You’re a US citizen or Green Card holder living in Japan, and you’ve just realized — through a tax accountant, a friend’s panic story, or a cold IRS letter — that you should have been filing US tax returns every year since you moved abroad. The good news: the IRS has a specific program designed for exactly your situation. The Streamlined Foreign Offshore Procedures (SFOP) allows non-willful non-compliant Americans abroad to catch up on US filings with no penalties. The bad news: the eligibility bar is real, and one wrong move during the catch-up process can disqualify you.

This guide walks you through the Streamlined program specifically as it applies to Americans living in Japan: who qualifies, what to file, how the “non-willful” certification works, the step-by-step process, and the common pitfalls that derail otherwise-clean cases.

Important Notice

This article is for general informational purposes only and does not constitute tax, legal, or financial advice. Streamlined procedures involve substantive IRS rules and individual fact patterns vary significantly. Always engage a qualified US tax attorney or CPA experienced with Streamlined cases before initiating the program — mistakes are difficult to reverse once filed.

Behind on US tax filings while in Japan?

Get matched with a Streamlined-experienced US tax professional — free.

Table of Contents

- Who Should Use Streamlined Filing in Japan?

- What Is the Streamlined Foreign Offshore Procedure?

- Eligibility: The Non-Willful Standard

- What You’ll File: 3 Tax Returns + 6 FBARs

- The Non-Willful Certification (Form 14653)

- Streamlined vs. Standard Late Filing: The Cost Comparison

- The Streamlined Filing Process: Step-by-Step

- After Streamlined: Staying Compliant Going Forward

- Common Streamlined Filing Pitfalls

- Frequently Asked Questions

- Get Expert Help With Streamlined Filing

1. Who Should Use Streamlined Filing in Japan?

You should read this guide if all of the following describe your situation:

- You are a US citizen or Green Card holder (the obligation follows citizenship/permanent residency, regardless of where you live).

- You have been living outside the United States, including Japan, for at least 3 years (the program requires meeting the non-residency test for at least 3 of the 6 prior tax years).

- You have not filed US tax returns and/or FBARs for 3 or more recent years, despite having an obligation to do so.

- Your failure to file was non-willful — i.e., due to negligence, inadvertence, mistake, or a good-faith misunderstanding (not intentional concealment or tax evasion).

- You are not currently under IRS audit or criminal investigation for any tax matter.

The typical Streamlined candidate in Japan

The most common Streamlined candidates we see among Japan residents:

- The “I didn’t know I had to file” American — moved to Japan in their 20s or 30s, settled in, never realized US citizens must file globally regardless of residency.

- The Green Card holder who left — emigrated to Japan, kept the Green Card “just in case,” didn’t realize that retaining LPR status carries continuing US tax obligations.

- The “I tried but stopped” American — filed for a year or two, found it overwhelming, gave up, didn’t realize stopping creates more problems than starting over.

- The accidental American — born in the US to non-US parents, left as an infant, raised in Japan, only learned about the obligation as an adult applying for a Japan job that asked about US tax compliance.

If any of these matches your situation — and you weren’t deliberately hiding income from the IRS — Streamlined is almost certainly the right path. If you’re not sure whether your situation qualifies as non-willful, do not proceed without consulting a US tax attorney first; the certification you sign is under penalty of perjury, and getting it wrong has serious consequences.

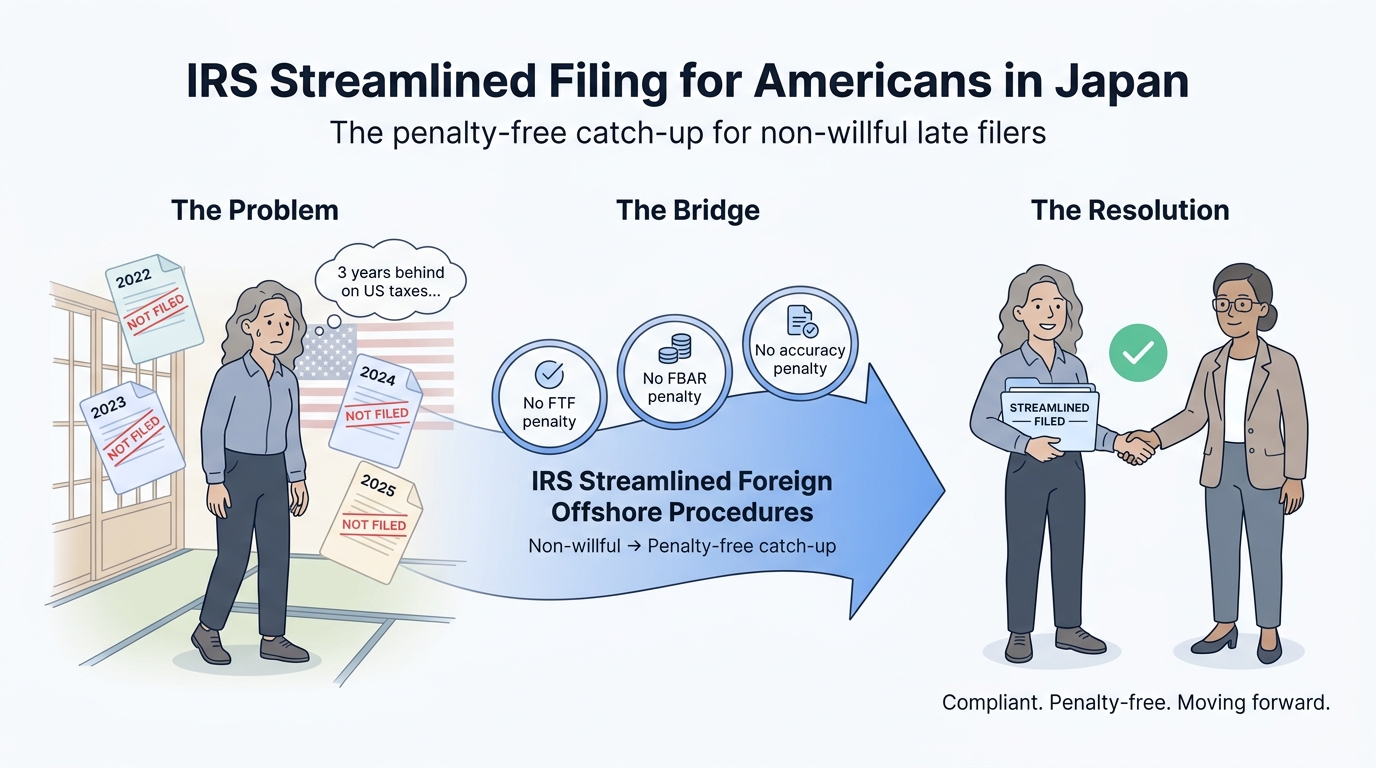

2. What Is the Streamlined Foreign Offshore Procedure?

The Streamlined Foreign Offshore Procedure (SFOP) is one of two Streamlined Filing Compliance Procedures the IRS offers (the other is the Streamlined Domestic Offshore Procedure, for non-residents abroad less than the threshold). For US citizens and GC holders living in Japan who meet the criteria, SFOP is the applicable program.

The procedure offers four major concessions for non-willful late filers:

| Streamlined Concession | Standard Late Filing |

|---|---|

| No failure-to-file penalty | 5% per month up to 25% |

| No failure-to-pay penalty | 0.5% per month up to 25% |

| No accuracy-related penalty | 20% of underpayment |

| No FBAR penalty | $10,000+ per non-willful year, or 50% of account balance for willful |

| Only file 3 years of late returns | All open years (6 with substantial omission, indefinite for fraud) |

| Only file 6 years of late FBARs | 6 years standard |

| Pay only actual back tax + interest | Plus all of the above penalties |

The catch: you must certify under penalty of perjury that your failure to file was non-willful. The IRS reserves the right to audit any Streamlined submission and reject it post hoc if they determine willfulness. A rejected submission has worse consequences than not having filed Streamlined in the first place.

3. Eligibility: The Non-Willful Standard

The single most important eligibility criterion — and the one most often misunderstood — is the non-willful standard. The IRS’s definition:

“Non-willful conduct is conduct that is due to negligence, inadvertence, or mistake or conduct that is the result of a good faith misunderstanding of the requirements of the law.”

What clearly qualifies as non-willful

- You honestly didn’t know US citizens must file globally (most common case)

- You misunderstood treaty positions or which forms applied to you

- You relied in good faith on incorrect professional advice

- You were aware of US filing obligations but believed you had no income/below threshold (and were honestly wrong about that)

- You couldn’t access US tax forms or didn’t know how to file from abroad

What does NOT qualify as non-willful

- You knew you had a filing obligation and chose to ignore it

- You actively concealed foreign accounts, used nominee structures, or moved assets to avoid disclosure

- You received a US tax notice and didn’t respond

- You filed in some years but deliberately omitted certain accounts or income

- You had a US tax professional and lied to them about foreign accounts

The gray area: “I sort of knew but didn’t really act on it”

The grayest cases are people who had a vague awareness that something was required but didn’t pursue it. The IRS treats these with nuance — and a good US tax attorney will help you frame your facts honestly. If your gut says “I knew, I just didn’t deal with it,” consult an attorney before assuming Streamlined applies. The alternative — Voluntary Disclosure Practice (VDP), with much heavier penalties but greater protection — may be more appropriate.

The 3-year non-residency requirement

Beyond non-willfulness, you must meet the non-residency test: in at least 3 of the most recent 6 tax years for which the due date has passed, you were either:

- Not a US resident under the substantial presence test (less than 35 days in the US during the year), OR

- A bona fide foreign resident with the requisite intent to remain abroad indefinitely

For Americans living in Japan on long-term visas (Spouse, PR, Highly Skilled Professional, Work, etc.) who don’t make extended US visits, this test is easily satisfied. The main trip-up: spending extended time in the US during recent years can disqualify you.

4. What You’ll File: 3 Tax Returns + 6 FBARs

Streamlined requires filing for a specific catch-up window — not your entire missing history. The window is shorter than standard late-filing, which is one of the program’s main benefits.

The 3 most recent tax years (Form 1040 + schedules)

You file complete Form 1040 returns for the 3 most recent tax years for which the due date has passed. As of mid-2026, these are tax years 2023, 2024, and 2025.

Each return includes:

- Form 1040 (main return) — see our Tax Filing Guide for the parallel Japan-side return

- Schedule A, B, C, D, E as applicable

- Form 2555 (Foreign Earned Income Exclusion) OR Form 1116 (Foreign Tax Credit) — see our FEIE vs FTC decision guide

- Form 8938 (Statement of Specified Foreign Financial Assets) if you exceed thresholds

- Form 8621 for any Passive Foreign Investment Companies (PFICs) — be very careful if you hold any Japanese mutual funds or investment trusts

- Any other applicable international information forms (Form 5471 for foreign corporations, 8865 for partnerships, 3520 for foreign trusts/gifts)

The 6 most recent FBARs (FinCEN Form 114)

You file 6 years of late FBARs. For 2026 submission, this means calendar years 2020 through 2025. Each FBAR lists every foreign financial account (bank, brokerage, retirement) where the aggregate of all your accounts exceeded $10,000 at any point during the year. For comprehensive FBAR mechanics, see our FBAR Filing Guide for US Citizens in Japan.

Required certifications and attachments

- Form 14653 — the Streamlined Foreign Offshore Certification (see Section 5)

- Personal narrative explaining the non-willful reasons in detail

- Identification statement noting “Streamlined Foreign Offshore” on the top of each return

- Tax payment — you pay any tax actually owed (plus interest), but no penalties

5. The Non-Willful Certification (Form 14653)

Form 14653 is the heart of the Streamlined submission. You sign it under penalty of perjury, certifying that your failure to file was non-willful. The form requires a detailed narrative — typically 2-5 pages — explaining:

- Your background and how you came to live in Japan

- Your understanding (or lack thereof) of US tax filing obligations during the non-filing years

- How and when you became aware of the obligation

- What steps you took once you became aware

- Specific facts supporting that your conduct was non-willful

What a strong narrative looks like

Effective non-willful narratives:

- Are specific — name dates, locations, conversations, advisors

- Are chronological — walk through the period of non-compliance in order

- Explain why you didn’t know in concrete terms (not just “I didn’t know”)

- Describe the moment of realization — the conversation, the article, the tax notice

- Demonstrate good faith going forward — engaging counsel, gathering records, filing promptly upon discovery

What kills a narrative

- Vague claims (“I always thought it wasn’t required”)

- Inconsistencies with the financial records (you claim ignorance but had a US tax attorney listed in old emails)

- Indications that you were aware but chose not to act

- References to “advice” from non-attorneys who don’t qualify as authoritative sources

- Boilerplate language that suggests it was drafted by a service rather than personalized to your situation

The narrative is the single most-reviewed document in a Streamlined submission. Have an attorney draft it (or at least review yours) — not a generic CPA who handles standard returns.

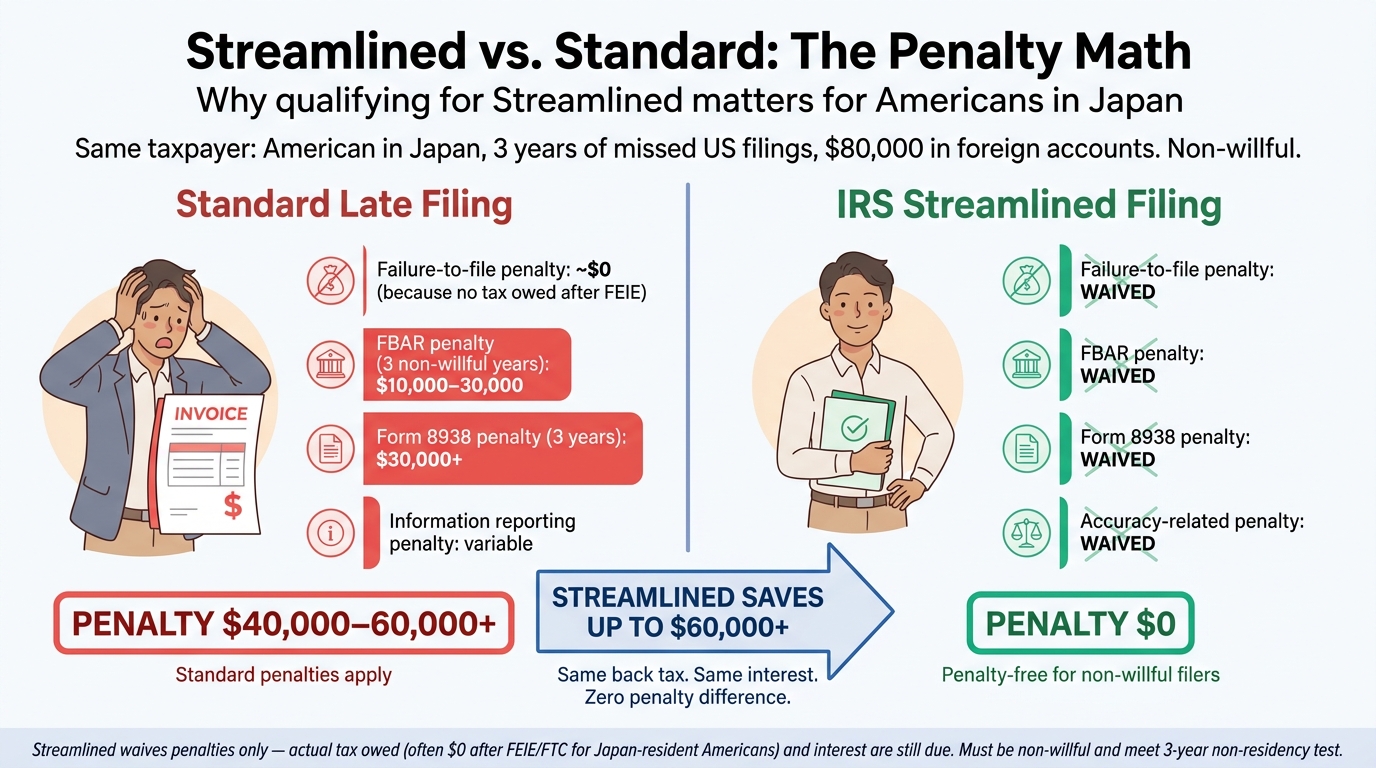

6. Streamlined vs. Standard Late Filing: The Cost Comparison

To make the value of Streamlined concrete, consider a representative American in Japan: salary equivalent of $120,000/year, three years late on US filings, foreign account balances around $80,000 average, no fraudulent intent — the typical “I just didn’t know” case.

| Penalty Category | Standard Late Filing | Streamlined |

|---|---|---|

| 3 years of tax owed (after FEIE/FTC) | ~$0 (covered by FTC) | ~$0 (same) |

| Failure-to-file penalty (3 years) | ~$0 (no tax owed) | $0 |

| FBAR penalty (3 unfiled years, non-willful) | $10,000–30,000 | $0 |

| Form 8938 penalty (3 unfiled years) | $10,000+ per year × 3 = $30,000+ | $0 |

| Information reporting penalty exposure | Variable, potentially significant | $0 |

| Interest on any tax owed | Applies | Applies |

| Estimated total | $40,000–60,000+ | ~$0 |

The math is rarely close. Even cases where actual back tax is meaningful (e.g., investment income exceeded FEIE), Streamlined saves tens of thousands in penalty exposure on the information-reporting side alone. For most Americans in Japan in this situation, the only question is whether they qualify — not whether to use it.

7. The Streamlined Filing Process: Step-by-Step

The full process typically runs 3-6 months from engaging counsel to mailing the complete package. The phases:

Phase 1: Engagement and document gathering (4-8 weeks)

- Engage a US tax attorney or CPA experienced specifically with Streamlined cases — not a general expat tax preparer

- Sign engagement letter; receive document request list

- Gather: W-2s, 1099s if any, foreign income summaries, full account histories for all foreign accounts (the bank-by-bank reconstruction is the most time-consuming step)

- Obtain Wage and Income Transcripts from the IRS for the catch-up years to ensure nothing US-source was missed

- Reconstruct US tax positions: did you owe under FEIE? Were there missed FTC carryforwards? Any PFIC exposure?

Phase 2: Return preparation (4-6 weeks)

- Prepare the 3 most recent year Form 1040s, with all required schedules and international forms

- Calculate any actual tax owed (often $0 or small after FEIE/FTC)

- Prepare the 6 years of FBARs separately

- Draft the personal narrative for Form 14653

- Review for consistency across all years — narrative facts must match return positions

Phase 3: Submission (1-2 weeks)

- Mail the complete package (3 tax returns + Form 14653 + supporting documents) to the IRS Streamlined unit in Austin, TX

- E-file or submit the 6 years of FBARs through the BSA E-Filing System

- Pay any actual tax owed and interest by check or electronic payment

- Retain copies of everything for at least 7 years

Phase 4: Aftermath (6-18 months)

After submission:

- The IRS reviews the package; processing typically takes 3-9 months

- You receive no formal “acceptance” letter — the absence of a follow-up audit is the acceptance signal

- If the IRS has questions, they request additional information by mail

- Rejection rate is low (<5% for properly prepared submissions), but does happen — usually due to incomplete records or narratives that suggest willfulness

You should resume normal annual filing for tax year 2026 and beyond, starting with the next due date after your Streamlined submission.

8. After Streamlined: Staying Compliant Going Forward

Streamlined is a one-time fix. To avoid needing it again, you must maintain annual US compliance from this point forward.

The ongoing US obligations for Americans in Japan

- Annual Form 1040 — due April 15, auto-extended to June 15 for residents abroad, further extendable to October 15 with Form 4868

- Annual FBAR (FinCEN 114) — due April 15, auto-extended to October 15

- Annual Form 8938 if asset thresholds exceeded — filed with Form 1040

- Form 8621 each year for any PFIC holdings — easier to avoid than to file

- State tax obligations if you maintain state residency in CA, NY, NJ, or other “sticky” states — see our US Employer Remote Work guide for state tax mechanics

The discipline of expat tax

The Americans who stay compliant share three habits:

- They engage the same bilingual US tax professional every year, even when their situation feels stable

- They track all foreign accounts in real time, including peak balances during the year (not just year-end)

- They avoid the easy traps — no Japanese mutual funds, no NISA accounts as a US citizen, no informal trust structures

If you also have unfiled Japan-side returns (typically required if you’ve had Japanese employer or sole-proprietor income), address those separately through the Japan Overdue Tax Filing process. The two cleanups are independent but often appear in the same client situation.

9. Common Streamlined Filing Pitfalls

Underestimating the document reconstruction effort

Gathering complete account histories for 3-6 years across Japanese banks, brokerages, retirement accounts (including JP Post), and any foreign accounts in your home country is by far the longest phase. Start early. Japanese banks can take 2-4 weeks to provide historical statements; some only retain 5-7 years of records.

Using a generic CPA instead of a Streamlined specialist

Streamlined is a niche area. A general expat CPA may have filed a few. A Streamlined-specialist attorney or CPA has filed hundreds and knows the IRS reviewer expectations, the narrative templates that work, the PFIC traps to spot, and the warning signs of willfulness. The difference in outcome quality is significant; the price difference is usually 30-50% on the engagement fee — well worth it.

Forgetting state tax

Streamlined addresses only federal US tax. If your last US state of residence taxes worldwide income (CA, NY, NJ, MA, VA), you may have parallel state filings due. Some states accept federal Streamlined-style relief; others do not. Discuss this explicitly with your attorney.

PFIC holdings discovered mid-process

Japanese mutual funds, investment trusts, certain insurance products, and even some NISA holdings are PFICs under US law. If you discover PFIC holdings mid-Streamlined, the disclosure obligation triggers Form 8621 — and the tax treatment can be punitive (mark-to-market or excess distribution regime). Often the cleanest move is to divest PFICs immediately upon discovery and report the holdings only for the years they existed, but this is a fact-specific call.

Filing too quickly without legal review

Some online services advertise “DIY Streamlined for $X.” Resist. A non-attorney service cannot give you legal opinion on non-willfulness, cannot defend the certification under penalty of perjury, and cannot represent you if the IRS rejects the submission. The downside of a botched Streamlined far exceeds the cost of proper representation.

Continuing the same patterns post-Streamlined

The IRS reviews Streamlined submissions with an eye to whether the taxpayer has corrected the underlying behavior. If you file Streamlined in year X and then fail to file in year X+1, that’s evidence the non-willfulness claim was suspect. Set up ongoing compliance immediately.

10. Frequently Asked Questions

Can I do Streamlined Filing myself, or do I need a professional?

Technically yes, but practically no. The Form 14653 non-willful certification is signed under penalty of perjury, and the narrative drafting requires legal judgment about what constitutes non-willful conduct. A botched submission can be worse than not filing Streamlined at all. Engage a US tax attorney or CPA with specific Streamlined experience — typically a $5,000–$15,000 engagement that easily pays for itself in penalty avoidance.

What if my failure to file was actually willful?

Streamlined is not the right path. Filing a Streamlined submission with a willful failure can constitute false certification, which is a criminal offense. Instead, consider the IRS Voluntary Disclosure Practice (VDP), which provides much greater protection for willful cases but at significantly higher cost. A US tax attorney is essential to evaluate which program applies.

Do I have to pay back taxes through Streamlined?

Yes — Streamlined waives penalties, not the underlying tax. You pay any actual tax owed for the 3 catch-up years (often near zero after FEIE/FTC for Americans in Japan), plus interest at the IRS underpayment rate. The penalty waiver is the major value.

Can I use Streamlined if I owe Japan taxes too?

Streamlined addresses only US filings. If you also haven’t filed Japanese returns (kakutei shinkoku), that’s a separate Japan-side cleanup — see our Overdue Tax Filing in Japan guide. The two procedures are independent but often appear together in client situations. Address both, ideally in parallel through coordinated US+Japan tax counsel.

How long does Streamlined take from start to finish?

Engagement to mailed submission: typically 3–6 months. IRS processing and silent acceptance: another 6–18 months. So the full timeline is 9–24 months from when you decide to act. The longest delay is usually gathering complete foreign account records, not the IRS side.

Will Streamlined hurt my future US citizenship/immigration?

Streamlined is specifically designed to be a path back to compliance without immigration consequences for non-willful taxpayers. The certification does not affect citizenship or residency status. By contrast, willful tax evasion can affect status of residence. Streamlined is a clean record-clearing mechanism.

What if I’m only missing 1-2 years of US filings, not 3+?

Streamlined still requires the 3-year non-residency lookback and the 3-year tax return catch-up. If your gap is shorter, you may be eligible to simply file the missing years late through the standard process, often with no penalty due to the IRS’s general policy of waiving FTF/FTP penalties when no balance is due. Discuss with a CPA — Streamlined isn’t always the right tool.

Can my spouse and I file Streamlined together?

Each spouse files their own Form 14653 with their own narrative. Joint Form 1040 returns may be filed for the catch-up years (the typical case for married Americans), but each spouse’s non-willful certification is individual. Both must meet eligibility criteria independently.

11. Get Expert Help With Streamlined Filing

Streamlined Filing is one of the few US tax programs where doing it right the first time matters more than the speed of filing. A well-prepared submission goes through with no follow-up; a rushed or DIY submission can derail into months of correspondence or — worst case — outright rejection that puts you in a worse position than where you started.

The right time to engage is as soon as you realize you have a multi-year gap. The IRS has shown no indication of phasing out Streamlined, but the option is at the IRS’s discretion and could be modified or withdrawn in the future. Acting while the program is available is materially safer.

TaxMatch Japan matches you with US-credentialed tax attorneys and CPAs with specific Streamlined Foreign Offshore experience, including coordination with Japan-side cleanup when both are needed. Initial consultations are free; engagement timelines and fees vary by complexity.

Related Guides

US Employer Remote Work in Japan

Ongoing US-Japan dual tax filing for Americans with US employers

FBAR Filing for US Citizens

The $10K trigger, what to report, the form mechanics

US-Japan Tax Treaty Guide

Treaty positions, FTC mechanics, saving clause

Japan Overdue Tax Filing

If you also missed Japan-side filings — the parallel cleanup

3 missed years. 6 missed FBARs. Zero penalties — if filed correctly.

TaxMatch Japan matches you with Streamlined-experienced US tax attorneys for a confidential first conversation.

Get Matched with a Streamlined Specialist →

Or message us directly on WhatsApp