If you’re a US citizen or Green Card holder working remotely from Japan for a US company, your tax situation just got materially more complex than the friends you left behind. You’re now subject to two parallel tax regimes — US worldwide tax (because of citizenship) and Japan resident tax (because of physical presence) — and the way they interact is not something most US employers, payroll providers, or even general American tax preparers understand well.

This guide is specifically for the US employer + Japan resident combination — not generic remote work, not Japanese employees abroad, not digital nomads on tourist visas. It walks through how your income is sourced, who taxes it first, how the US-Japan treaty resolves the overlap, the practical filing on both sides, and the most expensive mistakes Americans make in this exact setup.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. US and Japanese tax laws change frequently, and individual situations vary substantially. Always consult a qualified tax professional familiar with both jurisdictions for advice specific to your circumstances.

Need a US-Japan dual-qualified tax accountant?

Get matched with a specialist — free.

Table of Contents

- Who This Guide Is For

- The Big Picture: Two Tax Systems, One Paycheck

- Where Is Your Japan Income Taxed? Source-of-Income Rules

- The US-Japan Tax Treaty: How Double Tax Is Resolved

- Your Japan-Side Tax Obligations

- Your US-Side Obligations: FEIE vs. Foreign Tax Credit

- Social Security and the US-Japan Totalization Agreement

- The Self-Employment / Contractor Trap

- State Tax: California, New York, and the Sticky States

- Common Mistakes and US-Japan Penalty Triggers

- Frequently Asked Questions

- Get Expert Help With US-Japan Dual Taxes

1. Who This Guide Is For

You should read this guide if all of the following describe your situation:

- You hold US citizenship or a Green Card (lawful permanent residence in the United States).

- You are physically resident in Japan under a Spouse, Highly Skilled Professional, Working, Permanent Resident, or other long-term visa.

- Your employer is a US-incorporated company that has not registered a Japan branch or subsidiary for you.

- You receive W-2 compensation (or 1099-NEC if you’re a contractor — covered in Section 8).

- Your work is substantially performed from Japan, not on US business trips.

If you’re a Japanese citizen working remotely for a US company, the framework is similar on the Japan side but very different on the US side — you have no US tax obligation unless you have US-source income. If you’re a US citizen working in Japan for a Japan-based subsidiary, your situation is simpler (the local entity handles withholding). And if you’re on a Digital Nomad Visa or a tourist stay under 183 days, broader scenarios are covered in our Remote Work Tax in Japan guide.

Why This Combination Is Uniquely Painful

Three things make US citizen + Japan resident + US employer the hardest combination in modern remote work:

- The US taxes citizens worldwide. Most countries tax based on residency. The US is one of only two countries (Eritrea is the other) that taxes by citizenship. You owe US tax on your global income forever, regardless of where you live, until you renounce citizenship.

- Japan taxes residents worldwide too, once you become a Permanent Resident (after 5 years of any 10-year window) or while you are remitting income as a Non-Permanent Resident. Your salary from the US employer is fully taxable in Japan from day one.

- Your US employer’s payroll system was not designed for this. They withhold US federal tax, US state tax, FICA (Social Security + Medicare), and report it all on a W-2 — but they don’t withhold Japanese income tax, residence tax, or health insurance premiums. The Japan-side obligation falls entirely on you.

The combined burden, before any tax planning, can easily exceed 50% of gross income. With planning, it can settle to roughly what a US-resident equivalent would pay — but only if both sides are handled correctly.

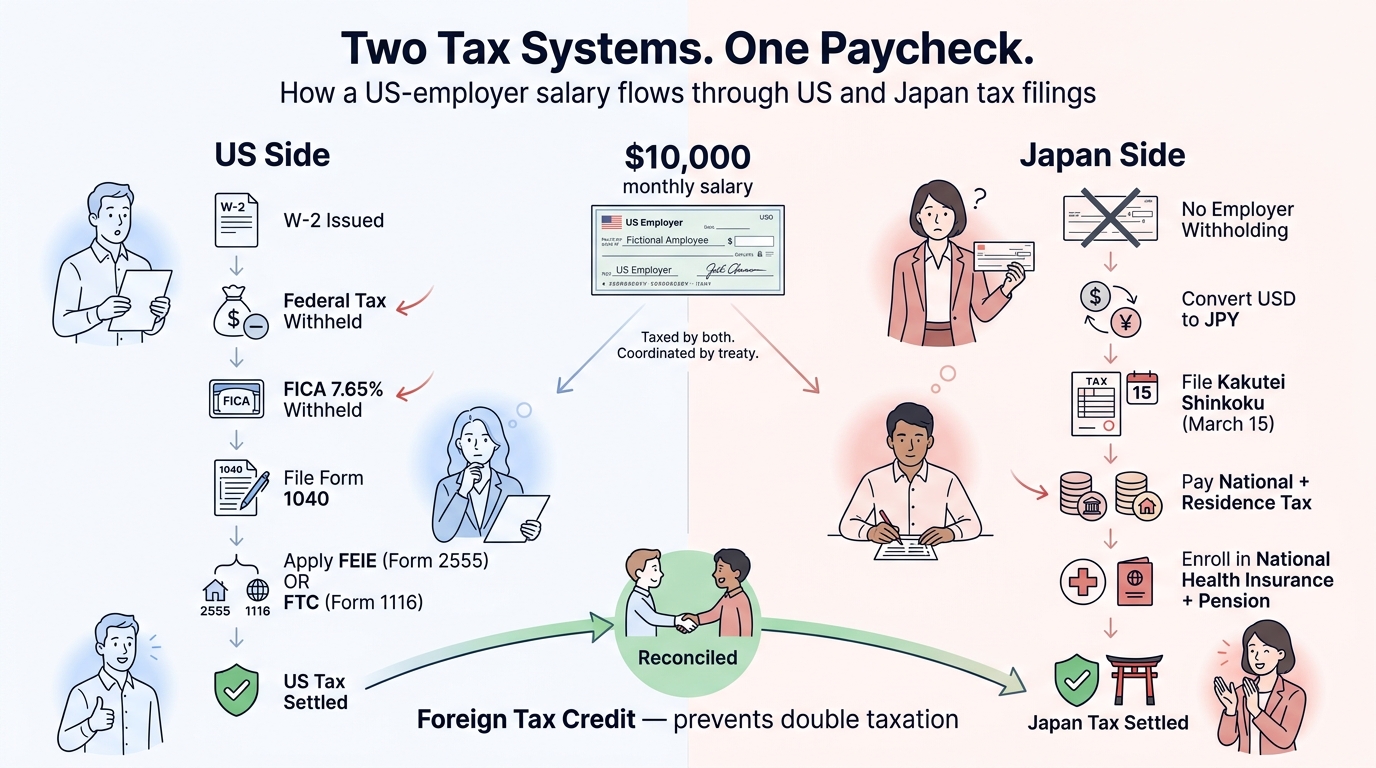

2. The Big Picture: Two Tax Systems, One Paycheck

Before the mechanics, the framework. Here’s what happens to a typical dollar of W-2 income paid by a US employer to a US citizen living in Japan:

| Step | What Happens | Who Acts |

|---|---|---|

| 1 | US employer pays salary in USD to your US bank | Employer |

| 2 | Employer withholds US federal tax, FICA (7.65%), and US state tax | Employer payroll |

| 3 | You file a US tax return (Form 1040) reporting the income | You |

| 4 | You file a Japanese tax return (kakutei shinkoku) reporting the same income | You |

| 5 | Japan calculates its tax (national + residence) at progressive rates | NTA & local municipality |

| 6 | You claim Foreign Tax Credit on either the US or Japan side to avoid double taxation | You (or your accountant) |

| 7 | Social Security obligation is resolved via the Totalization Agreement | You + employer |

The critical insight: steps 4–7 are entirely on you. Your US employer’s payroll system handles US federal/state/FICA — but Japan obligations, treaty application, and Totalization coordination are not their problem. If you don’t file in Japan, the NTA can — and increasingly does — match data through CRS/Article 26 treaty exchange and assess penalties (see Overdue Tax Filing in Japan).

The Default Outcome (No Planning)

If you do nothing — file US return only, ignore Japan — here’s what eventually happens:

- Japan-side: NTA notice, back tax assessment with 5–30% penalty plus 2.8–9.1% interest (see Overdue Tax Filing).

- US-side: You correctly paid US tax, but missed the chance to claim Foreign Tax Credit for the Japan tax you’ll eventually owe, paying double on the overlap.

- Cumulative effective tax rate: 60–75% of gross.

The Planned Outcome

With proper coordination, the combined burden looks like:

- Japan tax: ~20–45% of gross at Japan progressive rates (depending on income level)

- US tax: Largely or fully offset by FEIE and/or FTC

- Net cumulative: ~25–50% of gross, dominated by the Japan side

The delta between planned and unplanned is typically 15–25 percentage points of your gross income. On a $150,000 salary, that’s $22,500–$37,500 per year saved through correct tax filing.

3. Where Is Your Japan Income Taxed? Source-of-Income Rules

The starting point for every cross-border tax analysis is where the income is sourced. Both tax systems use a “where the work is performed” rule for compensation income, which is unambiguous in our case: you are physically working in Japan, so the income is Japan-source.

The US Source-of-Income Rule

Under Internal Revenue Code §861, compensation for personal services is sourced “where the services are performed.” If you perform services in Japan, the resulting compensation is foreign-source income for US tax purposes, even though your employer is in the US and pays you in USD into a US bank account.

This is the basis for two later mechanisms:

- Foreign Earned Income Exclusion (FEIE) — Form 2555 — allows you to exclude up to a per-year cap of foreign-source earned income.

- Foreign Tax Credit (FTC) — Form 1116 — allows you to credit foreign tax paid against US tax owed on that income.

Both presuppose your income is foreign-source. The fact that you’re physically in Japan when working is what makes it so — not the employer’s location.

The Japan Source-of-Income Rule

Japan applies essentially the same rule: compensation for services performed in Japan is Japan-source income (国内源泉所得 / kokunai gensen shotoku), taxable in Japan regardless of who pays it or where it’s paid from. For residents (anyone living in Japan with intent to remain for over one year), this is straightforward: 100% of your salary is taxable in Japan.

There is no minimum threshold — even a single day of services performed in Japan for a US employer generates Japan-source income for that day, in principle. In practice, the de minimis cases are absorbed without controversy, but anyone working primarily from Japan owes Japan tax on the entire compensation.

The W-2 Trap

Your W-2 will report your gross pay, US federal income tax withheld, FICA withheld, and (likely) US state income tax withheld. There is no line for “Japan-source amount” or “foreign tax withheld.” The W-2 is silent on the fact that your income is technically foreign-source — and most US employers’ payroll systems are not capable of producing a “shadow payroll” that calculates Japan-side withholding.

This is why the entire Japan-side filing falls on you. The W-2 is correct on its own terms (US payroll reporting); it just doesn’t capture what Japan needs.

4. The US-Japan Tax Treaty: How Double Tax Is Resolved

The US-Japan Income Tax Treaty (originally 2003, amended 2013 and ratified 2019) provides the framework that prevents the same dollar of income from being taxed twice at full rates. The key articles for our scenario — explained in fuller depth in our US-Japan Tax Treaty Practical Guide — are:

Article 14 — Income From Employment

Article 14 says (paraphrasing): compensation for services performed in a country may be taxed in that country. So Japan, as the country where services are performed, has the primary right to tax your remote-work compensation.

A short-stay exception applies if all three conditions are met:

- You are in Japan for 183 days or less in any 12-month period;

- Your compensation is paid by an employer not resident in Japan;

- The compensation is not borne by a Japan permanent establishment of the employer.

If all three apply, only the US taxes the income (and Japan does not). Almost no one this guide is written for qualifies — by definition you’re a Japan resident. The exception is mentioned only to dispel the myth that “the employer is in the US, so Japan can’t tax me.”

Article 23 — Avoidance of Double Taxation

Article 23 obligates each country to provide relief from double taxation through a credit mechanism. For Americans living in Japan, the practical result is:

- Japan taxes your salary first, at its progressive rates.

- The US also taxes it (because of the saving clause — see below).

- You claim a US Foreign Tax Credit (Form 1116) for the Japan tax paid against your US tax.

- The combined burden is roughly the higher of the two rates — typically the Japan rate at most income levels.

The Saving Clause

Article 1(4) of the treaty contains a “saving clause” — the United States reserves the right to tax its citizens and residents as if the treaty had not entered into force, except for specific carve-outs. The practical effect: as a US citizen, most treaty benefits do not actually reduce your US tax liability beyond what domestic US law already provides.

The saving clause is why FEIE and FTC matter so much for Americans in Japan: they are US domestic mechanisms (not treaty benefits) and therefore apply notwithstanding the saving clause. The treaty’s main practical role for US citizens is in the credit ordering rules (which country taxes first) and in Article 17 (Social Security), discussed in Section 7.

Article 26 — Exchange of Information

Article 26 authorizes the IRS and the NTA to exchange tax information about each other’s taxpayers. Under recent expansion, this includes automatic exchange of financial account data (the OECD Common Reporting Standard equivalent, though the US uses FATCA bilaterally). The practical implication: your US bank, brokerage, and 1099-issuer data flows to the NTA, and your Japanese bank account data flows to the IRS. Discrepancies between filings get noticed. See also our Overseas Asset Reporting (CRS) guide.

5. Your Japan-Side Tax Obligations

Japan has the primary taxing right and no employer is withholding Japanese tax on your behalf. The filing burden is entirely yours.

Annual Filing (Kakutei Shinkoku)

You must file an annual Japanese individual tax return for each calendar year:

- Form: Shinkokusho B (申告書B) — the standard individual return

- Deadline: March 15 of the following year (e.g., 2026 income → March 16, 2027 since March 15 is a Sunday)

- What you report: Full gross compensation from your US employer, converted to JPY using the year-average TTM exchange rate (or annual average from a sourceable rate table)

- Where to file: Your local tax office (zeimusho) or via e-Tax with a My Number card

A general step-by-step guide is in our Tax Filing Guide for Foreigners — but be aware that the standard form assumes Japan-based employer income with year-end adjustment already done. Foreign employer income goes in different boxes; if you’re not confident, use a bilingual tax accountant.

Estimated Tax Payments (Yotei Nozei)

If your prior year’s tax exceeded ¥150,000, you may be required to make estimated tax payments twice during the year — July 31 (first installment, ⅓ of the prior year’s tax) and November 30 (second installment, another ⅓). The remainder is settled at filing in March.

The NTA sends a yotei nozei notice in mid-June. You must pay it even if your income has changed materially — though you can apply for a reduction (genshin shōnin) if your current-year income is demonstrably lower.

Residence Tax (Juminzei)

In addition to national income tax, you owe residence tax at your local prefecture and municipality, calculated as ~10% of the prior year’s taxable income. This is billed the year following the income year — so 2026 income generates residence tax due in mid-2027. The bill arrives in June; you can pay in four quarterly installments or as a lump sum.

Critical for newcomers: your first year in Japan has zero residence tax, then in year 2 the bill hits as a delayed lump sum based on year-1 income. Budget for this.

For full mechanics, see our Residence Tax Guide.

Health Insurance and Pension

As a Japan resident without a Japanese employer to enroll you in shakai hoken (employer-based social insurance), you must enroll in:

- National Health Insurance (NHI) — premiums based on prior-year income, typically 8–12% of net income, capped at around ¥1.06M/year for high earners

- National Pension (kokumin nenkin) — flat ¥16,520/month in 2026

These are non-trivial — a $200K earner can owe ¥1.2–1.5M annually in NHI premiums alone, which is a deductible expense but still a real cash outflow.

If your US employer has a Japan subsidiary willing to put you on local payroll, you can join shakai hoken (the employee-based system), which is roughly equivalent in cost but covers more (including disability and certain unemployment benefits). For most US-employer remote workers, this is not an option.

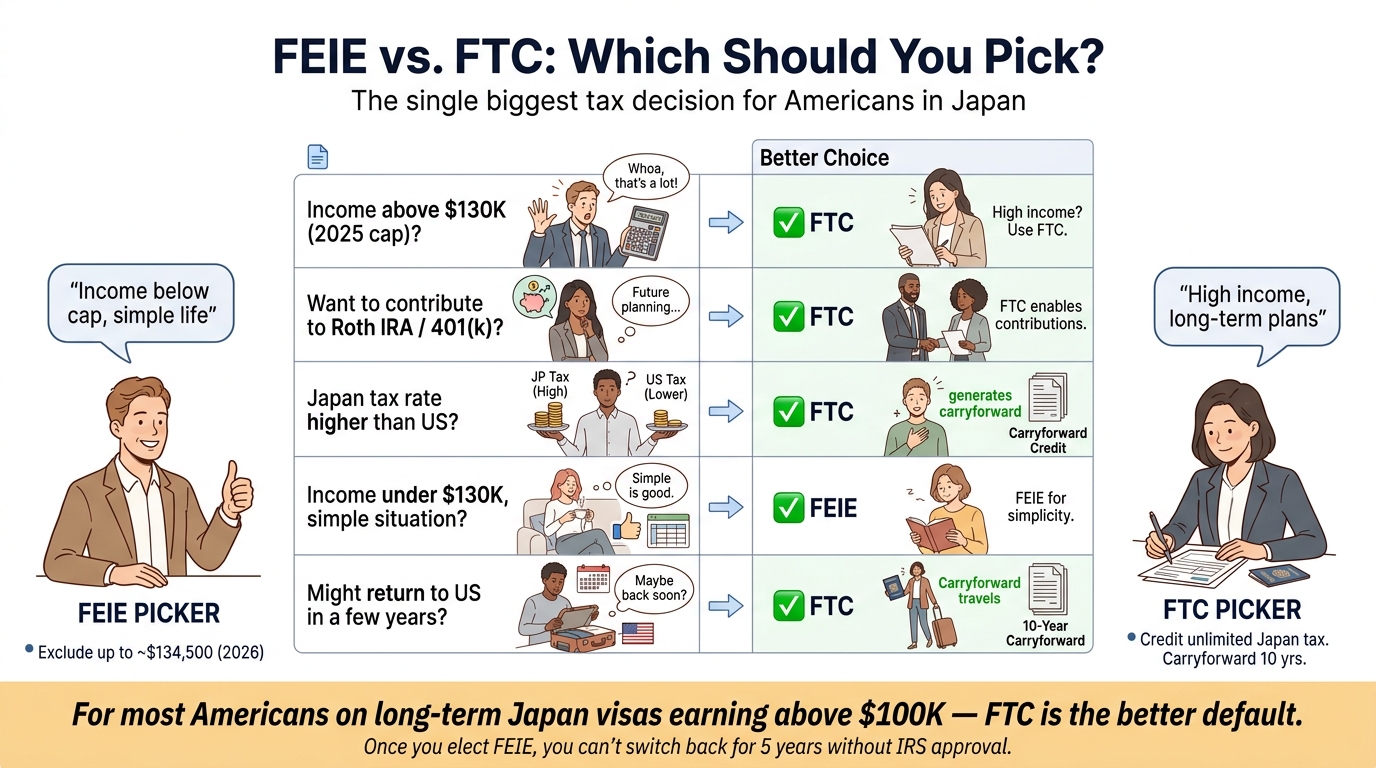

6. Your US-Side Obligations: FEIE vs. Foreign Tax Credit

Because the US taxes citizens worldwide, you continue filing a US Form 1040 every year. The question is how to relieve the double taxation on the Japan-source income that is fully taxable on both sides.

There are two relief mechanisms — Foreign Earned Income Exclusion (FEIE) and Foreign Tax Credit (FTC) — and choosing between them is the single most consequential tax-planning decision in this scenario.

Foreign Earned Income Exclusion (Form 2555)

The FEIE allows you to exclude foreign earned income from US taxation up to a per-year cap. Key 2026 numbers:

| Provision | 2025 Value | 2026 Value (est.) |

|---|---|---|

| Maximum exclusion | $130,000 | ~$134,500 (inflation-indexed) |

| Foreign Housing Exclusion base | $20,800 | ~$21,520 |

| Tokyo housing cap (FAQ-listed high-cost city) | ~$93,300 | ~$96,500 (TBD by IRS) |

To qualify, you must meet either:

- Bona Fide Residence Test — you are a resident of a foreign country for an uninterrupted period that includes an entire tax year, with intent to remain.

- Physical Presence Test — you are physically present in foreign countries for 330 full days in any 12-month period.

Most Japan-resident Americans on Spouse, PR, or long-term work visas easily satisfy the Bona Fide Residence test after the first full year.

Foreign Tax Credit (Form 1116)

The FTC allows you to credit the foreign tax you paid against your US tax on the same income. There is no income cap. The credit is calculated by income category (“basket”) — for our purposes, the “general” basket covers earned income.

The credit is dollar-for-dollar for foreign tax paid that does not exceed the US tax on the same foreign-source income. Excess credit can be carried back 1 year and forward 10 years.

When to Use Each

The decision tree:

| Your Situation | Generally Better Choice |

|---|---|

| Income mostly below FEIE cap, low housing cost area | FEIE — simpler, fully excludes |

| Income well above FEIE cap | FTC — covers entire amount, no income limit |

| High Japan income tax rate (>US rate at that bracket) | FTC — generates carryforward credit to use later |

| Want to contribute to Roth IRA / 401(k) | FTC — FEIE-excluded income doesn’t count as “earned income” for these contributions |

| Self-employed with significant business expenses | FTC — FEIE is per-person and limits other planning |

| Variable income, may return to US in a few years | FTC — carryforward credits travel with you |

In practice, for most Americans on Japan-resident long-term visas earning above ~$100K, FTC is the better default. FEIE is often more attractive on paper but loses to FTC when you account for IRA/401(k) contributions and credit carryforwards. Discuss with a tax accountant who handles US-Japan dual cases specifically.

The FTC Mechanics in Detail

For Japan-paid tax to be creditable against US tax, it must be:

- An income tax (or in lieu of income tax) — Japan national income tax and residence tax both qualify; National Health Insurance and pension contributions do not.

- Legally owed — voluntary over-payments are not creditable.

- Paid or accrued in the tax year — most expats use the accrual basis (Form 1116 election).

The credit calculation is essentially: (Foreign-source taxable income / Total taxable income) × US tax owed before credit = limit on FTC. Japan tax paid up to that limit is fully creditable; any excess generates a carryforward.

For high-income Americans in Japan, Japan tax rates often exceed US rates at the same income level, producing excess FTC carryforward that can offset future US tax in years with US-source income (e.g., a temporary return to the US, or a US-source capital gain).

Other US Filings to Remember

In addition to Form 1040, you likely also need:

- Form 8938 (Statement of Specified Foreign Financial Assets) — if foreign accounts exceed $200K at year-end / $300K at any time during year (for married filing jointly living abroad, double those thresholds)

- FBAR (FinCEN Form 114) — separate from your tax return, if any foreign account or aggregate of accounts exceeded $10K at any time during the year. See our FBAR Filing Guide

- Form 8621 — if you hold any Passive Foreign Investment Companies (PFICs), which most non-US-domiciled mutual funds are. This is a major trap — never buy non-US mutual funds while you’re a US citizen.

7. Social Security and the US-Japan Totalization Agreement

The US and Japan have a Social Security Totalization Agreement, in force since October 2005, designed to prevent double Social Security taxation and to coordinate benefit eligibility.

Default Rule Without Coordination

Without the agreement, a US citizen working in Japan for a US employer could owe both:

- US FICA (7.65% employee + 7.65% employer, on first $168,600 in 2024) — withheld automatically because the employer is US-based

- Japan social insurance (employee + employer rates combined ~30%, but for self-paying NHI + pension, ~10–15% of net) — required because you’re a Japan resident

Combined, that approaches 25–40% of gross income on top of income tax. The Totalization Agreement prevents this overlap.

How the Election Works

The agreement allows you to elect to pay social security in only one country based on assignment rules:

- 5-year assignment from US to Japan: If your US employer formally assigned you to Japan for ≤5 years, you can obtain a Certificate of Coverage from the US Social Security Administration and remain on US FICA only — exempt from Japan social insurance contributions.

- Indefinite assignment (your case if you’re a Japan resident): After the initial assignment period (or if you were never on assignment to begin with), you switch to Japan social insurance only and the US FICA withholding should stop.

The Practical Problem

In practice, US employers’ payroll systems almost universally continue to withhold FICA regardless of your Japan residency, because their HR doesn’t know how to issue or accept a Certificate of Coverage. You then face the burden of either:

- Getting your employer to stop FICA withholding (often requires escalation to HR or finance leadership), and instead enrolling yourself in Japan’s National Pension and National Health Insurance, OR

- Continuing to pay both and filing for a US FICA refund (which is messy and not always successful) plus enrolling in Japan NHI/pension anyway

Approach #1 is the correct path. The CoC is issued by the SSA at https://www.ssa.gov/international/CoC_link.html. The Japan side accepts it through your local Pension Office (Nenkin Jimusho) to exempt you from Japan social insurance, OR — once you’re past the assignment window — vice versa.

Most Americans in this exact scenario benefit from engaging a bilingual tax accountant or HR specialist familiar with Totalization to handle the employer-side and Japan-side coordination.

Self-Employment Note

If you are self-employed (1099 contractor — see Section 8) rather than W-2 employed, the Totalization Agreement still applies but the mechanics differ. As a self-employed US citizen abroad, you owe US self-employment tax (15.3%) on net SE income — unless covered by Totalization, in which case you owe Japan social insurance instead and are exempt from US SE tax.

8. The Self-Employment / Contractor Trap

A growing number of Americans in Japan are “1099 contractors” for US companies rather than W-2 employees. This often happens when a US company doesn’t want to set up Japanese payroll or worry about Permanent Establishment risk — they convert the relationship to independent contractor.

Why Companies Push for This

For the US employer, classifying you as a contractor:

- Eliminates FICA employer match (saves 7.65%)

- Eliminates state unemployment tax

- Eliminates benefits administration

- Reduces PE risk in Japan (theoretically — though see below)

For you, the consequences are significant:

Tax Impact of Being a Contractor

As a 1099 contractor:

- You owe self-employment tax (15.3%) on net income up to the FICA cap — this is the employer half of FICA that you now pay

- No employer benefits — health insurance, retirement match, paid time off all become your cost

- Japan-side: You’re a sole proprietor (kojin jigyo) and must register, file aoi-shinkoku (Blue Tax Return) if you want the ¥650K special deduction, and manage your own quarterly consumption tax if revenue exceeds ¥10M

- Totalization: SE tax can be exempted via Certificate of Coverage if you elect Japan social insurance — but most contractors don’t bother

For coverage of the Japan-side mechanics, see our Side Job Tax Rules — the framework applies whether the work is your main income or supplemental.

The PE Trap for Your “Employer”

Ironically, the contractor structure doesn’t actually eliminate Japan Permanent Establishment (PE) risk for the US company. If you’re effectively a full-time worker — using their email, attending their meetings, working their hours, treated as part of their team — Japan’s NTA may still find PE exists. This becomes the US company’s problem, not yours, but it can cause your engagement to be abruptly restructured or terminated when discovered.

The Right Move If You’re a Contractor

If you’ve been pushed onto 1099 status by your employer:

- Get a Certificate of Coverage to avoid SE tax (saves 15.3% on Japan-side income)

- Register as a sole proprietor in Japan and file Blue Tax Return for the ¥650K deduction

- Track and deduct legitimate business expenses — home office, equipment, professional dev, internet

- Negotiate higher gross compensation — a fair conversion from W-2 to contractor should add ~25–30% to gross to offset lost benefits and additional SE tax

- Consider forming a Japan LLC (合同会社 / GK) if your contractor income is consistently over ¥10M and you have multiple clients — see KK vs GK Guide

9. State Tax: California, New York, and the Sticky States

US federal tax follows citizenship; US state tax generally follows residency or domicile. Most states stop taxing you when you move away — but a few states make it remarkably hard to escape.

“Sticky” States

States that aggressively pursue former residents who claim to have moved:

| State | Stickiness Score | Why |

|---|---|---|

| California | Very sticky | Continues to tax until you can prove you severed all California ties — domicile change is hard |

| New York | Very sticky | Statutory residency rules; aggressively pursues high earners |

| New Jersey | Moderately sticky | Domicile-based, with documentation requirements |

| Massachusetts | Moderately sticky | Domicile-based |

| Virginia | Moderately sticky | Domicile-based |

If you moved from one of these states, simply filing a Japanese tax return doesn’t automatically sever your US state tax obligation. The state may continue to consider you a resident — and tax your worldwide income, including your remote Japan work — until you affirmatively change domicile.

How to Sever State Residency

To convincingly change domicile (especially from CA or NY):

- Surrender your driver’s license and obtain a new one in Japan (or your “new” US state if you maintained one)

- Re-register to vote elsewhere or not at all

- Close or move bank accounts out of the sticky state

- Sell or rent out any property in the state

- Update your federal tax address to a non-state address (Japan is fine)

- File a final part-year state return explicitly claiming non-residency going forward

- Document the move — keep evidence of where you spent each day in the first year after departure

This is a one-time effort but can save tens of thousands per year. For CA in particular, even years after a clean break, the Franchise Tax Board sometimes audits whether the change of domicile was bona fide. Documentation matters.

States That Don’t Tax Income

If you maintain a US presence in any of these, you have no state income tax obligation at all:

- Texas, Florida, Tennessee, Washington, Nevada, South Dakota, Wyoming, Alaska, New Hampshire (almost — limited to investment income for now)

Many remote workers headed for Japan establish or maintain an address in one of these states to neutralize state tax before the move.

10. Common Mistakes and US-Japan Penalty Triggers

The following mistakes are systematic — they happen to almost every US citizen + US employer + Japan resident at some point.

“My employer withholds federal tax, so I don’t owe Japan tax”

The single most common and most expensive misunderstanding. Your W-2 withholding covers US federal tax. Japan tax is owed in full on top, paid by you separately. Skipping it triggers overdue penalties at the rates covered in our Overdue Tax Filing guide.

“I’ll just file taxes when I move back”

Each unfiled Japan year accrues mukoshin kasanzei (5–30% penalty) plus entaizei (2.8–9.1% interest) starting day 1 after the deadline. Multi-year cleanups easily run into seven figures of penalties on substantial salaries.

Not coordinating FEIE/FTC consistently across years

Once you elect FEIE on a return, you must continue using it unless you formally revoke (which can lock you out for 5 years). Switching back and forth is not allowed. Plan the strategy at year 1 of your move.

Holding non-US mutual funds in a Japan brokerage

Foreign mutual funds (most Japanese investment trusts, including those held in NISA accounts) are PFICs under US tax law. Reporting them is brutal (Form 8621), tax treatment is punitive (mark-to-market or excess distribution regime), and most Americans don’t realize until they get audited. Do not buy non-US mutual funds while a US citizen. Hold US-domiciled ETFs in a US brokerage instead — even if the Japan side is less convenient.

Forgetting NISA tax treatment for US citizens

Japan’s NISA tax-advantaged investment account is not recognized by the US. Any gains in NISA are still fully US-taxable. Pairing NISA with US citizenship is the worst of both worlds — Japan won’t tax it, US will, and you may also have PFIC issues if you hold Japanese investment trusts inside.

Forgetting FBAR

If you opened a Japanese bank account, JP Post savings, or any brokerage and the aggregate balance exceeded $10K at any point during the year, you must file an FBAR by April 15 (auto-extended to October 15). The penalty for non-willful failure starts at $10,000 per year per missed filing. See our dedicated FBAR Filing Guide.

Not getting a Certificate of Coverage

Continuing to pay US FICA + Japan NHI/pension can mean overpaying social security by 15–25% of income. Get a CoC promptly after settling in Japan to fix this on a go-forward basis.

Forgetting state tax for sticky states

If you left CA/NY/NJ/MA without affirmatively changing domicile, the state may continue to tax you for years. Address this within the first 6 months of moving.

11. Frequently Asked Questions

Do I have to file in both the US and Japan?

Yes, every year. Two separate returns, filed independently of each other. Filing one does not satisfy the other. They are coordinated only through the FEIE / FTC mechanisms on the US side.

Can my US employer pay me in JPY to a Japanese bank account?

They can, but most won’t because their payroll system isn’t set up for foreign currency or foreign bank accounts. More commonly, you receive USD into a US bank and self-transfer to Japan. Be aware that bank-to-bank international wires generate FX cost and timing risk; consider Wise or Revolut for transfers.

What if my US employer wants to “set me up locally” in Japan?

If they’re willing to establish a Japan branch or subsidiary and put you on local payroll, take it — your tax life becomes radically simpler. Japan-side withholding is handled, you get shakai hoken (better than NHI+kokumin nenkin), and the Totalization mess largely disappears. Most US employers are unwilling to do this for a single employee, but if you’re at a growing-team stage, it’s worth pushing for.

Can I contribute to my US 401(k) while working from Japan?

Generally yes, if your US employer’s 401(k) plan allows it (most do — it’s based on US payroll). The contributions reduce your US taxable income but not your Japan taxable income (Japan doesn’t recognize 401(k) deferrals). You’ll owe Japan tax on the gross.

Can I contribute to a Roth IRA while working from Japan?

Only if you have “earned income” not excluded by FEIE. If you elect FEIE and your entire income is excluded, you have $0 of earned income for Roth purposes. Using FTC instead preserves your Roth eligibility — another point in favor of FTC for most expats.

What about my US state income tax — do I still owe it?

It depends on your state. From California, New York, and a few others, often yes, until you affirmatively change domicile. From most states, no — moving away is enough. See Section 9.

Should I renounce US citizenship to escape this?

Renunciation is a serious step with significant Exit Tax implications (if your net worth exceeds $2M or your average tax liability exceeds ~$200K, you may be a covered expatriate subject to the Exit Tax). It also requires a multi-year residency abroad and other criteria. It’s not a tax-planning move for most people, but for very high net worth expatriates committed to Japan long-term, it can make sense. See our Japan Exit Tax Guide for the Japan-side equivalent.

How do I find a tax accountant who handles US-Japan dual cases?

This is a specialized niche. You need someone (or a team) familiar with both US Form 1040 + Form 2555/1116 + Form 8938/FBAR/8621 AND Japan kakutei shinkoku + treaty positions. TaxMatch Japan maintains a vetted roster of dual-qualified practitioners — get matched free below.

12. Get Expert Help With US-Japan Dual Taxes

US citizen + US employer + Japan resident is, in tax terms, one of the most complex configurations a normal employee can find themselves in. There are six different forms to file in two countries, four separate elections that affect each other for years, and at least eight common pitfalls that compound expensively if missed.

The good news is that the framework is well-trodden — bilingual, US-tax-credentialed accountants handle hundreds of cases like yours every year. Once your first year is set up correctly, subsequent years become routine.

The right time to engage is at the start of your first full Japan tax year — ideally before March of the year following your arrival, so you can make the FEIE-vs-FTC decision deliberately and coordinate Totalization. If you’re already several years in and have been informal about the Japan side, see our Overdue Tax Filing guide — the cleanup is meaningful but resolvable.

TaxMatch Japan matches you with a bilingual tax accountant experienced in US-Japan dual filings, including FEIE/FTC optimization, Totalization Certificate of Coverage applications, and multi-year cleanups. Initial consultations are free; matching takes 1–2 business days.

Related Guides

US-Japan Tax Treaty Practical Guide

Full treaty mechanics: residency tie-breakers, credit ordering, treaty positions

FBAR Filing for US Citizens

$10K aggregate trigger, what to report, penalty avoidance

Overdue Tax Filing in Japan

Multi-year cleanup strategy if you missed Japan filings

Remote Work Tax: Other Scenarios

Generic remote work, Digital Nomad Visa, freelancer cases

Two countries. Six forms. One specialist who handles both.

Get Matched with a US-Japan Tax Specialist →

Or message us directly on WhatsApp