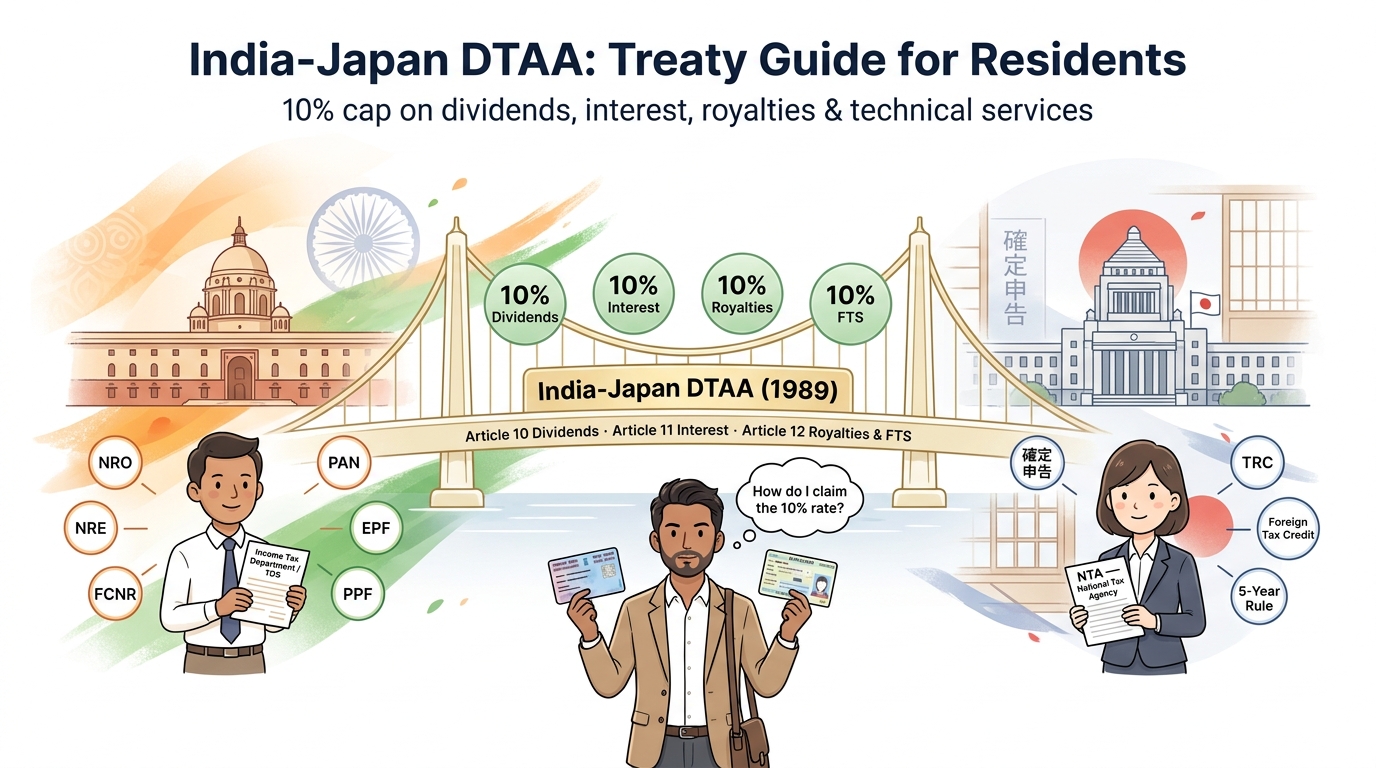

If you’re an Indian living in Japan — or a Japan-resident foreigner holding NRO accounts, Indian mutual funds, or Indian rental property — the India-Japan Double Taxation Avoidance Agreement (DTAA) is the document that decides whether your Indian TDS withholding is 30% or 10%. The treaty has been in force since 1989, and its 10% cap on dividends, interest, royalties, and fees for technical services is one of the most generous individual-friendly DTAA provisions India has signed. But you cannot just claim it — you need a PAN (in most cases), Form 10F, a Tax Residency Certificate from Japan, and a No-PE declaration. This guide walks through the mechanics from a Japan-resident perspective.

This is the treaty-side companion to our Indian Citizens Tax in Japan guide. Start here if you want the treaty mechanics; go to that one for persona-based “what do I do in what order” practical decisions.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. The India-Japan DTAA interacts with both Indian and Japanese domestic tax law, and every individual situation differs. Always engage a tax professional licensed in both jurisdictions (or a coordinated team) before relying on treaty positions.

Indian living in Japan with tax questions?

Get matched with a Japan tax accountant experienced in India-Japan cross-border issues — free.

Table of Contents

- Who Should Read This India-Japan DTAA Guide

- India-Japan DTAA: Background and Scope

- India-Japan Treaty Residency: NRI Status and Tie-Breakers

- India-Japan DTAA Withholding Rates: The 10% Story

- India-Japan Treaty Article 12: Royalties and Fees for Technical Services

- India-Japan DTAA Documentation: PAN, Form 10F, TRC, No-PE

- Capital Gains Under India-Japan DTAA

- NRO, NRE, FCNR Accounts: How They Interact with Japan Tax

- Japan-India Social Security Agreement

- Common India-Japan DTAA Mistakes

- India-Japan DTAA FAQ

- Get Expert Help With India-Japan DTAA

1. Who Should Read This India-Japan DTAA Guide

This guide is written for one or more of the following situations:

- You are an Indian national or NRI currently living in Japan and receiving Indian-source income (NRO interest, Indian mutual fund dividends, Indian rental property income, EPF/PPF distributions).

- You are a Japan-resident foreigner of any nationality holding Indian investments — Indian stocks, NRO deposits, Indian REITs, or Indian property.

- You are an IT professional or consultant receiving fees for technical services from Indian clients while based in Japan.

- You are planning to move from India to Japan — typically on a work, HSP (Highly Skilled Professional), or spouse visa — and need to understand which Indian assets will trigger ongoing Indian TDS and Japanese taxation.

- You are a tax professional or HR manager handling India-Japan cross-border tax for clients or employees and want a clean starting reference.

If none of the above applies, you probably don’t need DTAA analysis — a general guide on Japan tax residency rules or double taxation basics will serve you better.

2. India-Japan DTAA: Background and Scope

The formal name is the Agreement between Japan and India for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with Respect to Taxes on Income. Signed in 1989 and in force since then, the treaty was further modified by exchanges of notes and now operates alongside the Multilateral Instrument (MLI) updates that both India and Japan ratified.

What the DTAA Does

The India-Japan DTAA performs two core functions for individuals:

- Allocates taxing rights between India and Japan for specific income categories (employment, business profits, dividends, interest, royalties, fees for technical services, capital gains, pensions).

- Caps Indian withholding tax on outbound passive payments to Japan residents at a uniform 10% — substantially below India’s default TDS rates of 20–30% (plus surcharge and cess).

The DTAA does not eliminate filing. Both countries still apply domestic income tax to their respective residents on worldwide income. The treaty simply prevents you from being taxed twice on the same dollar — and provides the framework to claim the lower withholding rate on Indian-source income paid to Japan-resident recipients.

What the DTAA Does Not Cover

- The DTAA does not directly recognize EPF, PPF, or NPS as tax-deferred for Japan-resident account holders. Japan applies its own rules to investment income inside these accounts.

- The DTAA does not cover GST (Goods and Services Tax) in India or consumption tax in Japan. It is purely an income tax instrument.

- The DTAA does not cover social security contributions — that’s a separate matter under the Japan-India Social Security Agreement (in force since October 2016).

- The DTAA does not automatically apply. You must affirmatively claim treaty benefits by providing Indian payers with documentation (PAN, Form 10F, TRC, No-PE declaration) — covered in Section 6.

3. India-Japan Treaty Residency: NRI Status and Tie-Breakers

Before any DTAA provision applies, you must be a “resident of a Contracting State” under Article 4. Article 4 also resolves dual-residency through tie-breaker rules. Understanding the residency framework on both sides is foundational.

Indian Domestic Residency: Three Categories

Indian tax law recognizes three resident statuses for individuals:

- Resident and Ordinarily Resident (ROR): taxed on worldwide income.

- Resident but Not Ordinarily Resident (RNOR): taxed on Indian-source income plus foreign income from a business or profession controlled in India.

- Non-Resident (NR / NRI): taxed only on Indian-source income. Days-in-India tests govern the status:

- Less than 182 days in India during the financial year → Non-Resident.

- OR less than 60 days in India in the year AND less than 365 days in the preceding 4 years → Non-Resident.

For most Indians who move to Japan on a long-term visa, NRI status is established within the first Indian financial year (April–March) of departure, and continues as long as the days-in-India tests are met. The Income Tax Act’s exceptions for “deemed resident” (Indian citizens with India-source income above INR 15 lakh who are not tax-resident anywhere else) generally do not apply to Japan-resident Indians, since Japan claims you as resident under its own law.

Japan’s Domestic Residency Test

Japan considers you a tax resident if you have a jūsho (主たる生活の本拠地, primary base of living) in Japan, or a kyosho (居所, ordinary residence) of one year or more. For Indians on long-term work or HSP visas, Japan tax residency typically starts from arrival. For the first 5 of 10 years in Japan, you may qualify as a non-permanent resident, which limits Japanese taxation of foreign-source income to amounts actually remitted to Japan. See our Japan tax residency 5-year rule guide.

Article 4 Tie-Breaker for Dual Residency

If both India and Japan claim you under domestic law (which happens during transition years or for short-term assignees who maintain Indian residential ties), the treaty’s tie-breaker rules apply in this order:

- Permanent home: In which country do you have a permanent home available? If only one, that country wins.

- Centre of vital interests: If permanent homes exist in both, where are your personal and economic ties strongest?

- Habitual abode: Where do you habitually live (count days)?

- Nationality: Final tie-breaker.

- Mutual agreement: If still unresolved, India’s Competent Authority and Japan’s Competent Authority decide bilaterally.

For Indians who genuinely relocated to Japan with their immediate family, the tie-breaker confirms Japan residence — but only if you actually moved your “centre of vital interests” (family, employment, primary residence). Indians who maintain a flat in Mumbai or Bangalore and have established Japanese residency face genuine dual-residency analysis.

4. India-Japan DTAA Withholding Rates: The 10% Story

The signature feature of the India-Japan DTAA for individuals is the uniform 10% cap on the major categories of passive income. India’s default TDS rates without the treaty are significantly higher.

DTAA Withholding Rate Table

| Income Type | Indian Default TDS | India-Japan DTAA Rate |

|---|---|---|

| Dividends (from Indian companies) | 20% + surcharge + cess | 10% |

| Interest on NRO deposits | 30% + surcharge + cess | 10% |

| Royalties (literary, artistic, scientific) | 20% + surcharge + cess | 10% |

| Fees for Technical Services (FTS) | 20% + surcharge + cess | 10% |

| Rent (Indian rental property) | 30% TDS on gross | No special DTAA reduction (Indian domestic rate) |

| Pensions (private) | Variable, slab rates | Taxable in country of residence (Article 18) |

Source: India-Japan DTAA, India’s Income Tax Act, and CBDT Circulars. Rates current as of 2026.

A Practical Example: NRO Interest Paid to a Japan-Resident NRI

You hold an NRO Fixed Deposit in India earning INR 200,000 in interest for the year. What happens?

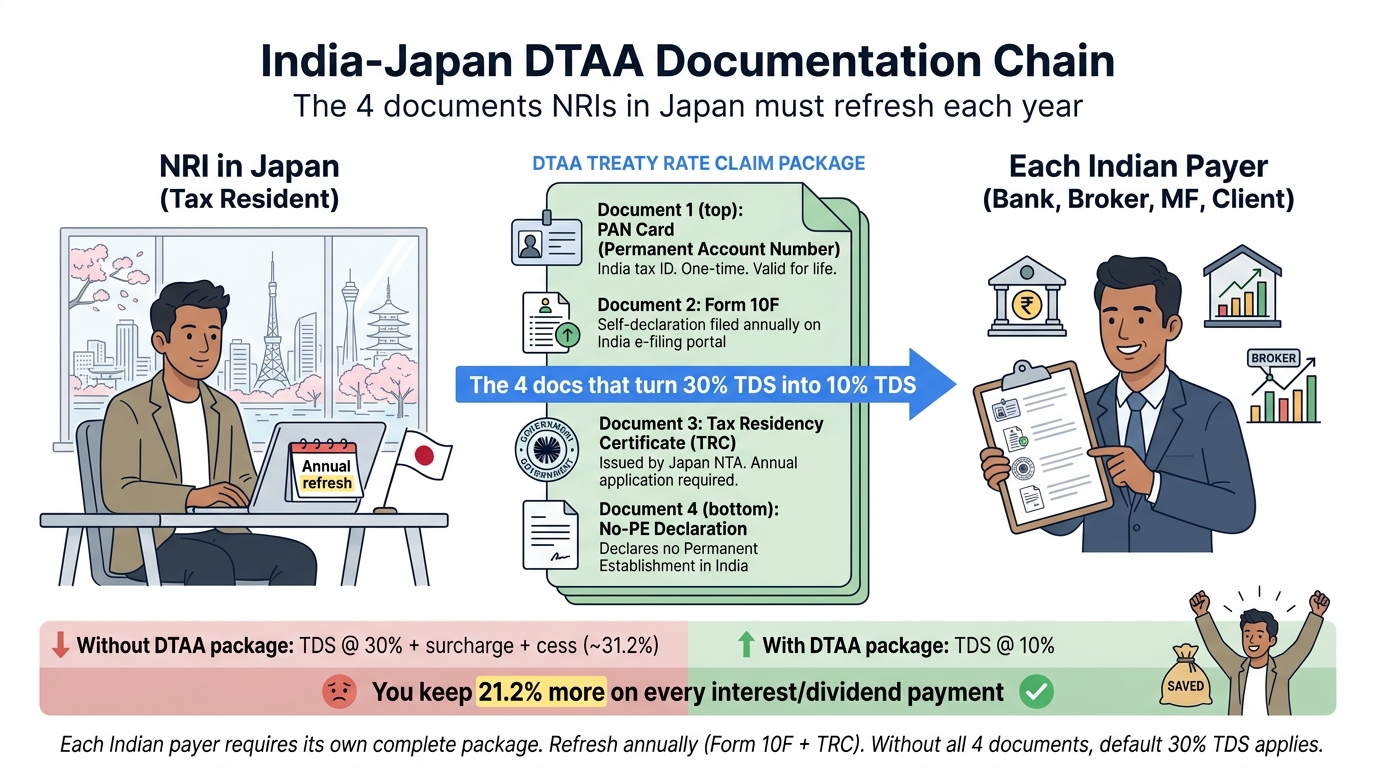

- Without DTAA documentation: Indian bank withholds TDS at 30% + surcharge + cess ≈ 31.2% = INR 62,400. You receive INR 137,600.

- With DTAA documentation properly filed (PAN + Form 10F + TRC + No-PE declaration): Indian bank withholds 10% = INR 20,000. You receive INR 180,000.

- Japan side: You declare the gross INR 200,000 interest on your Japanese tax return as foreign-source interest income. Japan taxes you at applicable rates.

- Foreign tax credit: You claim a Japanese foreign tax credit for the INR 20,000 (in JPY equivalent) already withheld by India, eliminating double taxation.

The DTAA-documentation step is what most Indians-in-Japan get wrong in their first year. The 21-percentage-point difference between 31.2% default TDS and 10% treaty TDS is real money — on INR 200,000 of interest, it’s a INR 42,400 cash flow improvement.

5. India-Japan Treaty Article 12: Royalties and Fees for Technical Services

Article 12 of the India-Japan DTAA covers royalties and fees for technical services (FTS) at a uniform 10% rate. This article is particularly relevant for Indian IT professionals, consultants, and engineers in Japan who continue to provide services to Indian clients.

What Counts as “Fees for Technical Services”

The DTAA defines FTS broadly. For Indian IT professionals working with Indian clients from Japan, the following payments typically fall under Article 12:

- Software development fees (where the IP transfers or licenses cross border).

- Consulting fees for technical, managerial, or engineering services.

- Training fees where the recipient acquires specialized technical knowledge.

- Maintenance and support fees for software or technical systems.

The “Make Available” Test (Modern Interpretation)

Indian courts and the CBDT have, over the years, narrowed the FTS definition through the “make available” test. For payments to be taxed as FTS, the technical service must make available the underlying technical knowledge to the recipient — i.e., the recipient must be able to use the knowledge independently after the engagement ends.

For routine software development outsourcing where the developer simply delivers code without transferring know-how, Indian payers and the Indian tax authority sometimes argue the payment is not FTS at all, but rather business profits under Article 7 — which means India can only tax if the Japan-resident provider has a Permanent Establishment in India. For a Japan-resident IT contractor with no Indian office, this position often results in zero Indian tax.

The exact classification — FTS vs business profits vs royalty — depends on contract language and the nature of services. Indian-tax-aware drafting of consulting agreements can significantly reduce Indian TDS exposure.

Practical Implications for IT Consultants in Japan

- If the Indian client treats the payment as FTS: 10% TDS withheld (treaty rate), Japanese foreign tax credit recovers it on Japanese return.

- If the engagement is characterized as business profits with no Indian PE: 0% Indian TDS, full Japanese taxation on net business income.

- If the engagement involves transfer of software ownership: may be characterized as royalty, also 10% under the treaty.

The strategic choice between “FTS-with-10%-TDS” and “business-profits-with-no-Indian-tax” depends on contractual structure and risk tolerance. Consult an Indian tax professional before structuring large consulting contracts.

6. India-Japan DTAA Documentation: PAN, Form 10F, TRC, No-PE

To claim DTAA benefits on Indian-source income, you must build a complete documentation package and provide it to each Indian payer (or income tax authority). Missing any component triggers the full default TDS rate.

The 4-Document Package

- PAN (Permanent Account Number): India’s tax identification number. Required for most transactions above modest thresholds. NRIs typically obtain PAN before becoming non-resident, but post-departure PAN application is also possible through India’s online portals. Without PAN, default TDS rates apply at higher rates (up to 20% even after treaty), and many Indian payers will not process treaty-rate payments.

- Form 10F: Self-declaration filed by the non-resident taxpayer with specific details (name, taxpayer ID, period covered, etc.). Filed electronically through India’s income tax e-filing portal. Required to support treaty claims even if you have PAN. Valid for one Indian financial year (April–March).

- Tax Residency Certificate (TRC): Issued by Japan’s National Tax Agency, certifying that you are a tax resident of Japan for the relevant year. The TRC is the official document that proves you qualify as a “resident of the other Contracting State” under Article 4 of the DTAA. Japan issues TRCs on request through your local Japanese tax office — typically takes 2–4 weeks.

- No Permanent Establishment Declaration: A simple declaration stating that you do not have a Permanent Establishment in India in respect of the income being claimed under treaty. Required by most Indian banks and corporate payers as part of the treaty-rate documentation package.

When to Submit the Package

The documentation must be on file with the Indian payer (bank, broker, employer, client) before the first treaty-rate payment is processed. Over-withheld TDS in prior periods is recoverable only through:

- Filing an Indian Income Tax Return as a non-resident and claiming the over-withheld amount as a refund.

- Or pursuing a refund through the Indian payer’s correction filings (rare in practice).

For ongoing income streams (NRO deposit interest, recurring mutual fund dividends), refresh the documentation package each Indian financial year. Form 10F has a strict one-year validity, so it must be re-filed annually.

7. Capital Gains Under India-Japan DTAA

Article 13 of the India-Japan DTAA allocates taxing rights on capital gains. The general principle: gains from selling Indian real property remain taxable in India (Article 13(1)), while gains from selling shares of Indian companies follow more nuanced rules.

Indian Real Property

Capital gains from selling Indian real estate are taxable in India regardless of the seller’s residence. Indian domestic law applies:

- Long-term capital gains (held >24 months): 20% with indexation benefit (subject to recent law changes — 2024 reforms removed indexation for many cases and applied 12.5% flat rate).

- Short-term capital gains (held ≤24 months): taxed at the seller’s slab rate.

- TDS on sale: the Indian buyer must withhold 20% on long-term gains or up to 30% on short-term gains paid to NRI sellers. Refund of over-withheld amount requires Indian tax filing.

Japan side: as a Japan resident, the gain is also reportable on your Japanese tax return. Foreign tax credit applies for Indian tax paid. For non-permanent residents (first 5 of 10 years in Japan), the gain may not be taxable in Japan if not remitted to Japan.

Indian Listed Securities (Shares, Mutual Funds)

Article 13(5) of the India-Japan DTAA gives India the right to tax gains from the alienation of shares in Indian companies (subject to subsequent protocol updates). India’s current domestic regime:

- Long-term capital gains on listed equity (held >12 months): 10% on gains exceeding INR 100,000 per year, without indexation.

- Short-term capital gains on listed equity: 15% flat.

- Long-term capital gains on unlisted shares: 12.5% flat (2024 reforms).

For Japan-resident Indians selling Indian listed shares, India’s flat 10% LTCG rate is often modest, and the foreign tax credit on the Japanese side typically neutralizes Indian tax. The friction is mainly procedural — claiming TDS refunds, coordinating exchange rate conversions, etc.

8. NRO, NRE, FCNR Accounts: How They Interact with Japan Tax

The three NRI-only bank account types in India have distinct tax treatments. For Japan-resident Indians, understanding each is essential.

NRO (Non-Resident Ordinary) Account

Holds Indian-source income (rent, dividends, interest from Indian deposits, mutual fund redemptions). Interest is fully taxable in India:

- Default TDS on NRO interest: 30% + surcharge + cess (≈31.2%).

- With DTAA documentation: 10% TDS under India-Japan treaty.

- Japan side: interest is foreign-source interest, declared on Japanese return with foreign tax credit.

- Repatriation: NRO funds can be repatriated up to USD 1 million per Indian financial year with documentation.

NRE (Non-Resident External) Account

Holds foreign earnings remitted to India and converted to INR. Interest is tax-free in India and fully repatriable. For Japan-resident Indians:

- NRE interest: 0% Indian tax, but fully taxable in Japan as foreign-source interest for Japan residents (the Indian exemption does not extend to Japanese taxation).

- Practically: for Japan residents, the Indian tax advantage of NRE accounts is mostly neutralized by Japanese taxation. NRE is still useful for free repatriation and for parking salary remittances.

FCNR (Foreign Currency Non-Resident) Account

Term deposit in foreign currency (USD, EUR, GBP, JPY). Interest is tax-free in India and the principal is repatriable. For Japan-resident Indians, FCNR interest is taxable in Japan, but the currency-hedge benefit (avoiding INR fluctuation) can be material.

When You Become NRI

Indian banking regulations require you to:

- Convert your existing Indian Resident Savings Account to an NRO account (mandatory).

- Notify mutual fund houses, brokers, and other Indian financial entities of your NRI status.

- Update KYC documentation with current Japanese address and proof of residence.

- If desired, open NRE and/or FCNR accounts for tax-free interest on remitted foreign earnings.

Many Indians moving to Japan delay these conversions, which results in continued resident-rate TDS (often higher than non-resident rates after DTAA) and complications later. Convert within 6 months of departure.

9. Japan-India Social Security Agreement

Separate from the DTAA, Japan and India have a Social Security Agreement (SSA) in force since October 1, 2016. The SSA covers two Indian programs (Employees’ Provident Fund / EPF and Employees’ Pension Scheme / EPS) and Japan’s public pension system (Kōsei Nenkin / Kokumin Nenkin).

What the SSA Does

- Detached-worker exemption: Indians sent to Japan by an Indian employer for up to 5 years can obtain a Certificate of Coverage from the Employees’ Provident Fund Organisation (EPFO), exempting them from Japanese pension contributions while continuing to contribute to Indian EPF. The same works in reverse for Japanese employer postings to India.

- Totalization for eligibility: Japanese pension contribution periods can be added to Indian EPF contribution periods to qualify for benefits in either country.

- Withdrawal of contributions: For Indians who paid Japanese pension contributions but did not have a detached-worker exemption (e.g., direct local hires), the standard Japanese lump-sum withdrawal process applies on departure. See our Japan pension lump-sum withdrawal guide.

EPF and PPF Treatment for Japan-Resident Indians

The DTAA and SSA do not, by themselves, give EPF or PPF tax-deferred status in Japan. For Japan-resident Indians:

- EPF: Annual interest credited to EPF is, in principle, taxable in Japan as foreign-source interest. In practice, NTA enforcement of this point varies and many Japan-resident Indians take the position of deferring tax until actual withdrawal.

- PPF: Same principle as EPF. Indian tax-exempt status does not transfer to Japan.

- Withdrawal: When you withdraw EPF or PPF as a Japan resident, the entire balance is, in principle, Japan-taxable income (with credit for any Indian withholding).

This is one of the grey areas where Indian-Japanese tax accountants disagree. Conservative positions declare annual EPF/PPF income; aggressive positions defer until withdrawal. Discuss with a qualified Japan tax accountant before filing.

10. Common India-Japan DTAA Mistakes

The most frequent India-Japan tax mistakes for individuals:

Mistake 1: Not Converting Resident Account to NRO

Once you become an NRI, Indian banking regulations require conversion of your Indian Resident Savings Account to an NRO account. Operating an Indian resident account as an NRI is technically illegal under FEMA and creates compliance complications later.

Mistake 2: Failing to Submit Form 10F Annually

Form 10F validity is one Indian financial year. Indians who file once and assume continued treaty rates often discover years later that TDS has been applied at default 30% rates throughout. Refresh Form 10F every April.

Mistake 3: Forgetting the TRC

Indian banks will not apply DTAA rates without a current Japan-issued TRC on file. Request a TRC from your local Japanese tax office at the start of each Indian financial year — the timing is misaligned with Japan’s calendar, so it requires deliberate planning.

Mistake 4: Ignoring the Japanese FTC on Indian TDS

Indian TDS at 10% is creditable against Japanese tax through the foreign tax credit (外国税額控除). Many first-time Japan-tax-filing Indians miss this and effectively double-pay.

Mistake 5: Mis-Characterizing IT Consulting Income

Indian IT contractors in Japan should carefully consider whether their work for Indian clients is properly FTS (10% Indian TDS) or business profits (potentially zero Indian tax if no PE). The choice has material cash flow implications.

Mistake 6: Triggering Remittance-Rule Tax

For Indian NRIs in their first 5 years in Japan (non-permanent resident status), foreign-source income is Japan-taxable only if remitted. Sending large NRO/NRE balances to Japan to buy a house can suddenly subject prior-year Indian gains to Japanese tax. Plan large remittances around the residency status carefully.

Mistake 7: Not Reporting Indian Assets to NTA

If your total overseas financial assets exceed JPY 50 million at year-end, you must file Japan’s Overseas Assets Statement (国外財産調書). Indian mutual funds, NRO/NRE/FCNR balances, Indian property, and EPF/PPF all count. See our Overseas Asset Reporting guide.

11. India-Japan DTAA FAQ

Q1: I just moved to Japan from India. Do I need to file Indian taxes anymore?

You file an Indian return for the financial year in which you departed (covering your pre-departure resident period) and continue filing in subsequent years only if you have Indian-source income. NRO interest, Indian rental, Indian capital gains, etc., are all Indian-taxable for NRIs and require an Indian Income Tax Return — typically Form ITR-2 for individuals with foreign assets.

Q2: Do I need a PAN if I no longer live in India?

Yes — for most India-source income above modest thresholds, PAN is required. Even with the India-Japan DTAA, Indian payers will withhold at higher rates if PAN is absent. Existing PANs remain valid regardless of residency change.

Q3: How does Indian crypto taxation interact with my Japanese tax?

India taxes Virtual Digital Assets (VDA) gains at a flat 30% with no loss offset. For NRIs, this applies to gains on Indian-platform crypto transactions. Japan also taxes crypto gains. Cross-border crypto activity by Japan-resident Indians is complex — engage a specialist before any large transaction.

Q4: I get a salary directly from my Indian employer while based in Japan. Where do I pay tax?

Employment income for work physically performed in Japan is Japan-taxable. Your Indian employer should generally not withhold Indian TDS on this salary (provided you have NRI status and the work is performed outside India). The salary is fully reportable on your Japanese tax return. If your Indian employer continues to apply Indian TDS, you’ll need to claim refund through Indian Income Tax Return filing.

Q5: Can I keep my SIP investments in Indian mutual funds while in Japan?

Yes, but you’ll need to update KYC with NRI status and link your NRO account. Most fund houses support NRI investors. Dividends and capital gains will face Indian TDS — at 10% under DTAA with proper documentation. Some fund houses restrict NRI investments (especially US-resident NRIs); Japan-resident NRIs typically have full access.

Q6: Do I need to report my Indian EPF balance to NTA?

Yes, if total overseas financial assets exceed JPY 50 million at December 31, the Overseas Asset Statement requirement applies. EPF balance counts among overseas financial assets.

Q7: My parents in India send me INR 1 lakh monthly. Is this taxable in Japan?

Gifts from family members within reasonable amounts are generally not income-taxable in Japan. However, very large transfers may attract Japanese gift tax (with the 110-man yen annual exemption per recipient). For Indian-side analysis, see the gift tax provisions under Indian Income Tax Act (gifts above INR 50,000 from non-relatives are taxable; gifts from defined relatives are exempt in India).

Q8: I plan to buy a Japanese house using funds from my NRO account. Tax implications?

Remitting NRO funds to Japan for a property purchase triggers two issues: (1) the remitted amount may bring previously-deferred foreign income within the Japanese tax base if you’re in non-permanent resident status; (2) the funds themselves are not taxable on transfer, but the underlying source income may now be. Run the math with a tax accountant before large remittances.

12. Get Expert Help With India-Japan DTAA

India-Japan tax planning combines two complex tax systems with relatively few practitioners deeply experienced in both. The right professional combination is either (a) a single Japan tax accountant with India-Japan exposure, or (b) coordinated teams of one Indian CA familiar with NRI taxation and one Japanese 税理士 (zeirishi) who handles NRI clients regularly.

TaxMatch Japan introduces Indian professionals and NRIs to Japan tax accountants who have handled multiple India-Japan files — including DTAA documentation, NRO/NRE optimization, EPF withdrawal strategy, FTS contract structuring, and ongoing dual-jurisdiction annual filings. Initial introductions are free.

Common engagement profiles for Indians in Japan:

- Pre-move planning: NRI status determination, NRO/NRE conversion, EPF/PPF strategy.

- First-year-in-Japan filings: Indian departure-year return + Japanese arrival return, DTAA documentation setup, Form 10F and TRC.

- IT consulting contract structuring: FTS vs business profits classification, PE risk management, withholding optimization.

- Ongoing annual coordination: Indian ITR + Japanese 確定申告, foreign tax credit calculation, overseas asset reporting.

Free Matching for India-Japan Tax Cases

Tell us your situation and we’ll match you with a Japan tax accountant experienced in India-Japan files. No fees, no obligation.

Prefer WhatsApp? Message us at +81 80-6075-2063

Related Guides

Indian Citizens Tax in Japan

NRI status, NRO/NRE, EPF withdrawal — citizen-side practical guide

Double Taxation in Japan

Treaty relief across US/UK/India/Canada/Australia comparisons

Foreign Tax Credit in Japan

Claiming Indian TDS back on your Japanese return

Japan Tax Residency Rules

Non-permanent resident framework — first 5 years critical

Overseas Asset Reporting in Japan

JPY 50M threshold including NRO/NRE/FCNR balances