You’re a Canadian who has moved to Japan, is planning to move, or already lives here and is finally tackling the tax side. The mechanics are different from the Canadian-only world you knew — Japan taxes your worldwide income, Canada keeps a claim on Canadian-source dollars, and your TFSA stops being tax-free the moment your plane lands. This is the citizen-focused companion to our Canada-Japan Tax Treaty Guide: less about treaty mechanics, more about what you actually do, in what order, and which mistakes to avoid as a Canadian living in Japan.

If you want the treaty-article-by-article version, start with the treaty guide. This article is the practical decision-tree.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Canada-Japan cross-border tax issues are technical and individual fact patterns vary widely. Engage a tax professional with cross-border experience before acting on any of the strategies discussed.

Canadian living in Japan with tax questions?

Get matched with a Japan tax accountant experienced in Canadian client files — free.

Table of Contents

- Who This Canadian-in-Japan Guide Is For

- Becoming a Japan Tax Resident as a Canadian

- Year One: The Canadian Exit Return + Japanese Arrival Return

- TFSA, RRSP, RRIF: What Happens When You Leave Canada

- CPP & OAS for Canadian Retirees in Japan

- Canadian Rental Property from Japan: Section 216

- Departure Tax: Planning the Deemed Disposition

- Section 217 Election: When It Saves Canadians Money

- Annual Filing Calendar for Canadians in Japan

- Common Pitfalls for Canadians in Japan

- FAQ: Canadian Citizens Tax in Japan

- Get Expert Help for Canadians in Japan

1. Who This Canadian-in-Japan Guide Is For

This guide assumes one or more of the following:

- You’re a Canadian citizen or permanent resident who has moved (or is moving) to Japan on a long-term visa — work visa, spouse visa, intra-company transfer, business manager, or HSP (Highly Skilled Professional).

- You’re a Canadian retiree who has settled in Japan and receives Canadian pensions (CPP, OAS, OMERS, Public Service, military, or private RRSP/RRIF withdrawals).

- You’re a Canadian working remotely in Japan for a Canadian employer or as a self-employed contractor with Canadian clients.

- You’re a Canadian on a working holiday or short-term contract who has stayed long enough to wonder about residency.

- You’re the spouse or partner of a Canadian in any of the above situations and need to understand the household tax picture.

If you’re not Canadian but your spouse is, this guide is still useful — Japan taxes each spouse individually, so your Canadian partner’s filings affect household cash flow but not your own return.

What This Guide Does Not Cover

- Canadian corporate tax issues — running a Canadian corporation from Japan triggers complex permanent-establishment, controlled-foreign-corporation, and FAPI rules that need bespoke advice.

- Quebec-specific tax — Quebec residents file a separate provincial return. Most Quebec departures resolve cleanly to non-resident status on emigration, but if you maintain Quebec ties, get specialist advice.

- US-Canada-Japan triangular cases — Canadians who are also US citizens or Green Card holders face a third layer of US filing obligations. See our US Citizens Tax in Japan complete guide.

2. Becoming a Japan Tax Resident as a Canadian

Japan determines tax residency based on jūsho (primary base of living) and kyosho (ordinary residence of at least one year). For most Canadians moving to Japan on a long-term visa, the practical effect is:

- From your arrival date, you are typically treated as a Japan tax resident, provided you intend to stay.

- For your first 5 of 10 years in Japan, you may qualify as a non-permanent resident — a sub-status that excludes foreign-source income from Japanese taxation unless remitted to Japan. This is the most important early-years tax planning opportunity for new arrivals.

- From year 6 onward (or earlier if you don’t qualify), Japan taxes your worldwide income, including all Canadian-source dividends, interest, capital gains, and pensions.

The full mechanics of non-permanent resident status, including remittance-rule traps, are covered in our Japan tax residency 5-year rule guide. The single most important point for Canadians: do not casually remit large Canadian funds to Japan during the non-permanent-resident window without analyzing the tax effect first. A poorly timed transfer can create a Japanese tax bill on Canadian dividends or capital gains that would otherwise have been outside Japan’s grasp.

Severing Canadian Residency

Becoming a Japan tax resident does not automatically make you a Canadian non-resident. You need to actively sever Canadian residential ties:

- Dispose of (or rent out) your Canadian primary residence. Keeping an empty home available to you is the single strongest tie keeping you Canadian-resident in CRA’s view.

- Move your spouse/common-law partner and dependents with you (or already separated/resolved).

- Close or convert personal-use Canadian assets — cars (sell or storage), social memberships, healthcare cards (notify provincial health insurance of departure).

- Maintain non-Canadian banking — keep a Canadian bank account if needed for CPP/OAS receipt, but convert it to a non-resident account and notify the bank.

- File Form NR73 (Determination of Residency Status — Leaving Canada) if you want CRA’s formal determination, or simply file your departure-year T1 with a clearly marked departure date and ensure the next year’s filings reflect non-resident status.

The single biggest risk: dual residency. If you keep significant Canadian ties (home, spouse) and also become Japan-resident, both countries will claim you. The Canada-Japan treaty’s tie-breaker rules (covered in our treaty guide) will resolve the conflict — but you’ll have spent the year filing in both countries, often with double tax owed up front and refunded much later.

3. Year One: The Canadian Exit Return + Japanese Arrival Return

Your first calendar year covers two halves: pre-departure Canadian resident, post-arrival Japan resident. Both countries get a return for that year.

Canadian Side: The Departure T1

For the year you leave Canada, you file a standard T1 return with a departure date in the relevant section. This return covers:

- Your worldwide income from January 1 through your departure date as a Canadian resident.

- Your Canadian-source income only, from departure date through December 31 (non-resident period).

- The deemed disposition calculation on departure-eligible property (see Section 7).

- Any final claims for Canadian tax credits, RRSP contributions, etc.

Filing deadline: April 30 (or June 15 if self-employed) of the following year. Same as a normal Canadian resident T1.

Japanese Side: The First 確定申告 (Kakutei Shinkoku)

Japan’s tax year is the calendar year (January–December). Your first Japanese filing covers:

- Income from arrival date through December 31 of that year.

- For non-permanent residents: Japanese-source income only, plus foreign-source income actually remitted to Japan.

- For permanent-resident-status (uncommon in Year 1): worldwide income.

Filing window: February 16 through March 15 of the following year. The deadline is firm — late filing triggers Japanese penalties (see our Japan overdue tax filing guide).

Coordination Issues in Year 1

The two filings can interact in subtle ways:

- Currency conversion. Canada and Japan use different rules for converting income to local currency. Run conversions consistently using NTA-acceptable rates on the Japanese side and CRA Bank of Canada averages on the Canadian side.

- Tax credits. Don’t claim Canadian foreign tax credit for Japanese tax on income that’s also covered by a Canadian non-resident return — you’ll be claiming the same thing twice through different mechanisms.

- RRSP contributions. You can contribute to RRSP in your departure year up to your contribution room, deducted on the Canadian return. After departure, RRSP contributions get more complicated (and are usually inadvisable for non-residents).

Year 1 is also when the Japanese foreign tax credit framework starts — every year you have Canadian withholding tax on dividends, interest, or pension, you claim it as a foreign tax credit on the Japanese return. See our Foreign Tax Credit in Japan guide for the calculation mechanics.

4. TFSA, RRSP, RRIF: What Happens When You Leave Canada

These three accounts are at the heart of most Canadians’ financial lives — and all three behave very differently once you become a Japan tax resident.

TFSA: Tax-Free in Canada, Taxable in Japan

Japan does not recognize TFSA as a tax-protected account. Practical implications:

- Stop contributing immediately upon ceasing Canadian residency. Each new contribution as a non-resident triggers a 1% per month Canadian penalty until withdrawn.

- Income inside the TFSA is technically taxable in Japan for a Japan-resident account holder — dividends, interest, and realized capital gains.

- Withdrawals are not taxed by Canada (TFSA withdrawals never are), but the underlying income is Japan-taxable.

For most Canadians staying in Japan long-term, the cleanest move is to close the TFSA before or shortly after departure and reinvest into Japan’s NISA (Nippon Individual Savings Account), which is the actually-tax-free Japanese equivalent.

RRSP: Deferred in Canada, Grey Zone in Japan

RRSPs are tax-deferred for Canadian residents. For non-residents, the rules change at the moment of withdrawal:

- While the RRSP sits untouched, Canada doesn’t tax growth. The treaty is silent on whether Japan can tax the growth — most Japan-resident Canadians take the position that growth is deferred until withdrawal, mirroring Canadian treatment. This is a defensible but not bulletproof position.

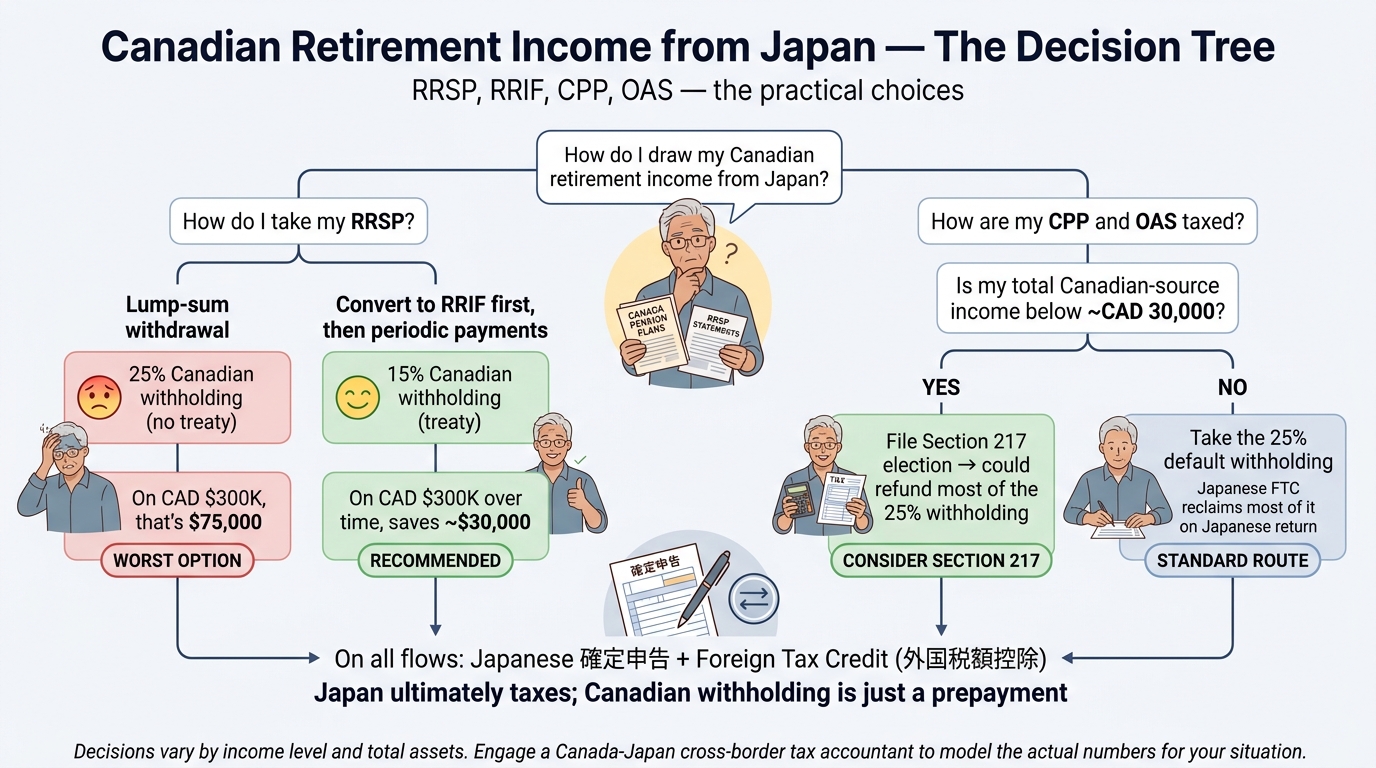

- Lump-sum RRSP withdrawal as a Canadian non-resident: 25% Canadian withholding tax, no treaty reduction.

- Convert RRSP to RRIF first, then take periodic payments: this reduces Canadian withholding to 15% under treaty principles for periodic pension payments (payments not exceeding the greater of twice the RRIF minimum amount or 10% of opening fair market value).

The lump-sum-vs-periodic decision is one of the most consequential financial choices a Canadian retiree in Japan will make. On a CAD 300,000 RRSP/RRIF, the difference between 25% lump-sum withholding and 15% periodic withholding is CAD 30,000 over the lifetime of the account.

RRIF: Easier in Practice

The RRIF (Registered Retirement Income Fund) is essentially an RRSP in payout mode. Once converted, you must take a minimum amount each year (calculated by age). For Japan-resident Canadians, the RRIF route offers:

- The 15% periodic-payment treaty withholding rate.

- Stable, predictable annual income for budgeting and Japanese tax planning.

- Foreign tax credit claim on the Japanese side for the 15% Canadian withholding.

Most Canadian financial institutions will handle the RRSP-to-RRIF conversion for a non-resident on request. Confirm with your institution that they’ll apply the 15% rate (with NR301 on file) rather than the 25% default. Some institutions default to 25% and require explicit instruction to apply the treaty rate.

5. CPP & OAS for Canadian Retirees in Japan

If you’re approaching retirement age in Japan, you’ll deal with two main Canadian public pensions:

CPP (Canada Pension Plan)

CPP is a contributory pension. You qualify based on your years of CPP contributions (or, under the Japan-Canada Social Security Agreement, Japanese pension contributions can be added to qualify you for CPP). Once receiving CPP as a Japan-resident non-resident of Canada:

- Canadian withholding: 25% (the Canada-Japan treaty has no specific pension provision reducing this).

- Japanese taxation: CPP is treated as miscellaneous income (雑所得 zatsushotoku) on your Japanese tax return.

- Foreign tax credit: claim the 25% Canadian withholding on your Japanese return.

- Section 217 election: may reduce Canadian tax to below 25% if your Canadian-source income is modest (see Section 8).

OAS (Old Age Security)

OAS is a residency-based pension. You qualify by having lived in Canada for at least 10 years (or, with the SSA, totalization can help). The Japan-Canada SSA recognizes Japanese residence periods to help meet the OAS 10-year threshold.

For Japan-resident OAS recipients:

- Canadian withholding: 25% default.

- OAS clawback (Recovery Tax): high-income recipients (worldwide income above the annual clawback threshold) have a portion of OAS recovered. Japan-source income counts.

- Japanese taxation: same miscellaneous income treatment as CPP.

- Section 217 election: strongly worth running the numbers (OAS is the prime use case).

Direct Deposit to Japanese Banks

Service Canada offers direct deposit of CPP and OAS to Japanese bank accounts in JPY. This eliminates the wire/conversion fees of receiving payments to a Canadian bank and converting. Set this up in advance — paperwork is straightforward but takes time.

6. Canadian Rental Property from Japan: Section 216

If you retained a Canadian rental property after moving to Japan, you have specific compliance obligations:

The Default 25% Gross-Rent Withholding

Without taking action, your Canadian tenant or property manager must withhold 25% of the gross rental income (not net after expenses) and remit it to CRA monthly. This is brutal — your actual net rental income after Canadian expenses (mortgage interest, property tax, repairs, management fees) might be a small fraction of gross rent, yet the 25% comes off gross.

Section 216 Election: The Fix

To pay tax only on net rental income at non-resident marginal rates:

- File Form NR6 — Undertaking to File a Section 216 Return with your Canadian property manager or tenant. Once accepted by CRA, withholding switches from 25% of gross rent to 25% of net rental income.

- File an annual Section 216 return by June 30 of the following year. This calculates your actual net rental tax owed; any over-withholding is refunded.

For most Canadian rental properties, Section 216 reduces effective Canadian tax dramatically — sometimes to zero (if interest and depreciation offset rental income). Filing Section 216 is essential for Canadians-in-Japan with retained rental property.

Japan Side: The Rental Income Also Goes on Your Japanese Return

For permanent-resident-status Canadians (year 6+), the gross rental income (with Japanese-rules expenses) goes on your Japanese return as foreign rental income. Foreign tax credit applies for Canadian tax paid. For non-permanent residents (years 1-5), Japanese rental tax only applies if rental income is remitted to Japan.

7. Departure Tax: Planning the Deemed Disposition

This is the one-time Canadian tax most departing Canadians forget about — and it can be expensive.

What Gets Deemed Disposed

On the day you cease Canadian tax residency, Canada treats you as having sold (and immediately repurchased at fair market value) most types of taxable Canadian property. Capital gains tax is owed on your departure-year T1 return.

Subject to deemed disposition:

- Shares and ETFs in non-registered Canadian or foreign brokerage accounts.

- Foreign currency holdings above a de minimis threshold.

- Cryptocurrency held by you personally.

- Most other capital property held for investment.

Exempt from deemed disposition:

- Canadian real property (taxed only when actually sold, with Section 116 process).

- RRSP, RRIF, TFSA accounts (the wrapper exempts from deemed disposition, though future withdrawals are still taxed).

- Pension rights, life insurance.

The Planning Window

Departure tax is essentially a tax on accrued unrealized gains. Smart Canadians planning a move to Japan often:

- Realize losses pre-departure to offset gains that will be deemed-disposed.

- Decide whether to trigger gains pre-departure (at known Canadian marginal rates) or accept the deemed disposition (which can be deferred with security posted).

- Consider the Japan side — if you become Japan-resident with high-cost-basis assets (because Japan starts your basis at fair market value on the day you become Japan-resident, in many cases), you may have a wash; if Japan uses original cost, you may face double taxation on the same gain.

This is one of the highest-value places to engage a Canadian cross-border tax accountant before your move.

Deferring the Departure Tax

You can elect to defer the departure tax until the property is actually sold, but you must post security with CRA (cash, bond, or letter of credit from a Canadian financial institution). For small departure-tax balances (under CAD 16,500 in most cases, indexed annually), security is waived automatically.

8. Section 217 Election: When It Saves Canadians Money

Section 217 of Canada’s Income Tax Act allows non-resident Canadians to elect to be taxed on certain Canadian-source income (called “qualifying Canadian benefits”) as if they were Canadian residents — getting access to personal tax credits, the basic personal amount, and possibly lower marginal rates.

Qualifying Income

Section 217 applies to:

- OAS pension

- CPP and Quebec Pension Plan

- Old Age Security Guaranteed Income Supplement (GIS — though GIS is generally not paid to non-residents after 6 months)

- Registered pension plan benefits

- RRSP and RRIF income

- Retiring allowances

- Unemployment Insurance / Employment Insurance benefits (rare for emigrants)

When Section 217 Saves Money

Run the numbers if your Canadian-source income is below approximately CAD 30,000 (basic personal amount + low-marginal-rate space). At that level, Section 217 typically refunds part or all of the 25% non-resident withholding tax. As income rises above CAD 50,000–60,000, the math tips back to non-resident withholding being the cheaper option.

How to Elect

- By April 30 (or June 30 for some cases) of the following year, file a Section 217 return with CRA.

- Report all Canadian-source income covered by Section 217 plus any other Canadian-source income.

- Calculate tax as if you were a Canadian resident (with credits) and reconcile against the 25% already withheld. Any over-withholding is refunded; any under-withholding (uncommon) is owed.

The election is annual — you decide each year whether to use it based on your numbers.

9. Annual Filing Calendar for Canadians in Japan

Once past Year 1, the annual rhythm for a typical Canadian-in-Japan looks like this:

| Month | Canadian Tax Action | Japanese Tax Action |

|---|---|---|

| Jan – Feb | T-slips arrive from Canadian payers (T4A, T4RIF, T5, NR4). | Gather Japanese income documents (源泉徴収票, etc.). |

| Feb 16 – Mar 15 | — | File Japanese tax return (確定申告). Include Canadian income with foreign tax credit. |

| Apr 30 | File Canadian T1 non-resident return (if needed). Section 217 election deadline. | — |

| Jun 30 | Section 216 rental return deadline, if applicable. | — |

| Year-end | Renew NR301 forms (every 3 years). | Overseas Asset Statement (国外財産調書) if assets >JPY 50M. |

Currency and Documentation

Throughout the year, retain:

- Canadian T-slips (T4A for pension, T4RIF for RRIF, T5 for investment, NR4 for non-resident withholding statements).

- Bank statements showing Canadian-source receipts and Japanese deposits.

- NR301 acknowledgments from each Canadian payer.

- Currency conversion records — Bank of Canada annual average for CRA filings, NTA-approved rates for Japanese filings.

10. Common Pitfalls for Canadians in Japan

The most expensive mistakes we see Canadians-in-Japan make:

Pitfall 1: Assuming the Canadian Tax System Stops at the Border

Canadian-source income continues to be taxable in Canada even after you move to Japan. NR301 forms, Section 216 returns, Section 217 elections — all are ongoing obligations, not one-time exit tasks. Plan for them in your annual rhythm.

Pitfall 2: Continuing TFSA Contributions

The 1% per month penalty on non-resident TFSA contributions is automatic and unforgiving. CRA tracks this through annual TFSA reporting. Stop contributing the moment you become non-resident.

Pitfall 3: Pulling RRSP as Lump Sum Without Considering RRIF Conversion

Withholding 25% vs 15% on a CAD 200,000 RRSP is a CAD 20,000 difference. The conversion paperwork is straightforward — but it has to happen before the withdrawal.

Pitfall 4: Forgetting the Japanese Foreign Tax Credit

Every year you have Canadian withholding tax, you should be claiming a Japanese foreign tax credit on your 確定申告. Many Canadians-in-Japan filing their own first-year Japanese returns miss this and double-pay.

Pitfall 5: Failing to File Section 216 on Canadian Rental

25% gross-rent withholding can exceed your actual rental profit, leaving you with negative cash flow on a property that should be profitable. NR6 + Section 216 is the standard fix.

Pitfall 6: Mis-Timing the Non-Permanent Resident Window

The first 5 of 10 years in Japan offer a unique foreign-income shelter — but only on income not remitted to Japan. Sending Canadian funds to Japan to buy a house in year 4 can suddenly subject prior-year Canadian gains to Japanese tax. Plan large remittances around the residency status carefully.

Pitfall 7: Not Reporting Overseas Assets to NTA

The Overseas Asset Statement (国外財産調書) is required if your overseas financial assets exceed JPY 50 million at December 31. Penalties for non-filing include reduced foreign tax credit and increased exposure on income from undisclosed accounts. Most Canadians with RRSP + Canadian brokerage + Canadian real estate cross the threshold easily.

Pitfall 8: Forgetting Provincial Healthcare

If you don’t actively notify your provincial healthcare authority (OHIP, BC MSP, etc.) of your departure, you may remain technically enrolled — and any future medical claims will be flagged. Some Canadians have had unpleasant surprises when returning briefly to Canada and being denied service.

11. FAQ: Canadian Citizens Tax in Japan

Q1: I just moved to Japan on a work visa. Do I file in both countries this year?

Yes — your departure-year Canadian return covers your pre-departure Canadian residency period (worldwide income) plus any Canadian-source income after departure. Your first Japanese return covers from arrival through December 31. Year 2 onward, you typically file annually in Japan and only in Canada if you have Canadian-source income.

Q2: My company offered to put me on a “Canadian payroll, Japan location.” What’s the tax impact?

Mismatched payroll location and tax residency is a frequent source of confusion. As a Japan tax resident working physically in Japan, your employment income is Japan-source under treaty rules, regardless of which entity cuts the paycheck. Canadian payroll deductions are usually wrong in this case — you’ll likely need to request a Canadian payroll-withholding waiver and then declare the income fully in Japan. Get specialist advice before accepting this structure.

Q3: Can I keep my CRA online account access from Japan?

Yes — CRA My Account works internationally. You can file Canadian non-resident returns electronically through CRA-approved software. Direct deposit to a Japanese bank account is supported for CPP, OAS, and tax refunds.

Q4: I have CAD 400,000 in RRSPs and I’m moving to Japan at age 55. Should I withdraw before leaving?

Almost certainly not as a lump sum. Pre-departure RRSP withdrawal is taxed at your Canadian marginal rate (potentially 30-50%+ with provincial tax). Post-departure with RRIF conversion + periodic payments, you’d face 15% Canadian withholding plus your Japanese marginal rate (with foreign tax credit). Run the numbers with a cross-border accountant — usually post-departure RRIF wins, especially if you expect Japan-side marginal rates to be moderate.

Q5: How does Japan tax my Canadian-dollar cash holdings?

Foreign currency cash held by a Japan resident is not taxable until disposed of. Currency gains realized when you convert CAD to JPY can be considered miscellaneous income in Japan if substantial. Most personal-scale currency holdings stay below thresholds that NTA actively pursues.

Q6: What about Canadian inheritance — if my parents pass away while I’m in Japan?

Canada has no inheritance tax (the estate pays Canadian capital gains tax via deemed disposition; the recipient receives net assets tax-free). Japan, however, has steep inheritance tax that applies to a Japan-resident heir on worldwide inheritance — including from a non-Japanese parent. See our Japan gift tax 10-year rule guide for the residency-based exposure rules. Canadians in Japan inheriting from Canadian parents have faced 6- and 7-figure Japanese inheritance tax bills they didn’t anticipate.

Q7: I’m a Canadian self-employed contractor with Canadian clients. Do I bill in CAD or JPY?

Operationally, either works — your books just need to convert consistently for both tax authorities. Tax-wise: you’re a Japan-resident self-employed person earning Japan-source income (the work is performed in Japan). Canadian clients should not withhold Canadian income tax. You file Japanese 確定申告 declaring the income net of Japanese-rule expenses; Canada generally has no claim on this income.

Q8: My spouse is Japanese and I’m Canadian. Do we file jointly?

Japan does not have joint spousal returns — each spouse files independently. Some spouse-related deductions exist (the Japanese spousal deduction, for example, if one spouse has low income). Canadian non-resident returns are also individual filings. Coordinate household tax planning, but the filings stay separate.

12. Get Expert Help for Canadians in Japan

Canada-Japan cross-border tax is one of the trickier expat tax interfaces. The right professional combination is usually either (a) a single Japan tax accountant with Canada-Japan experience, or (b) a coordinated team of one Canadian cross-border accountant and one Japanese tax accountant.

TaxMatch Japan introduces Canadians to Japan tax accountants who have handled multiple Canada-Japan files — including departure-tax timing, RRSP/RRIF strategy, Section 217 elections, and ongoing dual-jurisdiction annual filings. Initial introductions are free.

Common engagement profiles for Canadians in Japan:

- Pre-move planning: optimize departure timing, structure RRSP for post-move drawdown, decide on TFSA closure, evaluate property disposal vs Section 216 retention.

- First-year-in-Japan filings: depart return + arrival return, foreign tax credit setup, NR301 with Canadian payers, overseas asset statement preparation.

- Ongoing annual filings: Japanese 確定申告 with Canadian foreign income, Canadian Section 216/217 returns, RRSP-to-RRIF transitions, Canadian rental property reporting.

- Pre-retirement and inheritance planning: CPP/OAS timing, RRIF drawdown strategy, Japanese inheritance tax exposure analysis.

Free Matching for Canadians in Japan

Tell us your situation and we’ll match you with a Japan tax accountant who has handled Canadian client files. No fees, no obligation.

Prefer WhatsApp? Message us at +81 80-6075-2063

Related Guides

Canada-Japan Tax Treaty Guide

The treaty mechanics article-by-article — withholding, pensions, capital gains

Japan Tax Residency 5-Year Rule

Non-permanent resident status — your biggest early-years opportunity

Foreign Tax Credit in Japan

Claiming Canadian withholding back on your Japanese return

Overseas Asset Reporting in Japan

JPY 50M threshold for the annual 国外財産調書

Japan Pension Lump-Sum Refund

If you later leave Japan — the Japanese pension refund process