Working remotely from Japan — whether as a digital nomad, a foreign employee of an overseas company, or a freelancer serving international clients — creates tax obligations that are far more complex than most people expect. Japan does not use a simple “183-day rule” for tax residency; instead, it applies a domicile and livelihood test that can make you a tax resident from day one if you establish a home here. Once you are a tax resident, Japan taxes your worldwide income, even if every yen is earned from clients or employers outside the country. This guide covers every remote work scenario, including Japan’s Digital Nomad Visa introduced in 2024 and its unique tax treatment.

Remote Work Tax: Different scenarios, different obligations

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Remote work and cross-border tax rules are exceptionally complex and depend on bilateral tax treaties, individual visa status, and multiple jurisdictions. Always consult a qualified tax professional (税理士 / zeirishi) for advice specific to your situation.

Quick Summary

- Japan determines tax residency by domicile (住所) and livelihood center, not a 183-day count

- Foreign employees working remotely FROM Japan for overseas companies are taxed on worldwide income once tax resident

- Digital Nomad Visa holders (6-month stay) are not taxed on foreign-source income during their DN visa period

- Freelancers/contractors in Japan must file self-employment tax returns and may owe consumption tax

- Your overseas employer may create a Permanent Establishment (PE) risk in Japan by having you work here

Remote worker in Japan? Get your tax situation sorted.

Table of Contents

- Tax Residency Rules for Remote Workers

- Scenario 1: Working for an Overseas Employer from Japan

- Scenario 2: Japan-Based Employee Working Remotely

- Scenario 3: Digital Nomad on Tourist or Short-Term Visa

- Scenario 4: Freelancer/Contractor Working Remotely in Japan

- Japan’s Digital Nomad Visa (2024)

- Permanent Establishment (PE) Risk for Employers

- Social Insurance for Remote Workers

- Cross-Border Tax Complications

- Common Mistakes and Pitfalls

- Frequently Asked Questions

1. Tax Residency Rules for Remote Workers

The single most important factor in your Japan tax obligations is your tax residency status. Many remote workers assume Japan uses a 183-day rule (as many countries do), but Japan’s system is fundamentally different.

The Domicile Test (住所主義)

Japan determines tax residency based on where you have your domicile (住所 / jusho) — defined as your “principal place of livelihood” (生活の本拠). The NTA considers factors such as:

- Whether you have signed a residential lease or own property in Japan

- Whether your family lives with you in Japan

- Whether you have registered your address at the municipal office (住民登録)

- Whether you have a Japanese bank account, social insurance enrollment, and other life infrastructure

- The duration of your intended stay

Warning: The 183-Day Misconception

There is no “183-day rule” in Japanese domestic tax law. If you rent an apartment in Tokyo, register your address, and start working remotely on day one, the NTA can treat you as a tax resident immediately. The 183-day test exists only in certain bilateral tax treaties (like the US-Japan Treaty) as a tie-breaker for determining which country has primary taxing rights on employment income — it does not determine your Japan tax residency.

Three Categories of Tax Residents

| Category | Definition | What Is Taxed |

|---|---|---|

| Non-Resident | No domicile or residence in Japan | Only Japan-source income (flat 20.42% withholding) |

| Non-Permanent Resident (NPR) | Tax resident with domicile in Japan for ≤5 of past 10 years, without Japanese nationality | Japan-source income + foreign-source income remitted to Japan |

| Permanent Resident (tax) | Tax resident with domicile in Japan for >5 of past 10 years, or Japanese national | Worldwide income |

For a deep dive into NPR status and the remittance rule, see our Non-Permanent Resident & Remittance Rule Guide. For the 5-year rule details, see our Japan Tax Residency: 5-Year Rule Explained.

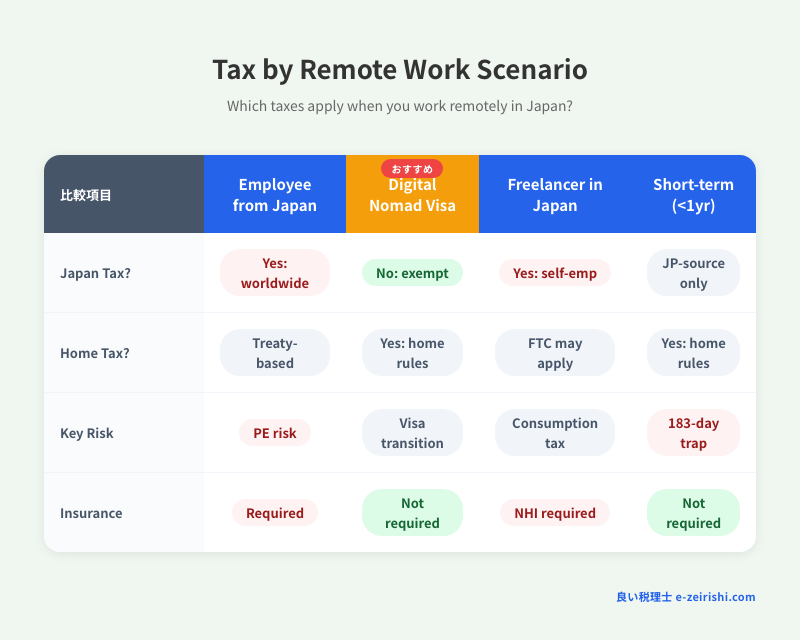

2. Scenario 1: Working for an Overseas Employer from Japan

This is the most common — and most misunderstood — remote work scenario. You have a job with a company in the US, UK, Singapore, or another country, and you physically perform the work from Japan.

Your Tax Obligations

| Factor | Status |

|---|---|

| Where is the income sourced? | Japan — employment income is sourced where the work is physically performed, regardless of where the employer is located or where you are paid |

| Japan income tax | Yes — progressive rates (5%–45% + 2.1% surtax + 10% resident tax) |

| Japan resident tax | Yes — flat 10% on prior-year income, billed by your municipality |

| Withholding by overseas employer | Typically NO — overseas employers without a Japan entity do not withhold Japanese tax. You must self-report and pay directly. |

| Home country tax | Depends on your citizenship and home country rules. US citizens: still must file US returns. Most other countries: no longer taxed once you are not a tax resident there. |

Key Implication: You Must File Your Own Tax Return

Unlike a normal employee in Japan where the employer withholds income tax monthly, an overseas employer typically does not withhold Japanese tax. This means you must:

- File a 確定申告 (kakutei shinkoku) tax return annually by March 15

- Pay estimated tax installments (予定納税) if your prior-year tax exceeded ¥150,000

- Report the income as employment income (給与所得) — same as domestic employment

- Claim the foreign tax credit if your home country also taxes this income

See our Tax Filing Guide for the step-by-step process.

Tip: NPR Status Advantage for Remote Workers

If you are a Non-Permanent Resident (in Japan ≤5 years), foreign-source income is only taxed if “remitted” to Japan. However, employment income for work performed in Japan is always Japan-source, even if your employer is overseas. NPR status does NOT exempt your salary. It only helps with other types of income (overseas investments, rental income, etc.).

3. Scenario 2: Japan-Based Employee Working Remotely

This is the most straightforward scenario: you work for a Japanese company (or a company with a Japan entity), and you work from home or a coworking space in Japan.

Tax Treatment

Identical to working at the office. Your employer:

- Withholds income tax monthly from your salary

- Performs year-end adjustment (年末調整) in December

- Pays your social insurance (health insurance + pension) as employer + employee split

- Reports your income to the municipality for resident tax

Remote Work Expense Deductions

Japan does not have a specific “home office deduction” for employees. However, since 2020, companies can provide tax-free remote work allowances (テレワーク手当) of a “reasonable amount” to cover internet, electricity, and office supplies used for work at home. If your company provides this, it is not included in your taxable income.

If your company does NOT provide an allowance and your work-related expenses are unusually high, you may qualify for the Specified Expenditure Deduction (特定支出控除) — but this requires expenses exceeding 50% of your employment income deduction, which is a very high bar for most employees.

4. Scenario 3: Digital Nomad on Tourist or Short-Term Visa

You enter Japan on a tourist visa (visa waiver), stay for 90 days, and work on your laptop the entire time for clients or an employer outside Japan.

Tax Residency: Generally Non-Resident

If you do not establish a domicile in Japan (no residential lease, no resident registration, no long-term intent to stay), you are generally treated as a non-resident for tax purposes. Non-residents are taxed only on Japan-source income.

Is Your Income “Japan-Source”?

This is the critical question:

| Income Type | Japan-Source? | Notes |

|---|---|---|

| Salary from overseas employer, work performed in Japan | Yes | Employment income is sourced where the work is performed. However, tax treaties may exempt short-stay employment (typically <183 days + employer has no PE in Japan + salary not borne by Japan entity). |

| Freelance income from overseas clients, work performed in Japan | Technically yes, but… | Self-employment income for services rendered in Japan is Japan-source. In practice, enforcement against short-stay nomads is minimal, but the legal obligation exists. |

| Investment income (dividends, capital gains) from overseas accounts | No | Investment income is sourced where the asset is located, not where you sit when you click “sell.” |

Practical Reality vs. Legal Theory

In practice, Japan has no mechanism to tax most short-stay digital nomads. There is no withholding agent, no employer reporting to the NTA, and no practical way for the tax office to know you worked from a cafe in Shibuya. However, this does not mean the legal obligation does not exist. If you transition from tourist to a work visa or Digital Nomad Visa, the NTA may examine your prior activities retroactively.

5. Scenario 4: Freelancer/Contractor Working Remotely in Japan

You live in Japan on a work visa (or spouse visa, PR, etc.) and work as an independent contractor for clients in Japan and/or overseas.

Tax Treatment

You are taxed as a self-employed individual (個人事業主). Key obligations:

| Obligation | Details |

|---|---|

| Business Registration | Submit 開業届 (kaigyou todoke) to your local tax office within 1 month of starting |

| Blue Return Application | Submit 青色申告承認申請書 within 2 months to claim the ¥650,000 special deduction |

| Income Tax | Progressive rates 5%–45% + 2.1% reconstruction surtax on business income (revenue minus expenses) |

| Resident Tax | Flat 10%, billed quarterly based on prior-year income |

| Consumption Tax (消費税) | Required if taxable sales exceed ¥10,000,000 in a base period (2 years prior). Rate: 10%. Under the Invoice System (2023+), being registered improves client relationships. |

| Social Insurance | National Health Insurance (NHI) + National Pension (国民年金) — no employer share, you pay 100% |

Deductible Expenses for Remote Freelancers

As a self-employed person, you can deduct business-related expenses including:

- Home office portion of rent, electricity, internet (proportional to space/time used for work)

- Equipment: Computer, monitor, desk, chair (items under ¥100,000 can be fully expensed)

- Software subscriptions: SaaS tools, cloud services, design software

- Communication: Phone bills, internet service (business portion)

- Coworking space fees

- Professional development: Books, courses, conferences

- Travel: Client meetings, business travel (domestic and international)

For the full freelancer tax guide, see our Freelancer Tax in Japan: Complete Guide.

6. Japan’s Digital Nomad Visa (2024)

Japan introduced the Digital Nomad Visa (特定活動 — デジタルノマド) on March 31, 2024, allowing remote workers from 49 eligible countries to stay in Japan for up to 6 months.

Eligibility Requirements

| Requirement | Details |

|---|---|

| Nationality | Citizen of one of 49 countries with tax treaties with Japan (includes US, UK, Australia, Canada, Germany, France, South Korea, etc.) |

| Income | Annual income of at least ¥10,000,000 (approximately $67,000 USD) |

| Work type | Remote work for employers or clients outside Japan. You cannot work for Japanese clients or employers. |

| Insurance | Must have private health insurance covering your stay in Japan (minimum ¥10M coverage) |

| Duration | Maximum 6 months, non-renewable (must leave for 6 months before reapplying) |

Tax Treatment of Digital Nomad Visa Holders

Key Advantage: No Japan Tax on Foreign-Source Income

Digital Nomad Visa holders are treated as non-residents for tax purposes during their DN visa period. Since all their income must be from sources outside Japan (that is the visa requirement), their income is not taxable in Japan. This is one of the most favorable tax treatments available to remote workers in Japan.

However, there are important caveats:

- No transition path: You cannot convert a DN visa to a work visa without leaving Japan. If you later return on a work visa, you become a tax resident.

- Consumption tax: If you provide digital services consumed in Japan (e.g., consulting for a Japanese company), consumption tax may apply even as a non-resident under the “reverse charge” mechanism.

- No social insurance: You are not enrolled in NHI or pension, hence the private insurance requirement.

- ¥10M income threshold: This effectively limits the visa to mid-to-senior professionals and excludes most entry-level remote workers.

7. Permanent Establishment (PE) Risk for Employers

When you work remotely from Japan for an overseas employer, your physical presence can create a Permanent Establishment (PE / 恒久的施設) for your employer in Japan. This is a serious corporate tax risk that many remote workers and their employers overlook.

What Creates a PE?

| PE Type | How Remote Work Can Trigger It | Risk Level |

|---|---|---|

| Fixed Place of Business | You work from a dedicated home office or coworking space in Japan for an extended period, at the employer’s direction | Medium–High (if >6 months) |

| Dependent Agent PE | You have authority to conclude contracts on behalf of your overseas employer while in Japan | High |

| Service PE | You provide services in Japan for more than 183 days in any 12-month period (some treaties) | Medium |

Consequences of PE Creation

If Japan determines your employer has a PE here, the employer must:

- File Japanese corporate tax returns and pay corporate tax on profits attributable to Japan

- Register for consumption tax and charge/collect on Japan-related services

- Withhold and remit your individual income tax

- Enroll you in Japanese social insurance (health insurance + pension)

Warning: This Can Get Your Employer in Trouble

Many overseas employers are unaware that allowing an employee to work from Japan creates PE risk. If the NTA determines a PE exists, the employer faces back taxes, penalties, and interest — potentially years’ worth. Some companies have policies explicitly prohibiting employees from working abroad for more than 30–90 days for this reason. Always disclose your situation to your employer.

8. Social Insurance for Remote Workers

Social insurance obligations depend on your employment arrangement:

| Scenario | Health Insurance | Pension |

|---|---|---|

| Employee of Japanese company (remote) | Company health insurance (健康保険) — employer pays half | Employees’ Pension (厚生年金) — employer pays half |

| Employee of overseas company (no Japan entity) | National Health Insurance (NHI / 国民健康保険) — you pay 100% | National Pension (国民年金) — ~¥16,980/month |

| Freelancer/self-employed | NHI — you pay 100% | National Pension — ~¥16,980/month |

| Digital Nomad Visa holder | Private insurance (required for visa) | Not enrolled |

For NHI details, see our Japan Health Insurance Guide for Foreigners.

Social Security Agreements (Totalization Agreements)

Japan has social security agreements with 23 countries (including the US, UK, Germany, Australia, France, and South Korea) that prevent double coverage. If your home country has an agreement with Japan and your overseas employer dispatches you to Japan temporarily, you may be exempt from Japanese pension/health insurance and remain covered under your home country system. You need a Certificate of Coverage from your home country’s social security agency.

9. Cross-Border Tax Complications

Double Taxation

If both Japan and your home country claim the right to tax the same income, you face double taxation. Relief is available through:

- Tax treaties: Japan has treaties with 80+ countries. These assign primary taxing rights and provide mechanisms to eliminate double taxation.

- Foreign tax credit (外国税額控除): Japan allows you to credit foreign taxes paid against your Japanese tax liability. See our Foreign Tax Credit Guide.

- Home country exemptions: Some countries (e.g., UK, Australia) stop taxing you once you are a non-resident there.

For country-specific guidance, see our Double Taxation Guide (US, UK & India).

Currency and Reporting

- All income must be reported in Japanese yen using the TTM rate on the date received (or a reasonable alternative rate)

- Overseas bank accounts with balances exceeding ¥50M must be reported on the Overseas Asset Report (国外財産調書)

- If total assets exceed ¥300M or ¥1B, the Wealth Report (財産債務調書) is required

10. Common Mistakes and Pitfalls

Mistake 1: Assuming You Are Not a Tax Resident Because You “Just Got Here”

The problem: Japan’s domicile test can make you a tax resident from day one if you establish a home. Signing a 1-year lease and registering your address = tax resident, regardless of how many days you have been here.

Mistake 2: Thinking Your Overseas Employer Handles Your Japan Taxes

The problem: Unless your employer has a Japan entity with payroll capability, nobody is withholding or paying your Japanese taxes. You are 100% responsible for filing and paying. Failure to file by March 15 triggers penalties of 15%–20% of tax owed.

Mistake 3: Not Declaring Foreign Bank Accounts and Assets

The problem: Once you are a Japan tax resident, you may need to report overseas assets. Japan participates in the Common Reporting Standard (CRS), meaning your foreign bank likely reports your account to the NTA automatically. Not declaring known assets triggers additional penalties.

Mistake 4: Working on a Tourist Visa and Then Transitioning to a Work Visa

The problem: If you worked for 3 months on a tourist visa, then switched to a work visa, the NTA may retroactively determine you were earning Japan-source income during those 3 months. If you did not declare that income, you face back taxes and penalties.

Mistake 5: Ignoring Consumption Tax as a Freelancer

The problem: If your taxable sales exceeded ¥10,000,000 two years ago, you are a consumption tax-registered business. This applies even if all your clients are overseas — though exports of services may be zero-rated. Not registering when required exposes you to back-assessed consumption tax.

Summary

- Japan determines tax residency by domicile (where you live), not a simple day count

- Remote workers for overseas employers are taxed on their salary in Japan and must self-file

- Digital Nomad Visa (6 months, ¥10M+ income) offers tax-free foreign-source income

- Freelancers must register as sole proprietors, consider Blue Return, and watch consumption tax thresholds

- Your presence in Japan can create PE risk for your overseas employer

- Social security agreements can prevent double coverage with your home country

- Use foreign tax credits and tax treaties to avoid double taxation

Remote worker tax situation keeping you up at night?

Or message us directly: WhatsApp

Frequently Asked Questions

Do digital nomads pay tax in Japan?

It depends on your visa and length of stay. If you hold Japan’s Digital Nomad Visa (introduced 2024), your foreign-source income is not taxed in Japan during the 6-month visa period. If you enter on a tourist visa and work remotely for less than 183 days without establishing a domicile, you are generally treated as a non-resident and your overseas employment income may be exempt under applicable tax treaties. However, establishing a domicile (signing a lease, registering an address) can trigger tax residency regardless of duration.

I work remotely from Japan for a US company. Do I pay Japan tax?

Yes. If you are a tax resident of Japan (you have a domicile here), your salary is subject to Japanese income tax regardless of where your employer is located. Employment income is sourced where the work is performed — in this case, Japan. Since your US employer likely does not withhold Japanese tax, you must file a tax return (確定申告) by March 15 and pay income tax, resident tax, and social insurance directly. You can claim a foreign tax credit for any US tax paid on the same income.

Will working from Japan create a PE for my overseas employer?

Potentially, yes. If you work from a fixed location in Japan for an extended period (typically more than 6 months), or if you have authority to conclude contracts on behalf of your employer, Japan may deem that your employer has a Permanent Establishment here. This would require your employer to file Japanese corporate tax returns and potentially register for consumption tax. The risk is higher for senior employees with decision-making authority. Always inform your employer about your work location.

Can I deduct home office expenses as a remote worker in Japan?

If you are self-employed (freelancer/sole proprietor), yes — you can deduct the business-use portion of rent, utilities, internet, and equipment. If you are an employee, Japan does not have a general home office deduction. Your employer may provide a tax-free remote work allowance, but you cannot unilaterally claim home office expenses as an employee unless your total work-related expenses exceed a very high threshold under the Specified Expenditure Deduction (特定支出控除).

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Cross-border tax rules are complex and depend on bilateral treaties, visa status, and individual circumstances. Always consult a qualified tax professional (税理士) for advice specific to your situation. Information is current as of March 2026.