You’re an Indian living in Japan — IT professional on an HSP visa, spouse on a long-term visa, a researcher, or a senior leader on intra-company transfer. The tax mechanics are different from the India-only world you knew: India still claims a slice of your Indian-source income, Japan taxes your global income, and the documentation chain (PAN, Form 10F, TRC, No-PE) determines how much you’ll lose to withholding. This is the citizen-focused companion to our India-Japan DTAA Guide: less treaty mechanics, more “what do I do and in what order.”

If you want the treaty-article-by-article version, start with the DTAA guide. This article is the practical decision-tree for Indians settling in (or already settled in) Japan.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. India-Japan cross-border tax issues are technical and individual fact patterns vary widely. Engage a tax professional with cross-border experience before acting on any of the strategies discussed.

Indian living in Japan with tax questions?

Get matched with a Japan tax accountant experienced in Indian client files — free.

Table of Contents

- Who This Indian-in-Japan Tax Guide Is For

- Becoming an NRI: India-Side Status Change

- Becoming a Japan Tax Resident as an Indian

- Year One: India Departure ITR + Japan Arrival 確定申告

- NRO/NRE/FCNR Conversion: The First Banking Action

- EPF, PPF, NPS: What Happens When You Move to Japan

- Indian DTAA Documentation Chain Every Year

- Indian Rental Property from Japan

- Indian IT Consulting Income from Japan

- Annual Filing Calendar for Indians in Japan

- FAQ: Indian Citizens Tax in Japan

- Get Expert Help for Indians in Japan

1. Who This Indian-in-Japan Tax Guide Is For

This guide assumes one or more of the following:

- You are an Indian national who has moved (or is moving) to Japan on a long-term visa — work visa, HSP (Highly Skilled Professional), spouse visa, intra-company transfer, or business manager.

- You are an IT or engineering professional sent to Japan by an Indian or global employer and now navigating dual tax obligations.

- You are an Indian researcher or academic on a long-term Japanese university or institute placement.

- You are a senior leader or manager on intra-company transfer holding equity, ESOPs, or RSUs vested in either jurisdiction.

- You are an Indian spouse of a Japanese citizen or other foreign resident, now living long-term in Japan with Indian assets you need to manage.

If you’re not Indian but your spouse is, this guide still helps you understand the household tax picture. Japanese tax law treats each spouse as an individual filer.

What This Guide Does Not Cover

- Indian corporate tax issues — running an Indian company from Japan triggers complex Permanent Establishment, Place of Effective Management (POEM), and other risks that need specialist Indian tax counsel.

- State-specific Indian tax — India’s income tax is federal, but states have stamp duty and other taxes on specific transactions. Out of scope here.

- US-India-Japan triangular cases — Indians who are also US Green Card holders face an extra layer of US filing. Consult our US Citizens Tax in Japan complete guide.

2. Becoming an NRI: India-Side Status Change

India’s tax residency framework hinges on physical presence. Under the Income Tax Act:

- Resident: 182+ days in India during the financial year (April–March), OR 60+ days in the year AND 365+ days in the preceding 4 years.

- Non-Resident (NRI): Fails both tests.

- Resident but Not Ordinarily Resident (RNOR): An intermediate status for newly returning Indians or those with limited recent residency history.

For most Indians moving to Japan on a long-term visa, NRI status is established in the first full financial year after departure. The status is reassessed each year based on physical presence.

“Deemed Resident” Risk

Recent changes to Indian tax law introduced a “deemed resident” category: Indian citizens with India-source income above INR 15 lakh who are not tax-resident anywhere else are deemed Indian resident. For Japan-resident Indians, this rule rarely bites because Japan claims you as a tax resident under its own law — but it’s worth confirming with your tax advisor each year, especially if your Japan stay is short or partial.

What NRI Status Means for India-Side Tax

- Taxable in India: only Indian-source income (NRO interest, Indian rental, Indian capital gains, dividends from Indian companies, salary for work physically performed in India).

- Not taxable in India: foreign salary, foreign investment income, NRE deposit interest (tax-exempt by domestic law), FCNR interest.

- Filing obligation: required if Indian-source income exceeds the basic exemption (INR 2.5 lakh for individuals under 60) or if claiming TDS refund.

3. Becoming a Japan Tax Resident as an Indian

Japan determines tax residency based on jūsho (primary base of living) and kyosho (ordinary residence of one year or more). For most Indians on long-term work, HSP, or spouse visas, Japan tax residency starts from arrival.

Non-Permanent Resident Status (First 5 of 10 Years)

For your first 5 years of residency within any 10-year period, you may qualify as a non-permanent resident — a sub-status that excludes foreign-source income from Japanese taxation unless remitted to Japan. This is one of Japan’s most generous tax features for new foreign arrivals.

For Indians, the practical implications include:

- NRO interest income earned in India and kept in India: not taxable in Japan during non-permanent resident years (provided not remitted).

- Indian mutual fund dividends reinvested in India: same treatment.

- Indian rental income deposited into Indian accounts and held there: same treatment.

- The remittance trap: any transfer of foreign-source income to Japan during the non-permanent period brings the remitted amount within the Japanese tax base. Sending NRO funds to Japan to buy a house can suddenly subject years of prior NRO interest to Japanese tax.

Plan large remittances carefully. The framework is fully covered in our Japan tax residency 5-year rule guide.

4. Year One: India Departure ITR + Japan Arrival 確定申告

Your first transition year covers two halves: pre-departure Indian resident, post-arrival Japan resident. Both countries get a return for that year.

India Side: Departure-Year ITR

For the Indian financial year (April–March) in which you depart, file your Indian Income Tax Return as a resident for the pre-departure portion (your worldwide income from April 1 through departure) and continue reporting Indian-source income for the post-departure portion. Use Form ITR-2 if you have foreign assets or income, or ITR-1 if your case is simpler.

Filing deadline: July 31 of the following year (with possible extensions). Late-filing penalties under Section 234F apply if missed.

Japan Side: First 確定申告 (Kakutei Shinkoku)

Japan’s tax year is the calendar year (January–December). Your first Japanese filing covers:

- Income from arrival date through December 31 of that year.

- For non-permanent residents: Japanese-source income only, plus foreign-source income actually remitted to Japan.

- For permanent-resident-status filers (uncommon in Year 1): worldwide income.

Filing window: February 16 through March 15 of the following year. The deadline is firm — late filing triggers Japanese penalties. See our Japan overdue tax filing guide.

Coordination Issues in Year One

- Currency conversion: India and Japan use different conversion rules. India uses the State Bank of India TT buying rate for most transactions; Japan uses NTA-acceptable rates. Be consistent within each return.

- Salary continuity: If your Indian employer continued to pay you after departure for work performed in Japan, that salary is Japan-source income (treaty rule) and should not be subject to Indian TDS. Coordinate with your Indian payroll team before the first post-departure paycheck.

- RSU/ESOP vesting: If you have RSUs or ESOPs vesting during the transition year, the tax treatment depends on grant location, vesting location, and your residency at vesting. This is one of the most common pitfalls — get specialist advice if you have material equity vesting around your move.

5. NRO/NRE/FCNR Conversion: The First Banking Action

Indian banking regulations (FEMA) require that you convert your Indian Resident Savings Account to an NRO account within a reasonable time of becoming NRI. Operating an Indian resident account as an NRI is non-compliant and creates downstream issues (KYC freezes, tax notices, refund delays).

Three Account Types Compared

| Feature | NRO | NRE | FCNR |

|---|---|---|---|

| Funding Source | India-source income | Foreign earnings remitted to India | Foreign earnings (foreign currency) |

| India TDS on Interest | 30% default / 10% with DTAA | 0% (tax-free in India) | 0% (tax-free in India) |

| Japan Taxation for Resident | Yes, with FTC for Indian TDS | Yes (Indian exemption not recognized) | Yes (currency gains also taxable) |

| Repatriation | USD 1M/year cap with documentation | Freely repatriable | Freely repatriable |

Practical Setup Steps

- Within 6 months of departure: convert your existing Indian Resident Savings Account to NRO at your existing bank. Most major Indian banks (HDFC, ICICI, SBI, Axis, Kotak) support this conversion online or via embassy-attested documentation.

- Open NRE at the same or different bank to receive future foreign salary remittances tax-free in India.

- Consider FCNR if you plan to hold significant amounts in INR-hedge format (USD, GBP, EUR, JPY term deposits).

- Update KYC with current Japanese address proof and Japanese tax ID (if available).

- Submit DTAA documentation (Form 10F, TRC, No-PE declaration) to each bank to claim 10% TDS instead of 30% on NRO interest.

6. EPF, PPF, NPS: What Happens When You Move to Japan

These three Indian retirement accounts have very different mechanics for Japan-resident Indians.

EPF (Employees’ Provident Fund)

Most salaried Indians have an EPF balance accumulated from their Indian employment. After moving to Japan:

- Continuing contributions: not possible unless you are on detached-worker status under the Japan-India SSA (in force since October 2016).

- Withdrawal before age 58: subject to TDS in India and tax in Japan as foreign-source pension income.

- Withdrawal after age 58: tax-free in India for Indian residents, but for Japan residents the entire balance is principally Japan-taxable (with foreign tax credit for any Indian withholding).

- Keeping it dormant: EPF earns interest annually. Indian residents enjoy tax-free interest; for Japan residents, the annual interest is, in principle, Japan-taxable each year (though enforcement varies).

PPF (Public Provident Fund)

PPF accounts cannot be opened by NRIs, but existing PPF accounts opened while resident continue until maturity (15-year initial term). For Japan-resident Indians with existing PPF:

- Annual contributions: not permitted as NRI (technical compliance question — many banks allow continued contributions in practice, but it’s grey).

- Withdrawal at maturity: tax-free in India for Indian residents; for Japan residents, the entire maturity amount is principally Japan-taxable.

- Premature closure: not generally permitted, with limited exceptions for specific circumstances.

NPS (National Pension System)

NPS accounts can be opened and maintained by NRIs. For Japan-resident Indians:

- Continuing contributions: permitted as NRI through Tier-I and Tier-II accounts.

- Tax treatment: Indian deductions (Section 80C, 80CCD) apply only to Indian taxable income. For Japan-resident Indians with primarily Japanese income, the deduction benefit is limited.

- Withdrawal: same Japan-side taxation as EPF/PPF.

For most Indians moving to Japan, the rational EPF/PPF/NPS strategy is “hold and consolidate at withdrawal” rather than chase Indian tax benefits that no longer flow through to your effective Japan tax bill.

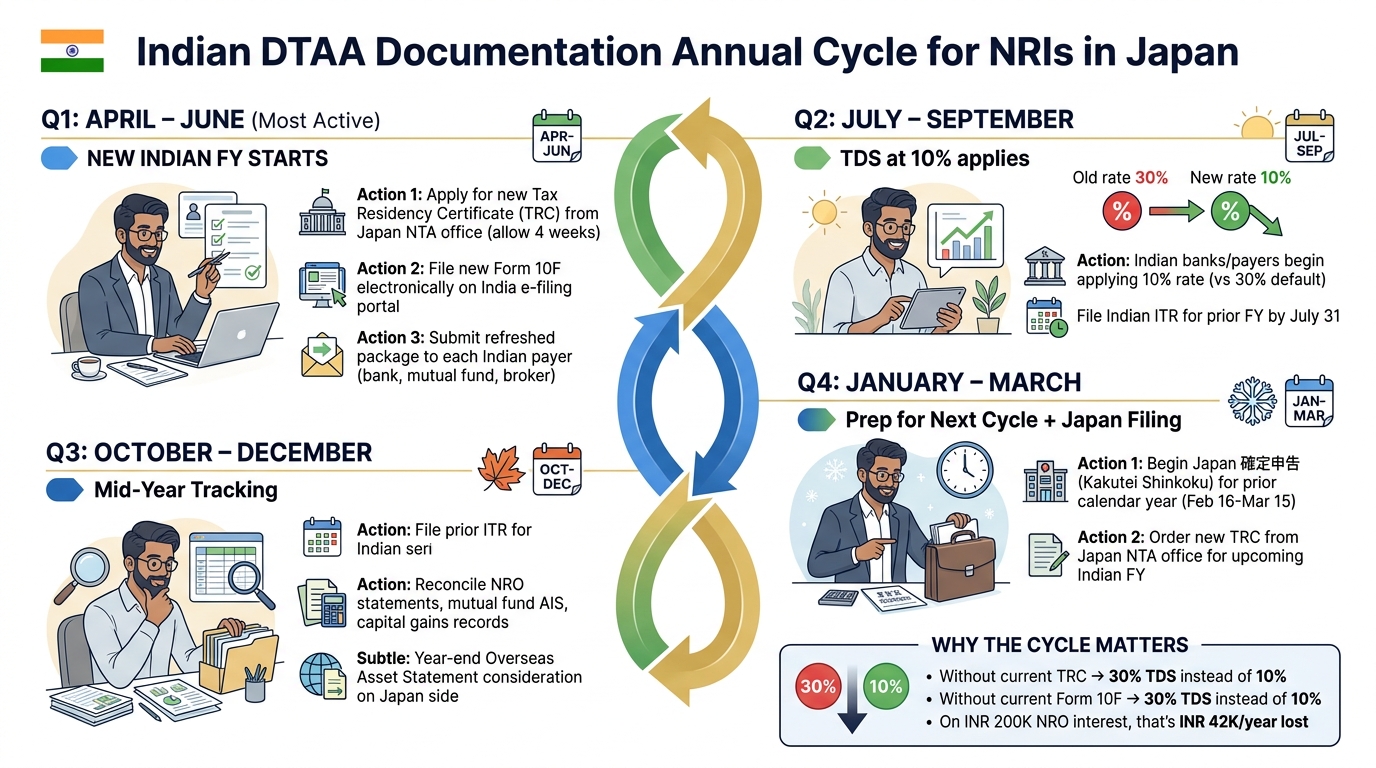

7. Indian DTAA Documentation Chain Every Year

The single most important annual recurring task for Indians in Japan: refresh the DTAA documentation chain so that NRO interest, mutual fund dividends, and other Indian-source income face only 10% TDS instead of 30%+.

The 4 Components

- PAN: One-time setup, but stays valid for life. If you don’t have PAN, obtain one before applying for treaty benefits.

- Form 10F: Self-declaration filed electronically each Indian financial year (April–March). Validity: one financial year.

- Tax Residency Certificate (TRC): Issued by Japan’s NTA upon request, certifying Japan tax residency for the relevant year. Apply through your local Japanese tax office. Processing time: 2–4 weeks. Validity: typically one calendar year.

- No-PE Declaration: Standard declaration stating no Permanent Establishment in India. Most Indian banks have their own format.

Where to Submit

The package must be on file with each Indian payer separately:

- Your Indian bank holding NRO/NRE/FCNR accounts.

- Each mutual fund house where you hold investments.

- Any Indian broker holding equity or bond positions.

- Any Indian client paying you fees for technical services.

- Indian property management agents collecting rent on your behalf.

Annual Refresh Routine

Most Indians-in-Japan refresh the documentation in late March / early April:

- Apply for new TRC from your Japanese tax office in February (allow 4 weeks).

- File new Form 10F electronically once TRC is received.

- Submit fresh package (PAN copy, Form 10F, TRC, No-PE declaration) to each Indian payer.

- Track each payer’s confirmation in a spreadsheet — Indian banks especially can lose paperwork.

8. Indian Rental Property from Japan

Many Indians moving to Japan retain Indian residential property — either an old family flat or an investment property. The compliance picture for NRI landlords:

India-Side

- TDS on rent paid to NRI: 30% on gross rent under Section 195. The tenant or rental agent withholds and remits to the Indian government.

- Net Indian tax: After filing your Indian ITR claiming standard deduction (30% of net rent), municipal taxes paid, and home loan interest, the actual net tax is typically much lower than the 30% TDS — and the over-withholding is refunded.

- Lower Deduction Certificate (LDC): For NRIs with predictable rental income and confirmed low net tax liability, you can apply to Indian Assessing Officer for an LDC reducing TDS to closer to your actual tax rate.

Japan-Side

- Non-permanent residents: Indian rental income is Japan-taxable only if remitted to Japan. Most Indians leave it in NRO and use it for Indian expenses, avoiding Japan tax until non-permanent status ends.

- Permanent-resident-status filers: Indian rental income is fully reportable on Japanese 確定申告 as foreign-source rental income, with Japanese expense rules and foreign tax credit for Indian tax paid.

For most Indian-in-Japan landlords, the rental income is profitable on a net basis once depreciation and home loan interest offset are claimed. The friction is mainly paperwork — TDS refund claims, LDC applications, and annual Japan reporting.

9. Indian IT Consulting Income from Japan

A common scenario: Indian IT or consulting professional living in Japan but providing services to Indian clients. The tax treatment hinges on how the engagement is structured.

Three Possible Characterizations

- Salary (employee): If you remain on an Indian payroll while in Japan, the salary is Japan-source income (work performed in Japan, under treaty Article 14). Your Indian employer should not withhold Indian TDS; the income is fully Japan-taxable. Coordinate with HR before the first post-departure paycheck.

- Fees for Technical Services / FTS: If you are an independent contractor or consultant under a services agreement, payments may fall under Article 12 of the DTAA (10% Indian TDS) or Article 7 (business profits — no Indian tax without PE).

- Royalty: If you transfer or license software intellectual property, payments may be characterized as royalty (10% under Article 12).

The “Make Available” Test

Modern Indian tax jurisprudence has narrowed the FTS definition: technical services must “make available” the underlying technical knowledge to the recipient — i.e., transfer of know-how, not just delivery of a result. For routine software development without IP transfer, many engagements can be characterized as business profits, escaping Indian TDS entirely (provided no Indian PE).

Strategic Choice

For Indian IT consultants based in Japan, the strategic decision is:

- Accept FTS characterization with 10% Indian TDS: simpler, but you give up 10% on every payment (recoverable via Japanese FTC, but creates working-capital drag).

- Structure as business profits with no Indian PE: zero Indian TDS, full Japanese taxation on net business profits. Requires careful contract drafting and clean separation from any Indian-based activities.

The choice depends on contract structure, risk tolerance, and the specific Indian client’s tax position. For large or recurring engagements, consult an Indian tax professional with international taxation experience.

10. Annual Filing Calendar for Indians in Japan

Once past Year 1, the annual rhythm for an Indian-in-Japan typically looks like:

| Month | Indian Tax Action | Japanese Tax Action |

|---|---|---|

| January–February | — | Apply for new TRC from local Japanese tax office (allow 4 weeks). |

| February 16 – March 15 | — | File 確定申告 for previous calendar year. Include Indian income with foreign tax credit. |

| April | File new Form 10F for new Indian FY. Submit refreshed DTAA package to each Indian payer. | — |

| July 31 | File Indian ITR (typically ITR-2) for previous financial year. Claim TDS refund if applicable. | — |

| Year-end | Reconcile NRO statements, mutual fund AIS, capital gains records. | File Overseas Asset Statement (国外財産調書) if assets >JPY 50M. |

11. FAQ: Indian Citizens Tax in Japan

Q1: I’m an Indian IT professional moving to Japan next month. What do I do this week?

Top three: (1) confirm with your Indian employer that they will not withhold Indian TDS on post-departure salary; (2) start the NRO conversion paperwork with your existing Indian bank; (3) gather your PAN, address proof, and visa documents — you’ll need them for both Indian compliance and Japanese resident registration.

Q2: My Indian employer says I have to keep paying Indian TDS while in Japan. Is that right?

Generally no. If your work is physically performed in Japan and you have NRI status, the salary is Japan-source income and your Indian employer should not withhold Indian TDS. You may need to provide your employer with a written declaration of your NRI status and Japanese tax residency. If they insist on Indian TDS, you’ll need to claim refund through Indian ITR — but the correct approach is to fix the withholding upfront.

Q3: How are ESOPs from my Indian employer taxed when I exercise them while in Japan?

ESOPs are taxed at two events: vesting (perquisite value taxable as employment income) and sale (capital gain taxable on disposal). The split between Indian and Japanese taxing rights depends on where the work was performed during the vesting period and where you are resident at exercise. This is one of the most common cross-border tax disputes — get specialist advice before exercising material ESOP positions.

Q4: Can I send money to my parents in India without tax issues?

Gifts to parents from Japan are generally not Japan-taxable for the recipient (gift tax in Japan applies to the recipient, but parents in India are not Japan-resident). India-side: gifts from defined relatives (parents, children, siblings, spouse) are exempt from Indian gift tax. Standard remittances to support parents are uncontroversial. Large lump-sum transfers (above LRS thresholds) may attract scrutiny under FEMA.

Q5: I have ULIPs (Unit Linked Insurance Plans) in India. How are they treated in Japan?

ULIPs are tax-deferred during the lock-in period in India under Section 10(10D) (for policies meeting prescribed conditions). For Japan-resident holders, the Japanese tax treatment of ULIP investment income is unclear — the conservative position is to declare annual investment gains, the aggressive position is to defer until policy maturity. Discuss with your Japan tax accountant.

Q6: I’m thinking of buying a property in India while living in Japan. Tax implications?

NRI property purchase in India is permitted with some restrictions (no agricultural land or plantation property). The purchase itself is not taxable. Ongoing rental income (if rented) is Indian-taxable with TDS at 30% on gross. On eventual sale, Indian capital gains apply, with TDS withholding by the buyer. Japan side: property income reportable on 確定申告 for permanent residents; subject to remittance rule for non-permanent residents.

Q7: My spouse is on a dependent visa. Does she need to file in India and Japan?

India: If your spouse has Indian-source income (interest on a joint NRO account, dividends, etc.) and total Indian income exceeds the basic exemption, she files separately. Japan: each spouse files individually under Japanese tax law. Some spouse-related deductions exist on the Japanese side if one spouse has limited income.

Q8: I want to invest in Japanese stocks. How do I report Indian income alongside Japanese stock gains?

Japanese stock gains for residents are reported on 確定申告. Indian income (NRO interest, Indian dividends, etc.) is also reported, with foreign tax credit for Indian withholding. Both sit on the same Japanese return for permanent-resident-status filers. For non-permanent residents, Indian income is excluded from Japanese tax base unless remitted — Japanese stock gains are always Japanese-source and fully taxable.

12. Get Expert Help for Indians in Japan

India-Japan tax planning combines two complex regimes with relatively few practitioners deeply experienced in both. The right professional combination is usually either (a) a single Japan tax accountant with multiple Indian client files, or (b) a coordinated team of one Indian CA familiar with NRI taxation and one Japanese 税理士 (zeirishi) who handles cross-border individual cases.

TaxMatch Japan introduces Indians to Japan tax accountants who have handled multiple India-Japan files — including NRI transition, EPF/PPF strategy, DTAA documentation flow, FTS contract structuring, and ongoing dual-jurisdiction annual filings. Initial introductions are free.

Common engagement profiles for Indians in Japan:

- Pre-move planning: NRI transition timing, NRO/NRE setup, EPF/PPF strategy, RSU/ESOP vesting analysis.

- First-year-in-Japan filings: Indian departure ITR + Japanese arrival 確定申告, DTAA documentation setup, foreign tax credit framework.

- IT consulting contract structuring: FTS vs business profits classification for Indian-client work, PE risk management.

- Ongoing annual coordination: Indian ITR + Japanese 確定申告 synchronization, foreign tax credit, overseas asset reporting, refresh DTAA documentation.

Free Matching for Indians in Japan

Tell us your situation and we’ll match you with a Japan tax accountant who has handled Indian client files. No fees, no obligation.

Prefer WhatsApp? Message us at +81 80-6075-2063

Related Guides

India-Japan DTAA Guide

The treaty mechanics article-by-article — withholding, FTS, capital gains

Japan Tax Residency 5-Year Rule

Non-permanent resident — the remittance rule that protects NRO income

Foreign Tax Credit in Japan

Claiming Indian TDS back on your Japanese return

Overseas Asset Reporting in Japan

JPY 50M threshold including NRO/NRE/FCNR/EPF balances

Japan Pension Lump-Sum Refund

If you later leave Japan — Japanese pension refund process