If your investment thesis includes short-term rental (Airbnb/minpaku), the tax framework differs significantly — see our Minpaku/Airbnb Tax for Foreign Hosts guide.

Japan’s real estate market continues to offer foreign investors an extraordinary combination: positive yield spreads, unrestricted freehold ownership, and aggressive depreciation mechanics that can shelter cash flows for years. But extracting full value from these structural advantages requires precise entity selection, disciplined tax planning, and awareness of the 2026 regulatory shifts that are reshaping the landscape. This guide is written for sophisticated investors who already understand the basics of Japanese property taxes. It focuses on what matters most: how to structure, optimize, and exit Japanese real estate investments as a non-resident or offshore fund.

New to Japanese real estate taxes? This article assumes familiarity with acquisition tax, fixed asset tax, and rental income basics. For foundational concepts, see our Complete Guide to Real Estate Tax in Japan for Foreigners first.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Real estate investment structures involve complex corporate, securities, and tax regulations. Always consult a qualified tax professional (税理士 / zeirishi) and legal counsel before implementing any investment strategy discussed here.

Need a bilingual tax accountant for real estate investment?

Get matched with a specialist in cross-border property taxation — free.

Table of Contents

- Investment Entity Structures Compared

- The GK-TK Pass-Through Structure

- Depreciation Strategies & the Wooden Building Hack

- Non-Resident Investor Framework

- Cross-Border Taxation & Treaty Benefits

- Financing & Interest Deductions

- Exit Strategies & Capital Gains Optimization

- 2026 Regulatory Changes

- Portfolio Scenarios with Numbers

- Common Investor Mistakes

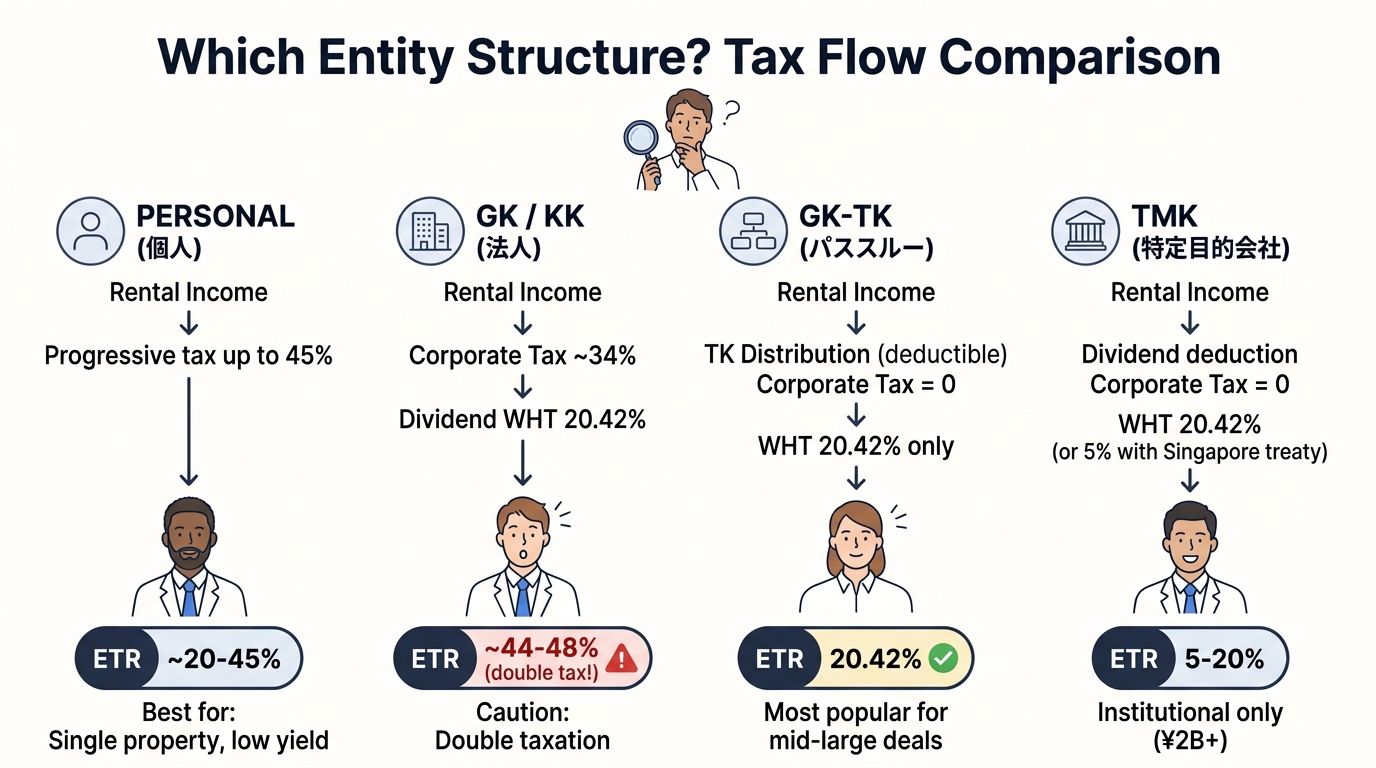

1. Investment Entity Structures Compared

The single most consequential decision a foreign investor makes is the legal entity used for acquisition. The Japanese tax code discriminates sharply between individual ownership and corporate ownership, and further between standard operating companies and passive investment conduits. Choosing the wrong vehicle can trap capital, inflate effective tax rates, and trigger punishing exit taxes.

Direct Personal Ownership (個人 / Kojin)

Acquiring property as a non-resident individual is administratively simple and avoids incorporation costs. However, the taxation is highly punitive for high-yielding properties:

- National income tax brackets scale up to 45% on taxable income exceeding 40,000,000 yen

- Plus the 2.1% special reconstruction surtax, yielding a peak marginal rate of 45.945%

- Non-residents are generally exempt from the 10% local inhabitant tax (residents face a combined top rate of 55%)

- No ability to stream income, defer taxes via retained earnings, or easily transfer assets to heirs

Best for: A single long-term yield property with modest rental income that falls in lower tax brackets.

Kabushiki Kaisha (KK) vs. Godo Kaisha (GK)

To flatten the progressive tax curve, investors frequently use a Japanese domestic corporation. The two primary vehicles are:

| Feature | KK (Joint-Stock Corp) | GK (LLC equivalent) |

|---|---|---|

| Board of Directors | Required | Not required |

| Statutory Auditors | Required (large cos) | Not required |

| Minimum Capital | 1 yen (technically) | 1 yen |

| Annual Gazette Filing | Required | Not required |

| Setup Cost | ~200,000-300,000 yen | ~60,000-100,000 yen |

| Profit Distribution | Pro-rata to shares | Flexible (per articles) |

| Effective Tax Rate (ETR) | 30.62% – 34.59% | 30.62% – 34.59% |

The GK has overwhelmingly superseded the KK as the vehicle of choice for foreign real estate investors due to lower costs, fewer compliance requirements, and flexible profit distribution. SMEs with paid-in capital under 100,000,000 yen enjoy a preferential national corporate tax rate of 15% on the first 8,000,000 yen of taxable income.

Warning: Double Taxation

Standard GKs and KKs face a critical flaw for pure real estate holding: double taxation. The entity pays corporate tax (~30-34%) on net rental income. When retained earnings are repatriated to the offshore parent as dividends, those distributions face an additional 20.42% withholding tax — unless mitigated by a bilateral tax treaty.

Master Comparison Table

| Feature | Personal | GK / KK | GK-TK | TMK |

|---|---|---|---|---|

| Typical Target | Single residential | Small-mid commercial | Mid-large TBI | Institutional portfolios (2B+ yen) |

| Entity-Level Tax | Progressive up to ~45% | Flat ~30-34% | Eliminated via TK expense | Eliminated via dividend deduction |

| Distribution Tax | N/A (20.42% WHT on rent) | 20.42% WHT on dividends | 20.42% WHT on TK payout | 20.42% WHT on dividends |

| Setup Cost | Minimal | Low-Moderate | Moderate | High (FSA filings, auditors) |

| Regulatory Burden | None | Low | Medium | Severe (Asset Liquidation Plan) |

| Final ETR on Distributions | 20.42% (after filing) | ~44-48% (double tax) | 20.42% | 20.42% (5% with treaty) |

2. The GK-TK Pass-Through Structure

The GK-TK (Godo Kaisha – Tokumei Kumiai) is the dominant structure for mid-to-large foreign real estate investments in Japan. It circumvents the double taxation problem that makes standard corporate ownership inefficient.

How It Works

The structure pairs a standard GK, acting as the business operator (営業者 / Eigyosha), with a silent partnership agreement (匿名組合 / Tokumei Kumiai or TK) executed with the offshore investor:

- The GK technically owns the asset and conducts the leasing business

- The TK agreement stipulates that the GK must distribute net operating profits to the silent partner

- These profit distributions are treated as tax-deductible expenses for the GK

- A properly modeled GK-TK distributes 100% of profits, reducing the GK’s taxable income to zero

- The offshore investor then faces only a final 20.42% withholding tax on the TK distribution

Trust Beneficiary Interest (TBI) Optimization

In practice, the GK typically acquires Trust Beneficiary Interests (信託受益権 / TBI) rather than direct fee-simple real estate. The physical property is placed into a trust managed by a licensed Japanese trust bank, and the GK buys the TBI. This approach:

- Significantly reduces real estate acquisition taxes and registration taxes (from ~3-4% down to nominal registration fees)

- Simplifies the transfer process for subsequent sales

- Provides structural separation between the asset and the operating entity

Critical: The Permanent Establishment Risk

To maintain pass-through tax status, the foreign TK investor must remain strictly passive. Any active involvement in the GK’s management risks the NTA reclassifying the TK as a Permanent Establishment (PE) in Japan, which would instantly subject the foreign investor to full Japanese corporate taxation at ~34%.

TMK for Institutional Portfolios

For large-scale portfolios and securitization plays typically exceeding 2-3 billion yen, the Tokutei Mokuteki Kaisha (TMK) is the premier conduit vehicle. Established under the Asset Securitization Act, a tax-qualifying TMK can deduct dividend payments from taxable income, provided it distributes more than 90% of distributable profits each fiscal year and issues specified bonds to qualified institutional investors.

The administrative burden is extreme: drafting and filing an Asset Liquidation Plan (ALP) with the FSA and Local Finance Bureau, regulatory approval for any business plan changes, and mandatory annual audited financial statements. TMKs are unsuitable for investments under approximately 2 billion yen due to the cost overhead.

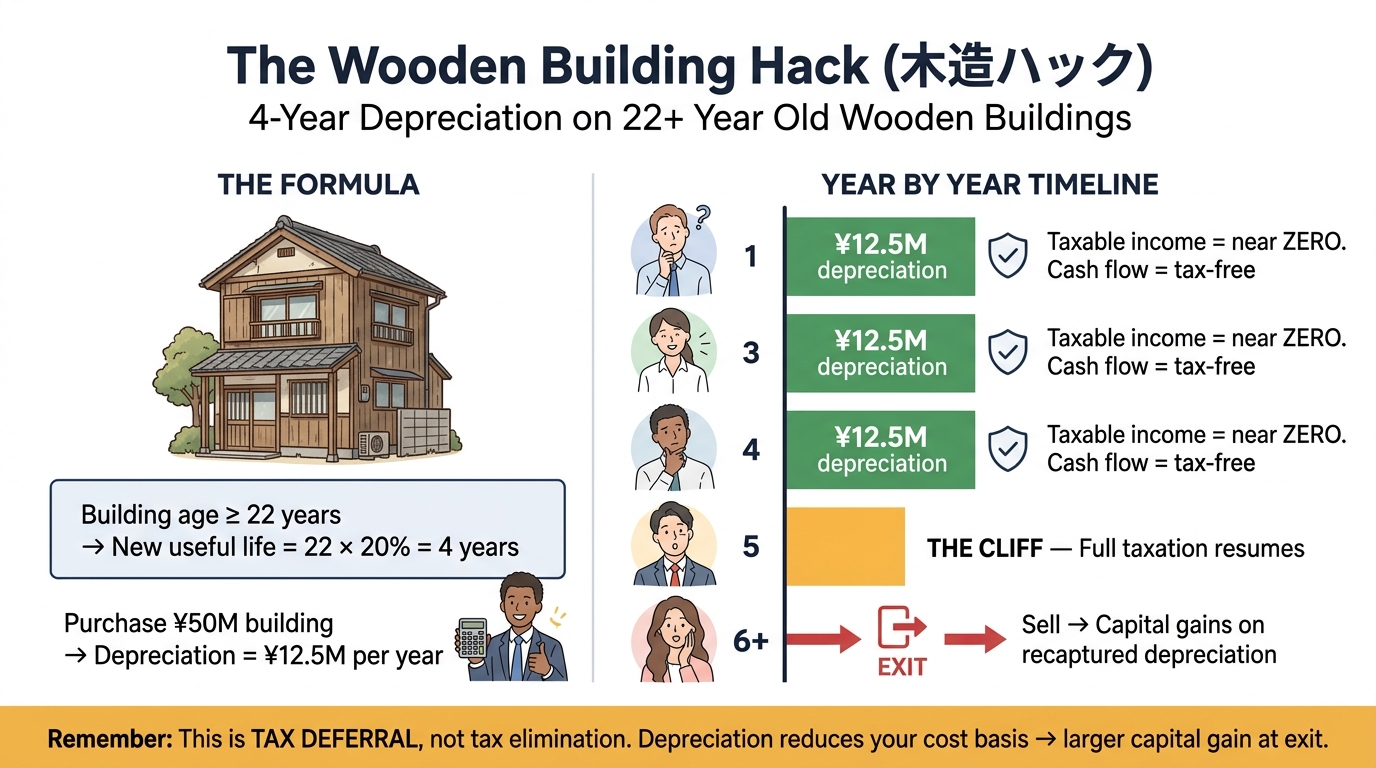

3. Depreciation Strategies & the Wooden Building Hack

Depreciation of tangible real property is the cornerstone of real estate tax optimization in Japan. The tax code allows rapid depreciation schedules that create substantial paper losses, shielding cash flows from income tax for years.

Statutory Useful Lives by Structure Type

| Building Material | Statutory Life (New, Residential) | Annual Depreciation Rate |

|---|---|---|

| Reinforced Concrete (RC) | 47 years | 2.13% |

| Heavy Steel Frame | 34 years | 2.94% |

| Light Steel Frame (< 3mm) | 19-27 years | 3.70-5.26% |

| Wooden Frame | 22 years | 4.55% |

The Used Property Formula

The real power of Japanese depreciation is unlocked when acquiring second-hand assets. The NTA determines the remaining useful life for used buildings using a simplified formula — not an engineer’s estimate:

- Building has exceeded its statutory life: Remaining life = Statutory Life x 20%

- Building has partially exceeded its life: Remaining Life = (Statutory Life – Years Used) + (Years Used x 0.20)

- Fractional years are discarded (rounded down)

The Wooden Building Hack (木造ハック)

How It Works

Acquire a wooden apartment building that is 22 years old or older. The statutory life (22 years) has been exceeded. Applying the 20% rule: 22 x 0.20 = 4.4 years. Discard the fraction: 4-year depreciation schedule.

If you allocate 50,000,000 yen to the building portion, you deduct 12,500,000 yen annually — a massive non-cash expense that routinely drives taxable income below zero, creating effectively tax-free cash flow during the holding period.

Land vs. Building Allocation (配分戦略)

A critical vulnerability: the purchase price must be split between land (non-depreciable) and building (depreciable). In older properties, the building’s intrinsic value may approach zero, meaning the purchase price is effectively paying for land.

- Investors frequently attempt to inflate the building ratio in the sales contract

- The NTA actively monitors this and may mandate use of the local Fixed Asset Tax (FAT) assessed value ratio

- FAT assessments historically assign much higher relative value to land than aging buildings

- Mitigation: Secure a third-party real estate appraisal at the time of transaction, justifying a higher building valuation based on replacement cost or income approaches

Warning: The Depreciation Recapture Trap

Japan has no separate “depreciation recapture” tax rate (unlike the US Section 1250 rate capped at 25%). Every yen of depreciation taken directly reduces the tax book value. Upon sale, the capital gain is calculated as: Sale Price minus Adjusted Depreciated Book Value. The massive paper losses during the holding period translate into a correspondingly massive capital gains tax liability upon exit.

The wooden building hack works as tax deferral, not tax elimination. Its validity relies on rate arbitrage: offsetting rental income taxed at progressive rates (up to ~45%) against long-term capital gains taxed at a flat 15.315% for non-residents.

2026 Status: Non-Resident Eligibility

The 2020 tax reform prohibited using overseas real estate depreciation to offset domestic Japanese salary income. However, the wooden building strategy remains entirely legal and effective for foreign non-resident investors acquiring domestic Japanese real estate. The NTA has not restricted the simplified depreciation formula for properties physically located in Japan.

4. Non-Resident Investor Framework

The Japanese tax system treats non-resident investors as a high flight risk for capital. Consequently, a strict withholding framework shifts the burden of tax collection onto domestic counterparties.

Withholding Taxes at Source

| Income Type | WHT Rate | Withheld By | Due Date |

|---|---|---|---|

| Rental Income | 20.42% of gross rent | Tenant or PM company | 10th of following month |

| Capital Gains (sale) | 10.21% of gross sale price | Purchaser | At settlement |

| Corporate Dividends | 20.42% (treaty may reduce) | Paying entity | 10th of following month |

Key Point: Withholdings Are Prepayments

These withholding amounts are not the final tax liability. To calculate actual tax owed on net income (gross rent minus allowable expenses — management fees, property taxes, insurance, loan interest, and depreciation), you must file an annual Japanese income tax return (due March 15). Because the 20.42% is levied on gross rent, the final tax liability on net rent is almost always lower, resulting in a refund from the NTA.

Tax Representative (納税管理人 / Nozei Kanrinin)

Japanese law requires non-resident property owners to appoint a Tax Representative who acts as legal proxy for:

- Receiving annual Fixed Asset Tax and City Planning Tax invoices from the municipality

- Preparing and filing national income tax returns

- Claiming withholding tax refunds

- Managing all communications with the NTA

Typically, investors hire bilingual accounting firms or empower their local property management company for this role. Failure to appoint a representative can result in inability to process acquisitions, delayed tax refunds, and penalties for unpaid local taxes.

The Banking Bottleneck

Japan’s strict AML protocols mean that individuals without a valid long-term residency visa (在留カード / Zairyu card) are generally prohibited from opening a domestic bank account. The practical workaround:

- The property management company acts as the primary financial conduit

- The PM collects rent, pays domestic expenses (maintenance, utilities, local taxes)

- Executes bulk international wire transfers of net yield to the investor’s offshore account

- Negotiate remittance frequencies (e.g., quarterly) to mitigate cross-border wire fees and FX spreads

Non-resident tax filing is complex.

Get matched with an English-speaking zeirishi who handles non-resident property investors.

5. Cross-Border Taxation & Treaty Benefits

Navigating the intersection between Japanese domestic law and the investor’s home-country tax code is essential to prevent double taxation and optimize the global effective tax rate.

Tax Treaty Mechanics

Japan maintains an extensive network of bilateral double taxation agreements (DTAs) modeled on the OECD framework. The key articles for real estate investors:

- Article 6 (Rental Income): Treaties universally preserve the primary taxing right in the country where the property is physically located. Japan retains full rights — no treaty can exempt your Japanese rental income.

- Article 13 (Capital Gains): Gains from alienation of real property may be taxed in the situs country. Japan retains full rights to levy capital gains taxes on offshore sellers.

- Article 10 (Dividends): This is where treaties provide real value. Dividend withholding rates are heavily modified by treaties.

Foreign Tax Credit (FTC) Mechanism

Since Japan retains primary taxing rights on rental income and capital gains, the prevention of double taxation relies on the investor’s home country granting a Foreign Tax Credit:

| Home Country | FTC Mechanism | Key Notes |

|---|---|---|

| United States | IRS Form 1116 | Dollar-for-dollar credit; excess FTC carries back 1 year / forward 10 years |

| United Kingdom | Double Tax Relief | Credit limited to UK tax on the same income |

| Australia | Foreign Income Tax Offset | Offset capped at Australian tax on foreign income |

| Singapore | Foreign-sourced income exemption | Dividends may be exempt from Singapore tax entirely |

The Singapore-TMK Strategy

A highly sophisticated treaty optimization involves the Japan-Singapore DTA:

- Under domestic law, dividends from a Japanese entity face 20.42% WHT

- Article 10 of the Japan-Singapore treaty reduces this to just 5% if the Singaporean recipient holds 25%+ of voting shares

- A TMK deducts its dividend payouts from corporate taxable income (reducing Japanese corporate tax to near zero)

- Those dividends face only 5% WHT at the Japanese border

- Singapore does not tax foreign-sourced dividends under certain conditions

- Result: global effective tax rate collapses to approximately 5%

Note

The Japanese Ministry of Finance has openly criticized this “double dipping” (deduction at corporate level plus treaty reduction at the border) and actively seeks to close this avenue in treaty renegotiations. As of 2026, the 5% rate for qualifying TMK distributions to Singapore remains available, but investors should monitor for treaty amendments.

6. Financing & Interest Deductions

Debt-funded structures can dramatically amplify return on equity. However, non-resident investors face severe constraints in the Japanese lending market.

Japanese Mortgages for Non-Residents

The sub-1% residential mortgage rates enjoyed by Japanese citizens are inaccessible to non-residents. Traditional megabanks view offshore individuals as unacceptable credit risks. However, specialized lenders have filled this gap:

| Parameter | Typical Terms (2026) |

|---|---|

| Lenders | SBI Shinsei Bank, SMBC Trust (PRESTIA), Orix Bank |

| LTV Ratio | 50% – 70% of bank’s internal appraisal |

| Interest Rate | ~3.5% – 4.0% p.a. (variable, e.g., SBI Shinsei ~3.65%) |

| Income Requirement | 8,000,000+ yen equivalent annual income |

| Location Restrictions | Central Tokyo, Osaka typically required |

| Bank Account | Domestic account mandatory (managed with loan) |

Thin Capitalization Rules (過少資本税制)

When offshore funds capitalize a Japanese GK or KK, they often mix equity with intercompany debt (loans from the offshore parent). Because interest is tax-deductible, funds are incentivized to load entities with debt to eliminate taxable income.

Japan enforces strict Thin Capitalization Rules with a safe harbor:

Safe Harbor: 3:1 Debt-to-Equity Ratio

If interest-bearing debt from the overseas controlling shareholder exceeds three times the subsidiary’s net equity, interest payments on the excess debt become non-deductible for corporate tax purposes. Example: A GK with 100M yen equity can deduct interest on up to 300M yen of related-party debt. Interest on any amount above 300M yen is disallowed.

7. Exit Strategies & Capital Gains Optimization

The realization of returns in Japan requires precise timing. The system severely penalizes short-term speculation and provides virtually no mechanisms for tax-deferred capital recycling.

Capital Gains Tax Rates for Individuals

| Holding Period | Non-Resident Rate | Resident Rate (for reference) |

|---|---|---|

| 5 years or less (short-term) | 30.63% (30% + 2.1% surtax) | 39.63% (incl. local tax) |

| Over 5 years (long-term) | 15.315% (15% + 2.1% surtax) | 20.315% (incl. local tax) |

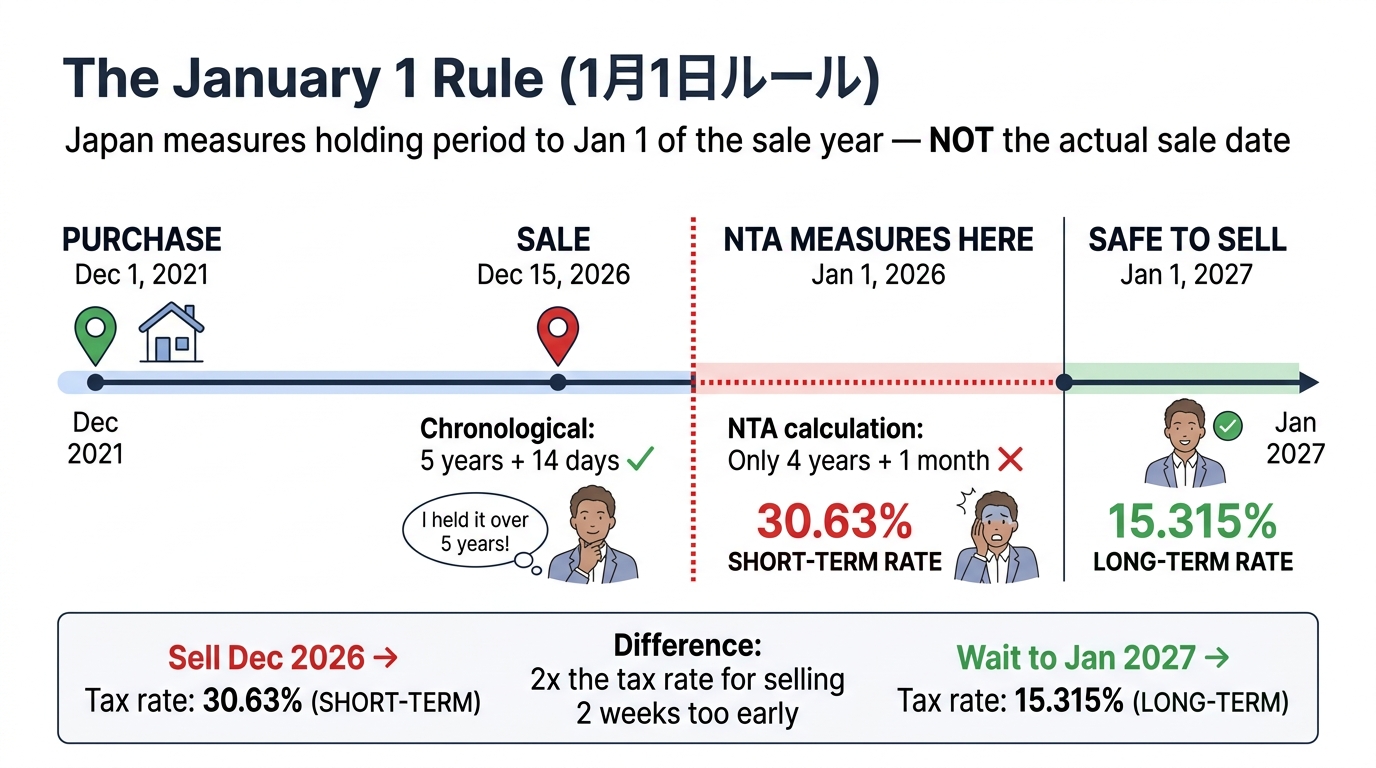

The January 1 Rule (1月1日ルール)

Critical Trap: The 5-Year Test Is NOT Chronological

The holding period is measured from the acquisition date to January 1 of the year in which the sale occurs — not the actual sale date.

Example: An investor buys on December 1, 2021 and sells on December 15, 2026. Chronologically: 5 years and 14 days. Under the January 1 rule: measured as of January 1, 2026, the property has been held for only 4 years and 1 month. This triggers the punitive 30.63% short-term rate.

To qualify for the long-term rate, the sale must close on or after January 1, 2027.

No Tax-Deferred Exchanges

A frequent shock to US and UK investors: Japan lacks a comparable mechanism to US Section 1031 exchanges or UK Rollover Relief. The Japanese code contains the Business Asset Replacement Exception (事業用資産の買換え), but it is highly restrictive:

- Requires the replacement asset to meet incredibly specific geographic and usage criteria

- Only defers 80% of the gain (not 100%)

- Largely useless for foreign portfolio investors

Bottom line: Underwrite your models assuming capital gains tax will be fully realized and paid in cash upon sale.

Corporate Exits: Asset Sale vs. Share Sale

Institutional funds using a GK or KK face a structural dilemma at exit:

| Asset Sale | Share Sale (Entity Sale) |

|---|---|

|

|

GK Liquidation and Deemed Dividends (みなし配当)

If the investor chooses an asset sale followed by GK liquidation, the NTA bifurcates the payout into:

- Return of capital: Tax-free (up to the original invested amount)

- Deemed Dividend (みなし配当): The retained earnings portion is classified as a dividend, subject to 20.42% WHT (reducible if a favorable treaty applies)

8. 2026 Regulatory Changes

The Japanese regulatory environment has evolved rapidly in 2026 to address national security concerns, combat money laundering, and ensure equitable taxation between domestic and offshore investors.

Mandatory Nationality Disclosure (ESPA)

Taking full effect in 2026 under the Economic Security Promotion Act:

- Non-resident individuals must submit formal proof of nationality (passport) at the time of ownership transfer registration

- Japanese corporations must disclose ultimate beneficial control if a majority of officers or voting rights are held by non-Japanese nationals of the same country

- Data feeds into a centralized government database (not public registry)

- Signals a permanent shift toward aggressive oversight of cross-border land acquisitions

JCT on Brokerage Fees — Loophole Closed

New for 2026: 10% JCT Now Applies to Non-Resident Brokerage Fees

Previously, brokerage services for non-residents were classified as “export exempt” from the 10% Japanese Consumption Tax. The FY2026 Tax Reform explicitly eliminates this exemption. Brokerage fees and advisory services related to Japanese real estate are now fully subject to 10% JCT regardless of the client’s residency status. This adds a direct 10% surcharge to transaction friction costs for foreign buyers and sellers.

Transfer Pricing Documentation Mandates

A massive regulatory shift for foreign corporate investors: new, stringent rules targeting related-party transactions, specifically management and shared service fees.

- Japanese entities with specified transactions with foreign related parties (50%+ common ownership) must prepare and preserve detailed “Transaction-Related Documents”

- Required records: formal contracts, invoices, calculation bases for cost allocations, and granular time-logs of services rendered

- If the NTA finds documentation insufficient, they can revoke Blue Return status

- Loss of Blue Return status is catastrophic: strips the entity of the right to carry forward Net Operating Losses (NOLs) and allows the NTA to issue estimated, punitive tax assessments

9. Portfolio Scenarios with Numbers

The following scenarios model post-tax outcomes across distinct investor profiles, illustrating the compound effect of entity selection, depreciation, and treaty mechanics.

Scenario A: US Investor — Single Condo, Personal Ownership (10-Year Hold)

Profile: US-based executive. Newly built 50,000,000 yen condo in Minato-ku, Tokyo. 5.0% gross yield (2,500,000 yen/year). 10-year hold.

Annual Operations:

- PM withholds 20.42% of gross rent (510,500 yen)

- After deducting HOA, PM fees, fixed asset taxes, and RC depreciation (47 years), net taxable income is minimal

- Progressive tax rate on small bracket: ~5%. Substantial WHT refund received.

- US side: IRS Form 1116 credits Japanese tax paid. US marginal rate (~24%) exceeds Japanese effective rate, so investor pays remainder to IRS.

Exit (Year 10): Sold for 60,000,000 yen. January 1 rule met. Long-term rate: 15.315%. Japanese tax serves as FTC against US capital gains tax.

Verdict: Highly efficient. Low overhead makes personal ownership superior for a single, long-term yield play.

Why a KK Would Destroy This Deal

If the same investor sets up a KK for this 50M yen property:

- Net rental income taxed at ~30.62% corporate rate

- Annual KK maintenance: ~400,000 yen (scrivener + tax accountant filings)

- Dividends to US owner: 10% WHT under US-Japan treaty

- Result: negative cash flow. The administrative overhead and double taxation obliterate the 5% gross yield.

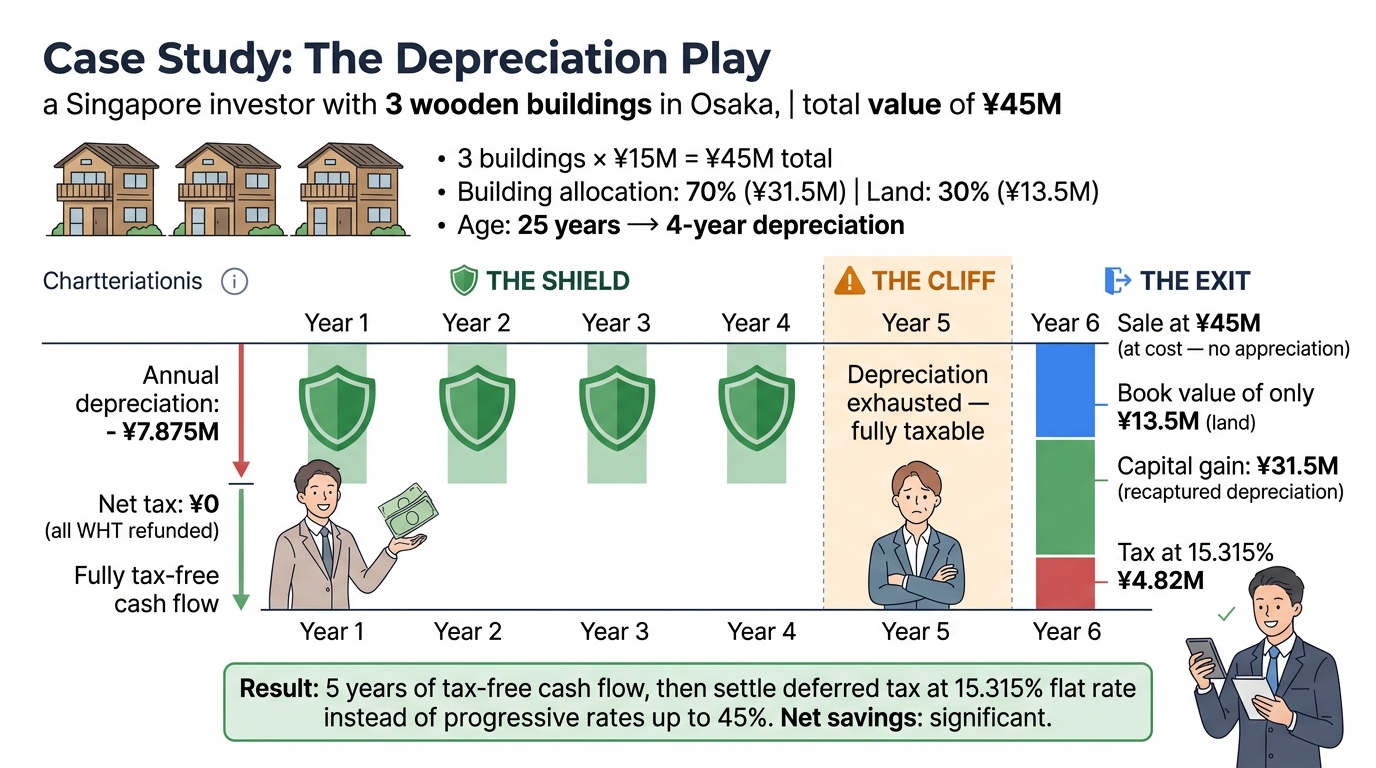

Scenario B: Singapore Investor — Wooden Building Depreciation Play

Profile: HNW individual in Singapore. Three 25-year-old wooden apartment buildings in Osaka. 15,000,000 yen each (total: 45,000,000 yen). Third-party appraisal validates 70% building (31,500,000 yen) / 30% land (13,500,000 yen) allocation.

Years 1-4 (The Shield):

- Buildings qualify for 4-year accelerated depreciation (exceeded 22-year life)

- Annual depreciation deduction: 7,875,000 yen

- Massive paper loss wipes out taxable rental income entirely

- 20.42% WHT on gross rent is fully refunded by the NTA each year

- Cash flow is effectively tax-free in Japan

Year 5 (The Cliff): Depreciation exhausted. Properties suddenly generate fully taxable income at progressive rates.

Year 6 (The Exit):

- Portfolio sold for 45,000,000 yen (at cost)

- Tax book value: only 13,500,000 yen (land — buildings fully depreciated)

- Capital gain: 31,500,000 yen (recaptured depreciation)

- Long-term rate (15.315%): exit tax of 4,824,225 yen

Verdict: Highly successful tax deferral. Investor reinvested gross cash flows for 5 years, then settled deferred tax at a favorable flat capital gains rate instead of progressive income rates.

Scenario C: Offshore Fund — GK-TK Commercial Asset

Profile: Cayman-domiciled institutional fund. 200,000,000 yen commercial logistics facility. GK-TK structure.

Structure:

- GK acquires Trust Beneficiary Interest (TBI) — minimizes acquisition taxes from 3-4% to nominal registration fees

- Capital stack: 100M yen equity + 100M yen non-recourse local bank loan at 2.5% (compliant with 3:1 thin cap rule)

- NOI after interest expenses: 12,000,000 yen

- TK agreement: GK distributes 100% of profit to Cayman fund

Taxation:

- 12M yen TK distribution is deductible for the GK: corporate tax = zero

- Distribution to Cayman fund: flat 20.42% WHT

- Net distribution to fund: ~9,550,000 yen

Verdict: Successfully bypassed the ~34% corporate tax rate, achieving an optimized 20.42% final ETR on a leveraged, large-scale commercial asset — without the regulatory burden of a TMK.

10. Common Investor Mistakes

Mistake 1: The JCT Trap on Commercial Buildings

Unlike residential buildings (where rent is exempt from JCT), the purchase of a commercial building triggers a 10% Japanese Consumption Tax. A 200M yen commercial acquisition creates a 20M yen JCT liability immediately. Unless the foreign entity is pre-registered as a taxable enterprise in Japan before the transaction, recovering this input JCT is legally impossible — a permanent 10% destruction of acquisition capital.

Mistake 2: Ignoring City Planning Tax

Investors model the Fixed Asset Tax (typically 1.4% of assessed value) but routinely omit the concurrent City Planning Tax (up to 0.3% of assessed value) levied on properties in designated urban zones. On low-yield core assets, this consistently erodes modeled NOI.

For full details on Fixed Asset Tax and City Planning Tax calculations, see our foundational real estate tax guide.

Mistake 3: The Inheritance Tax Exposure

Japan imposes inheritance tax based on asset location (situs), not the owner’s residency. A non-resident holding Japanese real estate in their own name exposes heirs to progressive inheritance tax rates scaling up to 55% (above the 30M yen + 6M yen per statutory heir basic allowance).

Solution

Hold the Japanese asset within an offshore corporate entity. Upon death, the shares of the offshore entity transfer outside Japan’s jurisdiction. The NTA cannot levy inheritance tax on a foreign share transfer.

Mistake 4: The “Flipping” Fallacy

Capital from high-velocity markets often attempts buy-renovate-flip within 12-24 months. This ignores the punitive 30.63% short-term capital gains tax. The Japanese system is fundamentally engineered to punish speculation and reward patient, long-term capital deployment.

Mistake 5: Treating Depreciation as Tax Elimination

Marketing materials for the wooden building hack frequently sell the concept as tax elimination rather than tax deferral. Investors who fail to build reserve funds for the capital gains tax liability at exit often lack the liquidity to settle the NTA bill, especially if the property failed to appreciate.

Mistake 6: Misunderstanding the January 1 Rule

Selling one month too early — even after holding the property for over 5 calendar years — can double your effective capital gains tax rate from 15.315% to 30.63%. Always verify the holding period against January 1 of the sale year, not the actual sale date.

Summary: Key Takeaways for Foreign Real Estate Investors in Japan (2026)

- Entity selection is the single most impactful decision. GK-TK eliminates ~34% corporate tax; standard GK/KK creates double taxation.

- The wooden building hack provides 4-year accelerated depreciation on 22+ year-old wooden buildings — tax deferral, not elimination.

- Non-residents face 20.42% WHT on gross rent (refundable to net via annual filing) and must appoint a Tax Representative.

- The January 1 rule measures holding period to January 1 of the sale year. Short-term rate is 30.63%; long-term is 15.315%.

- No 1031 exchange equivalent. Budget for full capital gains tax realization upon exit.

- Treaty benefits matter most for dividend WHT reduction (e.g., Singapore-TMK structure: 5% vs. 20.42%).

- 2026 changes: Mandatory nationality disclosure, JCT on non-resident brokerage fees, stricter transfer pricing documentation.

- Hold Japanese RE in a corporate wrapper to avoid up to 55% inheritance tax exposure.

Frequently Asked Questions

Which entity structure is best for foreign real estate investors in Japan?

For most mid-sized foreign real estate investments in Japan, the GK-TK (Godo Kaisha – Tokumei Kumiai) pass-through structure is the optimal choice. It avoids the double taxation that hits standard GKs and KKs while keeping setup costs manageable. Direct personal ownership only makes sense for a single low-yield property, and TMK is reserved for institutional portfolios above approximately 2 billion yen.

How much tax can a GK-TK structure save compared to personal ownership?

A GK-TK structure can reduce the effective tax rate from up to 45.945% (personal ownership for non-residents) to 20.42% (withholding tax on TK distributions only). For high-yielding properties, this means roughly halving the tax burden. The GK’s taxable income is reduced to zero because TK distributions are treated as deductible expenses, leaving only a single layer of withholding tax at the investor level.

What is the “wooden building 4-year depreciation hack”?

Japan’s tax code allows accelerated depreciation for used wooden residential properties whose statutory useful life (22 years) has fully elapsed. Such properties can be depreciated over just 4 years, generating substantial paper losses that shelter rental income. This is one of the most powerful tax optimization tools in Japanese real estate investing, though 2026 regulatory changes have tightened the rules for non-residents.

Structuring a Japan real estate investment?

Get matched with a bilingual tax accountant who specializes in cross-border property structures — completely free.

Or message us directly: WhatsApp