If you’re a Canadian living in Japan — or a Japan-resident foreigner earning Canadian dividends, pension benefits, or rental income — the Canada-Japan Income Tax Convention is the single most important document for your tax planning. It determines whether your dividends are taxed at 25% or 15%, whether your RRSP withdrawal gets a treaty rate, and which country has the right to tax your CPP and Old Age Security. This guide explains the treaty in practical terms, including the gaps that catch Canadians off-guard.

This is a long-form guide focused on individuals, not corporations. If you’re an investor structuring a Canada-Japan business, the rules differ — book a consultation. But if you’re a person who moved here, retired here, or kept Canadian financial roots, this article is for you.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. The Canada-Japan tax treaty interacts with both Canadian and Japanese domestic law, and every individual’s situation differs. Always engage a tax professional licensed in both jurisdictions (or coordinated cross-border tax accountants) before relying on treaty positions.

Canadian with Japan tax questions?

Get matched with a Japan tax accountant experienced in Canada-Japan cross-border issues — free.

Table of Contents

- Who Should Read This Canada-Japan Tax Guide

- The Canada-Japan Tax Treaty: Background & Scope

- Canada-Japan Treaty Residency: Tie-Breaker Rules

- Canada-Japan Treaty Withholding: Dividends, Interest, Royalties

- Pensions and the Treaty Gap: CPP, OAS, RRSP

- Capital Gains: Canadian and Japanese Assets

- TFSA in Japan: Why the “Tax-Free” Status Doesn’t Travel

- The Japan-Canada Social Security Agreement

- How to Claim Canada-Japan Treaty Benefits

- Common Canada-Japan Treaty Mistakes

- Canada-Japan Tax Treaty FAQ

- Get Expert Help With Canada-Japan Tax

1. Who Should Read This Canada-Japan Tax Guide

This guide is written for one or more of the following situations:

- You are a Canadian citizen or former Canadian resident who now lives in Japan and still receives Canadian-source income (dividends, RRSP distributions, CPP, OAS, rental income from Canadian property, etc.).

- You are a Japan-resident foreigner (any nationality) who owns Canadian investment assets — a Canadian brokerage account, RRSP, Canadian REITs, or shares of Canadian corporations.

- You are planning to move from Canada to Japan and need to understand which Canadian assets will trigger departure tax, ongoing Canadian withholding, or Japanese taxation upon arrival.

- You are a Canadian short-term assignee or working-holiday participant in Japan who needs to know whether you’ll be taxed by Japan, Canada, or both.

- You are a tax professional handling a Canada-Japan cross-border file and want a clean starting reference for the treaty’s individual provisions.

If none of the above applies, you probably don’t need treaty analysis — a general guide on Japan tax residency rules or double taxation basics will serve you better.

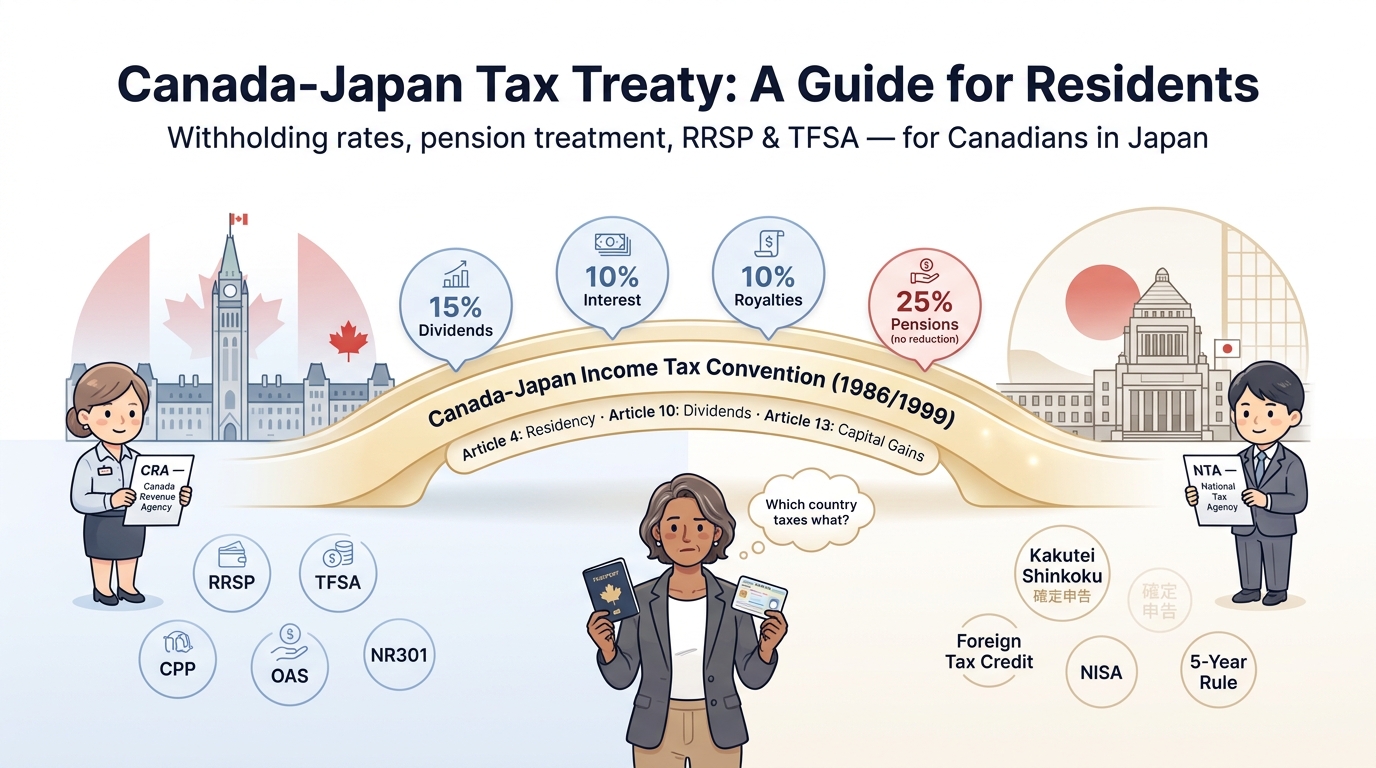

2. The Canada-Japan Tax Treaty: Background & Scope

The formal name is the Convention between Canada and Japan for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with Respect to Taxes on Income, signed in 1986 with a major amending protocol in 1999. The treaty was further updated by the Multilateral Instrument (MLI), which Japan and Canada both ratified — the MLI provisions apply to the Canada-Japan treaty for tax years beginning on or after the respective entry-into-effect dates.

What the Treaty Does

Like all bilateral tax treaties, the Canada-Japan treaty does two main things:

- Allocates taxing rights between the two countries for specific income types (employment, business profits, dividends, interest, royalties, capital gains, pensions, etc.).

- Reduces withholding taxes on cross-border passive income (dividends, interest, royalties), provided the income recipient meets the treaty’s beneficial-owner and residency tests.

The treaty does not exempt anyone from filing — both countries still apply their domestic income tax to their own residents on their worldwide income. The treaty just prevents you from being taxed twice on the same dollar.

What the Treaty Does NOT Cover

This is the trap that surprises Canadian retirees in Japan the most:

- The treaty does not have a specific pension article the way the Canada-US treaty does. CPP, OAS, and most private Canadian pensions paid to Japan residents fall back on Canada’s default 25% non-resident withholding rate.

- The treaty does not recognize TFSA or RRSP as tax-deferred in Japan. Japan taxes investment income inside these accounts under domestic rules.

- The treaty does not cover social security contributions — that’s the separate Japan-Canada Social Security Agreement (2008), discussed in Section 8.

- The treaty does not cover provincial income tax in Canada (Quebec, Ontario, etc.), though provincial tax for non-residents is generally not an issue once you’ve established non-resident status with Canada Revenue Agency.

3. Canada-Japan Treaty Residency: Tie-Breaker Rules

Before any treaty article can apply to you, you must be a “resident of a Contracting State” as defined in Article 4. Article 4 also provides tie-breaker rules for individuals who could be considered a resident of both Canada and Japan under each country’s domestic law.

Japan’s Domestic Residency Test

Japan considers you a tax resident if you have a jūsho (主たる生活の本拠地, “primary base of living”) in Japan, or if you have been physically present in Japan with a kyosho (居所, ordinary residence) for one year or more. Most foreigners on long-term visas become Japan tax residents from day one if they intend to stay.

For details on Japan’s residency framework, including the non-permanent resident sub-status that applies to the first 5 of 10 years, see our Japan tax residency 5-year rule guide.

Canada’s Domestic Residency Test

Canada uses a multi-factor “residential ties” test (primary ties: home in Canada, spouse/common-law partner in Canada, dependents in Canada) plus deemed residency if you spent 183+ days in Canada in a year. A common pitfall: simply leaving Canada does not automatically make you a non-resident — you usually need to formally sever ties by selling or renting out your home, closing significant accounts, etc.

The Article 4 Tie-Breaker

If both Canada and Japan claim you as a tax resident under domestic law, the treaty’s tie-breaker rules apply in this order:

- Permanent home — In which country do you have a permanent home available to you? If only one, that’s your treaty residence.

- Centre of vital interests — If permanent homes exist in both, where are your personal and economic ties strongest (family, job, social, banking)?

- Habitual abode — If still unclear, where do you habitually live (count days)?

- Nationality — Final tie-breaker.

- Mutual agreement — If none of the above resolves it, Canada and Japan’s competent authorities decide.

For most Canadians who genuinely relocated to Japan, the tie-breaker confirms Japan residence — but only if you actually closed your Canadian primary residence and don’t return for extended stays.

4. Canada-Japan Treaty Withholding: Dividends, Interest, Royalties

This is where the treaty most often saves Canadians in Japan real money. Without the treaty, Canada applies a flat 25% non-resident withholding tax on passive income paid to non-residents. The treaty cuts most of these in half or more.

Treaty Withholding Rate Table

| Income Type | Statutory Rate (No Treaty) | Canada-Japan Treaty Rate |

|---|---|---|

| Dividends (portfolio) | 25% (Canada) / 20.42% (Japan) | 15% |

| Dividends (≥10% voting stock) | 25% / 20.42% | 5% |

| Interest | 25% / 20.42% | 10% |

| Royalties | 25% / 20.42% | 10% |

| Pensions (general) | 25% | 25% (no treaty reduction) |

Source: Canada-Japan Income Tax Convention as amended; Canada Revenue Agency Information Circular IC76-12R. Rates current as of 2026.

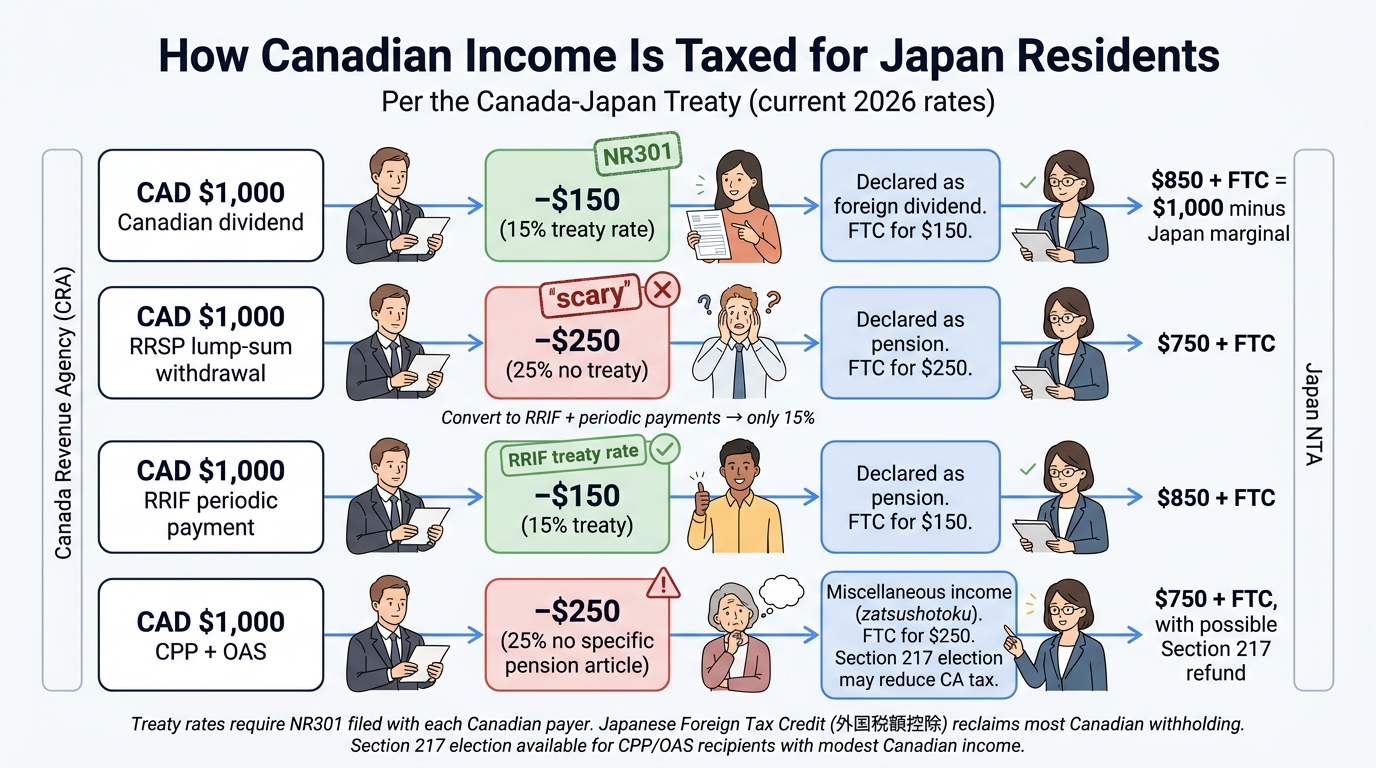

A Practical Example: Canadian Dividends Paid to a Japan Resident

You hold 500 shares of a Canadian dividend-paying stock in your Canadian brokerage account. The company pays CAD 1,000 in dividends to you for the year. What happens?

- Without the treaty: Canada withholds 25% = CAD 250, you receive CAD 750.

- With the treaty (you correctly claimed Japan residency on Form NR301): Canada withholds 15% = CAD 150, you receive CAD 850.

- Japan side: You declare the full CAD 1,000 dividend on your Japan tax return as foreign-source dividend income. Japan taxes you at marginal rates (potentially 20% if you elect separate taxation, or your normal income tax bracket if you elect aggregate taxation).

- Foreign tax credit: You claim a Japanese foreign tax credit for the CAD 150 already withheld by Canada, eliminating double taxation.

For deeper coverage of the Japanese-side Foreign Tax Credit mechanics, see our Foreign Tax Credit in Japan guide.

5. Pensions and the Treaty Gap: CPP, OAS, RRSP

The Canada-Japan tax treaty has an unusual feature among modern Canadian tax treaties: it does not include a specific pension article. The Canada-US treaty has Article XVIII (Pensions and Annuities) that caps US withholding at 15% on periodic pension payments to Canadians and vice versa. The Canada-Japan treaty has no equivalent.

What This Means for CPP and OAS Recipients in Japan

The default rule applies: Canada withholds 25% from CPP and OAS payments sent to a Japan-resident recipient. Japan also taxes the gross CPP/OAS as miscellaneous income. The Japanese foreign tax credit normally absorbs the 25% Canadian withholding, but there are timing and ceiling issues if your Japanese marginal rate is lower.

There is one important workaround for OAS specifically: you can apply to Canada Revenue Agency under Section 217 of the Income Tax Act to elect that your OAS (and certain other Canadian-source income) be taxed as if you were a Canadian resident, with personal credits applied. For Canadians with limited other Canadian income, this can reduce the effective Canadian tax on OAS to well below 25%. Filing is annual and via the standard Section 217 election form.

RRSP and RRIF Withdrawals from Japan

A Canadian RRSP (Registered Retirement Savings Plan) held by a Japan-resident former Canadian is subject to Canadian non-resident withholding tax on every withdrawal. The withholding rate depends on whether you take a lump sum or periodic payments:

- Lump-sum RRSP withdrawal: 25% Canadian withholding (no treaty reduction).

- RRIF (Registered Retirement Income Fund) periodic payments: If you first convert your RRSP into a RRIF and take only “periodic” payments — defined under the treaty rules as not exceeding the greater of (a) twice the minimum required RRIF amount or (b) 10% of the RRIF fair market value at the start of the year — Canada applies a reduced withholding rate. The Canada-Japan treaty does not have an explicit periodic-pension rate, but the standard 15% rate from Canada’s tie-treaty rules typically applies for periodic payments.

For Canadians in Japan with significant RRSP balances, this conversion-then-periodic-payment strategy commonly cuts effective Canadian withholding from 25% to 15% — a 10-percentage-point saving on potentially decades of withdrawals. Specialist tax accountants experienced in cross-border retirement planning are essential here. Errors during the RRSP-to-RRIF conversion can disqualify the periodic treatment.

Japan-Side Tax on RRSP and RRIF

Japan does not recognize RRSPs or RRIFs as tax-deferred vehicles. From the Japanese tax authority’s perspective, dividends, interest, and capital gains inside the RRSP/RRIF are technically taxable annually for a Japan-resident account holder. In practice, NTA enforcement on this point is inconsistent because the income is not reported by Canadian financial institutions to Japan. Many Japan-resident Canadians treat RRSP/RRIF as effectively deferred until withdrawal — but this is a legal grey area, and the conservative position (mirroring the IRS’s old, now-relaxed approach to Canadian RRSPs) is to declare annual investment income inside the RRSP on your Japanese return. Discuss this position with your Japan tax accountant before filing.

6. Capital Gains: Canadian and Japanese Assets

Article 13 of the Canada-Japan treaty allocates taxing rights on capital gains. The general rule for individuals: capital gains from the sale of most types of property are taxed only in the country of residence of the seller (Japan, for a Japan-resident Canadian). There are two important exceptions for Canadians:

Exception 1: Canadian Real Property

Gains from selling Canadian real estate (your old Toronto condo, a Vancouver investment property, BC land) remain taxable in Canada under Article 13(1), regardless of your move to Japan. As a non-resident, Canada applies a 25% withholding tax on the gross sale price (Section 116 withholding) until you obtain a clearance certificate, after which the actual gain is taxed at your marginal Canadian non-resident rates. Japan will then also tax the same gain, but with a foreign tax credit for Canadian tax paid.

Exception 2: Departure Tax (Deemed Disposition)

The day you cease to be a Canadian tax resident, Canada applies a “deemed disposition” — meaning you are treated as if you sold all your taxable Canadian property at fair market value on your departure date. Capital gains tax is owed in your final Canadian tax return.

Exemptions from the deemed disposition include: Canadian real property, RRSP/RRIF/TFSA accounts, and a few specific property types. But other taxable assets — shares in non-RRSP brokerage accounts, foreign investments — get marked to market. For Canadians with appreciated brokerage portfolios, this can be a substantial one-time tax bill timed to your move.

You can elect to defer the departure tax by posting security with Canada Revenue Agency, but this is administratively complex and is best discussed with a Canadian cross-border tax accountant before your move date.

Capital Gains from Japanese Property Sales

If you’re a Japan-resident Canadian and sell Japanese real estate or Japanese stocks, the gain is taxed in Japan (your country of residence) under domestic Japanese rules. Canada generally has no claim on these gains under Article 13.

For specifics on Japanese capital gains taxation of foreign residents, see our Capital Gains Tax in Japan guide.

7. TFSA in Japan: Why the “Tax-Free” Status Doesn’t Travel

This is one of the most frequently misunderstood points for Canadians in Japan.

A TFSA (Tax-Free Savings Account) is tax-free only under Canadian law. Japan does not recognize TFSAs as tax-exempt. From a Japan-resident perspective:

- Investment income earned inside your TFSA (dividends, interest, capital gains realized inside the account) is technically taxable in Japan on your Japanese tax return.

- TFSA contributions made while you are a non-resident of Canada are subject to a 1% per month penalty tax in Canada — even though no Canadian tax accrues on the income itself.

- TFSA withdrawals are not taxed by Canada, but are not exempt from Japanese taxation on the underlying income.

Practical Implications

For most Canadians moving to Japan, the rational TFSA strategy is:

- Stop contributing to your TFSA the moment you cease Canadian residency — the 1% monthly penalty makes new contributions immediately uneconomic.

- Decide whether to hold or close the existing TFSA. Holding it triggers Japanese annual taxation of investment income; closing it crystallizes positions but eliminates the ongoing reporting headache.

- If you stay, switch tax-efficient saving to Japan’s NISA (Nippon Individual Savings Account). NISA is Japan’s tax-free investment account, with annual contribution limits and a permanent tax-free wrapper for qualifying accounts. NISA is the actually tax-free Japanese equivalent of TFSA for Japan residents.

RESP and RDSP Considerations

Similar issues apply to Registered Education Savings Plans (RESP) and Registered Disability Savings Plans (RDSP). Japan does not recognize the tax-deferred status of either. Most Canadians in Japan with existing RESPs/RDSPs continue to hold them but should declare investment income annually on Japanese returns and seek professional advice on the optimal closure strategy if the beneficiaries are not expected to return to Canada.

8. The Japan-Canada Social Security Agreement

Separate from the tax treaty, Canada and Japan have a Social Security Agreement (SSA) in force since March 1, 2008. The SSA covers two Canadian programs (CPP and OAS) and Japan’s public pension system (Kōsei Nenkin / Kokumin Nenkin). It does not cover Canadian Employment Insurance or Japanese health insurance.

What the SSA Does

The SSA provides three practical benefits:

- Pension contribution exemption (detached workers). If you are sent from Canada to work in Japan for up to 5 years by a Canadian employer (or self-employed under specific conditions), you can obtain a Canadian Certificate of Coverage from CRA, and you are exempt from Japanese pension contributions. You continue contributing only to CPP. The same works in reverse for Japanese-employer postings to Canada.

- Totalization for benefit eligibility. Canadian pension periods can be added to Japanese coverage periods (and vice versa) to qualify you for benefits in either country. This matters most for people who worked partial careers in both countries.

- Health insurance carve-out. The Canada SSA exempts you only from pension insurance — you still need to enroll in Japan’s National Health Insurance or Employee Health Insurance.

The Detached-Worker 5-Year Limit

The standard detached-worker exemption runs for up to 5 years. If you need to stay longer because of unforeseen circumstances, you may apply for an extension of up to 3 additional years subject to individual examination by both countries’ authorities.

For workers who plan to stay in Japan permanently or beyond the 5-year detached period, the SSA does not exempt you from Japanese pension contributions long-term. You will need to enroll in Japan’s pension system and may later either claim a lump-sum withdrawal (if you leave Japan) or coordinate benefits through the SSA totalization rules.

For details on Japan’s pension lump-sum refund process for departing foreign workers, see our Japan pension lump-sum withdrawal and tax refund guide.

9. How to Claim Canada-Japan Treaty Benefits

Treaty benefits don’t apply automatically. You usually need to declare your treaty status proactively to both Canadian and Japanese tax administrations and payers.

On the Canadian Side: Form NR301

To get the reduced treaty withholding on Canadian-source income, you must provide your Canadian payer (your broker, your former employer, the RRSP/RRIF custodian) with a completed Form NR301 — Declaration of Eligibility for Benefits Under a Tax Treaty for a Non-Resident Taxpayer. This form certifies that you are a tax resident of Japan and the beneficial owner of the income. Without NR301 on file, payers default to the 25% statutory rate.

Common timing issues:

- NR301 should be filed before the first treaty-rate payment. Over-withholding before NR301 is on file requires you to file a separate NR7-R refund claim with CRA.

- NR301 must be refreshed periodically — typically every 3 years, or whenever your residency status changes.

- For multiple Canadian payers (broker, ex-employer, etc.), you need NR301 on file with each one.

On the Japanese Side

Japan does not have an equivalent of NR301 for inbound foreign-source income. Instead, you report all Canadian-source income on your annual Japanese tax return (確定申告) and claim a foreign tax credit (外国税額控除) for Canadian tax withheld. You’ll need to convert all amounts to JPY using the appropriate exchange rate (NTA publishes guidance on acceptable rates).

For income types where Japan is the source country and Canada is taxing your gross income (rare for individuals), you may need to file a treaty application with NTA — but for the typical Canadian-in-Japan profile, this is not required.

Documentation to Keep

Both CRA and NTA may request supporting documentation in audits. Keep:

- Copies of NR301 filings with each Canadian payer

- Canadian T-slips (T4A, T4RIF, T5, T3, NR4) showing income and withholding amounts

- Japanese tax returns showing the foreign income declared and foreign tax credit claimed

- Proof of Japanese residency (residence card, juminhyo, lease/ownership documents)

- For RRSP/RRIF, periodic-payment calculation worksheets

10. Common Canada-Japan Treaty Mistakes

From observed real-world cases, the most frequent Canada-Japan tax mistakes for individuals are:

Mistake 1: Not Filing the NR73 / Not Severing Canadian Residency

Canadians who move to Japan but don’t formally file a Form NR73 — Determination of Residency Status (Leaving Canada) with CRA risk being treated as a Canadian tax resident on worldwide income. Even if you don’t file NR73 (it’s optional), you should at minimum file a Canadian tax return for your departure year that clearly indicates your date of emigration, sever significant residential ties, and stop receiving Canadian-resident-only benefits (like provincial healthcare cards). The NR301 treaty form does not by itself sever residency.

Mistake 2: Not Realizing the Departure Tax

Many Canadians moving to Japan are surprised by the deemed disposition rules. Stock portfolios held in non-registered Canadian accounts are marked to market on departure day, triggering capital gains tax in your final Canadian return. Planning the disposition timing — possibly realizing gains pre-departure when your Canadian marginal rate is favorable, or deferring with security posted — can save significant amounts.

Mistake 3: Continuing to Contribute to TFSA

Many Canadians don’t realize that TFSA contributions made while a non-resident incur a 1% per month penalty in Canada — and the income earned inside the TFSA is also potentially Japan-taxable. Stop TFSA contributions the moment you cease Canadian residency.

Mistake 4: Lump-Sum RRSP Withdrawal Without Considering RRIF Conversion

Canadian non-residents who pull a full RRSP balance as a single lump sum pay 25% Canadian withholding — irreversibly. Converting first to a RRIF and drawing periodic payments typically reduces withholding to 15%, which on a CAD 200,000 RRSP saves CAD 20,000+ over time. The conversion is administratively straightforward but must be done correctly.

Mistake 5: Not Claiming the Japanese Foreign Tax Credit

Some Canadians-in-Japan don’t claim the foreign tax credit (外国税額控除) on their Japanese return for Canadian withholding tax already paid on dividends, interest, or pensions. This is straightforward double taxation — and it’s avoidable simply by filling in the foreign tax credit section of the Japanese return with the supporting Canadian T-slips and NR4 forms.

Mistake 6: Skipping the Section 217 Election on OAS

For Canadians-in-Japan with modest other Canadian income, electing under Section 217 of Canada’s Income Tax Act lets you be taxed on certain Canadian-source income (including OAS) as if you were a Canadian resident, with personal tax credits applied. This can drop effective Canadian tax on OAS well below the 25% non-resident withholding default. The election is annual.

Mistake 7: Ignoring the Treaty Beneficial-Owner Test

If you hold Canadian assets through a nominee, an intermediary, or a corporation, the treaty benefits flow only to the beneficial owner. Direct ownership in your own name is the cleanest. Indirect structures need careful analysis to confirm treaty access.

11. Canada-Japan Tax Treaty FAQ

Q1: I’m a Canadian who just moved to Japan. Do I file Canadian tax returns from now on?

You file a final-year Canadian return covering January 1 through your departure date as a Canadian resident, and your worldwide income for that period. After your departure date, you file Canadian returns only if you have Canadian-source income (Canadian rental property, dividends, RRSP/RRIF withdrawals, CPP/OAS) and only on that Canadian-source income. Most year-2 onward Canadians-in-Japan file a non-resident Canadian return (or none if all withholding is final) plus a full Japanese tax return.

Q2: Does the Canada-Japan treaty cover provincial tax?

The treaty primarily covers federal income tax. Provincial taxes (Ontario, Quebec, BC, etc.) apply only if you are a tax resident of that province. Once you have established Japanese residency and severed Canadian residential ties, you are generally no longer a resident of any Canadian province for provincial tax purposes (Quebec has some special rules). So in practice, the federal-only scope is not a real issue for individuals who genuinely moved abroad.

Q3: Can I keep my Canadian bank account after moving to Japan?

Yes, but you should notify the bank of your non-resident status. They will switch your account to a non-resident account and apply 25% withholding (or treaty rate if NR301 is on file) on Canadian-source interest. Many Canadians keep a small Canadian bank account for receiving CPP/OAS payments and managing remaining Canadian financial affairs.

Q4: I’m on a working holiday visa in Japan. Am I a Japan tax resident?

Working-holiday visa holders are generally treated as Japan tax residents from arrival if they live in Japan with a fixed base for the duration of the program. However, the short-stay nature means many working-holiday participants remain Canadian tax residents under Canada’s residential ties test (no Canadian home rented out, no spouse abroad). In that case, the Article 4 tie-breaker determines treaty residence. For most working-holiday participants, the practical treatment is to file as a Japan resident on Japanese-source income and continue Canadian-resident filing on worldwide income, claiming a Japan foreign tax credit on the Canadian return.

Q5: My Canadian broker requires a US W-8BEN. Don’t I need a Japanese equivalent?

For Canadian payers paying you Canadian-source income, the relevant form is Canada’s NR301, not the US W-8BEN. The W-8BEN is for US-source income paid to non-US persons — relevant if you hold US stocks in a Canadian or Japanese brokerage account, but not for the Canada-Japan treaty itself.

Q6: Do I need to report my RRSP balance to NTA each year?

If your total overseas financial assets exceed JPY 50 million at year-end, you must file Japan’s Overseas Assets Statement (国外財産調書). This includes RRSP balances, Canadian brokerage holdings, and Canadian real estate. Even below the threshold, the income inside the RRSP is technically reportable on your Japanese tax return for a Japan resident. See our Overseas Asset Reporting in Japan guide.

Q7: Is the treaty rate automatic, or do I have to apply each year?

For Canadian withholding, NR301 is on-file with each Canadian payer and renews every 3 years (or sooner if your residency changes). You don’t re-apply every year. For Japanese foreign tax credit, you claim it on each annual Japanese tax return based on actual Canadian withholding paid in that year.

Q8: What if my Canadian source income is just CPP and OAS — is it worth the paperwork?

For Canadians in Japan receiving only modest CPP/OAS amounts, the standard 25% non-resident withholding often ends up as their only Canadian tax (no Canadian return required). On the Japan side, you declare gross CPP/OAS as miscellaneous income and claim the 25% Canadian tax as a foreign tax credit. Section 217 election on OAS is usually worth running the numbers for — if your total Canadian-source income is below the Canadian basic personal amount thresholds, Section 217 can refund some or all of the 25% withholding.

12. Get Expert Help With Canada-Japan Tax

The Canada-Japan tax interface has more grey areas than most major treaty pairs — pension treatment, RRSP/TFSA recognition, departure-tax timing, Section 217 elections. The right professional is a tax accountant who understands both countries’ rules, or a coordinated team of one Canadian cross-border accountant and one Japanese tax accountant.

TaxMatch Japan introduces Canadians (and Canadian-asset-holding Japan residents of any nationality) to Japan tax accountants who have handled multiple Canada-Japan files. Initial introductions are free.

Common engagement profiles include:

- Pre-move planning: Optimize departure timing, deemed-disposition exposure, RRSP/RRIF setup.

- First Japanese tax return after arrival: Foreign tax credit setup, NR301 with Canadian payers, overseas asset reporting.

- Ongoing annual filings: Canadian non-resident returns coordinated with Japanese annual filings.

- Pre-retirement planning: RRSP/RRIF conversion, CPP/OAS election analysis (Section 217), residency-status review.

Free Matching for Canada-Japan Tax Cases

Tell us your situation and we’ll match you with a Japan tax accountant experienced in Canada-Japan files. No fees, no obligation.

Prefer WhatsApp? Message us at +81 80-6075-2063

Related Guides

Canadian Citizens Tax in Japan

TFSA, RRSP, CPP — the citizen-side complete guide

Double Taxation in Japan

Treaty relief across major Canada/US/UK/India scenarios

Foreign Tax Credit in Japan

Claiming the FTC against Canadian withholding tax

Japan Tax Residency Rules

The 5-year non-permanent resident framework explained

Leaving Japan Tax Checklist

If you later head back to Canada or onward — exit-side checklist