You’re a foreigner running (or planning to run) a short-term rental in Japan — Airbnb, Booking.com, Vrbo — through the Minpaku New Law (住宅宿泊事業法), Special Zone Minpaku (特区民泊), or a full Hotel Business Act licence. The platform handles bookings; the Japanese tax system handles the headaches. Your rental income gets classified as one of three categories, each with different consequences. Consumption tax kicks in at a specific threshold. Tokyo, Osaka, and Kyoto add accommodation tax. Non-resident hosts lose 20.42% to withholding before they see a yen. And 2026 has brought tighter local rules in Toshima Ward and Osaka. This guide walks through the tax framework for foreign hosts — resident and non-resident — operating short-term rentals in Japan.

This is a tax guide, not a licensing guide. If you need help with the Minpaku notification process or hotel licensing, our recommended partner network includes administrative scriveners (gyōsei shoshi) who specialize in Minpaku registration.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Japanese minpaku regulations, consumption tax rules, and local accommodation tax ordinances change frequently. Always engage a qualified Japan tax accountant (税理士 / zeirishi) before launching commercial short-term rental operations.

Foreign Airbnb host in Japan?

Get matched with a Japan tax accountant experienced in short-term rental taxation — free.

Table of Contents

- Who This Foreign Minpaku Host Tax Guide Is For

- Three Legal Frameworks for Japan Short-Term Rentals

- Minpaku Income Classification: The Three Buckets

- Consumption Tax on Japan Minpaku Operations

- Japan Accommodation Tax: Tokyo, Osaka, Kyoto

- Non-Resident Foreign Airbnb Hosts: 20.42% Withholding

- Income Tax on Minpaku Profits for Japan Residents

- Deductible Expenses for Minpaku Operators

- 2026 Local Rule Changes: Toshima, Osaka, and More

- Common Tax Mistakes for Foreign Minpaku Hosts

- Minpaku Tax FAQ for Foreign Hosts

- Get Expert Help With Minpaku Tax

1. Who This Foreign Minpaku Host Tax Guide Is For

This guide is written for one or more of the following situations:

- You are a foreign resident of Japan running a Minpaku or Airbnb operation as a side activity or full-time business.

- You are a non-resident foreigner who owns Japanese real estate and rents it out short-term via Airbnb, Booking.com, or other platforms.

- You are planning to launch a short-term rental in Japan and want to understand the tax overhead before committing capital.

- You operate multiple Minpaku properties and need to understand consumption tax registration timing and entity structuring.

- You are a real estate investor evaluating Minpaku-eligible properties as part of a broader Japan investment thesis.

If you operate a traditional long-term rental property in Japan and don’t do short-term hosting, your tax framework is fundamentally different — see our Non-Resident Landlord in Japan Tax Guide for traditional rental tax mechanics.

What This Guide Does Not Cover

- Licensing and permit processes — Minpaku notification, Hotel Business Act licensing, fire safety compliance. Get advice from a gyōsei shoshi (administrative scrivener) for licensing.

- Property purchase tax — acquisition tax, stamp duty, registration tax. Covered in our Japan Real Estate Tax for Foreign Investors guide.

- Corporate Minpaku operations — running multiple properties through a Japanese GK/KK adds layers of corporate tax, withholding, and consumption tax planning that need bespoke advice.

2. Three Legal Frameworks for Japan Short-Term Rentals

Japan distinguishes three legal pathways for offering short-term accommodation. Your tax treatment depends materially on which path you’ve chosen.

Pathway 1: Minpaku New Law (住宅宿泊事業法 / Jūtaku Shukuhaku Jigyō Hō)

In force since June 2018. National framework for residential property used as short-term rental. Key features:

- 180-day annual cap on rental nights per property.

- Notification (not full license) to local authority.

- Most popular pathway for individual foreign hosts.

- Local governments can impose stricter rules (covered in Section 9).

Pathway 2: National Strategic Special Zone Minpaku (特区民泊 / Tokku Minpaku)

Limited to designated Special Zones (Osaka, parts of Tokyo, Niigata, Kitakyushu, etc.). Features:

- No annual cap on nights (unlike the 180-day Minpaku Law).

- Minimum stay of 2 nights, 3 days in most zones.

- Stricter zoning and safety requirements.

- Local authorities can suspend new applications (Osaka City suspended new Special Zone applications in May 2026).

Pathway 3: Hotel Business Act (旅館業法 / Ryokangyōhō)

Traditional hotel/inn licensing. Most demanding requirements but no day-count restrictions. Three subcategories: Hotel (ホテル), Ryokan (旅館), and Kan’i Shukusho (簡易宿所 — simple guesthouse). Most flexible but operationally heaviest. Suited for full-time hospitality businesses rather than individual hosts.

Tax Treatment Differences Across Pathways

For income tax purposes:

- Minpaku New Law (180-day cap): typically miscellaneous income (雑所得 zatsushotoku) or real estate income (不動産所得 fudōsan shotoku), depending on scale and service intensity.

- Special Zone Minpaku: typically business income (事業所得 jigyō shotoku) given the year-round operations.

- Hotel Business Act: always business income — explicitly a business under the Hotel Business Act framework.

This classification has cascading effects on tax filing, deductible expenses, depreciation, and loss treatment.

3. Minpaku Income Classification: The Three Buckets

Japan’s tax law classifies income into 10 categories. For Minpaku operations, three of these categories may apply, with material tax differences.

Bucket A: Real Estate Income (不動産所得)

Traditional long-term rental income falls in this bucket. For Minpaku, you may be in this bucket if:

- You provide minimal services — no breakfast, no daily cleaning, no concierge.

- Your involvement is essentially “key handover and weekly cleaning.”

- The substance is property rental, not hospitality service.

Pros: simpler bookkeeping, real estate-specific deductions.

Cons: in practice, most Minpaku operations include enough hospitality elements (linen change between guests, communication with guests, in-property guides, etc.) that they exceed the “real estate income” threshold.

Bucket B: Business Income (事業所得)

Larger or more service-intensive Minpaku operations fall in this bucket:

- Multiple properties or full-time operation.

- Service-rich hosting (welcome service, breakfast, concierge, tours, etc.).

- Operations under Hotel Business Act or Special Zone licensing.

Pros: full expense deductibility, depreciation flexibility, blue-tax filer (青色申告) benefits including loss carry-forward and ¥650,000 deduction.

Cons: business-tax registration may apply, full bookkeeping required (double-entry), social insurance considerations for self-employed individuals.

Bucket C: Miscellaneous Income (雑所得)

Small-scale, hobby-level, or “one apartment as a side activity” operations often fall here:

- One property, occasional rentals.

- Annual income relatively modest.

- Hospitality services beyond simple rental but not at business scale.

Pros: simpler filing, less bookkeeping burden.

Cons: losses cannot offset other income categories, no blue-tax benefits, deductions are more restrictive.

How NTA Decides the Bucket

National Tax Agency officials look at substance over form:

- Service intensity (cleaning frequency, food, concierge).

- Number of properties.

- Marketing presence (separate website, branding, multi-platform presence).

- Time spent on operations.

- Whether operations are organized as a “business.”

For most foreign hosts with one Minpaku property under the 180-day Law, miscellaneous income is the typical classification — though aggressive operators may push for business income to capture deductions. Discuss your classification with a Japan tax accountant before your first filing year.

4. Consumption Tax on Japan Minpaku Operations

Japan’s national consumption tax (currently 10%) applies to most goods and services, including paid accommodation. For Minpaku operations:

Threshold for Consumption Tax Registration

The standard threshold: if your taxable sales exceed JPY 10 million in the “base period” (two years prior), you are a consumption tax taxpayer in the current year and must register, collect, and remit consumption tax. Below threshold, you can choose to be exempt (免税事業者).

Practical Math for Minpaku

JPY 10 million in annual booking revenue translates to roughly:

- JPY 833,000 per month — or roughly JPY 27,000/night × 30 nights at full occupancy.

- For 180-day-capped Minpaku at JPY 30,000/night and 60% occupancy: about JPY 3.2M annual — well below threshold for a single property.

- Multiple properties or Special Zone Minpaku with year-round operation can easily cross the JPY 10M line.

Qualifying Invoice System (適格請求書 / Inboisu Seido)

From October 2023, Japan transitioned to a Qualifying Invoice system. For Minpaku operators, the practical implication: if your guests include Japanese businesses (e.g., bookings by companies for staff travel) and they want to claim input consumption tax credit, you’ll need to register as a qualifying invoice issuer (適格請求書発行事業者). This is voluntary even below the JPY 10M threshold, but registering converts you to a consumption-tax-paying entity regardless of size.

For most individual foreign Minpaku hosts whose guests are predominantly leisure travelers, the qualifying invoice issue is minor — but if you market to corporate travelers, factor it in.

Platform Fees and Consumption Tax

Airbnb, Booking.com, and similar platforms typically deduct their service fees from your payout. The treatment varies by platform and your registration status. Most foreign Minpaku operators treat the gross booking amount as revenue and the platform fee as a deductible expense.

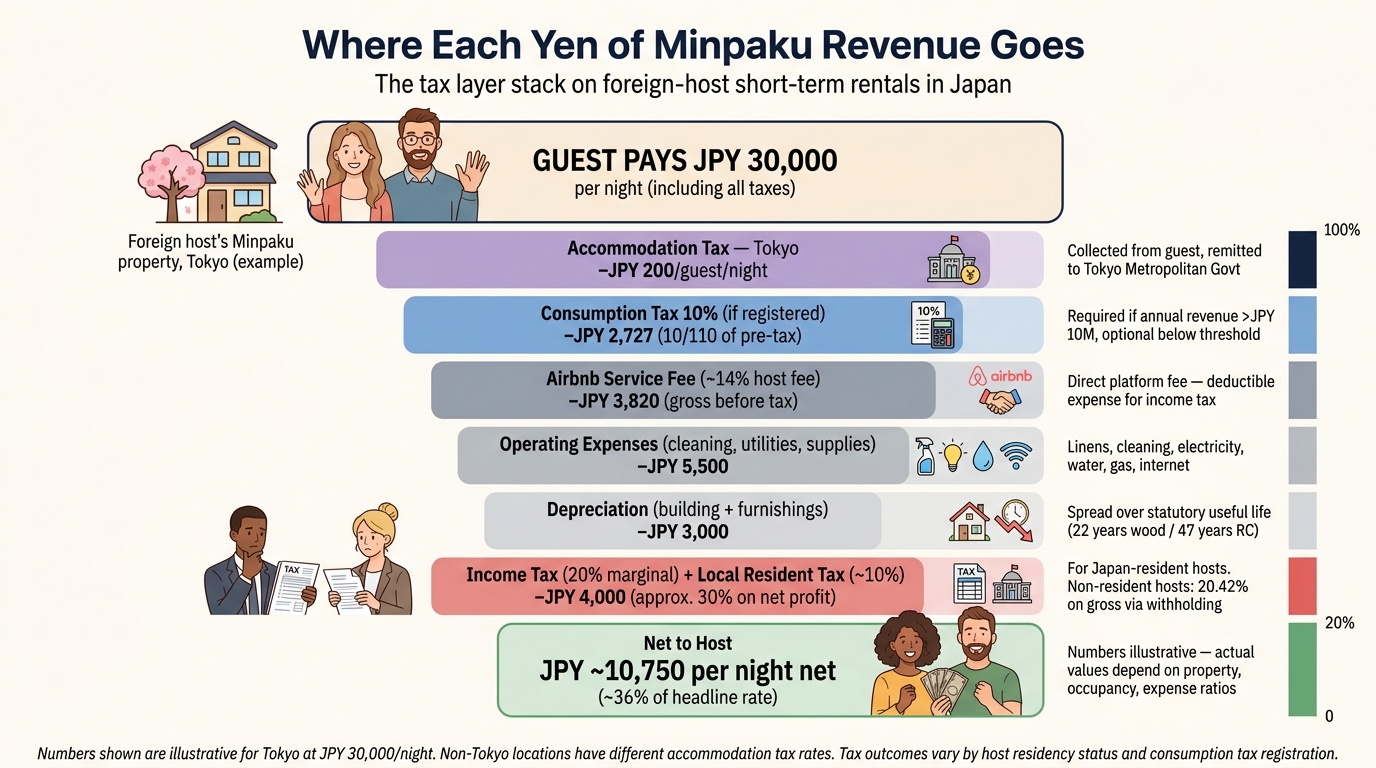

5. Japan Accommodation Tax: Tokyo, Osaka, Kyoto

Several Japanese local governments impose an accommodation tax (宿泊税 / shukuhakuzei) on paid lodging — including Minpaku, in many cases. Rates vary by jurisdiction and price point.

Tokyo Metropolitan Accommodation Tax

For accommodation in Tokyo:

- JPY 100 per person per night for stays priced JPY 10,000–14,999.

- JPY 200 per person per night for stays priced JPY 15,000 or higher.

- No tax for stays under JPY 10,000.

- From 2026, Tokyo’s enforcement explicitly extends to Minpaku operations registered under the New Law.

Osaka Prefectural Accommodation Tax

For accommodation in Osaka:

- JPY 100 per person per night for stays JPY 7,000–14,999.

- JPY 200 per person per night for stays JPY 15,000–19,999.

- JPY 300 per person per night for stays JPY 20,000 or higher.

- No tax for stays under JPY 7,000.

Kyoto City Accommodation Tax

Kyoto applies accommodation tax to all paid lodging regardless of price tier:

- JPY 200 per person per night for stays under JPY 20,000.

- JPY 500 per person per night for stays JPY 20,000–49,999.

- JPY 1,000 per person per night for stays JPY 50,000 or higher.

Other Jurisdictions

Fukuoka (city and prefecture), Kanazawa, Nagasaki, and several others apply local accommodation taxes. Several more are introducing taxes in 2026. Check the specific local government’s website for the property location.

Host Obligations

You collect accommodation tax from guests at check-in (or include it in the booking price) and remit it to the local government monthly or quarterly. The platform may or may not handle collection automatically — Airbnb began collecting some local accommodation taxes for hosts, but coverage is incomplete. As host, you remain liable if collection fails.

6. Non-Resident Foreign Airbnb Hosts: 20.42% Withholding

If you own a Japanese property and rent it out via Airbnb while you yourself live outside Japan, you face a specific tax setup similar to traditional non-resident landlords — but with Minpaku-specific complications.

The 20.42% Withholding Tax

For non-resident hosts:

- If guests pay directly to your Japanese bank account, no automatic withholding applies at the platform level (the platform doesn’t know about your residency for withholding purposes).

- However, if you use a Japanese property management agent who handles payments, that agent must withhold 20.42% (20% income tax + 0.42% reconstruction surtax) on the gross rental payment to you.

- Property management agents that handle Minpaku operations for non-resident hosts are obligated to withhold and remit this tax monthly.

Recovering the Withholding

The 20.42% is a prepayment, not final tax. You file an annual Japanese tax return (準確定申告 jun-kakutei shinkoku for some non-resident filings, or standard 確定申告 with non-resident designation) and:

- Calculate actual net Minpaku income after expenses.

- Apply Japanese progressive tax rates (or applicable rates).

- Reconcile against the 20.42% already withheld.

- Refund of over-withholding is generally significant since the 20.42% applies to gross, but actual tax is on net.

For Minpaku-specific expenses (platform fees, cleaning fees, utilities, depreciation, insurance), substantial deductions can mean actual tax is well below the 20.42% withheld.

Tax Representative Requirement

Non-resident hosts with Japanese-source rental income are required to appoint a Tax Representative (納税管理人 / nōzei kanrinin) — a Japan-resident individual or entity who receives NTA correspondence and handles filings on your behalf. Without a Tax Representative, NTA cannot communicate with you and may impose default assessments.

Property management companies often serve as Tax Representative for non-resident hosts they handle. Specialized cross-border tax accountants also offer this service.

Coordination with Home Country Tax

Non-resident hosts face Japanese tax on Japan-source Minpaku income, and may also face home-country tax on the same income. Most major tax treaties with Japan address real estate income — typically with primary taxing rights to Japan (where the property is located) and foreign tax credit available in your home country. Common scenarios:

- US-resident Minpaku host: Japan-source income on US 1040 with foreign tax credit for Japanese tax paid.

- UK-resident host: Japan-source income on UK Self Assessment with foreign tax credit.

- Singapore-resident host: Japan-Singapore treaty allocates taxing rights; Singapore generally exempts foreign-source income from Singapore tax.

7. Income Tax on Minpaku Profits for Japan Residents

For Japan-resident hosts (foreign or Japanese), Minpaku profits are part of your worldwide income, taxed at Japan’s progressive income tax rates plus local resident tax.

Japan Income Tax Brackets (2026)

| Annual Taxable Income (JPY) | National Income Tax Rate | Plus Local Resident Tax |

|---|---|---|

| Up to 1.95M | 5% | + ~10% (flat) |

| 1.95M – 3.3M | 10% | + ~10% |

| 3.3M – 6.95M | 20% | + ~10% |

| 6.95M – 9M | 23% | + ~10% |

| 9M – 18M | 33% | + ~10% |

| 18M – 40M | 40% | + ~10% |

| Over 40M | 45% | + ~10% |

Plus 0.42% reconstruction surtax on the national income tax portion. Effective marginal rates can approach 55% for highest earners.

Calculating Net Minpaku Income

- Gross rental revenue from all platforms (Airbnb, Booking.com, Vrbo, direct bookings).

- Subtract direct expenses — platform fees, cleaning, linens, utilities, supplies.

- Subtract property-related expenses — proportional mortgage interest (interest only, not principal), property tax, insurance, repairs.

- Subtract depreciation on the building portion of the property and on furnishings.

- For multi-use properties (you live there part of the year): allocate expenses by use ratio (rental nights ÷ total nights).

- Result: net Minpaku income, added to your overall taxable income at applicable rate.

8. Deductible Expenses for Minpaku Operators

Robust expense tracking is one of the highest-leverage tax tasks for Minpaku hosts. Common deductible categories:

Direct Operating Expenses

- Platform fees (Airbnb, Booking.com service fees).

- Cleaning fees (in-house or contracted).

- Linens, towels, toiletries, supplies.

- Utilities (electricity, water, gas, internet) — full deduction for Minpaku-dedicated properties; proportional for shared properties.

- Property management agency fees.

- Marketing and photography costs.

Property-Related Expenses

- Mortgage interest (not principal) on the rental property — proportional if mixed-use.

- Property tax (固定資産税) and city planning tax (都市計画税).

- Building insurance (fire, earthquake).

- Repairs and maintenance.

- Pest control, gardening, building common-area fees.

Depreciation

Buildings depreciate over statutory useful life (typically 22 years for wooden residential, 47 years for reinforced concrete residential). Furnishings (beds, appliances, electronics) depreciate over 5–15 years depending on category. For acquired older buildings, “used building” depreciation rules can accelerate the timeline materially.

Other Deductions

- Tax accountant fees.

- Administrative scrivener fees for Minpaku registration.

- Travel to property for inspections (within reason).

- Office supplies, software, communication tools for the Minpaku business.

- Insurance specifically for short-term rental liability (PL hoken).

Blue Tax Filer (青色申告) Benefits

If your Minpaku income is classified as business income (事業所得) and you register as a blue tax filer (青色申告者), you gain:

- Special deduction of up to JPY 650,000 (with e-Tax filing and double-entry bookkeeping).

- Loss carry-forward for up to 3 years.

- Family employee deduction (if family members work in the business).

- Accelerated depreciation for certain small assets.

Blue tax filer status requires advance notification to NTA (usually by March 15 of the relevant year) and double-entry bookkeeping. For serious Minpaku operations, the benefits typically far outweigh the bookkeeping overhead.

9. 2026 Local Rule Changes: Toshima, Osaka, and More

Minpaku regulation is local-government-driven, and 2026 has brought several material changes for foreign hosts.

Toshima Ward (Tokyo): 120-Day Cap from December 16, 2026

Toshima Ward in Tokyo announced a cap of 120 days (down from the national 180-day maximum) effective December 16, 2026. Existing properties already operating under the national framework are affected. Hosts in Toshima should plan for the tighter day cap and reduced revenue accordingly.

Osaka City: Special Zone Application Suspension

Osaka City suspended new Special Zone Minpaku (特区民泊) applications in May 2026. New foreign investors entering Osaka must now use the 180-day standard Minpaku framework — significantly reducing year-round revenue potential. Existing Special Zone properties continue under prior approvals but face uncertainty around renewals.

Other Ward-Level Restrictions

Several Tokyo wards have restrictive rules on Minpaku operating days:

- Some wards prohibit Minpaku operations on weekdays.

- Several restrict operations in residential zones.

- Most require specific notification timing aligned to the national framework.

Before purchasing a property for Minpaku purposes, verify with the specific local ward office that short-term rental is permitted in that location and what restrictions apply.

Accommodation Tax Expansion

The 2026 enforcement of accommodation tax explicitly extends to licensed Minpaku operations in Tokyo and Osaka. Hosts that previously collected only consumption tax must now also collect and remit accommodation tax.

10. Common Tax Mistakes for Foreign Minpaku Hosts

Mistake 1: Treating Minpaku as Pure Real Estate Income

Many foreign hosts initially treat Minpaku income the same as long-term rental income, claiming real estate income classification. NTA increasingly views Minpaku as business or miscellaneous income because of the hospitality service element. Wrong classification can trigger audits and retroactive penalties.

Mistake 2: Ignoring Accommodation Tax

Hosts focused on income tax and consumption tax often miss local accommodation tax. Tokyo, Osaka, Kyoto, and several other cities require collection and remittance. Penalties for non-compliance can be material.

Mistake 3: Missing the 180-Day Cap

Operating beyond the 180-day Minpaku cap (or stricter local caps like Toshima’s 120-day) leads to license suspension or revocation. Track nights carefully — the tax filings will inevitably reveal the operating volume.

Mistake 4: Not Appointing a Tax Representative as Non-Resident

Non-resident hosts must appoint a Tax Representative. Without one, NTA cannot deliver notices, leading to default assessments and difficulty recovering withheld amounts.

Mistake 5: Skipping Consumption Tax Registration Timing

The two-year lookback for consumption tax threshold catches operators by surprise. A property that earned JPY 8M in Year 1 falls under threshold for Year 1; but if Year 2 earnings are JPY 12M, you’re a consumption tax taxpayer in Year 3 — even if Year 3 itself stays under threshold.

Mistake 6: Mixing Personal and Minpaku Use Without Allocation

If you use your Minpaku property as your own holiday home part of the year, you must allocate expenses by rental-night vs personal-night ratio. Failing to do so risks deduction denial in audit.

Mistake 7: Forgetting Property Tax Updates

Properties used commercially (including Minpaku) may face a higher property tax (固定資産税) rate than purely residential properties. Notify the local property tax office of the commercial use to ensure correct assessment. Failure to notify can lead to back taxes and penalties.

11. Minpaku Tax FAQ for Foreign Hosts

Q1: I’m a US citizen living in Japan running Airbnb. Do I file in both countries?

Yes — your Japan-resident filing covers worldwide income including the Minpaku profits. As a US citizen, you also file a US return reporting worldwide income, with foreign tax credit (Form 1116) for Japanese tax paid on the same Minpaku income. See our US Citizens Tax in Japan complete guide.

Q2: Can I operate Minpaku in Japan without becoming a Japan tax resident?

Yes — you can be a non-resident owner-host. But you must appoint a Tax Representative, file annual Japanese non-resident tax returns, and accept 20.42% withholding on management-company-handled payouts. The mechanics are heavier than for Japan-resident hosts.

Q3: Are Airbnb’s “host insurance” payments taxable?

Yes — payments received from Airbnb’s Host Liability Insurance or Host Damage Protection in response to claims are generally taxable as income in Japan (they replace economic loss). Track these separately and include in annual income reporting.

Q4: I rent out one room in my apartment occasionally. Does that count as Minpaku?

If you accept paid guests for short stays, you must operate under one of the three legal frameworks (Minpaku New Law, Special Zone, or Hotel Business Act). Even one room counts. Operating without notification or license is illegal and subject to penalties.

Q5: My property is in a strict ward that bans weekday Minpaku. Can I rent it long-term during weekdays and short-term on weekends?

Practically difficult to operate cleanly. Long-term tenancy requires standard residential lease agreements with tenant protection rights. Mixing short and long-term occupancy on a single property in the same period typically violates residential lease law (借地借家法 Shakuchi Shakka Hō) and Minpaku notification terms. Consult a lawyer or gyōsei shoshi before attempting this.

Q6: Do platform fees from Airbnb include consumption tax?

Generally yes — Airbnb collects consumption tax on its host service fees from Japan-based hosts. The booking amount you receive is net of consumption tax-inclusive platform fees. Treat the gross booking as your revenue (with platform fee as deductible expense) for income tax purposes.

Q7: I want to scale to 5 properties. Should I form a Japanese GK (LLC)?

For multi-property Minpaku operations, a Japanese GK (合同会社) or KK (株式会社) is often advisable for:

- Liability separation between properties.

- Cleaner consumption tax management.

- Easier financing.

- Smoother sale of individual properties.

However, the corporate setup adds bookkeeping, corporate tax filings, and director compensation considerations. The crossover point varies but typically makes sense around 3+ properties.

Q8: I bought a property for Minpaku but my application was denied. Now what?

You can still rent the property long-term under standard residential rental law (which is not subject to Minpaku restrictions), or apply for Hotel Business Act licensing (more demanding), or sell. Some hosts in this situation pivot to monthly furnished rentals (which are technically allowed under residential rental law if the lease terms qualify) — but tax classification then differs. Consult both a lawyer and tax accountant before pivoting.

12. Get Expert Help With Minpaku Tax

Minpaku tax compliance combines real estate tax, consumption tax, local accommodation tax, and (for non-residents) tax representative obligations. The right professional is usually a Japan tax accountant with multiple short-term rental clients — ideally with experience servicing foreign hosts who also need cross-border coordination with home-country tax.

TaxMatch Japan introduces foreign Minpaku hosts to Japan tax accountants experienced in short-term rental operations. Initial introductions are free.

Common engagement profiles for foreign Minpaku hosts:

- Pre-launch planning: legal framework choice (Minpaku Law vs Special Zone vs Hotel Business Act), entity structuring (individual vs GK), break-even analysis with full tax burden modeling.

- First-year operation setup: blue tax filer registration, consumption tax registration decision, bookkeeping system, accommodation tax remittance procedure.

- Non-resident host services: Tax Representative appointment, annual tax filing, withholding recovery.

- Scaling operations: corporate structuring, multi-property tax coordination, succession planning.

Free Matching for Foreign Minpaku Hosts

Tell us your situation and we’ll match you with a Japan tax accountant experienced in Minpaku operations. No fees, no obligation.

Prefer WhatsApp? Message us at +81 80-6075-2063

Related Guides

Non-Resident Landlord in Japan

Traditional long-term rental tax — the non-Minpaku option

Japan Real Estate Tax for Foreign Investors

Acquisition tax, depreciation, entity structuring for property

Japan Tax Residency 5-Year Rule

Whether your Minpaku income falls into Japan tax base

Foreign Tax Credit in Japan

Avoiding double tax on the same Minpaku income

Double Taxation in Japan

Cross-border Minpaku income across treaty jurisdictions