Unlike some other bilateral relationships (notably the UK-Japan treaty, which does not include totalization), Australia and Japan have a Social Security Agreement that entered into force in 2009. This is excellent news for Australians building careers in Japan.

What Totalization Means

The agreement allows you to combine pension contribution periods in both countries to meet eligibility requirements:

- Japan’s National Pension (国民年金): Requires 10 years (120 months) of contributions. Your Australian working periods can be counted toward this requirement.

- Australia’s Age Pension: Requires minimum 10 years of Australian residence (with at least 6 continuous months). Your Japanese pension periods can be counted toward the residence requirement.

Dual Coverage Prevention

If you are sent to Japan by your Australian employer (a “posted worker”), you may be exempt from Japanese social insurance contributions for up to 5 years. You need a Certificate of Coverage from the ATO to prove your coverage under the Australian system.

Warning — Self-Employed Not Covered

The dual coverage prevention provisions do not apply to self-employed individuals. If you are self-employed in Japan, you must contribute to Japan’s National Pension system regardless of any Australian superannuation arrangements.

Claiming Australian Age Pension from Japan

If you qualify for the Australian Age Pension while living in Japan, be aware that it is subject to the income and assets test. Your Japanese income and assets (including Japanese real estate, savings, and pension entitlements) are counted in the assessment. The pension amount may be reduced or eliminated based on your total means.

You must have at least 12 months of Australian residence (including at least 6 continuous months) to qualify for the Age Pension from overseas.

Section Summary

- Australia-Japan Social Security Agreement includes totalization — pension periods can be combined

- Posted workers: exempt from Japan social insurance for up to 5 years with Certificate of Coverage

- Self-employed: NOT covered by dual coverage provisions

- Age Pension from Japan: subject to income & assets test (Japanese assets count)

Navigating Australia-Japan tax is complex. A bilingual tax accountant can help.

Frequently Asked Questions

Q: Do I need to file an Australian tax return if I am living in Japan?

A: It depends on your Australian tax residency status and income sources. If you are an Australian non-resident for tax purposes and have no Australian-sourced income, you generally do not need to file an Australian income tax return. However, if you have HECS-HELP debt, you must report your worldwide income to the ATO by October 31 regardless of your residency status. If you have Australian rental income, bank interest, or capital gains, you will need to file.

Q: Can I access my superannuation early because I have left Australia?

A: Permanent residents and citizens of Australia generally cannot access their super early just because they moved overseas. Early access on the grounds of departing Australia permanently is only available to temporary visa holders (the Departing Australia Superannuation Payment, or DASP). If you are an Australian citizen or permanent resident, your super remains locked until you meet a condition of release (typically reaching preservation age of 60).

Q: How do I handle Australian rental income in my Japanese tax return?

A: As a Japan tax resident (permanent resident status), you must report Australian rental income as worldwide income in your Japanese tax return. The income is reported in Japanese yen, converted at the average exchange rate for the period. You can deduct related expenses (mortgage interest, management fees, council rates, repairs). Any Australian tax withheld or paid on the rental income can be claimed as a foreign tax credit in Japan. Note that depreciation on overseas wooden buildings cannot be deducted against other income under the 2021 reform.

Q: Should I notify the ATO when I move to Japan?

A: Yes. You should update your residency status with the ATO when you leave Australia. This is done through your tax return by indicating the dates you were a resident and non-resident during the tax year. You should also update your address with the ATO, cancel or suspend your Medicare enrolment (and obtain the MES for levy exemption), and notify your super fund of your overseas address. If you have HELP debt, ensure you understand the overseas reporting requirements.