If you live in Japan on a spouse visa (配偶者ビザ / haigusha biza), you have unrestricted work rights — but your income level directly affects your household’s total tax burden, health insurance costs, and your Japanese spouse’s ability to claim valuable deductions. Earn too much and your spouse loses the ¥380,000 spouse deduction; earn just a little more and you are forced off your spouse’s company health insurance, adding hundreds of thousands of yen in annual costs. Understanding Japan’s system of “income walls” (年収の壁) is essential for every foreign spouse to make informed decisions about working in Japan.

The 4 Income Walls every foreign spouse should know

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Tax rules, social insurance thresholds, and deduction amounts are subject to legislative change. Always consult a qualified tax professional (税理士 / zeirishi) for advice specific to your situation.

Quick Summary

- Spouse visa holders have no work restrictions — you can work any job, any hours

- If your annual income stays below ¥1,030,000 (salary), your spouse keeps the full ¥380,000 spouse deduction

- The ¥1,300,000 wall is the biggest cliff: cross it and you must join your own health insurance + pension (~¥200,000+/year extra)

- Spouse special deduction phases out completely at salary of ~¥2,016,000

- Your filing obligations depend on whether you are employed (year-end adjustment) or self-employed (tax return required)

Need help understanding your tax situation as a foreign spouse?

Table of Contents

- Spouse Visa Basics: Work Rights and Tax Status

- The Income Walls Explained

- Spouse Deduction (配偶者控除)

- Spouse Special Deduction (配偶者特別控除)

- Social Insurance: The ¥1,300,000 Cliff

- Your Own Income Tax Obligations

- Common Scenarios for Foreign Spouses

- NHI and Pension: Dependent vs. Independent

- How This Affects Permanent Residency Applications

- Common Mistakes

- Frequently Asked Questions

1. Spouse Visa Basics: Work Rights and Tax Status

The Spouse or Child of Japanese National visa (日本人の配偶者等) is a Table 2 status of residence. This classification has two important implications:

Work Rights

Unlike Table 1 work visas (Engineer, Specialist in Humanities, etc.), a spouse visa imposes no restrictions on work activities. You can:

- Work part-time or full-time at any job

- Work in any industry (including manual labor, service industry, entertainment)

- Start your own business without a separate Business Manager visa

- Work for multiple employers simultaneously

- Freelance or work as an independent contractor

Tax Residency Status

As a Table 2 visa holder, you are a tax resident from day one. Unlike Table 1 visa holders who may qualify as “Temporary Foreigners” for gift and inheritance tax purposes, spouse visa holders face:

- Immediate worldwide income tax liability once you are a permanent tax resident (>5 years in Japan)

- Immediate worldwide gift/inheritance tax liability regardless of how long you have been in Japan

- If you have been in Japan ≤5 years, you are a Non-Permanent Resident — foreign-source income is only taxed if remitted to Japan

For more on NPR status, see our Japan Tax Residency: 5-Year Rule Guide.

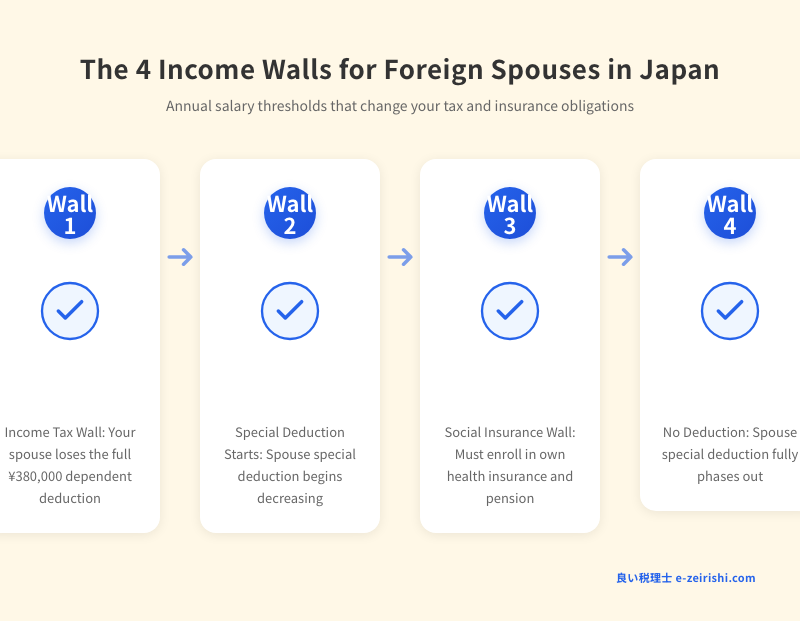

2. The Income Walls Explained

Japan’s tax and social insurance system creates several thresholds — colloquially called “walls” (壁) — where crossing a specific income level triggers a disproportionate increase in costs. Understanding these walls is critical for deciding how much to work.

| Wall | Annual Salary Threshold | What Happens When You Cross It | Approximate Cost Impact |

|---|---|---|---|

| ¥1,030,000 | 合計所得 ¥480,000 | Your spouse loses the full spouse deduction (配偶者控除). You begin paying income tax on your own income. | Your spouse’s tax increases by ~¥38,000–¥125,400/year (depending on their tax bracket) |

| ¥1,060,000 | 合計所得 ¥510,000 | Spouse special deduction starts decreasing from ¥360,000 | Gradual increase |

| ¥1,030,000 (resident tax) | 合計所得 ¥450,000 | You begin paying resident tax (住民税) on your own income | ~¥5,000–¥10,000+ (varies by municipality) |

| ¥1,300,000 | N/A (gross income test) | You are removed from your spouse’s company health insurance (被扶養者). You must enroll in NHI + National Pension independently. | ~¥200,000–¥400,000+/year in new insurance + pension costs |

| ¥1,500,000 | 合計所得 ¥950,000 | Spouse special deduction drops to ¥30,000 (minimal benefit) | Your spouse’s deduction benefit is nearly gone |

| ~¥2,016,000 | 合計所得 ¥1,330,000 | Spouse special deduction fully phases out to ¥0 | No more deduction benefit for your spouse |

Warning: The ¥1,300,000 Wall Is the Most Dangerous

The ¥1,300,000 social insurance wall creates a “dead zone” where earning ¥1,300,001 costs you more in insurance premiums than the extra income is worth. A person earning ¥1,290,000 may take home more money than someone earning ¥1,500,000, because the ¥1,500,000 earner must pay ~¥200,000+ in NHI + pension. You need to earn approximately ¥1,600,000–¥1,700,000+ before the extra income clearly outweighs the lost social insurance coverage.

3. Spouse Deduction (配偶者控除)

When your total income (合計所得金額) is ¥480,000 or less — which corresponds to a salary of approximately ¥1,030,000 or less — your Japanese spouse can claim the spouse deduction on their tax return.

How Much Your Spouse Saves

| Your Spouse’s Total Income | Income Tax Deduction | Resident Tax Deduction | Estimated Annual Tax Savings |

|---|---|---|---|

| ≤ ¥9,000,000 | ¥380,000 | ¥330,000 | ¥71,000–¥159,000 |

| ¥9,000,001–¥9,500,000 | ¥260,000 | ¥220,000 | ¥48,000–¥108,000 |

| ¥9,500,001–¥10,000,000 | ¥130,000 | ¥110,000 | ¥24,000–¥54,000 |

| Over ¥10,000,000 | ¥0 | ¥0 | No deduction available |

Key point: The spouse deduction benefits the higher-earning spouse (the one claiming it), not you directly. If your Japanese spouse earns ¥7,000,000 (20% tax bracket), the ¥380,000 deduction saves them about ¥109,000/year in combined income and resident tax.

4. Spouse Special Deduction (配偶者特別控除)

If your income exceeds ¥480,000 (salary above ~¥1,030,000), your spouse cannot claim the regular spouse deduction — but they may still claim the spouse special deduction (配偶者特別控除), which gradually decreases as your income rises:

| Your Total Income (合計所得) | Your Approx. Salary | Deduction (spouse income ≤ ¥9M) |

|---|---|---|

| ¥480,001–¥500,000 | ~¥1,030,001–¥1,050,000 | ¥380,000 (same as full deduction!) |

| ¥500,001–¥550,000 | ~¥1,050,001–¥1,100,000 | ¥360,000 |

| ¥550,001–¥600,000 | ~¥1,100,001–¥1,150,000 | ¥310,000 |

| ¥600,001–¥667,000 | ~¥1,150,001–¥1,217,000 | ¥210,000 |

| ¥667,001–¥833,000 | ~¥1,217,001–¥1,383,000 | ¥160,000 |

| ¥833,001–¥900,000 | ~¥1,383,001–¥1,450,000 | ¥110,000 |

| ¥900,001–¥950,000 | ~¥1,450,001–¥1,500,000 | ¥60,000 |

| ¥950,001–¥1,000,000 | ~¥1,500,001–¥1,550,000 | ¥30,000 |

| ¥1,000,001–¥1,330,000 | ~¥1,550,001–¥2,016,000 | ¥0 |

Notice: The ¥1,030,000–¥1,050,000 “Safe Zone”

If your salary is between ¥1,030,001 and ¥1,050,000, your spouse still gets the full ¥380,000 deduction through the spouse special deduction. The actual deduction does not decrease until your income exceeds ¥500,000 (salary ~¥1,050,000). This means the ¥1,030,000 wall is softer than many people think — you can earn slightly more without any impact on your spouse’s deduction.

5. Social Insurance: The ¥1,300,000 Cliff

The most financially impactful threshold for foreign spouses is the social insurance dependency limit. If your Japanese spouse is enrolled in company health insurance (健康保険 / Employees’ Health Insurance), you can be covered as a dependent (被扶養者) at zero additional cost — as long as your annual income stays below ¥1,300,000.

What You Get as a Social Insurance Dependent

- Health insurance: Full coverage under your spouse’s plan — no premiums, same benefits

- Pension: Covered as a “Category 3 insured person” (第3号被保険者) under the National Pension — no premiums, but you accumulate pension credits

- Total cost to you: ¥0/month

What Happens When You Exceed ¥1,300,000

Once your annual income (or projected annual income based on current monthly earnings) exceeds ¥1,300,000:

- You are removed from your spouse’s health insurance

- If employed: You join your employer’s health insurance + Employees’ Pension (company pays half)

- If self-employed or part-time: You must enroll in National Health Insurance (NHI) + National Pension at your own expense

Cost Comparison

| Income Level | Health Insurance Cost | Pension Cost | Total Annual Insurance |

|---|---|---|---|

| ¥1,290,000 (below wall) | ¥0 (dependent) | ¥0 (Category 3) | ¥0 |

| ¥1,400,000 (above wall, NHI) | ~¥100,000–¥150,000 | ~¥203,760 | ~¥300,000–¥350,000 |

The person earning ¥1,290,000 takes home more than the person earning ¥1,400,000 after insurance costs.

Important: The ¥1,060,000 Social Insurance Wall for Large Companies

If your employer has 51+ employees (lowered from 101 in October 2024), the social insurance threshold drops to ¥1,060,000 (monthly ¥88,000+). You must enroll in Employees’ Health Insurance + Pension if you work 20+ hours/week, earn ¥88,000+/month, and are expected to be employed for 2+ months. This makes the ¥1,300,000 wall irrelevant — the wall hits much earlier.

6. Your Own Income Tax Obligations

If You Are Employed (Part-Time or Full-Time)

Your employer handles tax through monthly withholding and year-end adjustment:

- Annual salary under ¥1,030,000: No income tax owed (employment income deduction of ¥550,000 + basic deduction of ¥480,000 = ¥1,030,000 tax-free)

- Annual salary ¥1,030,001+: Income tax applies on the excess. Your employer withholds monthly and reconciles at year-end.

- No tax return needed if you have one employer and salary is ≤ ¥20,000,000

If You Are Self-Employed or Freelancing

You must file a tax return (確定申告) annually by March 15:

- Register as a sole proprietor (開業届)

- Apply for the Blue Return (青色申告) for the ¥650,000 special deduction

- Deduct all business expenses from revenue

- Pay income tax, resident tax, and (if applicable) consumption tax

For the complete freelancer guide, see Freelancer Tax in Japan.

If You Have Multiple Income Sources

If you have employment income from one employer AND side income exceeding ¥200,000/year (freelance work, online sales, rental income, etc.), you must file a tax return. See our Side Job Tax Rules Guide for details.

7. Common Scenarios for Foreign Spouses

Scenario A: Stay-at-Home Parent

Income: ¥0

- Your spouse claims the full ¥380,000 spouse deduction

- You are covered as a social insurance dependent (¥0 cost)

- No tax filing required

- You accumulate National Pension credits (Category 3) for free

Scenario B: Part-Time Worker (Under ¥1,030,000)

Income: ¥800,000–¥1,030,000/year

- Your spouse still claims the full ¥380,000 spouse deduction

- You remain a social insurance dependent (¥0 cost)

- No income tax owed (below tax threshold)

- Resident tax may apply in some municipalities if income exceeds ~¥930,000–¥1,000,000

This is often considered the “sweet spot” for maximizing household income without triggering any walls.

Scenario C: Part-Time Worker (¥1,030,000–¥1,300,000)

Income: ¥1,100,000–¥1,290,000/year

- Your spouse claims spouse special deduction (reduced but still significant)

- You remain a social insurance dependent (¥0 insurance cost) if under ¥1,300,000

- You owe modest income tax + resident tax

- Household still benefits overall from the extra income

Scenario D: Full-Time Worker (Above ¥1,600,000+)

Income: ¥2,000,000+/year

- Your spouse gets no spouse deduction (phased out entirely)

- You have your own health insurance + pension (employer-sponsored if employed full-time)

- You file independently or through year-end adjustment

- Household income is clearly higher — the “walls” are only a concern in the ¥1,030,000–¥1,600,000 range

Scenario E: Freelancer Foreign Spouse

Income: Variable

- Income is measured as revenue minus expenses (not gross revenue)

- If business income (所得) is under ¥480,000, your spouse can claim the spouse deduction

- Social insurance dependency for freelancers is measured on revenue minus expenses for NHI purposes — check with your spouse’s health insurance society for exact rules

- Blue Return special deduction (¥650,000) is included in reducing your total income for spouse deduction purposes

Tip: Freelancer Advantage

As a freelancer, your “income” is revenue minus expenses (and minus the Blue Return deduction). A freelancer with ¥2,000,000 in revenue but ¥1,000,000 in legitimate expenses and a ¥650,000 Blue Return deduction has total income of only ¥350,000 — well below the ¥480,000 threshold. Your spouse can still claim the full spouse deduction even though you are generating significant revenue.

8. NHI and Pension: Dependent vs. Independent

As a Social Insurance Dependent

While your income is below the threshold (¥1,300,000 for most, ¥1,060,000 if your employer has 51+ employees):

- Health insurance: Covered under your spouse’s plan at no cost. Same benefits as your spouse.

- Pension: Category 3 insured person — no premiums, but you earn pension credits. Current basic pension benefit for 40 years of Category 3: approximately ¥816,000/year (2026 rates).

When You Must Enroll Independently

If your income exceeds the threshold and you do not qualify for employer-sponsored insurance:

- National Health Insurance (NHI): Premiums based on prior-year income + number of household members. Varies significantly by municipality but typically ¥80,000–¥300,000+/year.

- National Pension (国民年金): Flat rate of approximately ¥16,980/month (¥203,760/year in 2026).

For full NHI details, see our Japan Health Insurance Guide.

9. How This Affects Permanent Residency Applications

If you plan to apply for Permanent Residency (永住権), your tax and social insurance compliance is directly scrutinized by Immigration. Key requirements:

| Requirement | What Immigration Checks |

|---|---|

| Tax compliance | Resident tax payment certificates (課税証明書 + 納税証明書) for the past 5 years. Late payments or non-payment are grounds for denial. |

| Social insurance compliance | Proof of pension enrollment and payment for the past 2+ years. If you should have been paying National Pension but were not, this is a problem. |

| Income stability | Your household income (combined with spouse) should demonstrate financial stability. There is no strict minimum for spouse visa PR applicants, but having zero income for years may raise questions. |

Tip: Spouse Visa PR Application

Spouse visa holders can apply for PR after 3 years of marriage and 1 year of continuous residence in Japan (compared to 10 years for most other visa categories). However, even with this shorter path, tax and pension compliance is strictly enforced. Make sure all resident tax payments are current and pension premiums are paid on time.

10. Common Mistakes

Mistake 1: Not Registering as a Dependent for Social Insurance

The problem: Many foreign spouses are unaware they can be added to their Japanese spouse’s company health insurance as a dependent. They instead enroll in NHI and pay premiums unnecessarily. Contact your spouse’s HR department to register as a dependent — it is free and provides identical coverage.

Mistake 2: Accidentally Crossing the ¥1,300,000 Wall

The problem: Working overtime in December pushes your annual income past ¥1,300,000. You lose social insurance dependency for the following year. Track your cumulative income carefully throughout the year.

Mistake 3: Not Filing a Tax Return When Required

The problem: If you have income from multiple sources (two part-time jobs, freelance work, etc.) or self-employment income, you must file a tax return. Relying solely on year-end adjustment from one employer when you have other income is non-compliance.

Mistake 4: Confusing Income Tax Thresholds with Social Insurance Thresholds

The problem: The ¥1,030,000 wall (income tax) and the ¥1,300,000 wall (social insurance) are completely separate systems with different calculations. Staying under ¥1,030,000 for tax purposes does not automatically keep you under the social insurance threshold, and vice versa.

Mistake 5: Not Paying National Pension After Losing Dependent Status

The problem: After exceeding ¥1,300,000 and losing Category 3 status, you must enroll in National Pension (or your employer’s Employees’ Pension). Failing to enroll leaves gaps in your pension record, which affects your permanent residency application and future pension benefits.

Want to optimize your household tax situation?

Get Matched with an English-Speaking Tax Accountant — Free →

Or message us directly: WhatsApp

Frequently Asked Questions

Can I work on a spouse visa in Japan?

Yes. The Spouse or Child of Japanese National visa (配偶者ビザ) is a Table 2 status of residence with no work restrictions. You can work any job, any number of hours, in any industry. You can also start your own business without needing a separate Business Manager visa. This is one of the most flexible visa categories in Japan.

How much can I earn before my spouse loses the spouse deduction?

Your spouse keeps the full spouse deduction (配偶者控除, ¥380,000) as long as your total income (合計所得金額) is ¥480,000 or less, which corresponds to a salary of approximately ¥1,030,000 or less. If you earn more than this, your spouse can still claim the spouse special deduction (配偶者特別控除), which gradually decreases and phases out completely when your salary reaches approximately ¥2,016,000.

What is the ¥1.3 million wall?

The ¥1,300,000 wall (130万円の壁) is the social insurance threshold. If your annual income is below ¥1,300,000, you can remain on your Japanese spouse’s company health insurance as a dependent at no cost, and you are covered under the National Pension as a Category 3 insured person (also free). Once your income exceeds ¥1,300,000, you must enroll in your own health insurance and pension, adding approximately ¥200,000–¥400,000 per year in costs. Note: For employees at companies with 51+ staff, this threshold drops to ¥1,060,000.

Does my income affect my permanent residency application?

Yes, indirectly. Immigration checks your tax compliance (resident tax payment certificates for 5 years) and social insurance compliance (pension payment records for 2+ years). Having no income is not automatically disqualifying for spouse visa PR applicants, but you must demonstrate household financial stability and perfect compliance with tax and pension obligations. Late payments or non-enrollment in pension are common reasons for PR denial.

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax rules, social insurance thresholds, and immigration requirements change frequently. Always consult a qualified tax professional (税理士) and immigration specialist for advice specific to your situation. Information is current as of March 2026.