Running a short-term Airbnb/minpaku instead of a long-term rental? See our Minpaku/Airbnb Tax for Foreign Hosts guide.

You moved away from Japan but kept the apartment in Tokyo — and now the monthly rent shows up in your bank account minus a hefty 20.42% withholding. Or maybe you bought a property in Japan while you were living there, and now you’re back home wondering how to handle the tax. Either way, you’re a non-resident landlord, and Japanese tax law has a specific framework for you that’s different from both Japan-resident landlords and from the sophisticated multi-property investors covered in our Japan Real Estate Tax for Foreign Investors guide.

This guide is for the individual non-resident landlord with one or two Japan properties — typically inherited from a previous Japan residency, or bought as a hold for future return — and walks through the monthly withholding, annual filing, Tax Representative requirement, and the refund opportunity that most landlords miss.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Japanese tax laws and treaty positions change, and individual situations vary substantially. Always consult a qualified bilingual tax accountant for advice specific to your circumstances.

Live abroad and own Japan property?

Get matched with a Tax Representative — free.

Table of Contents

- Who This Guide Is For

- The Non-Resident Landlord Setup in Japan

- The 20.42% Withholding on Japan Rent: How It Works

- How to Get the 20.42% Japan Rent Withholding Back

- Annual Filing Obligations for Non-Resident Landlords

- Tax Representative (Nozei Kanrinin) — Required From Day 1

- Allowable Deductions for Japan Rental Income

- Capital Gains If You Sell the Property

- Common Non-Resident Landlord Mistakes

- Frequently Asked Questions

- Get Expert Help With Japan Rental Tax

1. Who This Guide Is For

You should read this guide if all of the following describe your situation:

- You are not a Japan resident for tax purposes (you live primarily in another country and your “center of life” is no longer Japan).

- You own one or two residential or commercial properties in Japan that generate rental income.

- The properties are managed by a Japanese Property Management Company (PM) or rented directly to tenants in Japan.

- You are not a sophisticated investor with a structured portfolio (GK-TK, TMK, etc.) — that’s covered in our Foreign Investors Real Estate Tax guide.

Common scenarios we see

The Foreign Lead intake at TaxMatch Japan regularly surfaces these patterns:

- The “kept the apartment” case — moved abroad for work, kept the Tokyo condo and rented it out instead of selling.

- The “investment property bought as resident” case — purchased a Japan property while resident, then moved abroad with the property still earning rent.

- The “inherited from parents” case — foreign national inherits a Japan property from family and chooses to rent it rather than sell.

- The “return planning” case — bought a Japan property intending to return within 5-10 years, renting it in the meantime.

If any of these matches you, this guide tells you what’s happening with your monthly rent, why you’re losing 20.42% of it, and how to get a meaningful portion back through proper filing.

2. The Non-Resident Landlord Setup in Japan

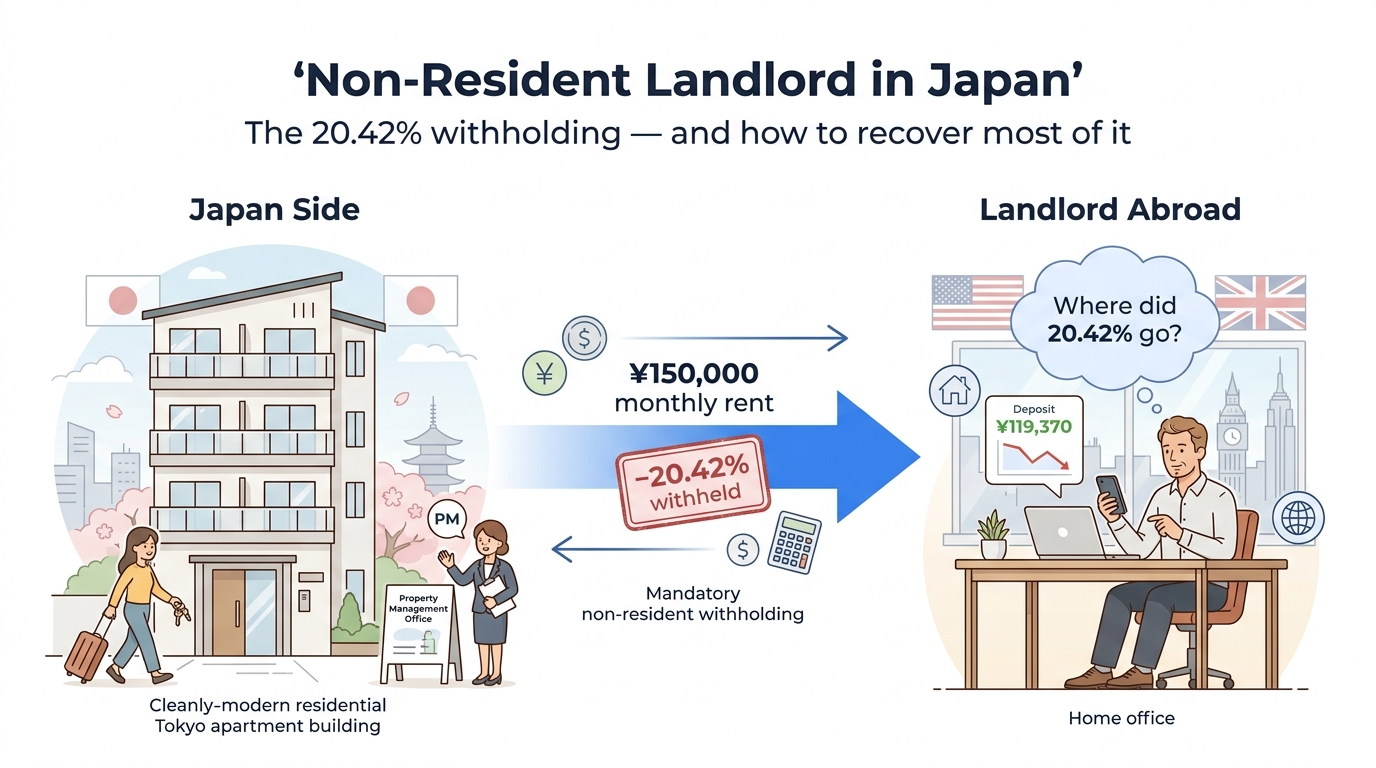

Under Japanese tax law, your rental income from a Japan property is Japan-source income regardless of where you live (Income Tax Act Article 161). This means:

- Japan has the right to tax the income first, before your home country considers it.

- Because you’re a non-resident, the default mechanism is withholding at source at 20.42% of gross rent — the tenant or PM is required by law to withhold and remit.

- You can file a Japan tax return to compute your actual tax liability on net income (gross rent minus deductible expenses) and claim a refund of the over-withheld portion.

The 20.42% rate explained

The withholding rate is composed of:

- 20% national income tax on Japan-source income for non-residents

- 0.42% reconstruction surtax (2.1% applied to the 20% base), in force through December 31, 2037

Total: 20.42% of the gross rent paid to a non-resident landlord. This is mandatory and applies whether the property is held individually, jointly, or through a foreign entity — though entity structures change the mechanics slightly.

When withholding doesn’t apply

There is a narrow exception: if the tenant is an individual who rents the property for their own residential use (not for business), the tenant is not required to withhold. This applies for many single-tenant residential rentals — but most landlords use a PM, which is itself a corporate entity that does have the withholding obligation.

In practice, almost all non-resident landlords with a PM-managed Japan property experience the 20.42% withholding.

3. The 20.42% Withholding on Japan Rent: How It Works

The mechanics of the monthly withholding are simple in form, surprising in impact.

The flow each month

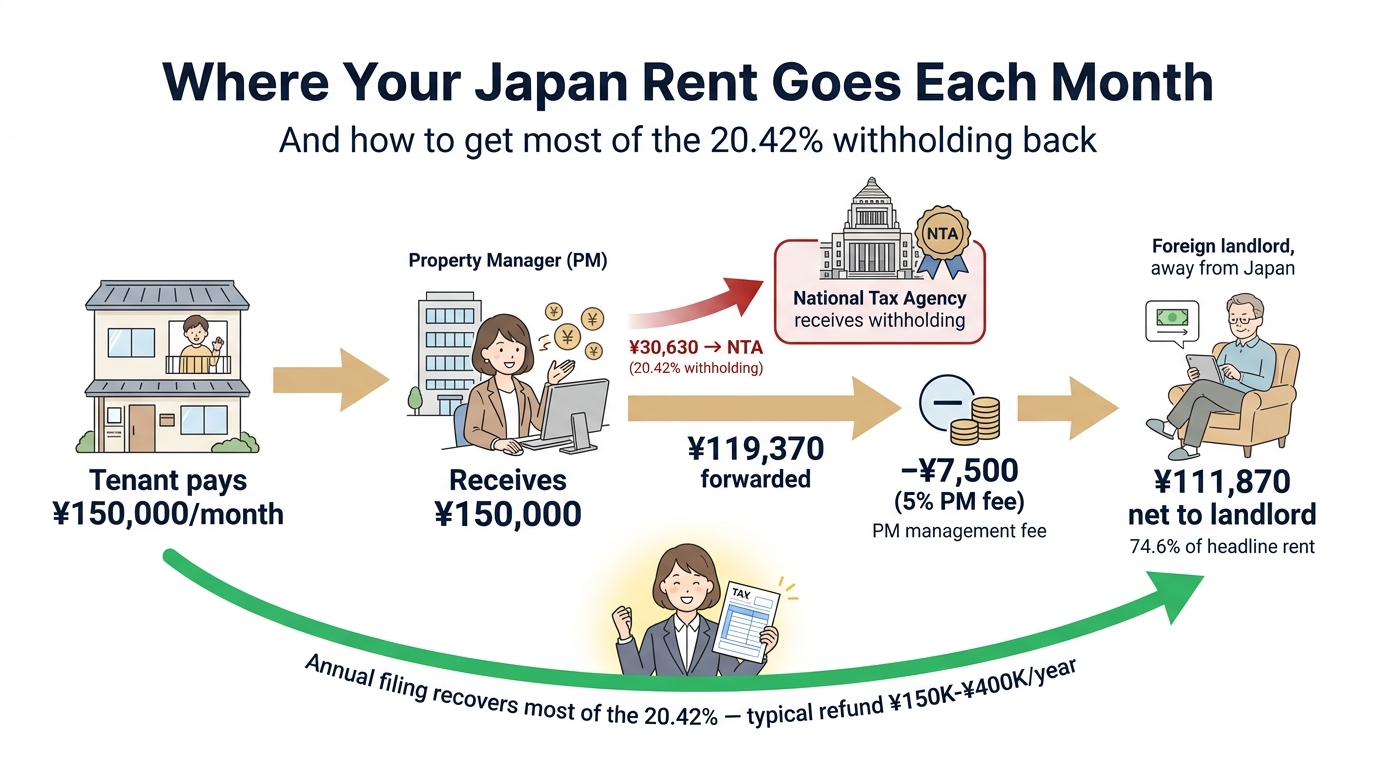

- Tenant pays full rent to your Property Manager (PM). Let’s say ¥150,000/month.

- PM withholds 20.42% of the gross rent. That’s ¥30,630 in the example.

- PM remits the withholding to the local tax office by the 10th of the following month.

- PM deducts their management fee (typically 5–8% of rent + admin fees).

- PM transfers the remaining amount to your designated bank account — Japan-based or overseas.

So for a ¥150,000 monthly rent with a 5% PM fee:

| Item | Amount |

|---|---|

| Gross rent | ¥150,000 |

| 20.42% withholding | −¥30,630 |

| PM fee (5%) | −¥7,500 |

| Net to landlord | ¥111,870 |

That’s roughly 74.6% of the headline rent reaching you — before any further tax in your home country.

Why it feels punitive but usually isn’t

The 20.42% withholding is a prepayment, not a final tax. The actual tax owed on rental income — once you deduct legitimate expenses like depreciation, repairs, insurance, mortgage interest, and management fees — is almost always less than 20.42% of gross rent. For most residential rentals at typical Japan price levels, the effective tax rate on net rental income is in the 5–15% range.

The difference between the 20.42% withheld and the actual tax owed is your potential refund — and for many landlords, this is tens to hundreds of thousands of yen per year waiting to be claimed.

4. How to Get the 20.42% Japan Rent Withholding Back

There are two ways to recover the over-withheld portion: annual refund through filing, or up-front reduction through pre-approval.

Method 1: Annual filing and refund

The default path. You file an annual Japanese tax return as a non-resident, compute the actual tax on your net rental income, and claim the difference as a refund. The mechanics:

- Throughout the year, the PM withholds 20.42% on each rent payment.

- By March 15 of the following year, you (through your Tax Representative — see Section 6) file Form B (申告書B) with the rental income schedule.

- The return computes your actual tax based on net rental income.

- The over-withheld amount is refunded to a designated bank account, typically within 4–8 weeks of filing.

For a typical ¥150,000/month rental property, the annual refund often ranges from ¥150,000 to ¥350,000 — meaningful enough to make the filing effort worthwhile.

Method 2: Pre-approved reduced withholding

Less commonly known, but available: you can file a Notification of Reduced Withholding Tax Rate (源泉徴収税額の軽減) in advance, supported by documentation of your expected net taxable income. If approved, your PM withholds at a lower rate going forward.

The trade-offs:

- Pro: cash flow benefit — you receive more rent each month, rather than waiting until annual filing for the refund.

- Con: requires upfront documentation, NTA approval (not automatic), and conservative estimation to avoid penalty if actual tax exceeds reduced withholding.

- Best for: landlords with consistent, well-documented expenses (mortgage, depreciation schedule) and confidence in their numbers.

Most non-resident landlords stick with Method 1 because the refund is reliable and the administrative burden is manageable. Method 2 is useful for those with multiple properties or material cash-flow sensitivity.

The 5-year refund window

If you’ve been a non-resident landlord and never filed, you can claim refunds for past years going back 5 years (Japan’s standard statute for refund claims). For a 5-year ¥150K/month property, this can easily be ¥750,000+ in recoverable refunds.

If you’ve gone longer than 5 years without filing, the older years are forfeit, but the most recent 5 are still claimable. Coordinate this through a Tax Representative who handles the back-filing — and be aware that if there’s a chance you also owe additional tax (e.g., capital gains from a sale, or significant net rental income that exceeds withholding), see our Overdue Tax Filing in Japan guide before initiating contact with the NTA.

5. Annual Filing Obligations for Non-Resident Landlords

Whether or not you want to claim a refund, you are technically required to file a Japanese tax return on your rental income if you have any Japan-source income above ¥0. In practice, the NTA does not aggressively pursue non-filers who are net-overwithheld (i.e., you’re owed money) — but they will if your actual tax exceeds the withholding.

The annual filing in detail

- Form: Shinkokusho B (申告書B), with the property income schedule

- Deadline: March 15 of the following year (e.g., 2026 rental year → March 16, 2027)

- Filing channel: Through your Tax Representative, since you cannot file from abroad without representation

- Currency: JPY only — convert any foreign-currency expenses using the date-of-transaction TTM rate

What goes on the return

For each rental property:

- Gross rental income for the calendar year

- Allowable expenses (see Section 7 for the full list)

- Depreciation based on building value and statutory useful life

- Net taxable income = gross − expenses − depreciation

- Tax calculation at non-resident rate (currently flat 20% national tax + 2.1% surtax = 20.42% applied to net income, with some progressive variation for high-income cases)

- Credit for withholding already paid by the PM during the year

- Refund or balance owed: typically a refund for residential properties at modest rents

Residence tax — typically zero for non-residents

Unlike Japan-resident landlords, non-resident landlords do not owe Japan residence tax (住民税) since residence tax is based on Japan residency on January 1 of the tax year. This is a meaningful saving — Japan residence tax is roughly 10% of taxable income, so non-resident landlords pay less total tax than resident-landlords on the same property income.

6. Tax Representative (Nozei Kanrinin) — Required From Day 1

If you do not have a Japan residence registered with your municipal office, you cannot interact with the NTA directly. You must appoint a Tax Representative (Nozei Kanrinin / 納税管理人) — a Japan-resident individual or firm who acts as your formal interface with the tax office.

What the Tax Representative does

- Files your annual rental income tax return

- Receives all NTA correspondence on your behalf (including determinations, audits, refund notices)

- Coordinates with your PM on tax-related matters

- Handles any back-filing for prior years if you start filing late

- Manages communication in Japanese — you do not need to speak Japanese yourself

A Tax Representative is not legally responsible for your tax liability — you remain the taxpayer. The representative is purely an administrative agent. The same Tax Representative concept appears in other contexts, including the pension lump-sum refund and overdue tax cleanup scenarios.

Who can be your Tax Representative?

- An individual resident in Japan (a friend, family member, or trusted associate)

- A licensed Japanese tax accountant (zeirishi) — by far the more practical choice for ongoing rental income

- A tax accounting firm (corporate Tax Representative)

For most non-resident landlords, engaging a bilingual zeirishi as Tax Representative is the standard approach. Annual fees for a typical single-property arrangement run ¥80,000–¥200,000/year depending on complexity, often comparable to the refund itself in the first year and net-positive thereafter.

The appointment procedure

- Complete the Nozei Kanrinin no Todokede-sho (Notice of Tax Representative Appointment) — Form 18

- Submit to the tax office covering your last Japanese address (or the property’s location, if you never had a Japan address)

- Effective immediately upon NTA receipt — no review process

If you appointed a Tax Representative before leaving Japan, you’re already set up. If not, you can appoint one at any time from abroad — most bilingual zeirishi handle the appointment as part of their onboarding.

7. Allowable Deductions for Japan Rental Income

The 20.42% withholding is on gross rent — but your actual tax is on net taxable income after legitimate expenses. The bigger your deductible expenses, the bigger your refund. Common allowable expenses:

| Expense Category | Notes |

|---|---|

| PM fees | Monthly management fees, leasing fees, renewal fees |

| Property tax (固定資産税) | Annual ~1.4% of assessed property value |

| City planning tax (都市計画税) | Annual ~0.3% of assessed value (urban properties) |

| Building depreciation | Statutory useful life schedule applies (concrete: 47 yrs new; wood: 22 yrs new; depreciable balance only) |

| Mortgage interest | Only the interest portion is deductible, not the principal repayment |

| Insurance premiums | Fire, earthquake, liability insurance |

| Repairs and maintenance | Routine repairs, periodic painting, plumbing |

| Common area fees | Condo management fees, repair fund contributions |

| Tax Representative fee | The fee you pay your zeirishi is itself deductible |

| Travel to Japan (limited) | For property inspection, repairs, tenant matters — must be specifically for the rental business, with documentation |

The depreciation deduction — often the largest item

For a residential property with significant building value (vs. land), depreciation alone can offset most of your rental income for the first 5–15 years of ownership. A simplified example:

- Property purchase: ¥40,000,000 (land: ¥15M, building: ¥25M)

- Building useful life (reinforced concrete, used at 10 years old): ~37 years remaining

- Annual depreciation: ¥25M / 37 ≈ ¥676,000/year

If your annual rent is ¥1.8M and your other expenses sum to ¥600K, your net taxable income is roughly ¥520K (¥1.8M − ¥676K depreciation − ¥600K other), and the actual tax is ~¥106K — vs. ¥367K withheld at 20.42%. Refund: ~¥261K.

What’s NOT deductible

- Mortgage principal — only the interest portion

- Land value — land doesn’t depreciate

- Personal travel costs not directly tied to the rental business

- Furniture for personal use if the property is partially personal-use

- Expenses for a different rental property if you have multiple (each property’s books must be kept separately)

8. Capital Gains If You Sell the Property

When you eventually sell your Japan rental property, a separate set of tax rules applies — capital gains tax on the sale, alongside any rental income tax for the partial year you held the property.

The basic structure

Capital gains on Japan real estate are taxed as separated income at flat rates (not combined with ordinary income):

| Holding Period | Tax Rate (Non-Resident) |

|---|---|

| 5 years or less (short-term) | 30.63% (30% income + 0.63% reconstruction) |

| Over 5 years (long-term) | 15.315% (15% income + 0.315% reconstruction) |

The holding period is measured by January 1 of the year of sale, not by actual calendar months. This “January 1 Rule” trips up many sellers — selling on December 31, 2030 of a property bought January 2, 2025 is treated as ~5 years − 1 day, triggering the short-term rate. Wait one more day (sell January 1, 2031) and you save approximately half the tax.

Withholding on sale proceeds

When a non-resident sells a Japan property, the buyer is required to withhold 10.21% of the sale proceeds and remit to the NTA. This is creditable against your actual capital gains tax on the annual return.

Calculation example

You bought the property in 2020 for ¥40M, are selling in 2026 for ¥48M, and have ¥3M of accumulated depreciation:

- Sale price: ¥48M

- Adjusted cost basis: ¥40M − ¥3M depreciation = ¥37M

- Capital gain: ¥11M

- Tax at 15.315% long-term: ~¥1.68M

- Buyer’s withholding (10.21% of ¥48M): ¥4.9M

- Refund: ¥3.22M

The “withholding much larger than actual tax” is structural — buyers withhold on gross proceeds, but tax is on net gain. Always file the post-sale return to claim the refund.

For depreciation recapture mechanics and entity-structure optimization, see our Foreign Investors Real Estate Tax guide. Also relevant: the broader Capital Gains Tax in Japan framework.

9. Common Non-Resident Landlord Mistakes

Not filing annual returns

The most common — and most expensive — mistake. Non-resident landlords frequently assume that “the PM is already withholding tax, so I’m done.” That’s wrong: the 20.42% is a prepayment, not a final tax. By not filing, you’re voluntarily overpaying tax to the Japanese government. Annual refunds typically run ¥150K–¥400K per property at typical rents.

Not appointing a Tax Representative before leaving

If you left Japan without appointing a Nozei Kanrinin, your relationship with the NTA is in administrative limbo until you fix it. Tax notices may be sent to your old Japan address (and ignored), your PM may not know how to handle audit inquiries, and your refund claim cannot be processed.

Missing depreciation deductions

Many self-filers focus on cash expenses (PM fees, repairs) and forget depreciation — typically the largest single deduction. A property accountant routinely captures this; a tenant trying to DIY often does not. The depreciation deduction is often the difference between a small refund and a meaningful one.

Mixing personal and rental property records

If you visited Japan and stayed in the property briefly (between tenants, or while doing repairs), you cannot deduct expenses for those days as rental expense. Keep clear records of any personal-use days; mixed-use property reporting is significantly more complex than pure rental.

Currency conversion errors

Rent is paid in JPY, but if you’re filing from abroad, your records may be in another currency. Use the date-of-transaction TTM rate for each transaction, not a year-end snapshot rate. NTA accepts a year-average rate for relatively stable currencies but documentation is needed.

Ignoring home-country tax obligations

Your home country likely also taxes the Japan rental income (subject to treaty relief). US citizens, for example, must report worldwide rental income on Form 1040, with the Japan tax serving as a Foreign Tax Credit. See our US-Japan Tax Treaty guide for the credit mechanics.

10. Frequently Asked Questions

Do I need to file a Japan tax return if my PM already withholds 20.42%?

Yes — technically required, and almost always financially beneficial. The 20.42% withholding is a prepayment, not a final tax. The actual tax on your net rental income (after deducting expenses and depreciation) is usually 5–15% of gross, meaning you’re owed a refund of the difference. Annual refunds typically run ¥150,000–¥400,000 per property at typical Japan rental levels.

How far back can I claim withholding refunds I never filed for?

Japan’s statute of limitations for refund claims is 5 years. If you’ve been a non-resident landlord for 10 years and never filed, you can claim refunds for the most recent 5 years; earlier years are forfeit. For a typical ¥150K/month property, 5 years of unclaimed refunds can easily be ¥750K–¥2M in recoverable money.

Can I be my own Tax Representative if I’m based abroad?

No. By definition, a Tax Representative (Nozei Kanrinin) must be a Japan resident. The role exists precisely because non-residents cannot directly interface with the NTA. You can appoint a friend, family member, or — most commonly — a bilingual Japanese tax accountant to serve as your representative.

What if I sell my Japan property — is the withholding the same?

Different mechanism. For the sale, the buyer withholds 10.21% of sale proceeds (not 20.42%), remitting to the NTA. Your actual tax is 15.315% on the net capital gain (if held over 5 years) or 30.63% (if 5 years or less). You file a separate capital gains return to true up the tax and typically receive a meaningful refund of the over-withholding.

Does my home country also tax this rental income?

Generally yes, depending on residency-based taxation in your home country. Most OECD countries tax worldwide income for residents, including foreign rental income. The Japan tax you pay can typically be credited against home-country tax through a Foreign Tax Credit (US: Form 1116). The combined effective tax is roughly the higher of the two countries’ rates.

Can I avoid the 20.42% withholding entirely?

There are two paths: (1) file a Notification of Reduced Withholding to get the PM to withhold less, supported by your expense documentation, or (2) restructure the holding via a Japan corporate entity (GK-TK or similar) — but this is only sensible at scale. For a single-property landlord, the annual filing-and-refund route is simpler and usually fully sufficient.

I haven’t filed in years — should I worry?

If you’ve been over-withheld (which most residential rental landlords are), filing is purely upside — you’ll receive refunds for the past 5 years. If your actual tax would have exceeded withholding (rare for residential rentals, possible for high-yield commercial), the cleanup is more complex and you should review our Overdue Tax Filing guide. Either way, a bilingual tax accountant can scope the situation in 30 minutes.

What documentation should I keep for my Japan rental?

PM monthly statements (showing gross rent, withholding, fees, net), annual PM summary, property tax notices, mortgage statements (separating interest vs principal), insurance policies, all repair and maintenance receipts, and your original property purchase documents with the land-vs-building allocation. Your Tax Representative will need a complete year’s package by January-February for the March 15 filing.

11. Get Expert Help With Japan Rental Tax

Non-resident landlording in Japan is one of those situations where the right professional support pays for itself in year one. The 20.42% withholding compounds month by month, and most landlords leave significant money on the table simply because they don’t file.

The right time to engage a Tax Representative is before you leave Japan (if you’re still here and planning to keep a rental property) — or immediately upon realizing you’ve been over-withheld (if you’ve already left). Either way, the typical first-year refund pays for several years of Tax Representative fees.

TaxMatch Japan matches you with bilingual zeirishi who specialize in non-resident rental income and back-filing for past-due refunds. Initial consultations are free; matching takes 1–2 business days.

Related Guides

Foreign Investors Real Estate Tax

Multi-property portfolios, GK-TK, depreciation hacks, exit strategies

Leaving Japan Tax Checklist

Set up your rental before departure — including the Tax Representative

Capital Gains Tax in Japan

When you sell the property — long-term vs short-term, the January 1 rule

Overdue Tax Filing

If you also owe past Japan tax beyond rental — cleanup strategy

Stop overpaying 20.42% on your Japan rent.

TaxMatch Japan matches you with a bilingual Tax Representative — annual refunds typically pay the first year’s fee several times over.

Get Matched with a Tax Representative →

Or message us directly on WhatsApp